Auditing Origin Energy: Materiality, Audit Procedures, and Review

VerifiedAdded on 2022/12/18

|10

|2096

|54

Report

AI Summary

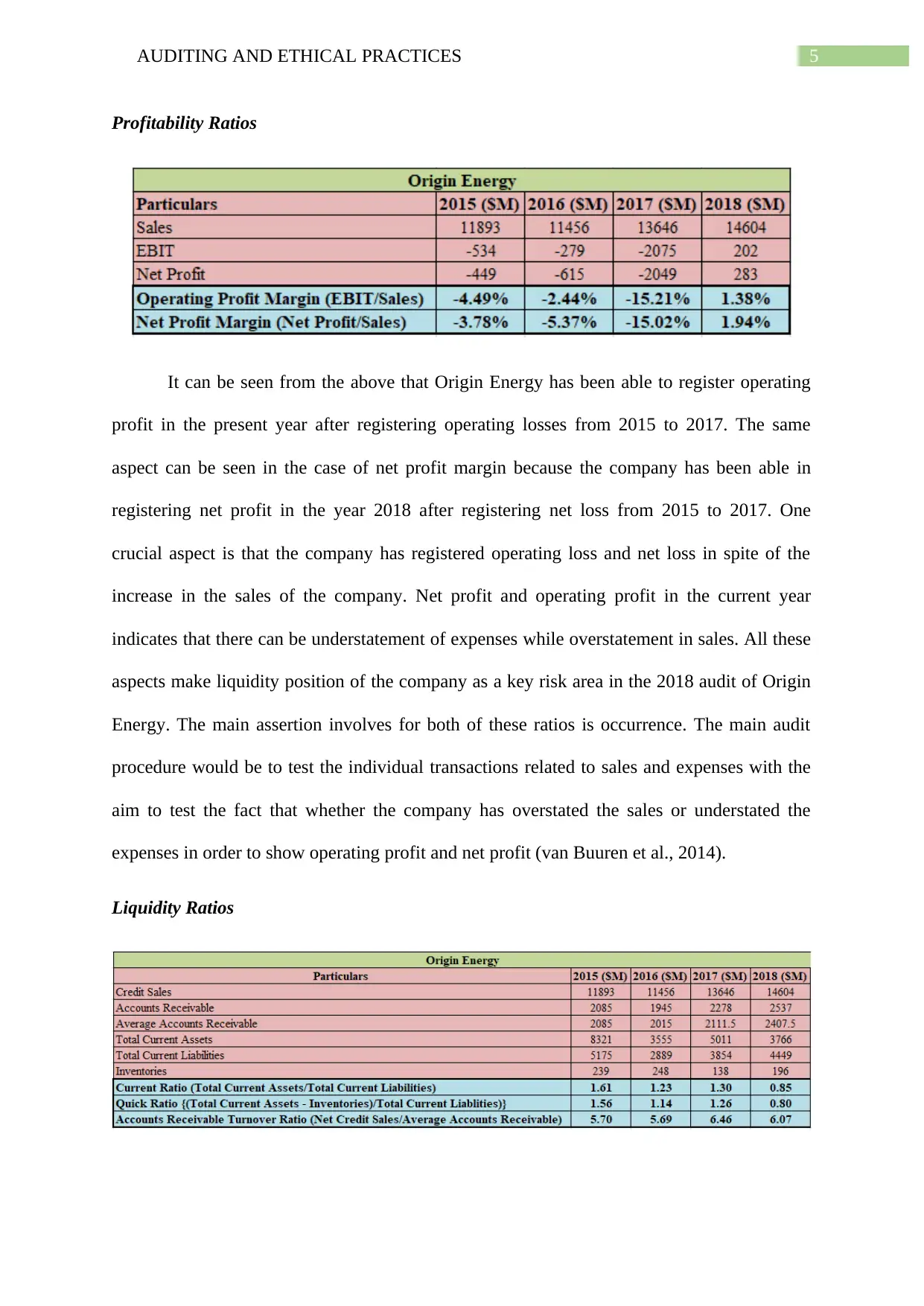

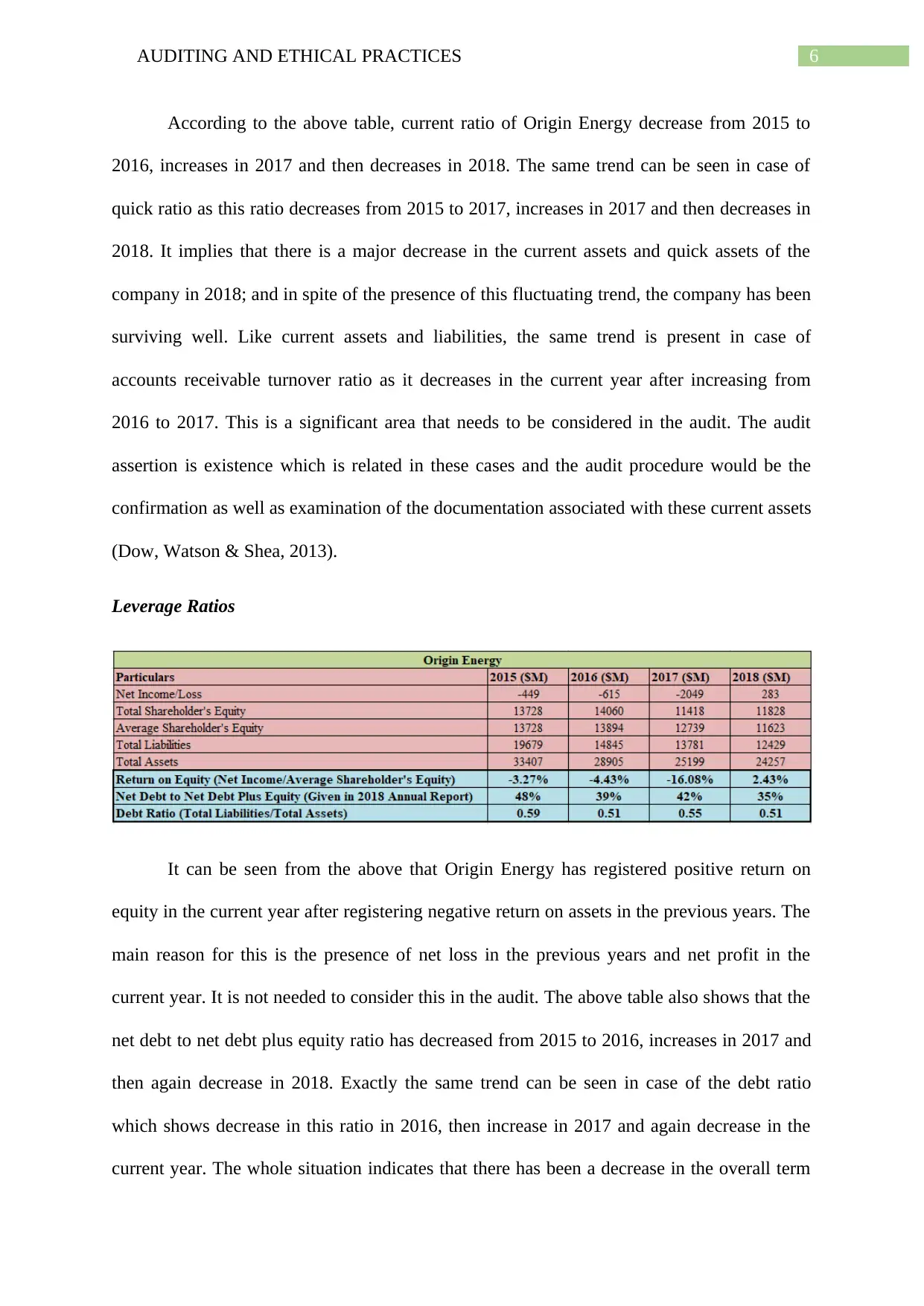

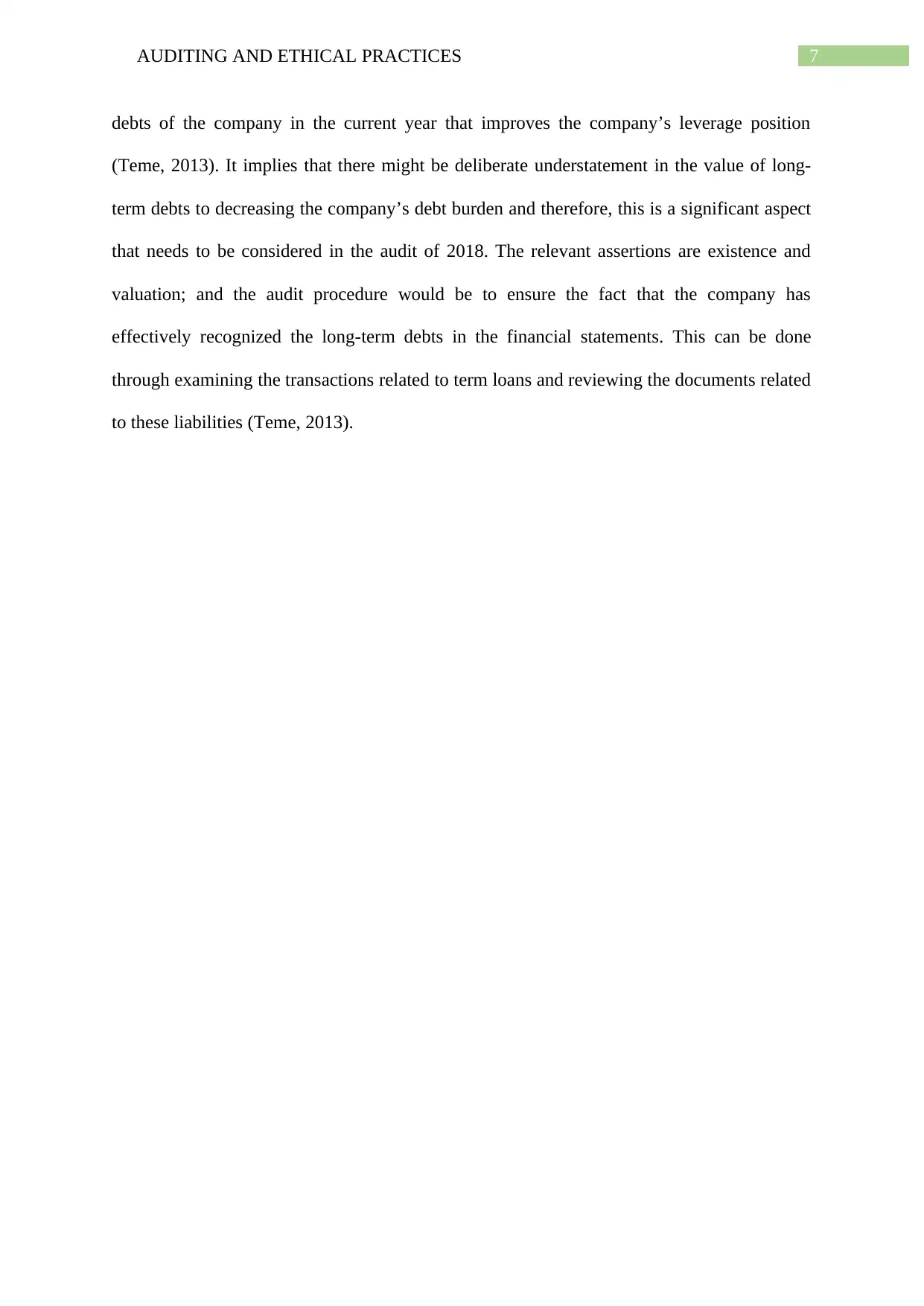

This report provides a comprehensive analysis of the 2018 audit of Origin Energy. Section 1 focuses on determining the level of materiality, discussing relevant benchmarks such as total assets due to the company's operating loss and recent small profit, and applying a 5% threshold. It also identifies significant audit areas, including contingent liabilities (guarantees, joint arrangements, and capital expenditures) and a change in accounting method. Section 2 conducts a preliminary analytical review using profitability, liquidity, and leverage ratios. The review highlights key financial trends, such as the company's operating profit, fluctuations in current and quick ratios, and changes in debt levels, and discusses the implications for the audit, including potential risks of misstatement and related audit procedures to verify financial statement assertions. The report emphasizes the importance of these aspects for a thorough audit of Origin Energy's financial statements.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.