Research, Analysis & Evaluation of Key Audit Matters in Audit Report

VerifiedAdded on 2023/01/23

|12

|3312

|38

Report

AI Summary

This report critically analyzes and evaluates key audit matters within independent auditor's reports, emphasizing the importance of auditing in risk management and fraud prevention. It explores the role of auditing standards, particularly ASA 701, in assessing internal controls and mitigating material misstatements, referencing the Commonwealth Bank as a case study. The report discusses the rationale behind ASA 701, highlighting its focus on communication and transparency to enhance trust and stability. Key areas examined include banking asset development, inventory management, and liquidity/funding, with recommendations for improving ethical considerations and consumer development plans. The analysis emphasizes the need for effective communication among auditors, investors, and supervisors to address financial issues and ensure adherence to auditing standards.

RESEARCH, CRITICALLY ANALYSE AND EVALUATE KEY

AUDIT MATTERS IN INDEPENDENT AUDITOR’S REPORT

1

AUDIT MATTERS IN INDEPENDENT AUDITOR’S REPORT

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report highlights the importance of auditing report for risk management as well as to

deter fraud. It aids in the prevention of accounting irregularities that prevent the risk of

material misstatement. Auditing standards are associated with internal assessment in order to

evaluate the effectiveness of the existing internal controls of the organization that limits the

attaining organization's business goals and objectives. The Commonwealth Bank adheres to

ASA 701 standard on auditing in order to control the internal operation in the organization

and reduce the risk of fraud as well as a material misstatement. It is recommended to consider

auditor’s ethical value that enhances the effectiveness of the auditing report.

2

The report highlights the importance of auditing report for risk management as well as to

deter fraud. It aids in the prevention of accounting irregularities that prevent the risk of

material misstatement. Auditing standards are associated with internal assessment in order to

evaluate the effectiveness of the existing internal controls of the organization that limits the

attaining organization's business goals and objectives. The Commonwealth Bank adheres to

ASA 701 standard on auditing in order to control the internal operation in the organization

and reduce the risk of fraud as well as a material misstatement. It is recommended to consider

auditor’s ethical value that enhances the effectiveness of the auditing report.

2

Table of Contents

Introduction................................................................................................................................4

Research Rationale of Auditing Standard 701.......................................................................4

Explanation.............................................................................................................................5

Analysis..................................................................................................................................6

Efficiency of Key audit Matters.............................................................................................7

Auditing Standards of Commonwealth Bank.........................................................................8

Recommendations......................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................11

Appendix: Internal Control in Auditing..................................................................................13

3

Introduction................................................................................................................................4

Research Rationale of Auditing Standard 701.......................................................................4

Explanation.............................................................................................................................5

Analysis..................................................................................................................................6

Efficiency of Key audit Matters.............................................................................................7

Auditing Standards of Commonwealth Bank.........................................................................8

Recommendations......................................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................11

Appendix: Internal Control in Auditing..................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Internal auditing of an organization aids in the prevention of fraud in the organization. The

auditing report is prepared based on strict rules and regulations associated with the

company’s operation and internal controls. It aids in the prevention of accounting

irregularities that prevent the risk of material misstatement. The auditing of an organization is

related to the judgment of the professional auditors who provides with a financial assessment

of the organization based on the various existing resources. The study highlights the auditing

standard of ASA 701, which is considered for analyzing the key auditing factors associated

with Commonwealth Bank. It also discusses the auditing standard of the organization along

with the efficiency of ASA 701 in relation to Commonwealth Bank.

Research Rationale of Auditing Standard 701

Auditing standards are associated with internal assessment in order to evaluate the

effectiveness of the existing internal controls of the organization that limits the attaining

organization's business goals and objectives. As highlighted by Abdullatif and Kawuq (2015,

p.32), maintaining effective internal control is essential in order to align the company's

operation with the objectives of the organization as well as prevent misappropriation of its

assets. It aids in preventing fraud as well as aid in minimizing the costs associated with

capital.

Ineffective and inefficient auditing report of the Lehman brothers leads to the collapse of the

investment firm. The main issue related to the auditing report associated with the investment

firm was the lack of future projections related to the market boom in the housing sector. Lack

of implementation of the counter-strategies during fluctuations in market conditions enhanced

the risk associated with the liquefaction of the form. The report provided by the auditor's

failure to reveal as well as communicate the associated firm regarding repurchase agreement

transactions. As opined by Cordoş and Fülöp (2015, p.67), lack of effective auditing report

failed to maintain the organizations' constant inflow of capital to finance operations. In order

to address this issue, the policymakers implemented a new Standard on auditing, ASA 701,

which is related to communicating key audit matters (Refer to Appendix).

The Auditing Standards of ASA 701 is associated with auditing Key Communicating Matters

in Independent Auditor's Report was amended on 5th December 2018. The scope of the

auditing standard of ASA 701 encompasses the importance of the auditor's and their

4

Internal auditing of an organization aids in the prevention of fraud in the organization. The

auditing report is prepared based on strict rules and regulations associated with the

company’s operation and internal controls. It aids in the prevention of accounting

irregularities that prevent the risk of material misstatement. The auditing of an organization is

related to the judgment of the professional auditors who provides with a financial assessment

of the organization based on the various existing resources. The study highlights the auditing

standard of ASA 701, which is considered for analyzing the key auditing factors associated

with Commonwealth Bank. It also discusses the auditing standard of the organization along

with the efficiency of ASA 701 in relation to Commonwealth Bank.

Research Rationale of Auditing Standard 701

Auditing standards are associated with internal assessment in order to evaluate the

effectiveness of the existing internal controls of the organization that limits the attaining

organization's business goals and objectives. As highlighted by Abdullatif and Kawuq (2015,

p.32), maintaining effective internal control is essential in order to align the company's

operation with the objectives of the organization as well as prevent misappropriation of its

assets. It aids in preventing fraud as well as aid in minimizing the costs associated with

capital.

Ineffective and inefficient auditing report of the Lehman brothers leads to the collapse of the

investment firm. The main issue related to the auditing report associated with the investment

firm was the lack of future projections related to the market boom in the housing sector. Lack

of implementation of the counter-strategies during fluctuations in market conditions enhanced

the risk associated with the liquefaction of the form. The report provided by the auditor's

failure to reveal as well as communicate the associated firm regarding repurchase agreement

transactions. As opined by Cordoş and Fülöp (2015, p.67), lack of effective auditing report

failed to maintain the organizations' constant inflow of capital to finance operations. In order

to address this issue, the policymakers implemented a new Standard on auditing, ASA 701,

which is related to communicating key audit matters (Refer to Appendix).

The Auditing Standards of ASA 701 is associated with auditing Key Communicating Matters

in Independent Auditor's Report was amended on 5th December 2018. The scope of the

auditing standard of ASA 701 encompasses the importance of the auditor's and their

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

responsibility associated with the importance of communication key in audit report

(auasb.gov.au, 2019), the Standard on Auditing 701 is associated with International Standard

on Auditing (ISA). It aids in the enhancement of the communication value of the auditing

report. As opined by Cordoş and Fülöp (2015, p.78), improved communication in case of

auditing report aids in the enhancement of team cooperation and also provides better ideas

associated with the execution of business strategies. As highlighted by Liao and

Radhakrishnan (2015, p.34), the new auditing standard the professional auditors are expected

to adhere to the risk-based auditing system in order to reduce the risk associated with frauds.

● The Standard on Auditing, ASA 701, is the standards highlighted are associated with

the importance of communication to provide accurate judgment on current financial

issues.

● Matters are addressed based on the report of the financial. Statement.

● It also includes references on the basis of Qualifies (Adverse) Opinion.

● The auditor's report is also associated with governance.

Alignment of the auditing report of Commonwealth Bank with Standard on Auditing 701

helps to provide with insightful reports associated with functions of the bank. This

contributes to enhancing trust among the public sector as well as helps to attain stability. As

opined by Javaid and Javid (2018, p.12), in the era of globalization the world is reduced to a

global village in which people are adhering to attain global standards by convergence or by

adopting the various rules and regulations. The International Standard of auditing aids in the

improvement of auditory communication. It aids in regulating the accounting standard of

Commonwealth Bank that includes the regulatory requirements which affect the financial

statement of the group (commbank.com.au, 2019).

Explanation

Implementation of the new standards associated with ASA 701 included the importance of

effective communication in order to enhance transparency while providing the report

concerning Commonwealth Bank. Enhanced communication increases the flexibility and

enables to adhere to effective approaches to deal with different risks. As opined by Sirois et

al. (2018, p.13), the communicating key associated with ASA 701 in order to disclose the

matter associated with auditing it is essential to adhere to proper references to frame auditor

report. The accounting standards of ASA 701 helps the Commonwealth Bank helps to

maintain consistency in accounting policies (commbank.com.au, 2019). In order to adhere to

5

(auasb.gov.au, 2019), the Standard on Auditing 701 is associated with International Standard

on Auditing (ISA). It aids in the enhancement of the communication value of the auditing

report. As opined by Cordoş and Fülöp (2015, p.78), improved communication in case of

auditing report aids in the enhancement of team cooperation and also provides better ideas

associated with the execution of business strategies. As highlighted by Liao and

Radhakrishnan (2015, p.34), the new auditing standard the professional auditors are expected

to adhere to the risk-based auditing system in order to reduce the risk associated with frauds.

● The Standard on Auditing, ASA 701, is the standards highlighted are associated with

the importance of communication to provide accurate judgment on current financial

issues.

● Matters are addressed based on the report of the financial. Statement.

● It also includes references on the basis of Qualifies (Adverse) Opinion.

● The auditor's report is also associated with governance.

Alignment of the auditing report of Commonwealth Bank with Standard on Auditing 701

helps to provide with insightful reports associated with functions of the bank. This

contributes to enhancing trust among the public sector as well as helps to attain stability. As

opined by Javaid and Javid (2018, p.12), in the era of globalization the world is reduced to a

global village in which people are adhering to attain global standards by convergence or by

adopting the various rules and regulations. The International Standard of auditing aids in the

improvement of auditory communication. It aids in regulating the accounting standard of

Commonwealth Bank that includes the regulatory requirements which affect the financial

statement of the group (commbank.com.au, 2019).

Explanation

Implementation of the new standards associated with ASA 701 included the importance of

effective communication in order to enhance transparency while providing the report

concerning Commonwealth Bank. Enhanced communication increases the flexibility and

enables to adhere to effective approaches to deal with different risks. As opined by Sirois et

al. (2018, p.13), the communicating key associated with ASA 701 in order to disclose the

matter associated with auditing it is essential to adhere to proper references to frame auditor

report. The accounting standards of ASA 701 helps the Commonwealth Bank helps to

maintain consistency in accounting policies (commbank.com.au, 2019). In order to adhere to

5

appropriate disclosure, changes are implemented in the Bank's existing policies and also

provides with significant decisions based on the management financial statements of the

Commonwealth Bank (commbank.com.au, 2019).

Analysis

Development of Banking Assets

Effective management of the banking assets enhances the efficiency to maintain buffer

capital that increases the risk-taking capacity of the bank. Efficient auditing of the financial

report of the Commonwealth Bank and increased transparency helps to develop trust among

the public sector. As opined by Boolaky and Quick (2016, p.45), efficient communication

adopted by the professional auditors for providing effective financial report helps to gather

information regarding the various aspects. It aids in providing static data that helps to obtain

future projection with maximum accuracy. As opined by Abdullatif and Kawuq (2015, p.45),

the auditor's report of the Commonwealth Bank aids in developing better understanding

related to assurance framework that increases the comfort level associated with disclosure of

risks as well the services that are being provided by the bank. The auditor’s report related to

banks is associated with satisfaction and trust level of the public sector, which is increased by

enhancing the transparency level of Commonwealth Bank. As suggested by Zhang et al.

(2017, p.238), effective analysis of the buffer capital in Commonwealth Bank aids to provide

future projection regarding the risk-taking capability of the bank. The ASA 701 adheres to

determining the key audit matters that are highlighted in the financial statement of the

Commonwealth Bank. As opined by Francis et al. (2016, p.163), this helps the organization

to align to effective approach during a specific situation. This aids in the development of the

Commonwealth Bank by increasing the existing buffer capital.

Inventory Management

The auditor of Commonwealth Bank mainly focuses on different types of loans, mainly

focusing on the amounts estimated by the management and the potential risks associated with

the failure of repayment (commbank.com.au, 2019). The bank mainly adheres to account

inventories, which are calculated based on the working capital. As mentioned by Brunelli

(2018, p.89), inventory management of Commonwealth Bank is associated with the

management of stock as well as existing working capital. The completion of the loans is

judged by the collective impairment of assessment as well as specific impairment of

assessment. The auditors address the key issue based on the ageing of the loans by

6

provides with significant decisions based on the management financial statements of the

Commonwealth Bank (commbank.com.au, 2019).

Analysis

Development of Banking Assets

Effective management of the banking assets enhances the efficiency to maintain buffer

capital that increases the risk-taking capacity of the bank. Efficient auditing of the financial

report of the Commonwealth Bank and increased transparency helps to develop trust among

the public sector. As opined by Boolaky and Quick (2016, p.45), efficient communication

adopted by the professional auditors for providing effective financial report helps to gather

information regarding the various aspects. It aids in providing static data that helps to obtain

future projection with maximum accuracy. As opined by Abdullatif and Kawuq (2015, p.45),

the auditor's report of the Commonwealth Bank aids in developing better understanding

related to assurance framework that increases the comfort level associated with disclosure of

risks as well the services that are being provided by the bank. The auditor’s report related to

banks is associated with satisfaction and trust level of the public sector, which is increased by

enhancing the transparency level of Commonwealth Bank. As suggested by Zhang et al.

(2017, p.238), effective analysis of the buffer capital in Commonwealth Bank aids to provide

future projection regarding the risk-taking capability of the bank. The ASA 701 adheres to

determining the key audit matters that are highlighted in the financial statement of the

Commonwealth Bank. As opined by Francis et al. (2016, p.163), this helps the organization

to align to effective approach during a specific situation. This aids in the development of the

Commonwealth Bank by increasing the existing buffer capital.

Inventory Management

The auditor of Commonwealth Bank mainly focuses on different types of loans, mainly

focusing on the amounts estimated by the management and the potential risks associated with

the failure of repayment (commbank.com.au, 2019). The bank mainly adheres to account

inventories, which are calculated based on the working capital. As mentioned by Brunelli

(2018, p.89), inventory management of Commonwealth Bank is associated with the

management of stock as well as existing working capital. The completion of the loans is

judged by the collective impairment of assessment as well as specific impairment of

assessment. The auditors address the key issue based on the ageing of the loans by

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recalculating the time period for delinquency and the mode of repayment by the borrower. As

highlighted by Sirois et al. (2018, p.13), effective communication during auditing report

helps to attain transparency regarding the risk assessment of the banking sector by analyzing

the risks in a more efficient manner. Efficient inventory management and efficient auditor's

report helps to maintain effective capital management and stochastic cash flow

(commbank.com.au, 2019). As mentioned by Barrow and Kourentzes (2016, p.90), the

auditors mainly assess the reasonableness of the collateral associated with it that reduces the

risk of the financial crisis that leads to merger or closure of banks. By adhering to an effective

financial statement, it helps to assess the ongoing capacity of the bank on the basis of

management and accounting (commbank.com.au, 2019).

Liquidity and Funding

The ASA 701 mainly aligns with judgments based decision making by aligning the goals and

objective of the organization. Enhanced communication with the stakeholders as well as

employees of the Commonwealth Bank aids in the development of effective risk management

and increases transparency regarding the issues of the current financial year. As opined by

Pollard et al. (2018, p. 1249), regular meeting with the supervisor of the bank and the auditor

aids in an enhanced level of communication. This helps to enhance the exchange of

information between different individuals that helps to address the risks and provides with

new guidelines and related to it in significant ways. The Commonwealth Bank adheres to the

standards of auditing 701 associated with liquidation and funding (as influenced by Carnegie,

2016, p.398), aligning the auditing report with the new Standard of auditing 701 aids in

effective implementation of the communicating practices that aids in maintaining accurate

assumption as well as a consolidated entity.

The efficiency of Key Audit Matters

The Commonwealth Bank adhering to Standard of Auditing adhere to ASA 701 that aids in

the enhancement of communication among the auditor’s as well as the investors and

supervisors that helps to address the issues in a current financial year. As opined by Hay et al.

(2018, p.473), the alignment of the auditor’s report with the associated risks focusing on

current aspects aids in adhering to specific approach in order to overcome the same.

Commonwealth bank follows the new guideline that helps to maintain an effective inventory

that enhances the transparency related to the risk assessment of the bank. By aligning with the

current financial statement, it aids to develop future projection related to the risk-taking

7

highlighted by Sirois et al. (2018, p.13), effective communication during auditing report

helps to attain transparency regarding the risk assessment of the banking sector by analyzing

the risks in a more efficient manner. Efficient inventory management and efficient auditor's

report helps to maintain effective capital management and stochastic cash flow

(commbank.com.au, 2019). As mentioned by Barrow and Kourentzes (2016, p.90), the

auditors mainly assess the reasonableness of the collateral associated with it that reduces the

risk of the financial crisis that leads to merger or closure of banks. By adhering to an effective

financial statement, it helps to assess the ongoing capacity of the bank on the basis of

management and accounting (commbank.com.au, 2019).

Liquidity and Funding

The ASA 701 mainly aligns with judgments based decision making by aligning the goals and

objective of the organization. Enhanced communication with the stakeholders as well as

employees of the Commonwealth Bank aids in the development of effective risk management

and increases transparency regarding the issues of the current financial year. As opined by

Pollard et al. (2018, p. 1249), regular meeting with the supervisor of the bank and the auditor

aids in an enhanced level of communication. This helps to enhance the exchange of

information between different individuals that helps to address the risks and provides with

new guidelines and related to it in significant ways. The Commonwealth Bank adheres to the

standards of auditing 701 associated with liquidation and funding (as influenced by Carnegie,

2016, p.398), aligning the auditing report with the new Standard of auditing 701 aids in

effective implementation of the communicating practices that aids in maintaining accurate

assumption as well as a consolidated entity.

The efficiency of Key Audit Matters

The Commonwealth Bank adhering to Standard of Auditing adhere to ASA 701 that aids in

the enhancement of communication among the auditor’s as well as the investors and

supervisors that helps to address the issues in a current financial year. As opined by Hay et al.

(2018, p.473), the alignment of the auditor’s report with the associated risks focusing on

current aspects aids in adhering to specific approach in order to overcome the same.

Commonwealth bank follows the new guideline that helps to maintain an effective inventory

that enhances the transparency related to the risk assessment of the bank. By aligning with the

current financial statement, it aids to develop future projection related to the risk-taking

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capacity of the bank. As opined by Pollard et al. (2018, p. 1249), helps to exchange

information among the supervisor as well as the auditors.

Figure 1: Current Issues in Auditing

(Source: as influenced by Pollard et al. 2018, p. 1249)

Auditing Standards of Commonwealth Bank

The Commonwealth Bank adheres to the Standard on Auditing ASA 701 in order to enhance

the performance of the bank based on the current financial report as well as the management

system of the Commonwealth Bank. As opined by Brunelli (2018, p.90), the Commonwealth

Banking Group is structured into 7 segments that include the competencies level. It also

highlights the appropriate skills that are associated with each segment that is essential to deter

the risks associated with the same insignificant manner. In order to adhere to effective

auditing, the Commonwealth Group identified different entities as well as the business

activities associated with it in an effective manner (commbank.com.au, 2019).

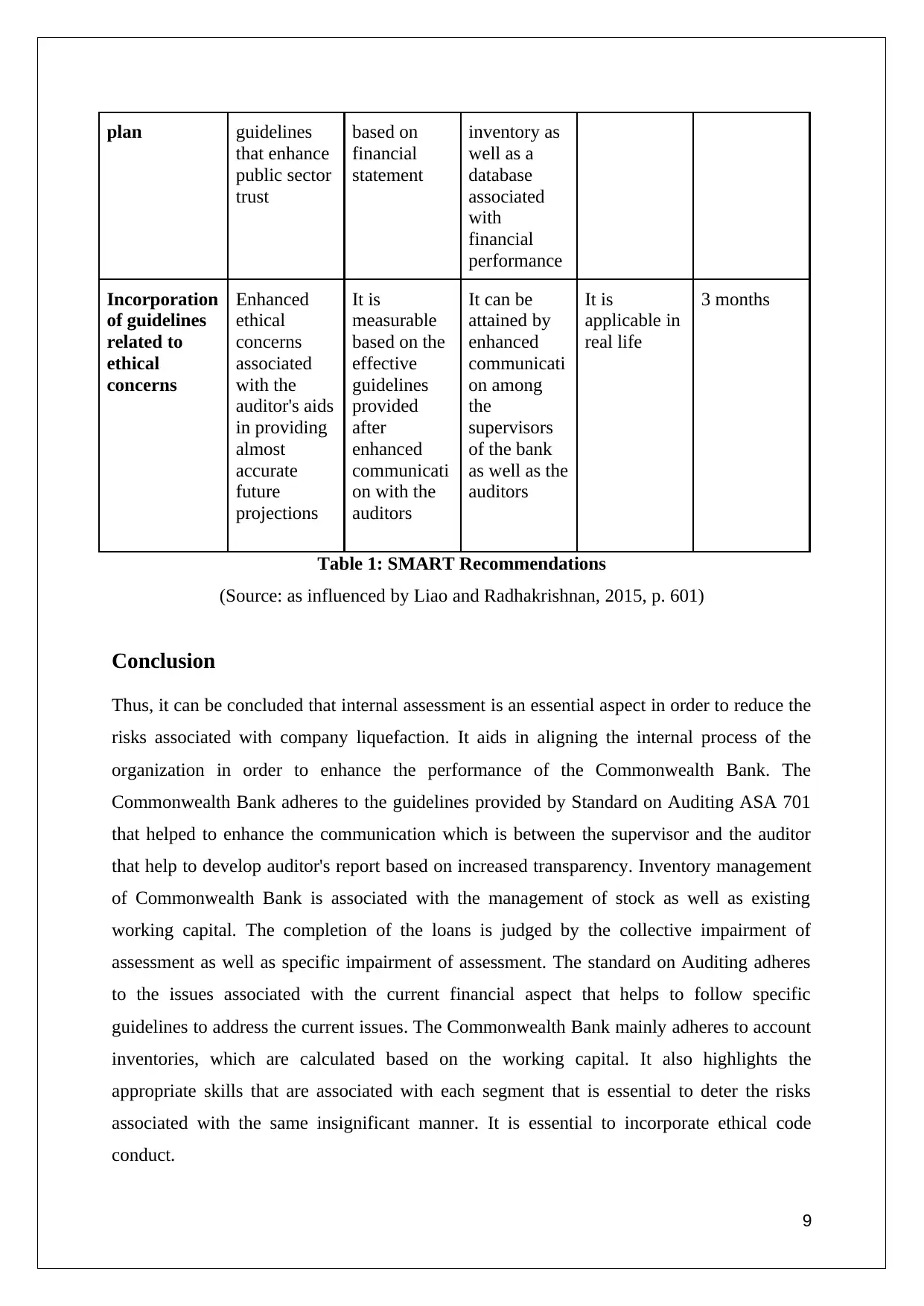

Recommendations

Objective Specific Measurable Attainable Realistic Time Period

Incorporation

of the

consumer

development

The

Commonwea

lth bank can

incorporate

It can be

measured by

analyzing the

performance

It can be

attained by

maintaining

effective

It is possible

in real life

application

6 months

8

Development of Banking Assets

Inventory Management

Liquidity and Funding

information among the supervisor as well as the auditors.

Figure 1: Current Issues in Auditing

(Source: as influenced by Pollard et al. 2018, p. 1249)

Auditing Standards of Commonwealth Bank

The Commonwealth Bank adheres to the Standard on Auditing ASA 701 in order to enhance

the performance of the bank based on the current financial report as well as the management

system of the Commonwealth Bank. As opined by Brunelli (2018, p.90), the Commonwealth

Banking Group is structured into 7 segments that include the competencies level. It also

highlights the appropriate skills that are associated with each segment that is essential to deter

the risks associated with the same insignificant manner. In order to adhere to effective

auditing, the Commonwealth Group identified different entities as well as the business

activities associated with it in an effective manner (commbank.com.au, 2019).

Recommendations

Objective Specific Measurable Attainable Realistic Time Period

Incorporation

of the

consumer

development

The

Commonwea

lth bank can

incorporate

It can be

measured by

analyzing the

performance

It can be

attained by

maintaining

effective

It is possible

in real life

application

6 months

8

Development of Banking Assets

Inventory Management

Liquidity and Funding

plan guidelines

that enhance

public sector

trust

based on

financial

statement

inventory as

well as a

database

associated

with

financial

performance

Incorporation

of guidelines

related to

ethical

concerns

Enhanced

ethical

concerns

associated

with the

auditor's aids

in providing

almost

accurate

future

projections

It is

measurable

based on the

effective

guidelines

provided

after

enhanced

communicati

on with the

auditors

It can be

attained by

enhanced

communicati

on among

the

supervisors

of the bank

as well as the

auditors

It is

applicable in

real life

3 months

Table 1: SMART Recommendations

(Source: as influenced by Liao and Radhakrishnan, 2015, p. 601)

Conclusion

Thus, it can be concluded that internal assessment is an essential aspect in order to reduce the

risks associated with company liquefaction. It aids in aligning the internal process of the

organization in order to enhance the performance of the Commonwealth Bank. The

Commonwealth Bank adheres to the guidelines provided by Standard on Auditing ASA 701

that helped to enhance the communication which is between the supervisor and the auditor

that help to develop auditor's report based on increased transparency. Inventory management

of Commonwealth Bank is associated with the management of stock as well as existing

working capital. The completion of the loans is judged by the collective impairment of

assessment as well as specific impairment of assessment. The standard on Auditing adheres

to the issues associated with the current financial aspect that helps to follow specific

guidelines to address the current issues. The Commonwealth Bank mainly adheres to account

inventories, which are calculated based on the working capital. It also highlights the

appropriate skills that are associated with each segment that is essential to deter the risks

associated with the same insignificant manner. It is essential to incorporate ethical code

conduct.

9

that enhance

public sector

trust

based on

financial

statement

inventory as

well as a

database

associated

with

financial

performance

Incorporation

of guidelines

related to

ethical

concerns

Enhanced

ethical

concerns

associated

with the

auditor's aids

in providing

almost

accurate

future

projections

It is

measurable

based on the

effective

guidelines

provided

after

enhanced

communicati

on with the

auditors

It can be

attained by

enhanced

communicati

on among

the

supervisors

of the bank

as well as the

auditors

It is

applicable in

real life

3 months

Table 1: SMART Recommendations

(Source: as influenced by Liao and Radhakrishnan, 2015, p. 601)

Conclusion

Thus, it can be concluded that internal assessment is an essential aspect in order to reduce the

risks associated with company liquefaction. It aids in aligning the internal process of the

organization in order to enhance the performance of the Commonwealth Bank. The

Commonwealth Bank adheres to the guidelines provided by Standard on Auditing ASA 701

that helped to enhance the communication which is between the supervisor and the auditor

that help to develop auditor's report based on increased transparency. Inventory management

of Commonwealth Bank is associated with the management of stock as well as existing

working capital. The completion of the loans is judged by the collective impairment of

assessment as well as specific impairment of assessment. The standard on Auditing adheres

to the issues associated with the current financial aspect that helps to follow specific

guidelines to address the current issues. The Commonwealth Bank mainly adheres to account

inventories, which are calculated based on the working capital. It also highlights the

appropriate skills that are associated with each segment that is essential to deter the risks

associated with the same insignificant manner. It is essential to incorporate ethical code

conduct.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Abdullatif, M. and Kawuq, S., (2015). The role of internal auditing in risk management:

evidence from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1),

pp.30-50.

Abdullatif, M. and Kawuq, S., (2015). The role of internal auditing in risk management:

evidence from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1),

pp.30-50.

auasb.gov.au (2019), Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report .Available

at:https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed on: 18.05.2019]

Barrow, D.K. and Kourentzes, N., (2016). Distributions of forecasting errors of forecast

combinations: implications for inventory management. International Journal of Production

Economics, 177, pp.24-33.

Bartlett, G.D., Kremin, J., Saunders, K.K. and Wood, D.A., (2016). Factors influencing

recruitment of non-accounting business professionals into internal auditing. Behavioral

Research in Accounting, 29(1), pp.119-130.

Boolaky, P.K., and Quick, R., (2016). Bank directors' perceptions of expanded auditor's

reports. International Journal of Auditing, 20(2), pp.158-174.

Brown, C.A., Davis, K.T. and Mayes, D.G., (2016). Regulatory change in Australia and New

Zealand following the global financial crisis. In The First Great Financial Crisis of the 21st

Century: A Retrospective (pp. 219-248).

Brunelli, S., (2018). Audit Reporting for Going Concern Uncertainty: Global Trends and the

Case Study of Italy. Springer.

Carnegie, G.D., (2016). The accounting professional project and bank failures: The case of

the early 1890s Australian banking crisis. Journal of Management History, 22(4), pp.389-

412.

commbank.com.au (2019), Annual Report 2018. Available

at:https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

results/fy18/cba-annual-report-2018.pdf [Accessed on: 18.05.2019]

commbank.com.au (2019), Commonwealth Bank of Australia. Available

at:https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/corporate-

10

Abdullatif, M. and Kawuq, S., (2015). The role of internal auditing in risk management:

evidence from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1),

pp.30-50.

Abdullatif, M. and Kawuq, S., (2015). The role of internal auditing in risk management:

evidence from banks in Jordan. Journal of Economic and Administrative Sciences, 31(1),

pp.30-50.

auasb.gov.au (2019), Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report .Available

at:https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed on: 18.05.2019]

Barrow, D.K. and Kourentzes, N., (2016). Distributions of forecasting errors of forecast

combinations: implications for inventory management. International Journal of Production

Economics, 177, pp.24-33.

Bartlett, G.D., Kremin, J., Saunders, K.K. and Wood, D.A., (2016). Factors influencing

recruitment of non-accounting business professionals into internal auditing. Behavioral

Research in Accounting, 29(1), pp.119-130.

Boolaky, P.K., and Quick, R., (2016). Bank directors' perceptions of expanded auditor's

reports. International Journal of Auditing, 20(2), pp.158-174.

Brown, C.A., Davis, K.T. and Mayes, D.G., (2016). Regulatory change in Australia and New

Zealand following the global financial crisis. In The First Great Financial Crisis of the 21st

Century: A Retrospective (pp. 219-248).

Brunelli, S., (2018). Audit Reporting for Going Concern Uncertainty: Global Trends and the

Case Study of Italy. Springer.

Carnegie, G.D., (2016). The accounting professional project and bank failures: The case of

the early 1890s Australian banking crisis. Journal of Management History, 22(4), pp.389-

412.

commbank.com.au (2019), Annual Report 2018. Available

at:https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

results/fy18/cba-annual-report-2018.pdf [Accessed on: 18.05.2019]

commbank.com.au (2019), Commonwealth Bank of Australia. Available

at:https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/corporate-

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profile/corporate-governance/Audit-Comittee-Charter-June-2018.pdf [Accessed on:

18.05.2019]

Cordoş, G.S. and Fülöp, M.T., (2015). Understanding audit reporting changes: introduction

of Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Francis, B.B., Hunter, D.M., Robinson, D.M., Robinson, M.N. and Yuan, X., (2016). Auditor

changes and the cost of bank debt. The Accounting Review, 92(3), pp.155-184.

Hay, D., Stewart, J. and Botica Redmayne, N., (2017). The role of auditing in corporate

governance in Australia and New Zealand: a research synthesis. Australian Accounting

Review, 27(4), pp.457-479.

Javaid, M.I. and Javid, A.Y., (2018). Efficacy of going concern prediction model for creditor

oriented regime via liquidation: A MDA approach. Journal of Applied Accounting

Research, 19(4), pp.552-573.

Liao, P.C. and Radhakrishnan, S., (2015). The effects of the auditor's insurance role on

reporting conservatism and audit quality. The Accounting Review, 91(2), pp.587-602.

Osma, B.G., Gisbert, A. and de las Heras Cristóbal, E., (2017). Public oversight systems for

statutory auditors in the European Union. European Journal of Law and Economics, 44(3),

pp.517-552.

Pollard, C., Mackintosh, B., Campbell, C., Kerr, D., Begley, A., Jancey, J., Caraher, M.,

Berg, J. and Booth, S., (2018). Charitable food systems’ capacity to address food insecurity:

An Australian capital city audit. International journal of environmental research and public

health, 15(6), p.1249.

Sirois, L.P., Bédard, J. and Bera, P., (2018). The informational value of key audit matters in

the auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2),

pp.141-162.

Zhang, Y., Sun, F. and Xian, C., (2017). Does auditor industry expertise affect bank loan

costs?. Managerial Auditing Journal, 32(3), pp.295-324.

11

18.05.2019]

Cordoş, G.S. and Fülöp, M.T., (2015). Understanding audit reporting changes: introduction

of Key Audit Matters. Accounting & Management Information Systems/Contabilitate si

Informatica de Gestiune, 14(1).

Francis, B.B., Hunter, D.M., Robinson, D.M., Robinson, M.N. and Yuan, X., (2016). Auditor

changes and the cost of bank debt. The Accounting Review, 92(3), pp.155-184.

Hay, D., Stewart, J. and Botica Redmayne, N., (2017). The role of auditing in corporate

governance in Australia and New Zealand: a research synthesis. Australian Accounting

Review, 27(4), pp.457-479.

Javaid, M.I. and Javid, A.Y., (2018). Efficacy of going concern prediction model for creditor

oriented regime via liquidation: A MDA approach. Journal of Applied Accounting

Research, 19(4), pp.552-573.

Liao, P.C. and Radhakrishnan, S., (2015). The effects of the auditor's insurance role on

reporting conservatism and audit quality. The Accounting Review, 91(2), pp.587-602.

Osma, B.G., Gisbert, A. and de las Heras Cristóbal, E., (2017). Public oversight systems for

statutory auditors in the European Union. European Journal of Law and Economics, 44(3),

pp.517-552.

Pollard, C., Mackintosh, B., Campbell, C., Kerr, D., Begley, A., Jancey, J., Caraher, M.,

Berg, J. and Booth, S., (2018). Charitable food systems’ capacity to address food insecurity:

An Australian capital city audit. International journal of environmental research and public

health, 15(6), p.1249.

Sirois, L.P., Bédard, J. and Bera, P., (2018). The informational value of key audit matters in

the auditor's report: Evidence from an eye-tracking study. Accounting Horizons, 32(2),

pp.141-162.

Zhang, Y., Sun, F. and Xian, C., (2017). Does auditor industry expertise affect bank loan

costs?. Managerial Auditing Journal, 32(3), pp.295-324.

11

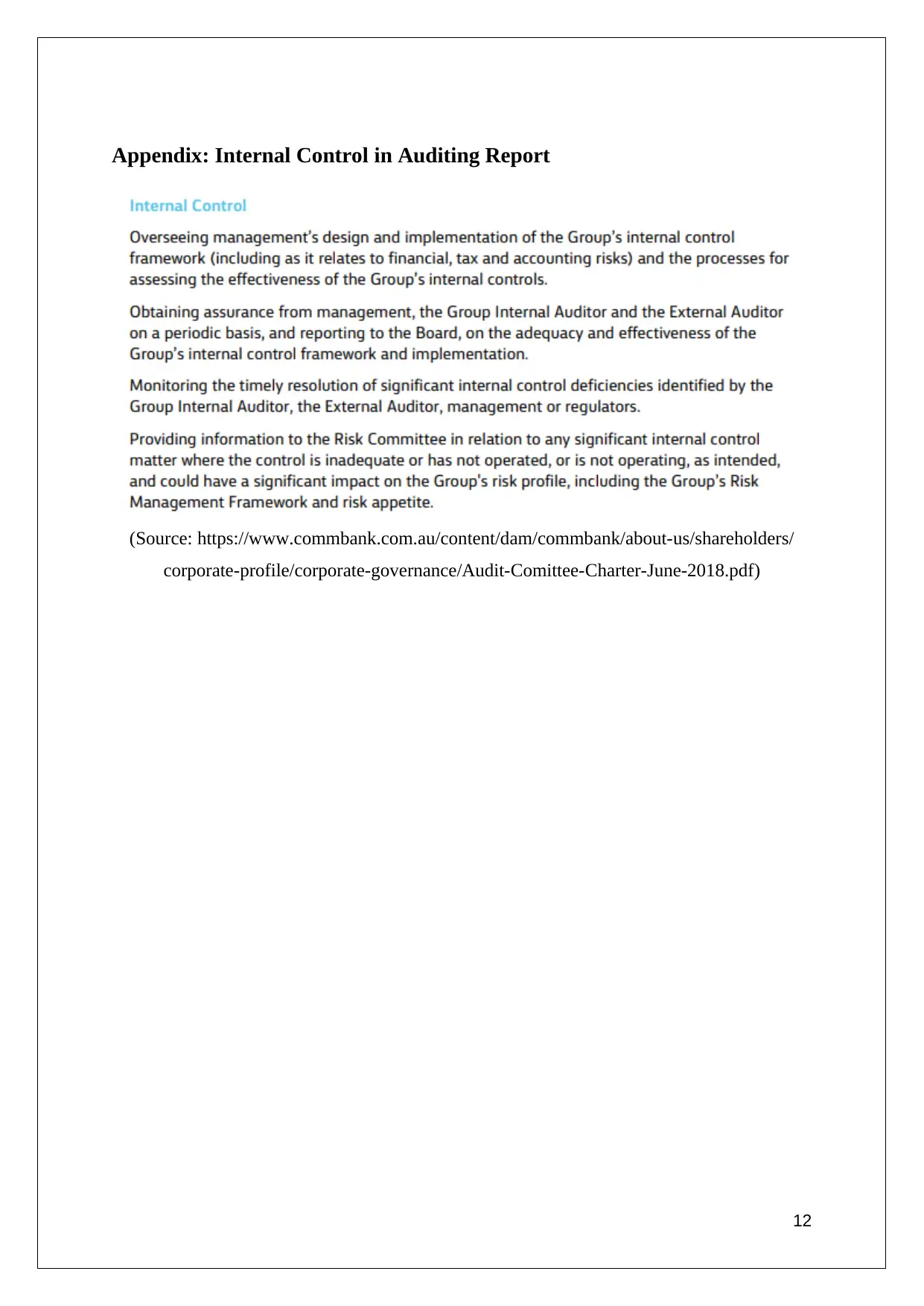

Appendix: Internal Control in Auditing Report

(Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

corporate-profile/corporate-governance/Audit-Comittee-Charter-June-2018.pdf)

12

(Source: https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/

corporate-profile/corporate-governance/Audit-Comittee-Charter-June-2018.pdf)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.