Professional Audit of Konekt Limited: Risk and Materiality Assessment

VerifiedAdded on 2023/03/31

|15

|3534

|322

Report

AI Summary

This report presents an audit of Konekt Limited, an Australian company specializing in organizational health and risk management. The audit focuses on identifying significant accounts at risk of material misstatement, setting planning materiality, and assessing potential risks. Key areas of concern include cash and cash equivalents, other assets, intangible assets, trade and other payables, and provisions. The report details the auditor's risk assessment procedures, which are crucial for forming an opinion on the fairness of the company's financial statements. Planning materiality is determined based on the company's total revenue, and the report emphasizes the importance of both qualitative and quantitative aspects of materiality in ensuring accurate financial reporting. Desklib offers a range of study tools, including past papers and solved assignments, to help students understand auditing principles and practices.

Running head: Professional Auditing

Professional Auditing

Name of the Student

Name of the University

Author Note

Professional Auditing

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Professional Auditing

Executive Summary

The report show about auditing process of the company y and show how the auditor gives its

opinion upon the financial statement of the company. It also shows about the company name

Konekt Limited. It shows about the misstatement of the account in the company and also

show the planning materiality of the company. Lastly it show the risk assessment procedure

which is to be followed by the auditor in regards of the misstatement of the account in the

company financial statement.

Professional Auditing

Executive Summary

The report show about auditing process of the company y and show how the auditor gives its

opinion upon the financial statement of the company. It also shows about the company name

Konekt Limited. It shows about the misstatement of the account in the company and also

show the planning materiality of the company. Lastly it show the risk assessment procedure

which is to be followed by the auditor in regards of the misstatement of the account in the

company financial statement.

2

Professional Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Client/ Company.........................................................................................3

Materiality in the Company financial statement....................................................................4

Audit Risk Assessment..........................................................................................................8

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Appendix..................................................................................................................................14

Professional Auditing

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Overview of the Client/ Company.........................................................................................3

Materiality in the Company financial statement....................................................................4

Audit Risk Assessment..........................................................................................................8

Conclusion................................................................................................................................11

Reference..................................................................................................................................12

Appendix..................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Professional Auditing

Introduction

Auditing is the process to know about the financial statement of the company,. The

auditing process is been carried by both internally and externally. Internally Audit is been

carried out by the employee of the company or the audit committee of the company. It is been

done so that the company can able to know whether there lacking behind and able to do the

correction of the mistake (Adler et al., 2018). As internal audit is able to check the internal

control of the company so it able to find all the problem which are there in the internal

control of the company and as a result it able to guide the company about the problem which

are there in the internal control and the company is able to do the correction in the internal

control problem and help the management to do the business smoothly (Barton and Bruder

2014). The external person is called auditor who carry audit process in the company and

gives its opinion whether the financial statement are showing true and fair view or not. To

check the details of the financial statement auditor have to carry many procedure so that it

able to ascertain the amount of risk which is there in the financial statement and able to give

proper opinion about the financial statement (Christensen, Elder and Glover 2014). It also

check about the internal control of the company as it is the main reason where the most fault

of the company can occur and also it is the place which can tell the auditor about whether

there is any fraud is happening in the company or not and also it show about the material

misstatement in the financial statement of the company. The assignment is been based about

the company Konekt Limited and it show about the various risk which are been associated in

the company and also it show about the planning materiality of the company.

Professional Auditing

Introduction

Auditing is the process to know about the financial statement of the company,. The

auditing process is been carried by both internally and externally. Internally Audit is been

carried out by the employee of the company or the audit committee of the company. It is been

done so that the company can able to know whether there lacking behind and able to do the

correction of the mistake (Adler et al., 2018). As internal audit is able to check the internal

control of the company so it able to find all the problem which are there in the internal

control of the company and as a result it able to guide the company about the problem which

are there in the internal control and the company is able to do the correction in the internal

control problem and help the management to do the business smoothly (Barton and Bruder

2014). The external person is called auditor who carry audit process in the company and

gives its opinion whether the financial statement are showing true and fair view or not. To

check the details of the financial statement auditor have to carry many procedure so that it

able to ascertain the amount of risk which is there in the financial statement and able to give

proper opinion about the financial statement (Christensen, Elder and Glover 2014). It also

check about the internal control of the company as it is the main reason where the most fault

of the company can occur and also it is the place which can tell the auditor about whether

there is any fraud is happening in the company or not and also it show about the material

misstatement in the financial statement of the company. The assignment is been based about

the company Konekt Limited and it show about the various risk which are been associated in

the company and also it show about the planning materiality of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Professional Auditing

Discussion

Overview of the Client/ Company

The assignment is been based about the company Konekt Limited. It is an Australian

based company which deals in regards of the employee’s safety as it deals in organizational

health and risk management solution in different industry. As the company help different

organization about minimization of the employee’s injury and also it help them to reduce the

workplace cost which the company have to spend in the business (Konekt.com.au 2019). It

mostly carries its business in Australia and it then largest company in its industry. The

company have a large experience as it have more than 20 years of experience in the field so it

can be said the company is most prominent in providing this kind of services in Australia.

Materiality in the Company financial statement

Materiality is the part which should be checked by the auditor, as if the company

financial statement have contain materiality than it will not able to provide true and fair view

(DeFond and Zhang 2014). Materiality represent the misstatement which is been done by the

company as it have done some amount of omission and error while recording the financial

transaction in the business as it also show about how the company is not able to prepare

proper accounting as result it affected the financial statement of the company. As if there will

be misstatement in the company than it will directly affect the stakeholder as stakeholder are

the one who take decision on the basis of the financial statement so if there is error or

omission than it will not able to take accurate or fair decision in regards of the company

(Edgley 2014). The company can have both kind of materiality as qualitative and quantitative

aspects.

Qualitative Aspects of Materiality

Professional Auditing

Discussion

Overview of the Client/ Company

The assignment is been based about the company Konekt Limited. It is an Australian

based company which deals in regards of the employee’s safety as it deals in organizational

health and risk management solution in different industry. As the company help different

organization about minimization of the employee’s injury and also it help them to reduce the

workplace cost which the company have to spend in the business (Konekt.com.au 2019). It

mostly carries its business in Australia and it then largest company in its industry. The

company have a large experience as it have more than 20 years of experience in the field so it

can be said the company is most prominent in providing this kind of services in Australia.

Materiality in the Company financial statement

Materiality is the part which should be checked by the auditor, as if the company

financial statement have contain materiality than it will not able to provide true and fair view

(DeFond and Zhang 2014). Materiality represent the misstatement which is been done by the

company as it have done some amount of omission and error while recording the financial

transaction in the business as it also show about how the company is not able to prepare

proper accounting as result it affected the financial statement of the company. As if there will

be misstatement in the company than it will directly affect the stakeholder as stakeholder are

the one who take decision on the basis of the financial statement so if there is error or

omission than it will not able to take accurate or fair decision in regards of the company

(Edgley 2014). The company can have both kind of materiality as qualitative and quantitative

aspects.

Qualitative Aspects of Materiality

5

Professional Auditing

1. Lack of Proper Disclosure – If the company is not able to provide the necessary

disclosure in regards of the accounting and other details of the company so it is been

consider as an misstatement in the financial statement as the company should

disclose all the information in regards of the financial statement of the company

(Eilifsen and Messier Jr 2014). As it should give proper disclosure of the matter such

as contingent liability or related party transaction in the business so it is been

consider a material misstatement so it should be disclose properly in the financial

statement of the company.

2. Error in the Financial Statement – Company should not have any error in the

financial statement as it may happen that the company is not able to record properly

in the financial statement so it will be consider as misstatement in the financial

statement of the company (Escobar and Demeritt 2017). As if there is an error in the

recording of the transaction so it can happen that the company is not having proper

records so it can over or under state so this will affect the financial statement and as a

result it will affect the financial decision of the stakeholders. So the company should

not have any error while preparing the financial statement of the company.

Quantitative Aspects of Materiality

There are some steps which should be follow by the auditor in order to know the

quantitative materiality, the steps are been shown below:

1. The auditor should make a judgement of the materiality in the planning stage of the

audit, as it should make a judgement over the financial statement as so that it can able

to assertion the amount of materiality which the financial statement can able to have

as it should make a percentage upon the profit so that it will help in the carrying audit

process in the company (Furnham and Gunter 2015).

Professional Auditing

1. Lack of Proper Disclosure – If the company is not able to provide the necessary

disclosure in regards of the accounting and other details of the company so it is been

consider as an misstatement in the financial statement as the company should

disclose all the information in regards of the financial statement of the company

(Eilifsen and Messier Jr 2014). As it should give proper disclosure of the matter such

as contingent liability or related party transaction in the business so it is been

consider a material misstatement so it should be disclose properly in the financial

statement of the company.

2. Error in the Financial Statement – Company should not have any error in the

financial statement as it may happen that the company is not able to record properly

in the financial statement so it will be consider as misstatement in the financial

statement of the company (Escobar and Demeritt 2017). As if there is an error in the

recording of the transaction so it can happen that the company is not having proper

records so it can over or under state so this will affect the financial statement and as a

result it will affect the financial decision of the stakeholders. So the company should

not have any error while preparing the financial statement of the company.

Quantitative Aspects of Materiality

There are some steps which should be follow by the auditor in order to know the

quantitative materiality, the steps are been shown below:

1. The auditor should make a judgement of the materiality in the planning stage of the

audit, as it should make a judgement over the financial statement as so that it can able

to assertion the amount of materiality which the financial statement can able to have

as it should make a percentage upon the profit so that it will help in the carrying audit

process in the company (Furnham and Gunter 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Professional Auditing

2. It should assertion upon the different account which can able to have misstatement

and able to effect the financial statement of the company.

3. It should bale to add all the amount which it have got in regards of the materiality and

should do the aggregate of the same in regards of the financial statement of the

company.

4. Auditor should compare the actual materiality and the estimated so that it able to

know about the risk which is been associated in the business and than it should carry

the audit procedure in the company.

Five account of the company which have materiality

1. Cash and Cash Equivalents – It can be seen from the financial statement of the

company that in there is significant increase in the cash account of the company as in

2017 it was $2848 but in 2018 it is $5661 so it can be seen that the increase is too

high so it is been consider by the auditor as it may contain misstatement in the

account it may happen the company have overstated it so that it can able to quick

ratio good and able to show the financial user so that it able to invest more in the

business of the company (Griffin 2014).

2. Other Assets – It can be seen from the financial statement of the company that there

is big increase in the other asset of the company so it is been consider as

misstatement by the company as in 2017 it was $290 and in 2018 it is $460 so this

show there is a big increase in the other asset so the auditor will take into

consideration as misstatement which is been done by the company so that it can able

to show a good current ratio of the company as it will able to attract more number of

the investor by the help of showing good current ratio (Griffiths 2016).

3. Intangible Assets – It can be seen from the balance sheet of the company as there is

so much increase in the intangible asset so it is been consider as materiality by the

Professional Auditing

2. It should assertion upon the different account which can able to have misstatement

and able to effect the financial statement of the company.

3. It should bale to add all the amount which it have got in regards of the materiality and

should do the aggregate of the same in regards of the financial statement of the

company.

4. Auditor should compare the actual materiality and the estimated so that it able to

know about the risk which is been associated in the business and than it should carry

the audit procedure in the company.

Five account of the company which have materiality

1. Cash and Cash Equivalents – It can be seen from the financial statement of the

company that in there is significant increase in the cash account of the company as in

2017 it was $2848 but in 2018 it is $5661 so it can be seen that the increase is too

high so it is been consider by the auditor as it may contain misstatement in the

account it may happen the company have overstated it so that it can able to quick

ratio good and able to show the financial user so that it able to invest more in the

business of the company (Griffin 2014).

2. Other Assets – It can be seen from the financial statement of the company that there

is big increase in the other asset of the company so it is been consider as

misstatement by the company as in 2017 it was $290 and in 2018 it is $460 so this

show there is a big increase in the other asset so the auditor will take into

consideration as misstatement which is been done by the company so that it can able

to show a good current ratio of the company as it will able to attract more number of

the investor by the help of showing good current ratio (Griffiths 2016).

3. Intangible Assets – It can be seen from the balance sheet of the company as there is

so much increase in the intangible asset so it is been consider as materiality by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Professional Auditing

auditor as it was shown such a big increase as in 2017 it was $12665 and in 2018 it is

$44112 so this show there is a big increase in the intangible asset so it is been

consider as a misstatement by the company as it is been increase by the company so

that it can able to show the financial user that the have so much brand value and

goodwill in the market so it is been consider as a material misstatement account by

the auditor (Groomer and Murthy 2018).

4. Trade and other Payables – It can be seen from the balanced sheet of the company

that there is a increase from a high margin which is been consider not proper by the

auditor so as a result the auditor consider it as a material misstatement which is been

done by the company. As in 2017 it was $5572 and in 2018 it is $13082 so this show

that there is a big increase so this can be done by the company so that it can able to

show the investors that the company is performing good as a result it able to get some

much amount credit from the creditors of the company (Hall 2015).

5. Provisions – It can be seen from the company financial statement that there is a

provision which is been created by the company in the current year as it does not

have any provision in the year 2017 so it is been consider as material misstatement by

the auditor as why suddenly the company is able to make provision in regards of the

trade receivables of the company (He, Zeadally and Wu 2015).

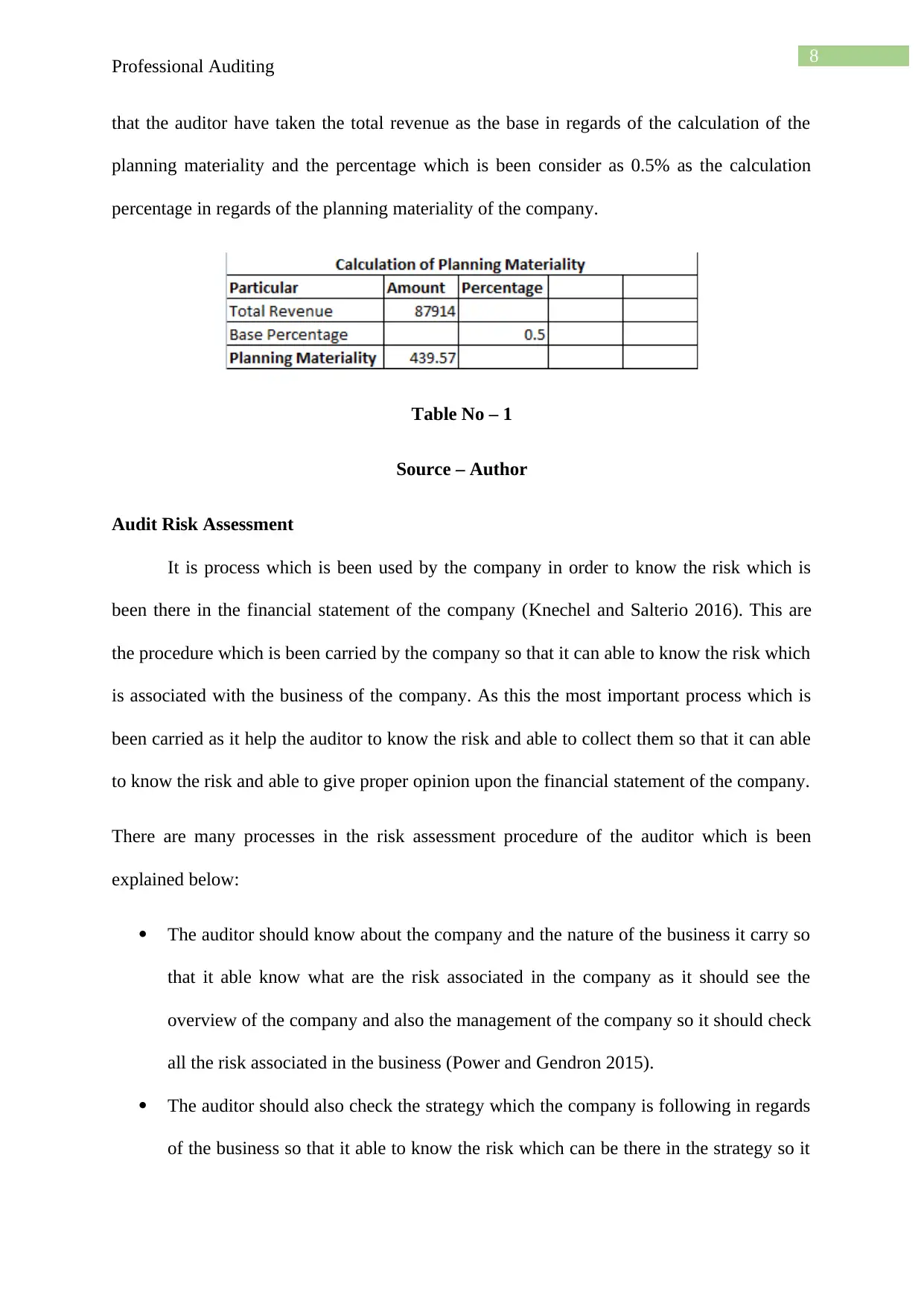

Planning Materiality

Planning materiality is the method which the auditor do in the planning stage of the

auditing as it should make a plan of the misstatement which is to be done by the auditor as it

make planning of the materiality which is been there in the financial statement of the

company (King 2014). It is the method which is been used by the auditor to ascertain the

financial statement materiality. As per the company is been concern the auditor have done

that it should take into consideration about the total revenue of the company. So it can be said

Professional Auditing

auditor as it was shown such a big increase as in 2017 it was $12665 and in 2018 it is

$44112 so this show there is a big increase in the intangible asset so it is been

consider as a misstatement by the company as it is been increase by the company so

that it can able to show the financial user that the have so much brand value and

goodwill in the market so it is been consider as a material misstatement account by

the auditor (Groomer and Murthy 2018).

4. Trade and other Payables – It can be seen from the balanced sheet of the company

that there is a increase from a high margin which is been consider not proper by the

auditor so as a result the auditor consider it as a material misstatement which is been

done by the company. As in 2017 it was $5572 and in 2018 it is $13082 so this show

that there is a big increase so this can be done by the company so that it can able to

show the investors that the company is performing good as a result it able to get some

much amount credit from the creditors of the company (Hall 2015).

5. Provisions – It can be seen from the company financial statement that there is a

provision which is been created by the company in the current year as it does not

have any provision in the year 2017 so it is been consider as material misstatement by

the auditor as why suddenly the company is able to make provision in regards of the

trade receivables of the company (He, Zeadally and Wu 2015).

Planning Materiality

Planning materiality is the method which the auditor do in the planning stage of the

auditing as it should make a plan of the misstatement which is to be done by the auditor as it

make planning of the materiality which is been there in the financial statement of the

company (King 2014). It is the method which is been used by the auditor to ascertain the

financial statement materiality. As per the company is been concern the auditor have done

that it should take into consideration about the total revenue of the company. So it can be said

8

Professional Auditing

that the auditor have taken the total revenue as the base in regards of the calculation of the

planning materiality and the percentage which is been consider as 0.5% as the calculation

percentage in regards of the planning materiality of the company.

Table No – 1

Source – Author

Audit Risk Assessment

It is process which is been used by the company in order to know the risk which is

been there in the financial statement of the company (Knechel and Salterio 2016). This are

the procedure which is been carried by the company so that it can able to know the risk which

is associated with the business of the company. As this the most important process which is

been carried as it help the auditor to know the risk and able to collect them so that it can able

to know the risk and able to give proper opinion upon the financial statement of the company.

There are many processes in the risk assessment procedure of the auditor which is been

explained below:

The auditor should know about the company and the nature of the business it carry so

that it able know what are the risk associated in the company as it should see the

overview of the company and also the management of the company so it should check

all the risk associated in the business (Power and Gendron 2015).

The auditor should also check the strategy which the company is following in regards

of the business so that it able to know the risk which can be there in the strategy so it

Professional Auditing

that the auditor have taken the total revenue as the base in regards of the calculation of the

planning materiality and the percentage which is been consider as 0.5% as the calculation

percentage in regards of the planning materiality of the company.

Table No – 1

Source – Author

Audit Risk Assessment

It is process which is been used by the company in order to know the risk which is

been there in the financial statement of the company (Knechel and Salterio 2016). This are

the procedure which is been carried by the company so that it can able to know the risk which

is associated with the business of the company. As this the most important process which is

been carried as it help the auditor to know the risk and able to collect them so that it can able

to know the risk and able to give proper opinion upon the financial statement of the company.

There are many processes in the risk assessment procedure of the auditor which is been

explained below:

The auditor should know about the company and the nature of the business it carry so

that it able know what are the risk associated in the company as it should see the

overview of the company and also the management of the company so it should check

all the risk associated in the business (Power and Gendron 2015).

The auditor should also check the strategy which the company is following in regards

of the business so that it able to know the risk which can be there in the strategy so it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Professional Auditing

should check the strategy as well the implication of the strategy in the business of the

company (Reid 2015).

It should also examine the company management so that it can know who are the

members in the management and also how much expert people are there and how the

management is able to manage the business of the company.

It should ask the individual working in the organization so that it able to know the

answer which are been given by the management is correct or not. As it should check

the management answer with the employee answer so that it can able to get a clarity

of the answer and also able to judge the same in the financial statement of the

company.

It can able to perform different analysis so that it can able to know about the different

in the figures so that it can proper judgement of the financial statement of the

company so that it able to know all the difference which are there in the financial

statement of the company.

Risk assessment of the above mention points

1. Cash Account – The auditor of the company will verify the cash account of the

company as per ASA 330 it will check all the transaction of the company related to

the cash and also check the cashier document so that it able to know about the cash

inflow and outflow as it will also check about the cash flow statement of the

company so that it can able to know the inflow and outflow of the cash which will

help the company to get an overview of the financial statement and as a result the

auditor will able to know reason of the increase in the cash and cash equivalent of the

company (Wang, Li and Li 2014).

2. Other Assets – The auditor of the company should verify all the items as per ASA

330 it will see the items which are been included by the company in their other asset

Professional Auditing

should check the strategy as well the implication of the strategy in the business of the

company (Reid 2015).

It should also examine the company management so that it can know who are the

members in the management and also how much expert people are there and how the

management is able to manage the business of the company.

It should ask the individual working in the organization so that it able to know the

answer which are been given by the management is correct or not. As it should check

the management answer with the employee answer so that it can able to get a clarity

of the answer and also able to judge the same in the financial statement of the

company.

It can able to perform different analysis so that it can able to know about the different

in the figures so that it can proper judgement of the financial statement of the

company so that it able to know all the difference which are there in the financial

statement of the company.

Risk assessment of the above mention points

1. Cash Account – The auditor of the company will verify the cash account of the

company as per ASA 330 it will check all the transaction of the company related to

the cash and also check the cashier document so that it able to know about the cash

inflow and outflow as it will also check about the cash flow statement of the

company so that it can able to know the inflow and outflow of the cash which will

help the company to get an overview of the financial statement and as a result the

auditor will able to know reason of the increase in the cash and cash equivalent of the

company (Wang, Li and Li 2014).

2. Other Assets – The auditor of the company should verify all the items as per ASA

330 it will see the items which are been included by the company in their other asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Professional Auditing

and also it verify all the transaction which the company have done in related to the

other assets of the company. It should check whether their no error and omission by

the company in recording of the transaction and lastly it should also check the

disclosure which is been given by the company in their financial reporting so that the

auditor can able to know the reason of the increase in the value of the other asset in

the financial statement of the company (Xia et al., 2015).

3. Intangible Asset – The auditor should check the items which are been included in

the intangible asset by the company as per ASA 330 it should check that the

company have done the valuation of the intangible asset as per the accounting

standard or not. It should also analysis about the transaction which is been done by

the company in related to the intangible asset of the company. As it should check the

disclosure of the company in the notes of account so that it can know the reason of

the increase in the intangible asset of the company so after carrying this procedure

the auditor will able to know the reason of the increase in the intangible asset.

4. Trade and other Payables – The auditor should check the transaction related to the

trade and other payables of the company. As per ASA 330 it should do the third party

verification so that it can able to know the real amount and able to verify the same

with the balance which is been given in the financial statement of the company lastly

it should check the disclosure which is been given by the company in regards of the

trade payables so that it able to know the reason of increase in the financial statement

of the company.

5. Provisions – The auditor should check about accounting treatment which is been

done by the in related to the provision of the company. As per ASA 330 It should

have a questioner with the management as it will help the auditor to know the reason

why the company have make the provision in the current year as it was not there in

Professional Auditing

and also it verify all the transaction which the company have done in related to the

other assets of the company. It should check whether their no error and omission by

the company in recording of the transaction and lastly it should also check the

disclosure which is been given by the company in their financial reporting so that the

auditor can able to know the reason of the increase in the value of the other asset in

the financial statement of the company (Xia et al., 2015).

3. Intangible Asset – The auditor should check the items which are been included in

the intangible asset by the company as per ASA 330 it should check that the

company have done the valuation of the intangible asset as per the accounting

standard or not. It should also analysis about the transaction which is been done by

the company in related to the intangible asset of the company. As it should check the

disclosure of the company in the notes of account so that it can know the reason of

the increase in the intangible asset of the company so after carrying this procedure

the auditor will able to know the reason of the increase in the intangible asset.

4. Trade and other Payables – The auditor should check the transaction related to the

trade and other payables of the company. As per ASA 330 it should do the third party

verification so that it can able to know the real amount and able to verify the same

with the balance which is been given in the financial statement of the company lastly

it should check the disclosure which is been given by the company in regards of the

trade payables so that it able to know the reason of increase in the financial statement

of the company.

5. Provisions – The auditor should check about accounting treatment which is been

done by the in related to the provision of the company. As per ASA 330 It should

have a questioner with the management as it will help the auditor to know the reason

why the company have make the provision in the current year as it was not there in

11

Professional Auditing

the previous year so it should be checked by the auditor about the reason of such

increase in the provision and it should also check the provision which is been given

by the company in the financial statement of the company so that it can able to know

the reason of the provision in the company.

Conclusion

The report conclude about the auditing process which is been carried by the auditor in

the company as the auditor check the financial statement of the company and gives it opinion

upon the financial statement of the company as whether the financial statement are showing

true and fair view or not. The auditor have to carry many procedure in the company so that it

able to know the risk which is been associated in the financial statement of the company. It

also check the internal control of the company so that it can able to know how the company

manages its business internal and the internal control help the auditor to know there are any

risk or fraud in the company or not. It check that the company does not have any material

misstatement of the company as it have contain material misstatement than it will affect the

decision power of the financial user of the company.

It show an details of the company Konekt Limited which is an Australian based

company and carry its business as risk management of the company and also help the

company to reduce employee cost. It shows about the materiality concept and show the

accounts of the company which contain misstatement and can affect the financial statement

of the company. It also includes the planning materiality and the auditor have taken the total

revenue as the base for the calculation of planning materiality of the company. Lastly it

concludes about the risk assessment procedure and also show the risk assessment which the

auditor has to carry in the company shown accounts.

Professional Auditing

the previous year so it should be checked by the auditor about the reason of such

increase in the provision and it should also check the provision which is been given

by the company in the financial statement of the company so that it can able to know

the reason of the provision in the company.

Conclusion

The report conclude about the auditing process which is been carried by the auditor in

the company as the auditor check the financial statement of the company and gives it opinion

upon the financial statement of the company as whether the financial statement are showing

true and fair view or not. The auditor have to carry many procedure in the company so that it

able to know the risk which is been associated in the financial statement of the company. It

also check the internal control of the company so that it can able to know how the company

manages its business internal and the internal control help the auditor to know there are any

risk or fraud in the company or not. It check that the company does not have any material

misstatement of the company as it have contain material misstatement than it will affect the

decision power of the financial user of the company.

It show an details of the company Konekt Limited which is an Australian based

company and carry its business as risk management of the company and also help the

company to reduce employee cost. It shows about the materiality concept and show the

accounts of the company which contain misstatement and can affect the financial statement

of the company. It also includes the planning materiality and the auditor have taken the total

revenue as the base for the calculation of planning materiality of the company. Lastly it

concludes about the risk assessment procedure and also show the risk assessment which the

auditor has to carry in the company shown accounts.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.