ACC 707: Audit Assignment 1 - Inventory and Intellectual Property

VerifiedAdded on 2023/06/04

|14

|2930

|289

Homework Assignment

AI Summary

This assignment solution addresses key audit assertions and procedures related to inventory and intellectual property, referencing relevant auditing standards. The assignment begins by analyzing the audit assertions at risk concerning inventory, specifically focusing on valuation and rights and obligations. It then details substantive audit procedures for these assertions, including inventory valuation and establishing ownership. The assignment also explores the requirements of ASA 701, emphasizing the importance of highlighting key audit matters in the auditor's report. The second part of the assignment shifts focus to intellectual property, outlining valuation methods, rights and obligations, and substantive audit procedures. It concludes with a discussion of ASA 701 in the context of intellectual property, highlighting key considerations for auditors. The solution provides a comprehensive overview of auditing practices for both inventory and intellectual property, including the application of relevant auditing standards and procedures.

Audit Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 7th Sep 2018.

1 | P a g e

By student name

Professor

University

Date: 7th Sep 2018.

1 | P a g e

2

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................5

References.................................................................................................................................................10

Audit assertion:

2 | P a g e

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................5

References.................................................................................................................................................10

Audit assertion:

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

It is the responsibility of the management of the company to take it upon himself to make sure

that all the important matters that are detrimental success of the company are properly

highlighted and checked by the auditor. These are known as audit assertions and the aim of these

assertions is to solve issues and put emphasis on the valuation, representation of the data in the

financial statements (Alexander, 2016). There are various categories based on which these

assertions have been divided which includes points like occurrence, completeness, relevance and

obligations. The auditor depends on these assertions to help him in conducting his audit and

identifying those areas in which the chances of risk occurrence is predominantly high. In this

assignment the key audit assertions regarding inventories are stated below and analysed and

presented.

1 a) Key assertions at risk.

AASB 102 deal with disclosure and reporting of inventory for the companies. They need to abide

with this auditing standard .Valuation is a key concept in case of inventories and it is also the key

assertion that should be taken into consideration. In most of the cases inventories are valued by

the companies at cost or net realisable value whichever is lower. It is important to treat wastage

correctly that is associated with inventories. Wastage should not be included in case it is

abnormal wastage while valuation. For goods that are work-in-progress valuation is difficult but

that also becomes easy if proper methods are followed (Arnott, et al., 2017). There are also

chances that the inventory might become redundant and obsolete in the long run if not used at the

right time. In case of Computing Solutions, they are dealing with computer appliances and there

are chances that the inventories might become obsolete because the upgradation in technology is

happening every now and then. Hence it is important to clear the stock as soon as possible. There

are also chances of impairment due to timing involved.

3 | P a g e

It is the responsibility of the management of the company to take it upon himself to make sure

that all the important matters that are detrimental success of the company are properly

highlighted and checked by the auditor. These are known as audit assertions and the aim of these

assertions is to solve issues and put emphasis on the valuation, representation of the data in the

financial statements (Alexander, 2016). There are various categories based on which these

assertions have been divided which includes points like occurrence, completeness, relevance and

obligations. The auditor depends on these assertions to help him in conducting his audit and

identifying those areas in which the chances of risk occurrence is predominantly high. In this

assignment the key audit assertions regarding inventories are stated below and analysed and

presented.

1 a) Key assertions at risk.

AASB 102 deal with disclosure and reporting of inventory for the companies. They need to abide

with this auditing standard .Valuation is a key concept in case of inventories and it is also the key

assertion that should be taken into consideration. In most of the cases inventories are valued by

the companies at cost or net realisable value whichever is lower. It is important to treat wastage

correctly that is associated with inventories. Wastage should not be included in case it is

abnormal wastage while valuation. For goods that are work-in-progress valuation is difficult but

that also becomes easy if proper methods are followed (Arnott, et al., 2017). There are also

chances that the inventory might become redundant and obsolete in the long run if not used at the

right time. In case of Computing Solutions, they are dealing with computer appliances and there

are chances that the inventories might become obsolete because the upgradation in technology is

happening every now and then. Hence it is important to clear the stock as soon as possible. There

are also chances of impairment due to timing involved.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Rights and Obligations

The assertions over rights and obligations over the inventories also happens normally. In this

case we see that most of the inventories are in transit and hence it becomes difficult to ascertain

ownership at some point. In case of Computing Solutions, the company is having a main

warehouse from which they are distributing to eight different locations, hence most of the goods

are in-transit and are held on consignment basis (Belton, 2017). There are also involvement of

different parties like insurance business and consignees and hence it is important that proper

ownership should be established at all stages.

1 b) Substantive Audit procedures.

Substantive audit matters help in gathering audit matters and there is a lot of substantial standing

and they are very useful to the auditor for the comprehensive and substantive information that

matters. It is useful from risk elements side of the auditor and helps in controlling the materiality

element of the company (Choy, 2018). They are divided into substantive audit procedures under

following head which includes: test of control, test of details, analytical procedures etc.

For valuation risk:

For valuation of inventories the auditor needs to understand few things which includes valuation

of the closing inventory, as it is done at the end of the year and only once it is done. There are

high chances that the management can mismanage the fund in this case. Inventory count should

be observed as much as possible and the auditor should closely monitor that in all regards.

Vouching and Verification of inventories is also important for the inventories (Das, 2017). There

are chances that the management can deflate the value of the goods that are in transit and hence

4 | P a g e

Rights and Obligations

The assertions over rights and obligations over the inventories also happens normally. In this

case we see that most of the inventories are in transit and hence it becomes difficult to ascertain

ownership at some point. In case of Computing Solutions, the company is having a main

warehouse from which they are distributing to eight different locations, hence most of the goods

are in-transit and are held on consignment basis (Belton, 2017). There are also involvement of

different parties like insurance business and consignees and hence it is important that proper

ownership should be established at all stages.

1 b) Substantive Audit procedures.

Substantive audit matters help in gathering audit matters and there is a lot of substantial standing

and they are very useful to the auditor for the comprehensive and substantive information that

matters. It is useful from risk elements side of the auditor and helps in controlling the materiality

element of the company (Choy, 2018). They are divided into substantive audit procedures under

following head which includes: test of control, test of details, analytical procedures etc.

For valuation risk:

For valuation of inventories the auditor needs to understand few things which includes valuation

of the closing inventory, as it is done at the end of the year and only once it is done. There are

high chances that the management can mismanage the fund in this case. Inventory count should

be observed as much as possible and the auditor should closely monitor that in all regards.

Vouching and Verification of inventories is also important for the inventories (Das, 2017). There

are chances that the management can deflate the value of the goods that are in transit and hence

4 | P a g e

5

care should be taken to ensure that their valuation is correct. Valuation experts can also be hired

to check the value of inventories.

For rights and obligations

For establishing the rights and ownership it is important that proper agreements should be there

among the company. There should also be agreement with the insurance company on how they

can handle the inventories. It is also important that they must read the consignment letter. The

minutes of the management also needs to be studied as per the management. Thus it is important

that auditors needs to understand the terms of the agreement and should verify it again and again

on timely basis so that the management can be informed in case there are no issues.

1c) As per ASA701, it is important that auditor should state all that matters which they feel are

detrimental for the company and should be stated in the auditors report. Proper matters should be

highlighted so that shareholders should become aware so that management should understand

which are the areas in which they should take charge of (Erik & Jan, 2017). The stakeholders

should also should take notice of which are the areas in which they are highlighted.

In the given case, the annual report of the Woolworths company has been completed and

important steps that has been taken by the company in the valuation and provisioning of the

inventory has been stated in details. An extract from the audit report is given below:

5 | P a g e

care should be taken to ensure that their valuation is correct. Valuation experts can also be hired

to check the value of inventories.

For rights and obligations

For establishing the rights and ownership it is important that proper agreements should be there

among the company. There should also be agreement with the insurance company on how they

can handle the inventories. It is also important that they must read the consignment letter. The

minutes of the management also needs to be studied as per the management. Thus it is important

that auditors needs to understand the terms of the agreement and should verify it again and again

on timely basis so that the management can be informed in case there are no issues.

1c) As per ASA701, it is important that auditor should state all that matters which they feel are

detrimental for the company and should be stated in the auditors report. Proper matters should be

highlighted so that shareholders should become aware so that management should understand

which are the areas in which they should take charge of (Erik & Jan, 2017). The stakeholders

should also should take notice of which are the areas in which they are highlighted.

In the given case, the annual report of the Woolworths company has been completed and

important steps that has been taken by the company in the valuation and provisioning of the

inventory has been stated in details. An extract from the audit report is given below:

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

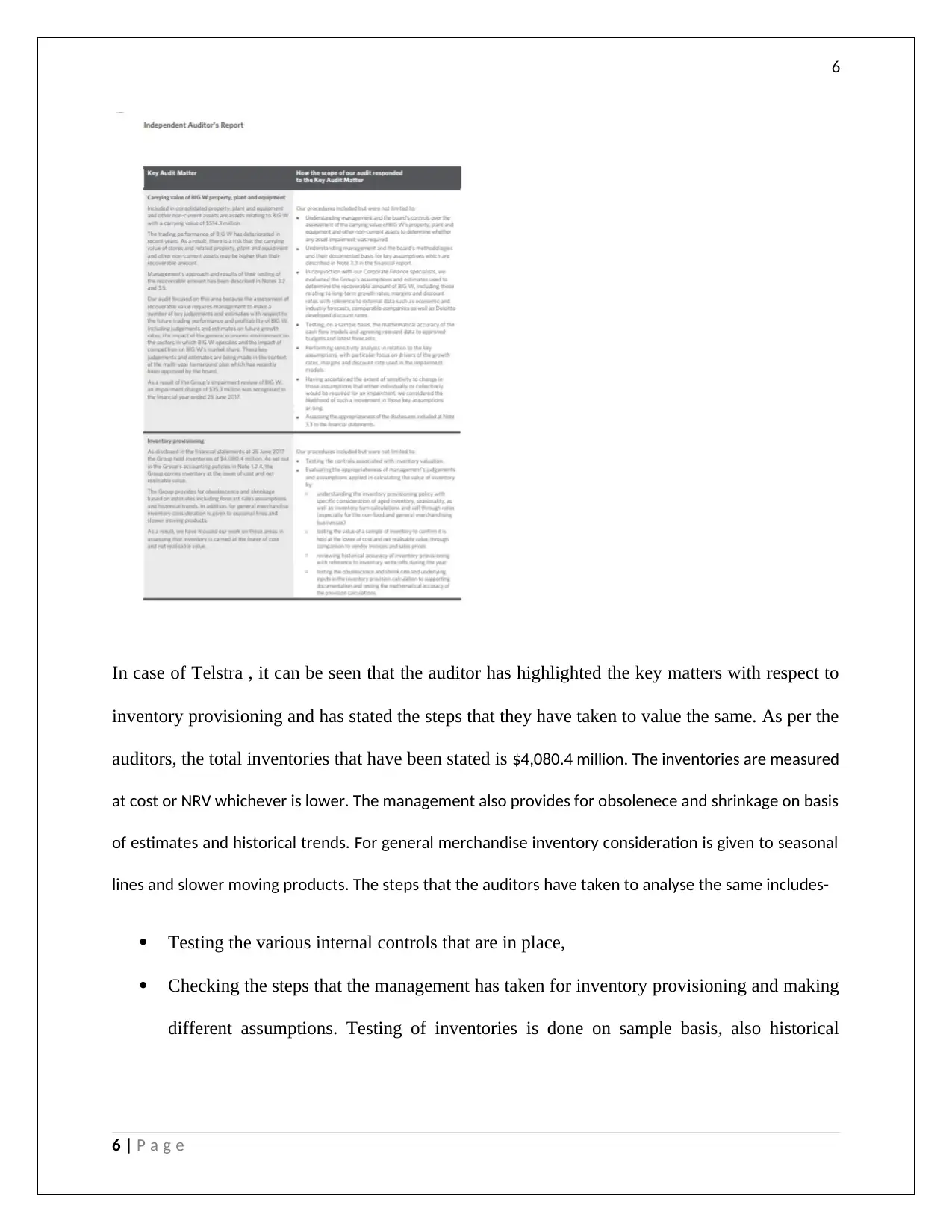

In case of Telstra , it can be seen that the auditor has highlighted the key matters with respect to

inventory provisioning and has stated the steps that they have taken to value the same. As per the

auditors, the total inventories that have been stated is $4,080.4 million. The inventories are measured

at cost or NRV whichever is lower. The management also provides for obsolenece and shrinkage on basis

of estimates and historical trends. For general merchandise inventory consideration is given to seasonal

lines and slower moving products. The steps that the auditors have taken to analyse the same includes-

Testing the various internal controls that are in place,

Checking the steps that the management has taken for inventory provisioning and making

different assumptions. Testing of inventories is done on sample basis, also historical

6 | P a g e

In case of Telstra , it can be seen that the auditor has highlighted the key matters with respect to

inventory provisioning and has stated the steps that they have taken to value the same. As per the

auditors, the total inventories that have been stated is $4,080.4 million. The inventories are measured

at cost or NRV whichever is lower. The management also provides for obsolenece and shrinkage on basis

of estimates and historical trends. For general merchandise inventory consideration is given to seasonal

lines and slower moving products. The steps that the auditors have taken to analyse the same includes-

Testing the various internal controls that are in place,

Checking the steps that the management has taken for inventory provisioning and making

different assumptions. Testing of inventories is done on sample basis, also historical

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

accuracy is checked through trend analysis, and checking the market rates. Shrinkage and

obsolence is also checked to check mathematical accuracy of the provisioning done.

Question 2

Intellectual property assets may be defined as those assets and right of an entity which

preserves the same and protects it from being copied or illegally altered. IT can be in the form of

an idea, a formula, and an innovation of any product or service by a person or a given company.

These are generally called copyright, trademarks, patents, etc. In the 21st century, there has been

a number of development and innovative ideas keep on coming and thereby companies keep on

coming up with new products and services. To protect these new technologies, it is necessary

that all these assets needs to be protected (Goldmann, 2016). These intellectual rights are being

governed and taken care off by the intellectual property laws which was formed with the

objective of encouraging creation of intellectual property rights.

2a)Key assertions at risk

1. Valuation: AASB 138, states the auditing provisions and disclosure requirements that

companies should follow with respect to intellectual property.The intellectual property

can be valued based on the 3 methods, which are historical cost method or the

replacement cost (cost of creating the intangible asset), the market value method (this is

based on compatibility of the market rates or the comparable royal rates of intangibles)

and thirdly based on economic value added method (this quantifies the future cash flows

or royalty income from the intellectual property and then capitalization of same post

discounting the cash flows) (Farmer, 2018). Economic value method is the most preferred

7 | P a g e

accuracy is checked through trend analysis, and checking the market rates. Shrinkage and

obsolence is also checked to check mathematical accuracy of the provisioning done.

Question 2

Intellectual property assets may be defined as those assets and right of an entity which

preserves the same and protects it from being copied or illegally altered. IT can be in the form of

an idea, a formula, and an innovation of any product or service by a person or a given company.

These are generally called copyright, trademarks, patents, etc. In the 21st century, there has been

a number of development and innovative ideas keep on coming and thereby companies keep on

coming up with new products and services. To protect these new technologies, it is necessary

that all these assets needs to be protected (Goldmann, 2016). These intellectual rights are being

governed and taken care off by the intellectual property laws which was formed with the

objective of encouraging creation of intellectual property rights.

2a)Key assertions at risk

1. Valuation: AASB 138, states the auditing provisions and disclosure requirements that

companies should follow with respect to intellectual property.The intellectual property

can be valued based on the 3 methods, which are historical cost method or the

replacement cost (cost of creating the intangible asset), the market value method (this is

based on compatibility of the market rates or the comparable royal rates of intangibles)

and thirdly based on economic value added method (this quantifies the future cash flows

or royalty income from the intellectual property and then capitalization of same post

discounting the cash flows) (Farmer, 2018). Economic value method is the most preferred

7 | P a g e

8

method out of all but it is completely upon the companies to use based on their

requirements.

2. Rights and Obligations: There are different categories and types of intellectual property

that is available for use and ownership and the right provided by each one of them differs

in one or the other way like the right which is being provided in the case of patents is not

similar to that provided in case of copyright or trademark. Copyright is generally in case

of books and journals, patent is in case of formulas and belongs to the person who has

created it (Grenier, 2017). This right becomes a right and ownership on the same is only

established once it is registered with the law. Unless this legal ownership is established,

the same cannot be recognised in books as an asset of the company. These complexities

altogether create the risks as well as assertions.

2b)Substantive Audit procedures

Substantive audit procedure may be defined as the collection of the primary and secondary data

from the database of the company in order to audit the client. This generally includes vouching

of incomes and expenses and verification of assets and liabilities and based on the differences

and issues found in the checking, the nature, extent and timing of the other audit procedures to be

employed is being determined (Jefferson, 2017). These are intended to justify the management

audit assertions that the financial statements as a whole are free from error and misstatement and

there are not material discrepancies with respect to the accuracy, validity and the completeness

of the financial statements.

8 | P a g e

method out of all but it is completely upon the companies to use based on their

requirements.

2. Rights and Obligations: There are different categories and types of intellectual property

that is available for use and ownership and the right provided by each one of them differs

in one or the other way like the right which is being provided in the case of patents is not

similar to that provided in case of copyright or trademark. Copyright is generally in case

of books and journals, patent is in case of formulas and belongs to the person who has

created it (Grenier, 2017). This right becomes a right and ownership on the same is only

established once it is registered with the law. Unless this legal ownership is established,

the same cannot be recognised in books as an asset of the company. These complexities

altogether create the risks as well as assertions.

2b)Substantive Audit procedures

Substantive audit procedure may be defined as the collection of the primary and secondary data

from the database of the company in order to audit the client. This generally includes vouching

of incomes and expenses and verification of assets and liabilities and based on the differences

and issues found in the checking, the nature, extent and timing of the other audit procedures to be

employed is being determined (Jefferson, 2017). These are intended to justify the management

audit assertions that the financial statements as a whole are free from error and misstatement and

there are not material discrepancies with respect to the accuracy, validity and the completeness

of the financial statements.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Some of the other substantive procedures in addition to the ones mentioned above are testing the

opening balances, disclosures and nature of transactions, journal entries and other material

adjustments done in the financial statements and the verification of the notes and financials with

the underlying records.

In case substantive procedures needs to be applied for the intangible assets, then the steps to be

applied include reviewing and checking the appropriateness of documentation w.r.t to ownership

or creation of the intangible asset, determining if the company has the ownership rights and if

yes, where is the legal documentation or the purchase agreement. The auditor should also be

checking the useful life of the intangible asset, the amortization policy which the company has

chosen, the amortization expenses booked in the P&L and whether or not any impairment is

required for the given carrying value of the asset. The auditor should also go through all the

management estimates and judgements with regards to the intangible assets (Kim, et al., 2017).

2c)Requirements of Auditing Standard ASA 701

As per ASA 701, “Communicating Key Audit Matters in the Independent Auditor’s Report”, the

auditor is supposed to report the key audit matters in the independent Auditors’ report of the

company. Key audit matter may be defined as the those issues which are most significant and

critical form the perspective of the audit based on the professional judgement applied by the

auditor and therefore the auditor generally undertakes additional steps to verify these items.

These are separately disclosed in the financial statements and are reported to ensure more

transparency and throw more stress on these issues.

There are various aspects which the auditor uses in determining what key audit matters, some of

which are are:

9 | P a g e

Some of the other substantive procedures in addition to the ones mentioned above are testing the

opening balances, disclosures and nature of transactions, journal entries and other material

adjustments done in the financial statements and the verification of the notes and financials with

the underlying records.

In case substantive procedures needs to be applied for the intangible assets, then the steps to be

applied include reviewing and checking the appropriateness of documentation w.r.t to ownership

or creation of the intangible asset, determining if the company has the ownership rights and if

yes, where is the legal documentation or the purchase agreement. The auditor should also be

checking the useful life of the intangible asset, the amortization policy which the company has

chosen, the amortization expenses booked in the P&L and whether or not any impairment is

required for the given carrying value of the asset. The auditor should also go through all the

management estimates and judgements with regards to the intangible assets (Kim, et al., 2017).

2c)Requirements of Auditing Standard ASA 701

As per ASA 701, “Communicating Key Audit Matters in the Independent Auditor’s Report”, the

auditor is supposed to report the key audit matters in the independent Auditors’ report of the

company. Key audit matter may be defined as the those issues which are most significant and

critical form the perspective of the audit based on the professional judgement applied by the

auditor and therefore the auditor generally undertakes additional steps to verify these items.

These are separately disclosed in the financial statements and are reported to ensure more

transparency and throw more stress on these issues.

There are various aspects which the auditor uses in determining what key audit matters, some of

which are are:

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

1. Issues that will be most important from user perspective,

2. Issues which involve complexities

3. Issues where the chances of misstatements is high

4. Issues where there are judgement and estimates involved.

5. Valuation issues requiring support of experts (Werner, 2017)

6. In terms of intangible assets, there can be doubts of existence of same and their useful

lives.

7. Valuation of the intangible property as it involves high level of complexities and the

chances of misstatements is quite high. Also, the method of amortization and the

impairment assumption of the entity also needs to be checked thoroughly.

The disclosure with respect to ASA 701 has been mentioned below:

While reporting the key audit matters in the independent audit report, the auditor should give a

brief description of the matter considered to be significant along with the reasons for the same.

This needs to be reported under a separate head in the Auditors report and besides that it needs to

be mentioned as to what all audit steps were being considered or taken to remove or resolve the

issue or the ambiguity (Trieu, 2017). The auditor should also justify how the key audit matter

affects the entity as a whole and its financials altogether. In case the auditor used the services of

the expert while approaching the issue, the same also needs to highlight along with the audit

procedures undertaken and the final outcome and key observations with regard to each of the key

audit matter.

10 | P a g e

1. Issues that will be most important from user perspective,

2. Issues which involve complexities

3. Issues where the chances of misstatements is high

4. Issues where there are judgement and estimates involved.

5. Valuation issues requiring support of experts (Werner, 2017)

6. In terms of intangible assets, there can be doubts of existence of same and their useful

lives.

7. Valuation of the intangible property as it involves high level of complexities and the

chances of misstatements is quite high. Also, the method of amortization and the

impairment assumption of the entity also needs to be checked thoroughly.

The disclosure with respect to ASA 701 has been mentioned below:

While reporting the key audit matters in the independent audit report, the auditor should give a

brief description of the matter considered to be significant along with the reasons for the same.

This needs to be reported under a separate head in the Auditors report and besides that it needs to

be mentioned as to what all audit steps were being considered or taken to remove or resolve the

issue or the ambiguity (Trieu, 2017). The auditor should also justify how the key audit matter

affects the entity as a whole and its financials altogether. In case the auditor used the services of

the expert while approaching the issue, the same also needs to highlight along with the audit

procedures undertaken and the final outcome and key observations with regard to each of the key

audit matter.

10 | P a g e

11

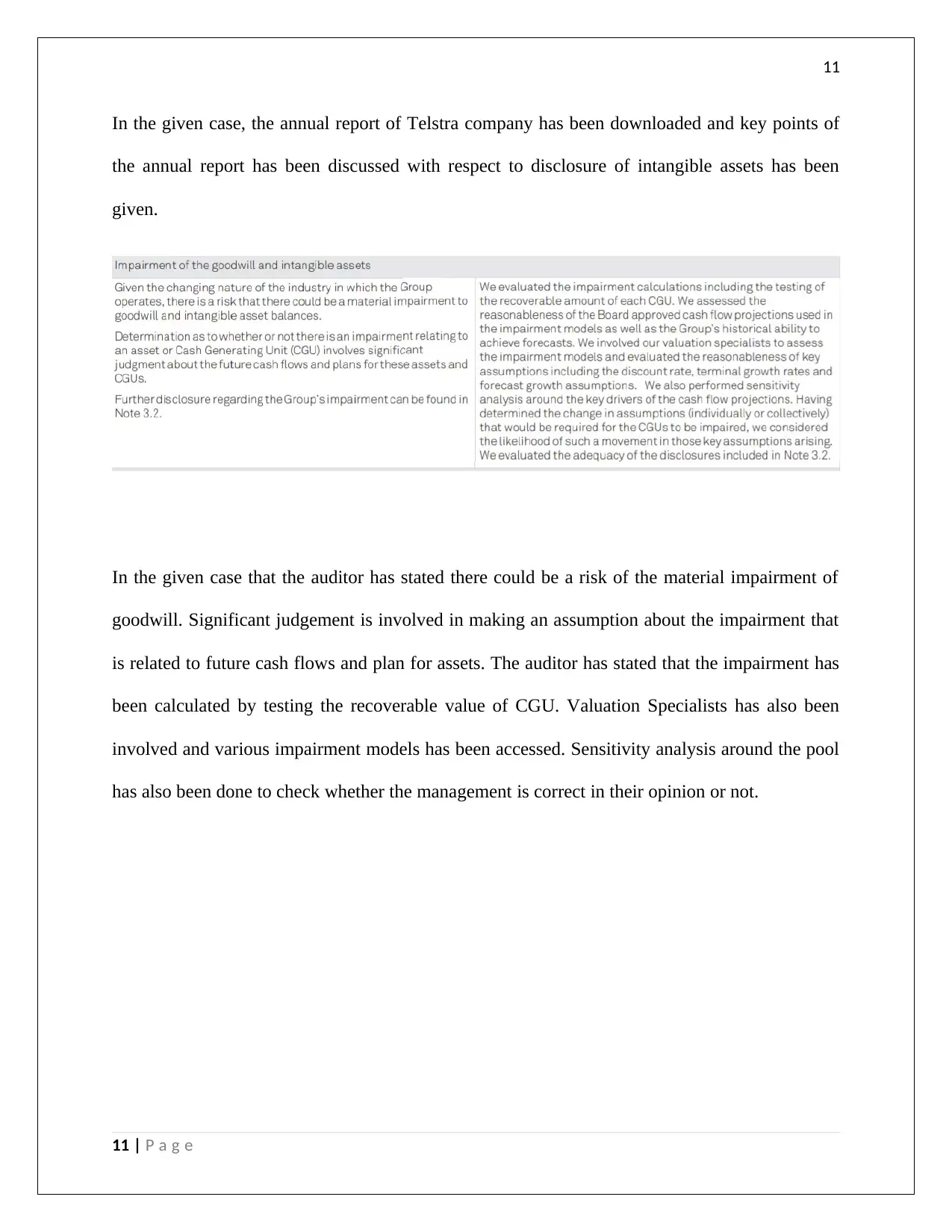

In the given case, the annual report of Telstra company has been downloaded and key points of

the annual report has been discussed with respect to disclosure of intangible assets has been

given.

In the given case that the auditor has stated there could be a risk of the material impairment of

goodwill. Significant judgement is involved in making an assumption about the impairment that

is related to future cash flows and plan for assets. The auditor has stated that the impairment has

been calculated by testing the recoverable value of CGU. Valuation Specialists has also been

involved and various impairment models has been accessed. Sensitivity analysis around the pool

has also been done to check whether the management is correct in their opinion or not.

11 | P a g e

In the given case, the annual report of Telstra company has been downloaded and key points of

the annual report has been discussed with respect to disclosure of intangible assets has been

given.

In the given case that the auditor has stated there could be a risk of the material impairment of

goodwill. Significant judgement is involved in making an assumption about the impairment that

is related to future cash flows and plan for assets. The auditor has stated that the impairment has

been calculated by testing the recoverable value of CGU. Valuation Specialists has also been

involved and various impairment models has been accessed. Sensitivity analysis around the pool

has also been done to check whether the management is correct in their opinion or not.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.