Project: Audit Materiality, Sample Size, Analytical Review - Finance

VerifiedAdded on 2022/11/29

|8

|1279

|323

Project

AI Summary

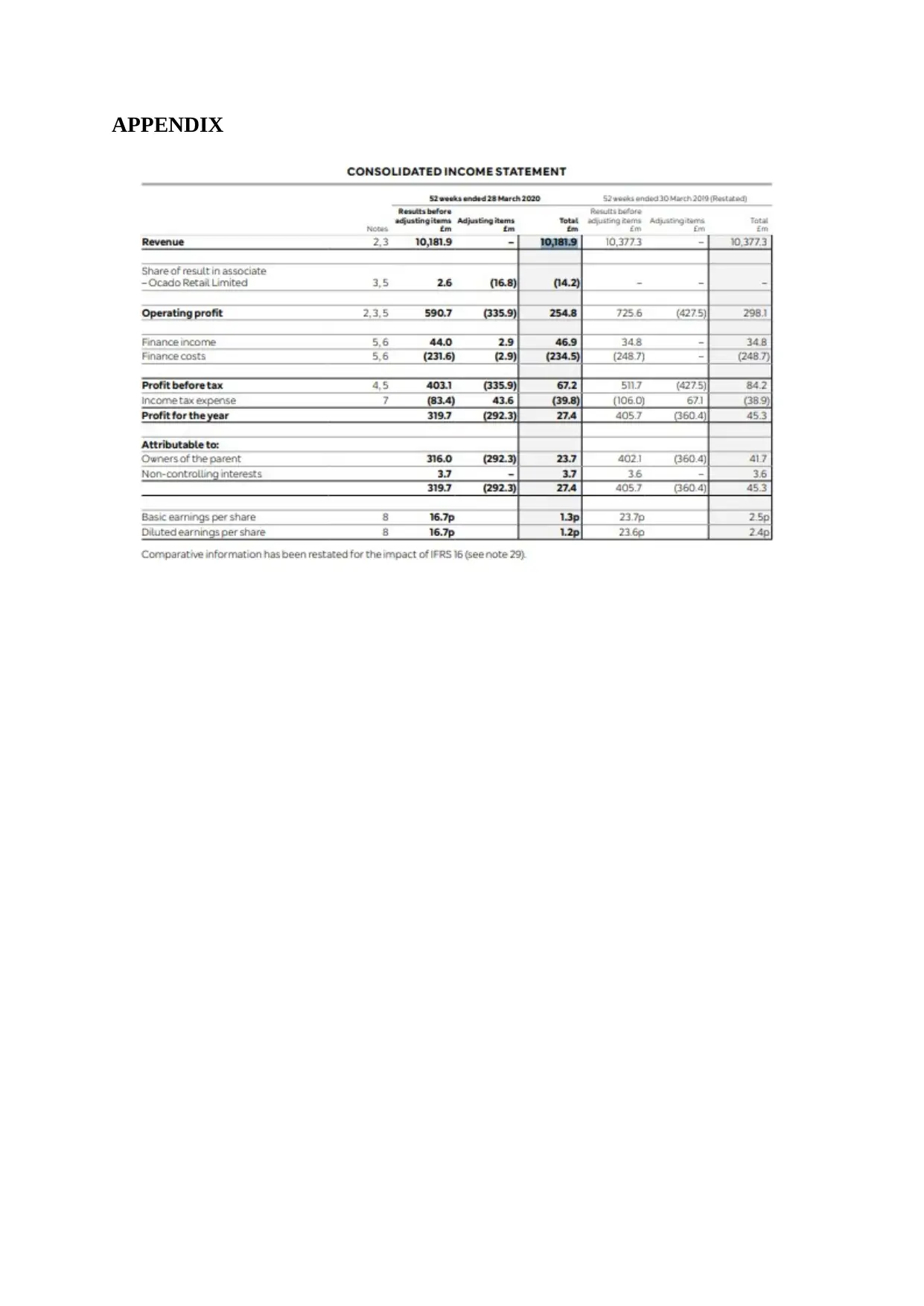

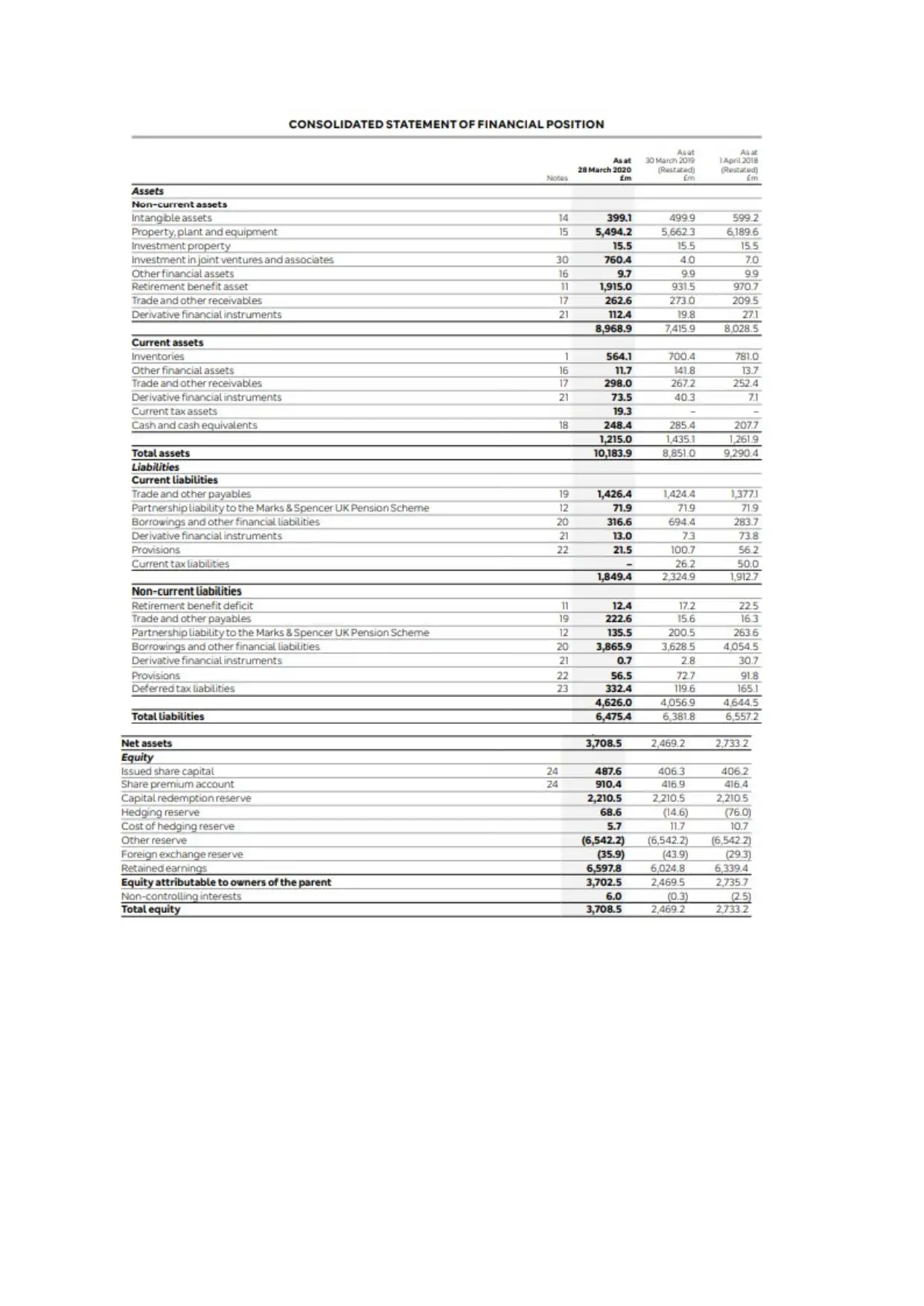

This project report focuses on determining planning materiality for an audit, calculating sample size for a statement of financial position, and performing a substantive analytical review. The planning materiality is calculated based on the financial statements, considering factors such as sales revenue and net profit. The sample size calculation utilizes statistical formulas to determine the number of items required for a high confidence level. The audit program outlines the assertions, evidence collection methods, and the direction of tests, followed by a critical evaluation of the evidence. The substantive analytical review involves developing an independent expectation, identifying significant differences, computing the differences, and investigating those differences to draw conclusions. The project references relevant academic literature and online resources to support its findings. The assignment is designed to enhance understanding of audit procedures and financial statement analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.