Audit and Non-Audit Services Report - University Finance Module

VerifiedAdded on 2023/01/23

|17

|5519

|42

Report

AI Summary

This report, prepared for a Masters of Accounting and Finance assignment, delves into the critical aspects of audit and non-audit services. Part 1 provides an executive summary, introduction, discussion and analysis, and conclusion regarding the provision of audit and non-audit services by auditors, examining the perspectives of both clients and accounting councils, and discussing the potential conflicts of interest and independence issues that can arise. Part 2 focuses on a planning memorandum for Myer Holdings Limited, analyzing major risks, performing horizontal and ratio analysis, identifying inherent risks, assessing key accounts and related assertions at risk of material misstatement, and defining materiality. The report highlights the complexities and challenges in maintaining auditor independence and the implications of providing non-audit services, especially considering the case of Myer Holdings Limited. The report also analyzes the quality of audit and the importance of auditor's independence.

MASTERS OF

ACCOUNTING AND

FINANCE

ASSIGNMENT

ACCOUNTING AND

FINANCE

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Part 1...........................................................................................................................................................3

Executive Summary.................................................................................................................................3

Introduction.............................................................................................................................................3

Discussion and Analysis...........................................................................................................................3

Conclusion and Recommendation...........................................................................................................5

Part 2...........................................................................................................................................................6

Background of the audit..........................................................................................................................6

Discussion and Analysis...........................................................................................................................6

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

2 | P a g e

Contents

Part 1...........................................................................................................................................................3

Executive Summary.................................................................................................................................3

Introduction.............................................................................................................................................3

Discussion and Analysis...........................................................................................................................3

Conclusion and Recommendation...........................................................................................................5

Part 2...........................................................................................................................................................6

Background of the audit..........................................................................................................................6

Discussion and Analysis...........................................................................................................................6

References.................................................................................................................................................12

Appendix...................................................................................................................................................14

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Part 1

Report for Financial Reporting Council

Executive Summary

A business report has been prepared on the topic audit and non-audit services offered by the auditors to

the clients. The report distinguishes between the two and shows the advantages and disadvantages of

engaging the auditor to perform the non-audit services from the perspective of the client or the

company. The report also mentions the views and opinion of the various distinguished groups of

accounting and councils and finally the conclusion has been given as to whether the auditors should be

prohibited from providing the non-audit services to the audit clients (Alieid, 2016).

Introduction

There have been several studies on the audit and non-audit services being conducted by the statutory

auditors of the company because of which there have been several independence issues in the past and

thereby the true and fair view has been compromised with in the audit report. The auditors in such a

scenario are basically biased towards the client and therefore companies like Enron, WorldCom and

Satyam has collapsed over the years. Recently, there was an update and recommendation from

Competition and Markets Authority’s Audit Services Market Study (CMA) in UK where they proposed for

separation of the audit and non-audit services into different legal entities within the audit firm so as to

ensure independence. The proposal is under discussion and consideration by Financial Reporting Council

(FRC) in Australia (Ehalaiye, et al., 2018).

Discussion and Analysis

Audit firms may be asked to provide the non-audit services to the client or company which may not

involve giving an opinion on the financial statements. Audit is an independent examination of the books

of accounts whether profit making or not, private or public, to give an opinion on the true and fair view

of the books of accounts prepared by the entity. It is a statutory requirement which is compulsory as per

law and has different laws and regulations stated for same in Corporation Act, 2001. During the audit,

the auditor has an obligation to express his opinion thereon on the financial statements and the auditor

has to comply with IFRS and local legislations. Typically it involves assessment of the risks in business,

assessment of the adequacy and sufficiency of internal controls, obtaining evidence on the stated

assertions, designing procedures to detect errors and frauds and to consider and assess if the client is a

going concern entity (Defond & Lennox, 2017).

On the other hand, the non-audit services are voluntary and the scope of the work is usually not defined

by any statute and is generally as per the agreement between the entity and the audit firm. By

definition, non-audit services are the professional services rendered by the audit firm during the audit

engagement period but the work is not connected with the audit or review of the financial statements.

Some of the such non-audit services include book keeping, tax filing services, valuation and appraisal

services, internal audit outsourcing services, actuarial services, management and human resource

function related services, implementation of system or software, legal and other expert services other

3 | P a g e

Part 1

Report for Financial Reporting Council

Executive Summary

A business report has been prepared on the topic audit and non-audit services offered by the auditors to

the clients. The report distinguishes between the two and shows the advantages and disadvantages of

engaging the auditor to perform the non-audit services from the perspective of the client or the

company. The report also mentions the views and opinion of the various distinguished groups of

accounting and councils and finally the conclusion has been given as to whether the auditors should be

prohibited from providing the non-audit services to the audit clients (Alieid, 2016).

Introduction

There have been several studies on the audit and non-audit services being conducted by the statutory

auditors of the company because of which there have been several independence issues in the past and

thereby the true and fair view has been compromised with in the audit report. The auditors in such a

scenario are basically biased towards the client and therefore companies like Enron, WorldCom and

Satyam has collapsed over the years. Recently, there was an update and recommendation from

Competition and Markets Authority’s Audit Services Market Study (CMA) in UK where they proposed for

separation of the audit and non-audit services into different legal entities within the audit firm so as to

ensure independence. The proposal is under discussion and consideration by Financial Reporting Council

(FRC) in Australia (Ehalaiye, et al., 2018).

Discussion and Analysis

Audit firms may be asked to provide the non-audit services to the client or company which may not

involve giving an opinion on the financial statements. Audit is an independent examination of the books

of accounts whether profit making or not, private or public, to give an opinion on the true and fair view

of the books of accounts prepared by the entity. It is a statutory requirement which is compulsory as per

law and has different laws and regulations stated for same in Corporation Act, 2001. During the audit,

the auditor has an obligation to express his opinion thereon on the financial statements and the auditor

has to comply with IFRS and local legislations. Typically it involves assessment of the risks in business,

assessment of the adequacy and sufficiency of internal controls, obtaining evidence on the stated

assertions, designing procedures to detect errors and frauds and to consider and assess if the client is a

going concern entity (Defond & Lennox, 2017).

On the other hand, the non-audit services are voluntary and the scope of the work is usually not defined

by any statute and is generally as per the agreement between the entity and the audit firm. By

definition, non-audit services are the professional services rendered by the audit firm during the audit

engagement period but the work is not connected with the audit or review of the financial statements.

Some of the such non-audit services include book keeping, tax filing services, valuation and appraisal

services, internal audit outsourcing services, actuarial services, management and human resource

function related services, implementation of system or software, legal and other expert services other

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

than audit, information system design, advocacy or litigation services on behalf of the client (DeZoort &

Harrison, 2016).

From the perspective of the company, when the auditor provides the non-audit services as well, the

company gets closer to the auditor and the auditor is more or less dependent on these non-audit

services for extra revenue. In this way, the client can supersede the interests of the auditor and can

influence their decision in the audit report in some or the other way. This makes the company attractive

avenue for the auditor in terms of bundled services so even though the auditor may be rotated after a

period of 5 or 10 years as per the laws and regulations, the auditor is still associated with the company

in terms of non-audit services (Bailey, et al., 2017). This also helps the company in getting non-audit

services being performed at lower cost as compared to the market rates. In case any deficiency in found

in the internal control or internal audit or in information system of the company , it is easier to convince

the auditor rather than in the scenario if the audit would have been performed by another auditor. In

some cases, clients also threaten to change the auditor if they do not get the favourable result of the

company’s audit report. Furthermore if there is any deficiency in the internal control system or the

financial system, the same can be settled internally with the auditor without being highlight to the

investor and other stakeholders in the annual report which helps in saving the goodwill and reputation

of the company and thereby affecting adversely to the share prices. One of the other advantages of this

is that all the inefficiencies pointed out in statutory audit can be resolved internally in advance if the

non-audit services like internal audit is also being done by the same auditor (Gassen & Schwedler, 2010).

On the other hand, there are several disadvantages as well to the company. Some of them being the

possibility of impaired report as the independence of the auditor is compromised in some way or the

other and he is bound to give the biased report. The same was the case of Arthur Anderson in case of

Enron scandal and PWC in case of Satyam. Furthermore, the professional scepticism of the auditor is

being compromised in this case and the chances of erroneous report increases, which may lead to loss

of goodwill and credibility of the company in the eyes of the stakeholders and investors if the faulty

audit report is being issued (Sonu, et al., 2017). This may also lead to non-correction of the internal

control issues, if any in the entity as the same might not be reported to the client. This may also lead to

huge penalties and loss for the company in future when the same is disclosed publically in the future

and the company might land up in the position of liquidation or bankruptcy as it may not come to know

the overall risks in the financial and internal system of the company.

As regards the decision on whether the auditors should be prohibited from providing the non-audit

services to their audit client, the discussion is wide and non-ending. There can be several advantages as

well as disadvantages of this scenario both to the entity in question as well as the auditors but it all

depends on the approach of the client entity and professional scepticism and independence being

practices by the auditor. The audit work conducted by the big 4 consulting firms have come under

scrutiny and the joint committee on corporations and financial services mentioned that the audit quality

over the past few years has deteriorated and that there should be a “serious review” mechanism for the

audit which has encountered several issues due to market dominance and conflict of interest that arises

due to the range of other activities being conducted by these firms apart from audit (Hoopes, et al.,

2012). It also mentioned that the big 4 firms have become corporate insiders rather than the

4 | P a g e

than audit, information system design, advocacy or litigation services on behalf of the client (DeZoort &

Harrison, 2016).

From the perspective of the company, when the auditor provides the non-audit services as well, the

company gets closer to the auditor and the auditor is more or less dependent on these non-audit

services for extra revenue. In this way, the client can supersede the interests of the auditor and can

influence their decision in the audit report in some or the other way. This makes the company attractive

avenue for the auditor in terms of bundled services so even though the auditor may be rotated after a

period of 5 or 10 years as per the laws and regulations, the auditor is still associated with the company

in terms of non-audit services (Bailey, et al., 2017). This also helps the company in getting non-audit

services being performed at lower cost as compared to the market rates. In case any deficiency in found

in the internal control or internal audit or in information system of the company , it is easier to convince

the auditor rather than in the scenario if the audit would have been performed by another auditor. In

some cases, clients also threaten to change the auditor if they do not get the favourable result of the

company’s audit report. Furthermore if there is any deficiency in the internal control system or the

financial system, the same can be settled internally with the auditor without being highlight to the

investor and other stakeholders in the annual report which helps in saving the goodwill and reputation

of the company and thereby affecting adversely to the share prices. One of the other advantages of this

is that all the inefficiencies pointed out in statutory audit can be resolved internally in advance if the

non-audit services like internal audit is also being done by the same auditor (Gassen & Schwedler, 2010).

On the other hand, there are several disadvantages as well to the company. Some of them being the

possibility of impaired report as the independence of the auditor is compromised in some way or the

other and he is bound to give the biased report. The same was the case of Arthur Anderson in case of

Enron scandal and PWC in case of Satyam. Furthermore, the professional scepticism of the auditor is

being compromised in this case and the chances of erroneous report increases, which may lead to loss

of goodwill and credibility of the company in the eyes of the stakeholders and investors if the faulty

audit report is being issued (Sonu, et al., 2017). This may also lead to non-correction of the internal

control issues, if any in the entity as the same might not be reported to the client. This may also lead to

huge penalties and loss for the company in future when the same is disclosed publically in the future

and the company might land up in the position of liquidation or bankruptcy as it may not come to know

the overall risks in the financial and internal system of the company.

As regards the decision on whether the auditors should be prohibited from providing the non-audit

services to their audit client, the discussion is wide and non-ending. There can be several advantages as

well as disadvantages of this scenario both to the entity in question as well as the auditors but it all

depends on the approach of the client entity and professional scepticism and independence being

practices by the auditor. The audit work conducted by the big 4 consulting firms have come under

scrutiny and the joint committee on corporations and financial services mentioned that the audit quality

over the past few years has deteriorated and that there should be a “serious review” mechanism for the

audit which has encountered several issues due to market dominance and conflict of interest that arises

due to the range of other activities being conducted by these firms apart from audit (Hoopes, et al.,

2012). It also mentioned that the big 4 firms have become corporate insiders rather than the

4 | P a g e

5

independent outsiders scrutinising the accounts of the company. They fail to fearlessly audit and

scrutinise the accounts as that may prove to be detrimental to the business interests of these consulting

firms. As per one of the surveys 95% of the companies on ASX200 is being audited by Big 4 but the

revenue share of these firms from audit has come down drastically to 14% and 21% in the last financial

years. The statutory audits have become more of side business when compared to the consulting and

non-audit services being provided by them. In Australia, there has been a conflict on the quality of audit

between ASIC and FRC and it has been found that in one out of every 5 audits, there is no sufficient

assurance that the financial statements are free from error and it is mainly because of the non-

independence due to provision of non-audit services. All these issues have led to increased chances of

risk with audit reports and its viability for decision making purposes (Mubako & O'Donnell, 2018). The

local arms of the big 4 consulting firms in Australia have rejected the proposal of their UK counterparts

to stop providing the non-audit services to large listed companies. The UK big 4 consulting firms have

stopped providing the non-audit services to their clients as per one of the recently conducted studies.

Conclusion and Recommendation

From the above discussion and analysis, it can be said that banning of the non-audit services all together

can be detrimental to the interest of the Big 4 consulting firms. Therefore, if adequate safeguards are

being ensured, both these types of services can benefit the client as well as the accounting and auditing

profession as a whole. Furthermore, in line with the discussion made above, the ideal scenario would be

that the non-audit services should not be banned all together instead only those services should be

banned that is likely to impair the integrity, objectivity and independence of the auditor. In that case,

the interest of both the parties can be sustained and it will also help serving the profession of

accounting and auditing well.

5 | P a g e

independent outsiders scrutinising the accounts of the company. They fail to fearlessly audit and

scrutinise the accounts as that may prove to be detrimental to the business interests of these consulting

firms. As per one of the surveys 95% of the companies on ASX200 is being audited by Big 4 but the

revenue share of these firms from audit has come down drastically to 14% and 21% in the last financial

years. The statutory audits have become more of side business when compared to the consulting and

non-audit services being provided by them. In Australia, there has been a conflict on the quality of audit

between ASIC and FRC and it has been found that in one out of every 5 audits, there is no sufficient

assurance that the financial statements are free from error and it is mainly because of the non-

independence due to provision of non-audit services. All these issues have led to increased chances of

risk with audit reports and its viability for decision making purposes (Mubako & O'Donnell, 2018). The

local arms of the big 4 consulting firms in Australia have rejected the proposal of their UK counterparts

to stop providing the non-audit services to large listed companies. The UK big 4 consulting firms have

stopped providing the non-audit services to their clients as per one of the recently conducted studies.

Conclusion and Recommendation

From the above discussion and analysis, it can be said that banning of the non-audit services all together

can be detrimental to the interest of the Big 4 consulting firms. Therefore, if adequate safeguards are

being ensured, both these types of services can benefit the client as well as the accounting and auditing

profession as a whole. Furthermore, in line with the discussion made above, the ideal scenario would be

that the non-audit services should not be banned all together instead only those services should be

banned that is likely to impair the integrity, objectivity and independence of the auditor. In that case,

the interest of both the parties can be sustained and it will also help serving the profession of

accounting and auditing well.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Part 2

Memorandum

To: XYXYXYXYX, Audit Partner

From: ZZZZZZZZZ, Senior Analyst

Date: 18th April, 2018

Subject: Planning memorandum for the company Myer Holdings Limited

Background of the audit

In the given case, an audit planning memorandum is prepared for the audit partner for the company

Myer Holding Limited for the year 2016. The memo highlights the major risks to the company and the

reason as to why the same is risk for the company. The analytical procedure has been performed by the

way of horizontal analysis as well as ratio analysis of the company. It also mentions the inherent risk in

the business that are being identified from the analytical procedures. One of the key accounts has been

identified and the related assertion being at risk of material misstatement has been stated in the memo.

As assessment of the overall inherent risk in the company has been conducted and materiality has been

defined in absolute amount by the way of workings. This memo is intended to help the audit team in

planning the audit of the entity in hand (Henderson, et al., 2014).

Discussion and Analysis

The company being analysed here is Myer Holdings Limited which is listed on the Australian Stock

exchange. The company is an upmarket departmental store chain operating in all the states of Australia.

It deals in a range of products including men, women, children clothing, accessories and footwear,

computer, electrical, cosmetic, furniture, toys, books, confectionary, food, travel, homewares and

flooring and bedding material, etc. The company was established in the year 1900 and employs over

14000 people (Choy, 2018).

a. Some of the major risks for the company are mentioned below:

i. Huge investment in New Myer: the company is making a huge investment in the new in-

store and Omni channel experiences in accordance with the 5 year strategy of the

company but it is not sure as to when the company will be able to retrieve the returns

out of it. The company also made a huge investment in the world’s first virtual reality

store launched in Christmas in partnership with eBay. The opening of the Warringah

store in November 2016 is another milestone as it is representative of true embodiment

of the customer led strategy. But all this can have a severe impact on the cash flows of

the company (Werner, 2017). There is huge capital expenditure in the years to come by

and therefore the same may also have a negative impact on the cash flows.

6 | P a g e

Part 2

Memorandum

To: XYXYXYXYX, Audit Partner

From: ZZZZZZZZZ, Senior Analyst

Date: 18th April, 2018

Subject: Planning memorandum for the company Myer Holdings Limited

Background of the audit

In the given case, an audit planning memorandum is prepared for the audit partner for the company

Myer Holding Limited for the year 2016. The memo highlights the major risks to the company and the

reason as to why the same is risk for the company. The analytical procedure has been performed by the

way of horizontal analysis as well as ratio analysis of the company. It also mentions the inherent risk in

the business that are being identified from the analytical procedures. One of the key accounts has been

identified and the related assertion being at risk of material misstatement has been stated in the memo.

As assessment of the overall inherent risk in the company has been conducted and materiality has been

defined in absolute amount by the way of workings. This memo is intended to help the audit team in

planning the audit of the entity in hand (Henderson, et al., 2014).

Discussion and Analysis

The company being analysed here is Myer Holdings Limited which is listed on the Australian Stock

exchange. The company is an upmarket departmental store chain operating in all the states of Australia.

It deals in a range of products including men, women, children clothing, accessories and footwear,

computer, electrical, cosmetic, furniture, toys, books, confectionary, food, travel, homewares and

flooring and bedding material, etc. The company was established in the year 1900 and employs over

14000 people (Choy, 2018).

a. Some of the major risks for the company are mentioned below:

i. Huge investment in New Myer: the company is making a huge investment in the new in-

store and Omni channel experiences in accordance with the 5 year strategy of the

company but it is not sure as to when the company will be able to retrieve the returns

out of it. The company also made a huge investment in the world’s first virtual reality

store launched in Christmas in partnership with eBay. The opening of the Warringah

store in November 2016 is another milestone as it is representative of true embodiment

of the customer led strategy. But all this can have a severe impact on the cash flows of

the company (Werner, 2017). There is huge capital expenditure in the years to come by

and therefore the same may also have a negative impact on the cash flows.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

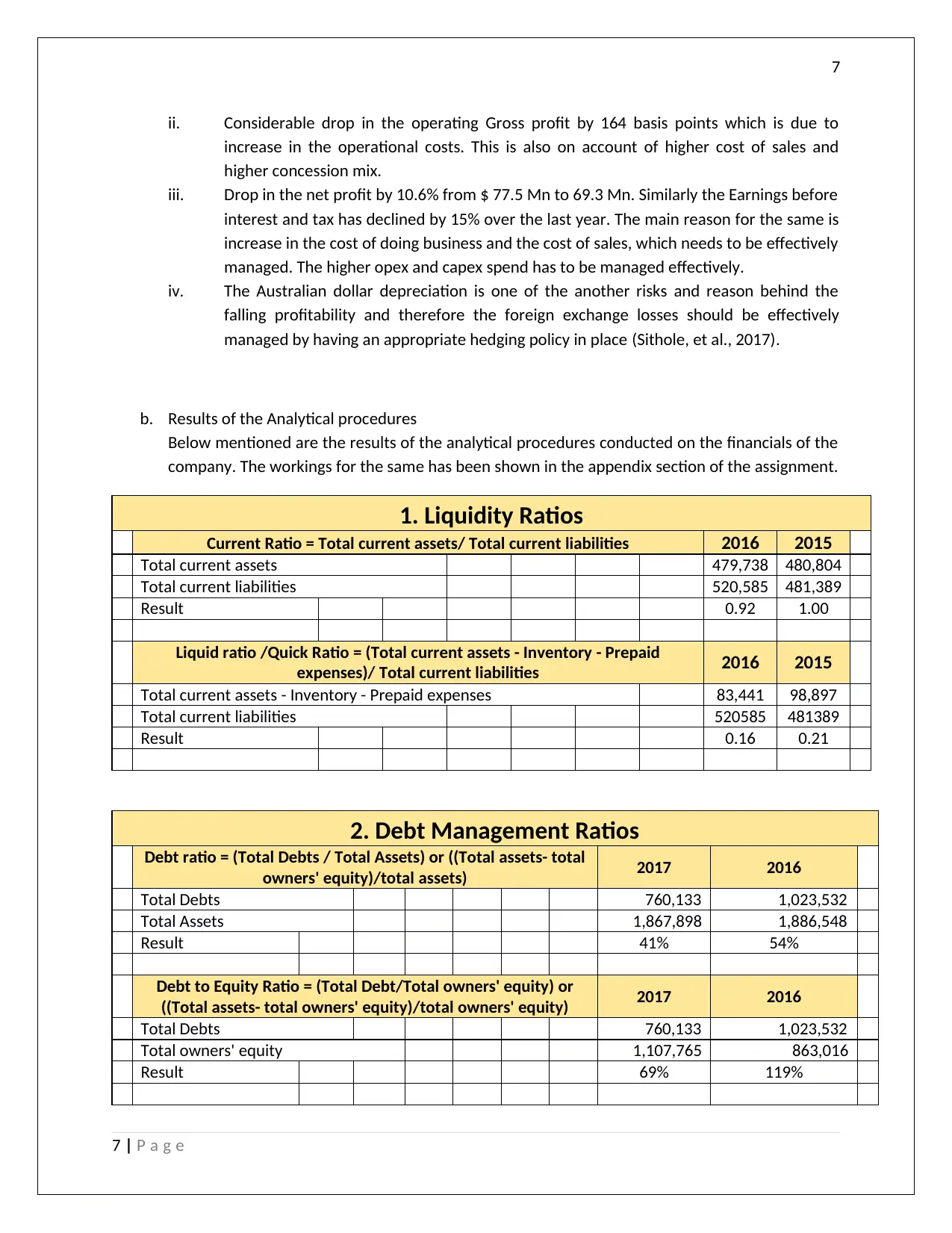

ii. Considerable drop in the operating Gross profit by 164 basis points which is due to

increase in the operational costs. This is also on account of higher cost of sales and

higher concession mix.

iii. Drop in the net profit by 10.6% from $ 77.5 Mn to 69.3 Mn. Similarly the Earnings before

interest and tax has declined by 15% over the last year. The main reason for the same is

increase in the cost of doing business and the cost of sales, which needs to be effectively

managed. The higher opex and capex spend has to be managed effectively.

iv. The Australian dollar depreciation is one of the another risks and reason behind the

falling profitability and therefore the foreign exchange losses should be effectively

managed by having an appropriate hedging policy in place (Sithole, et al., 2017).

b. Results of the Analytical procedures

Below mentioned are the results of the analytical procedures conducted on the financials of the

company. The workings for the same has been shown in the appendix section of the assignment.

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2016 2015

Total current assets 479,738 480,804

Total current liabilities 520,585 481,389

Result 0.92 1.00

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities 2016 2015

Total current assets - Inventory - Prepaid expenses 83,441 98,897

Total current liabilities 520585 481389

Result 0.16 0.21

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total

owners' equity)/total assets) 2017 2016

Total Debts 760,133 1,023,532

Total Assets 1,867,898 1,886,548

Result 41% 54%

Debt to Equity Ratio = (Total Debt/Total owners' equity) or

((Total assets- total owners' equity)/total owners' equity) 2017 2016

Total Debts 760,133 1,023,532

Total owners' equity 1,107,765 863,016

Result 69% 119%

7 | P a g e

ii. Considerable drop in the operating Gross profit by 164 basis points which is due to

increase in the operational costs. This is also on account of higher cost of sales and

higher concession mix.

iii. Drop in the net profit by 10.6% from $ 77.5 Mn to 69.3 Mn. Similarly the Earnings before

interest and tax has declined by 15% over the last year. The main reason for the same is

increase in the cost of doing business and the cost of sales, which needs to be effectively

managed. The higher opex and capex spend has to be managed effectively.

iv. The Australian dollar depreciation is one of the another risks and reason behind the

falling profitability and therefore the foreign exchange losses should be effectively

managed by having an appropriate hedging policy in place (Sithole, et al., 2017).

b. Results of the Analytical procedures

Below mentioned are the results of the analytical procedures conducted on the financials of the

company. The workings for the same has been shown in the appendix section of the assignment.

1. Liquidity Ratios

Current Ratio = Total current assets/ Total current liabilities 2016 2015

Total current assets 479,738 480,804

Total current liabilities 520,585 481,389

Result 0.92 1.00

Liquid ratio /Quick Ratio = (Total current assets - Inventory - Prepaid

expenses)/ Total current liabilities 2016 2015

Total current assets - Inventory - Prepaid expenses 83,441 98,897

Total current liabilities 520585 481389

Result 0.16 0.21

2. Debt Management Ratios

Debt ratio = (Total Debts / Total Assets) or ((Total assets- total

owners' equity)/total assets) 2017 2016

Total Debts 760,133 1,023,532

Total Assets 1,867,898 1,886,548

Result 41% 54%

Debt to Equity Ratio = (Total Debt/Total owners' equity) or

((Total assets- total owners' equity)/total owners' equity) 2017 2016

Total Debts 760,133 1,023,532

Total owners' equity 1,107,765 863,016

Result 69% 119%

7 | P a g e

8

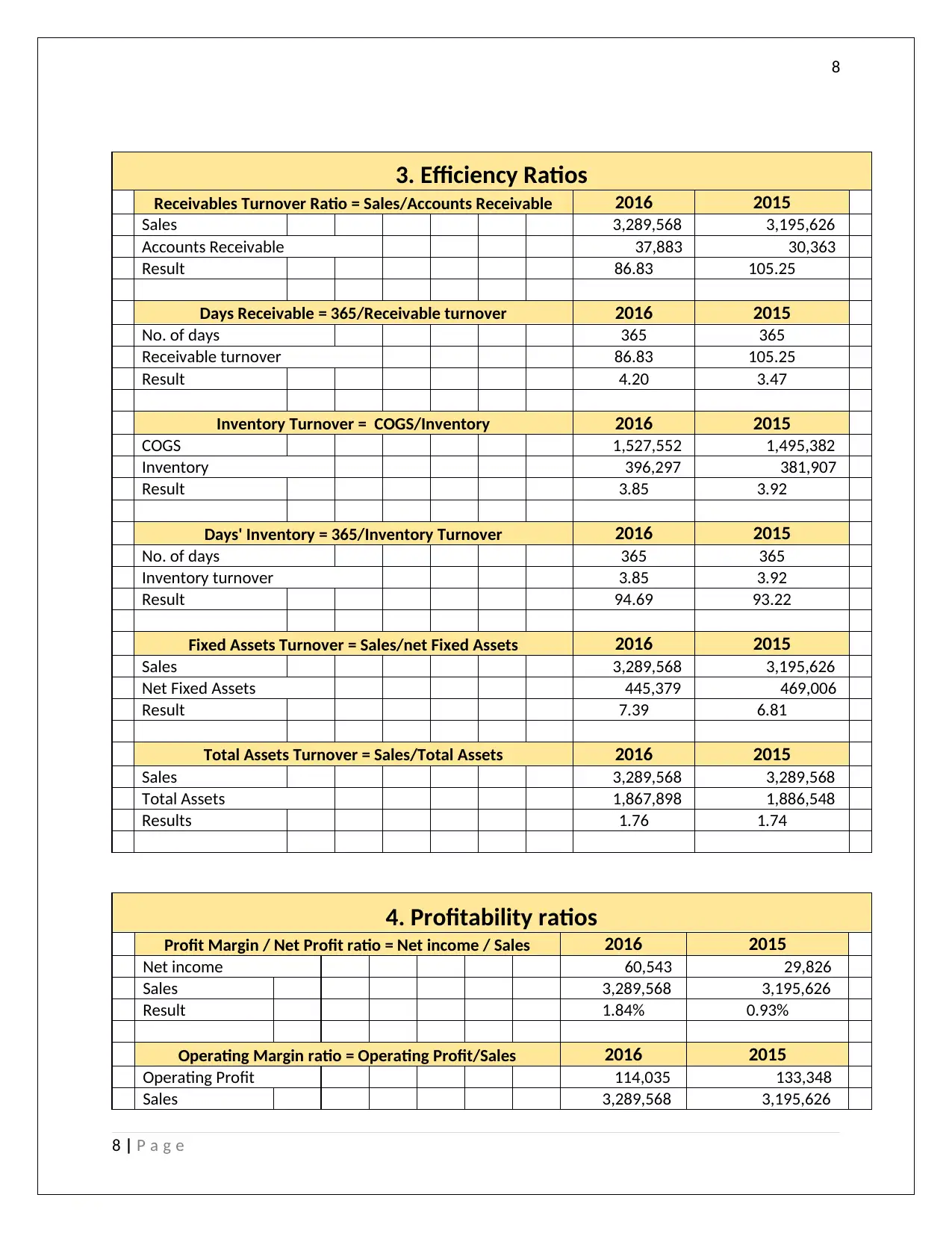

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2016 2015

Sales 3,289,568 3,195,626

Accounts Receivable 37,883 30,363

Result 86.83 105.25

Days Receivable = 365/Receivable turnover 2016 2015

No. of days 365 365

Receivable turnover 86.83 105.25

Result 4.20 3.47

Inventory Turnover = COGS/Inventory 2016 2015

COGS 1,527,552 1,495,382

Inventory 396,297 381,907

Result 3.85 3.92

Days' Inventory = 365/Inventory Turnover 2016 2015

No. of days 365 365

Inventory turnover 3.85 3.92

Result 94.69 93.22

Fixed Assets Turnover = Sales/net Fixed Assets 2016 2015

Sales 3,289,568 3,195,626

Net Fixed Assets 445,379 469,006

Result 7.39 6.81

Total Assets Turnover = Sales/Total Assets 2016 2015

Sales 3,289,568 3,289,568

Total Assets 1,867,898 1,886,548

Results 1.76 1.74

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales 2016 2015

Net income 60,543 29,826

Sales 3,289,568 3,195,626

Result 1.84% 0.93%

Operating Margin ratio = Operating Profit/Sales 2016 2015

Operating Profit 114,035 133,348

Sales 3,289,568 3,195,626

8 | P a g e

3. Efficiency Ratios

Receivables Turnover Ratio = Sales/Accounts Receivable 2016 2015

Sales 3,289,568 3,195,626

Accounts Receivable 37,883 30,363

Result 86.83 105.25

Days Receivable = 365/Receivable turnover 2016 2015

No. of days 365 365

Receivable turnover 86.83 105.25

Result 4.20 3.47

Inventory Turnover = COGS/Inventory 2016 2015

COGS 1,527,552 1,495,382

Inventory 396,297 381,907

Result 3.85 3.92

Days' Inventory = 365/Inventory Turnover 2016 2015

No. of days 365 365

Inventory turnover 3.85 3.92

Result 94.69 93.22

Fixed Assets Turnover = Sales/net Fixed Assets 2016 2015

Sales 3,289,568 3,195,626

Net Fixed Assets 445,379 469,006

Result 7.39 6.81

Total Assets Turnover = Sales/Total Assets 2016 2015

Sales 3,289,568 3,289,568

Total Assets 1,867,898 1,886,548

Results 1.76 1.74

4. Profitability ratios

Profit Margin / Net Profit ratio = Net income / Sales 2016 2015

Net income 60,543 29,826

Sales 3,289,568 3,195,626

Result 1.84% 0.93%

Operating Margin ratio = Operating Profit/Sales 2016 2015

Operating Profit 114,035 133,348

Sales 3,289,568 3,195,626

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

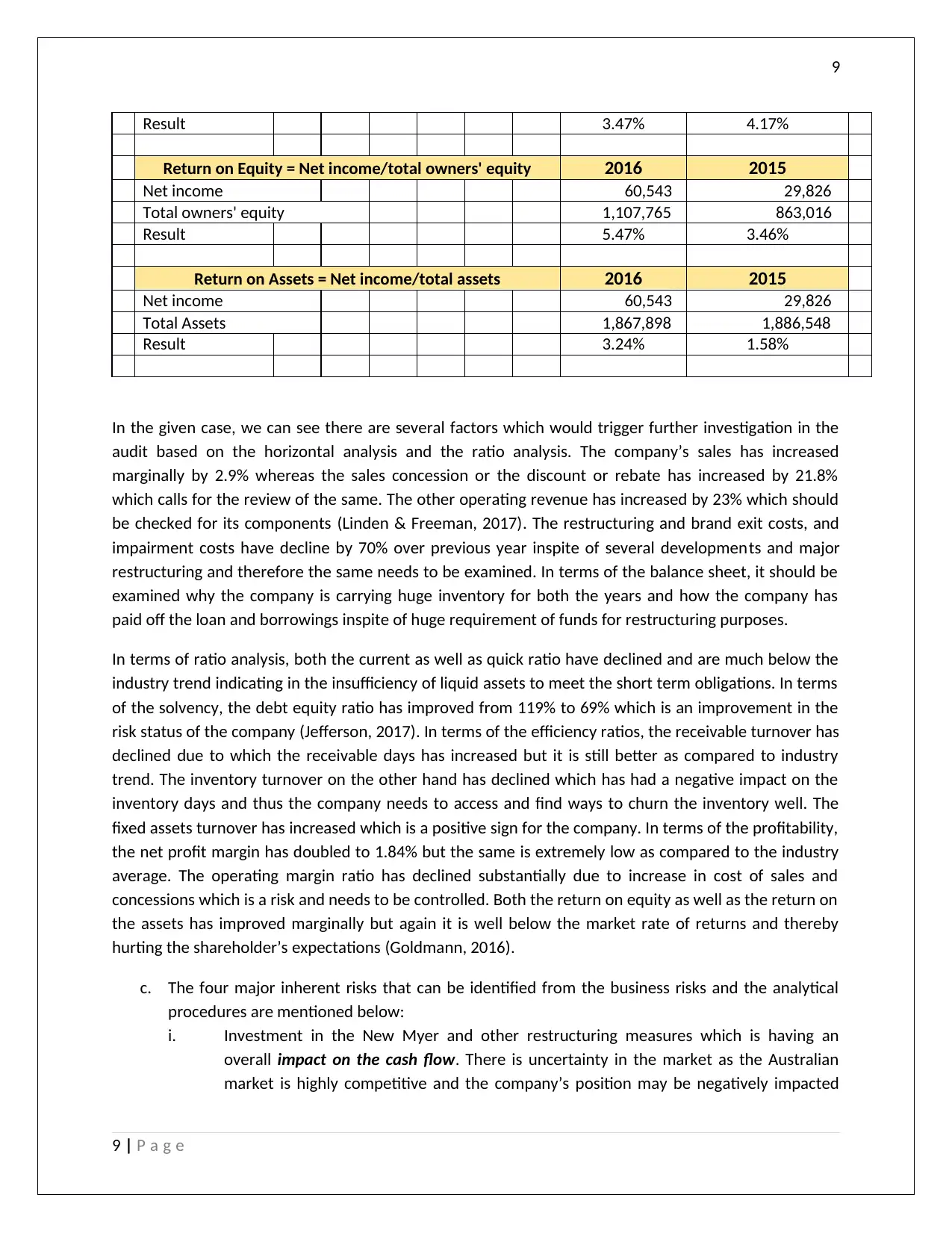

Result 3.47% 4.17%

Return on Equity = Net income/total owners' equity 2016 2015

Net income 60,543 29,826

Total owners' equity 1,107,765 863,016

Result 5.47% 3.46%

Return on Assets = Net income/total assets 2016 2015

Net income 60,543 29,826

Total Assets 1,867,898 1,886,548

Result 3.24% 1.58%

In the given case, we can see there are several factors which would trigger further investigation in the

audit based on the horizontal analysis and the ratio analysis. The company’s sales has increased

marginally by 2.9% whereas the sales concession or the discount or rebate has increased by 21.8%

which calls for the review of the same. The other operating revenue has increased by 23% which should

be checked for its components (Linden & Freeman, 2017). The restructuring and brand exit costs, and

impairment costs have decline by 70% over previous year inspite of several developments and major

restructuring and therefore the same needs to be examined. In terms of the balance sheet, it should be

examined why the company is carrying huge inventory for both the years and how the company has

paid off the loan and borrowings inspite of huge requirement of funds for restructuring purposes.

In terms of ratio analysis, both the current as well as quick ratio have declined and are much below the

industry trend indicating in the insufficiency of liquid assets to meet the short term obligations. In terms

of the solvency, the debt equity ratio has improved from 119% to 69% which is an improvement in the

risk status of the company (Jefferson, 2017). In terms of the efficiency ratios, the receivable turnover has

declined due to which the receivable days has increased but it is still better as compared to industry

trend. The inventory turnover on the other hand has declined which has had a negative impact on the

inventory days and thus the company needs to access and find ways to churn the inventory well. The

fixed assets turnover has increased which is a positive sign for the company. In terms of the profitability,

the net profit margin has doubled to 1.84% but the same is extremely low as compared to the industry

average. The operating margin ratio has declined substantially due to increase in cost of sales and

concessions which is a risk and needs to be controlled. Both the return on equity as well as the return on

the assets has improved marginally but again it is well below the market rate of returns and thereby

hurting the shareholder’s expectations (Goldmann, 2016).

c. The four major inherent risks that can be identified from the business risks and the analytical

procedures are mentioned below:

i. Investment in the New Myer and other restructuring measures which is having an

overall impact on the cash flow. There is uncertainty in the market as the Australian

market is highly competitive and the company’s position may be negatively impacted

9 | P a g e

Result 3.47% 4.17%

Return on Equity = Net income/total owners' equity 2016 2015

Net income 60,543 29,826

Total owners' equity 1,107,765 863,016

Result 5.47% 3.46%

Return on Assets = Net income/total assets 2016 2015

Net income 60,543 29,826

Total Assets 1,867,898 1,886,548

Result 3.24% 1.58%

In the given case, we can see there are several factors which would trigger further investigation in the

audit based on the horizontal analysis and the ratio analysis. The company’s sales has increased

marginally by 2.9% whereas the sales concession or the discount or rebate has increased by 21.8%

which calls for the review of the same. The other operating revenue has increased by 23% which should

be checked for its components (Linden & Freeman, 2017). The restructuring and brand exit costs, and

impairment costs have decline by 70% over previous year inspite of several developments and major

restructuring and therefore the same needs to be examined. In terms of the balance sheet, it should be

examined why the company is carrying huge inventory for both the years and how the company has

paid off the loan and borrowings inspite of huge requirement of funds for restructuring purposes.

In terms of ratio analysis, both the current as well as quick ratio have declined and are much below the

industry trend indicating in the insufficiency of liquid assets to meet the short term obligations. In terms

of the solvency, the debt equity ratio has improved from 119% to 69% which is an improvement in the

risk status of the company (Jefferson, 2017). In terms of the efficiency ratios, the receivable turnover has

declined due to which the receivable days has increased but it is still better as compared to industry

trend. The inventory turnover on the other hand has declined which has had a negative impact on the

inventory days and thus the company needs to access and find ways to churn the inventory well. The

fixed assets turnover has increased which is a positive sign for the company. In terms of the profitability,

the net profit margin has doubled to 1.84% but the same is extremely low as compared to the industry

average. The operating margin ratio has declined substantially due to increase in cost of sales and

concessions which is a risk and needs to be controlled. Both the return on equity as well as the return on

the assets has improved marginally but again it is well below the market rate of returns and thereby

hurting the shareholder’s expectations (Goldmann, 2016).

c. The four major inherent risks that can be identified from the business risks and the analytical

procedures are mentioned below:

i. Investment in the New Myer and other restructuring measures which is having an

overall impact on the cash flow. There is uncertainty in the market as the Australian

market is highly competitive and the company’s position may be negatively impacted

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

due to new entrants, increase in online competition, existing competitor policies

(Heminway, 2017).

ii. Financial Risk: Increase in the sales concession without substantial increase in the sales

which needs to be reviewed further as this is one of the main reason for the fall in the

operating margin percentage and lower levels of profitability and ROI. The company has

also not recognised the provision in the books of accounts for litigation which is due

against Portfolio Law Pty Ltd on behalf of Melbourne City Investments Pty Ltd (MCI) as

the company is not aware of the size of the claims (Marques, 2018).

iii. There is huge risk in the strategic and the internal business plan of the company as if it

fails in coming years, it may impact the sales, profitability, market position, share prices

and reputation of the company as a whole.

iv. The company is facing several external and macro-economic risks like that of Australian

dollar fluctuation, natural and unforeseen events, poor investor and customer

confidence, change in the government policies and weakness in the global economy as a

whole which might have a serious impact on the sales.

d. One of the key accounts which seems to be under risk is sales concession account and the risk of

material misstatement is quite high in this as the sales have grown by just 2.9% whereas the

sales allowance or the concession has increased by 21.8%. This shows that the company has

provided 7-8 times the original discount in order to trigger the sales. This also indicates the risk

that the company is selling the goods at losses.

The key related assertion here is the classification and completeness of the expenses booked

under the head sales allowance. It may be that the company has classified the cost of goods

sold or the advertisement and publicity expenses under the head sales allowance to show that

the goods are being sold at profit. The auditor should be checking the invoices at individual level

and should also check the arithmetical accuracy and classification of the sales concession

expenses to be sure if the company has reported the numbers correctly (Lessambo, 2018).

e. The overall ingredients of the inherent risks in the company have been shown in part c and

categorised into 4 parts namely cash flow and competition risk, financial risk, strategic and the

internal business plan risk and the external and macro-economic risks. The same has been

assessed based on the risks highlighted through analytical reviews and those highlighted in the

Director’s report of the company. Some of the factors which have led the company to assess all

this are expected operating and retail market conditions, competitive pressure, changing

government policies, exchange rate fluctuations and weakness in Australian dollars. The

company is also aware of the uncertain economic conditions and the risk associated with the

internal strategies and business plans. The company has implemented measures to mitigate the

technological and cyber security risks, people management risks and other related risks (Vieira,

et al., 2017). One another reason which has led to the assessment of the inherent risks in the

business is the sharp transformational strategy that the company has started to execute in the

last year with the horizon of 5 years as stated in the annual report. The company has shown

10 | P a g e

due to new entrants, increase in online competition, existing competitor policies

(Heminway, 2017).

ii. Financial Risk: Increase in the sales concession without substantial increase in the sales

which needs to be reviewed further as this is one of the main reason for the fall in the

operating margin percentage and lower levels of profitability and ROI. The company has

also not recognised the provision in the books of accounts for litigation which is due

against Portfolio Law Pty Ltd on behalf of Melbourne City Investments Pty Ltd (MCI) as

the company is not aware of the size of the claims (Marques, 2018).

iii. There is huge risk in the strategic and the internal business plan of the company as if it

fails in coming years, it may impact the sales, profitability, market position, share prices

and reputation of the company as a whole.

iv. The company is facing several external and macro-economic risks like that of Australian

dollar fluctuation, natural and unforeseen events, poor investor and customer

confidence, change in the government policies and weakness in the global economy as a

whole which might have a serious impact on the sales.

d. One of the key accounts which seems to be under risk is sales concession account and the risk of

material misstatement is quite high in this as the sales have grown by just 2.9% whereas the

sales allowance or the concession has increased by 21.8%. This shows that the company has

provided 7-8 times the original discount in order to trigger the sales. This also indicates the risk

that the company is selling the goods at losses.

The key related assertion here is the classification and completeness of the expenses booked

under the head sales allowance. It may be that the company has classified the cost of goods

sold or the advertisement and publicity expenses under the head sales allowance to show that

the goods are being sold at profit. The auditor should be checking the invoices at individual level

and should also check the arithmetical accuracy and classification of the sales concession

expenses to be sure if the company has reported the numbers correctly (Lessambo, 2018).

e. The overall ingredients of the inherent risks in the company have been shown in part c and

categorised into 4 parts namely cash flow and competition risk, financial risk, strategic and the

internal business plan risk and the external and macro-economic risks. The same has been

assessed based on the risks highlighted through analytical reviews and those highlighted in the

Director’s report of the company. Some of the factors which have led the company to assess all

this are expected operating and retail market conditions, competitive pressure, changing

government policies, exchange rate fluctuations and weakness in Australian dollars. The

company is also aware of the uncertain economic conditions and the risk associated with the

internal strategies and business plans. The company has implemented measures to mitigate the

technological and cyber security risks, people management risks and other related risks (Vieira,

et al., 2017). One another reason which has led to the assessment of the inherent risks in the

business is the sharp transformational strategy that the company has started to execute in the

last year with the horizon of 5 years as stated in the annual report. The company has shown

10 | P a g e

11

strong focus on this transformation and renovation in strategy and is expecting a turnaround in

the sales growth and overall performance of the company.

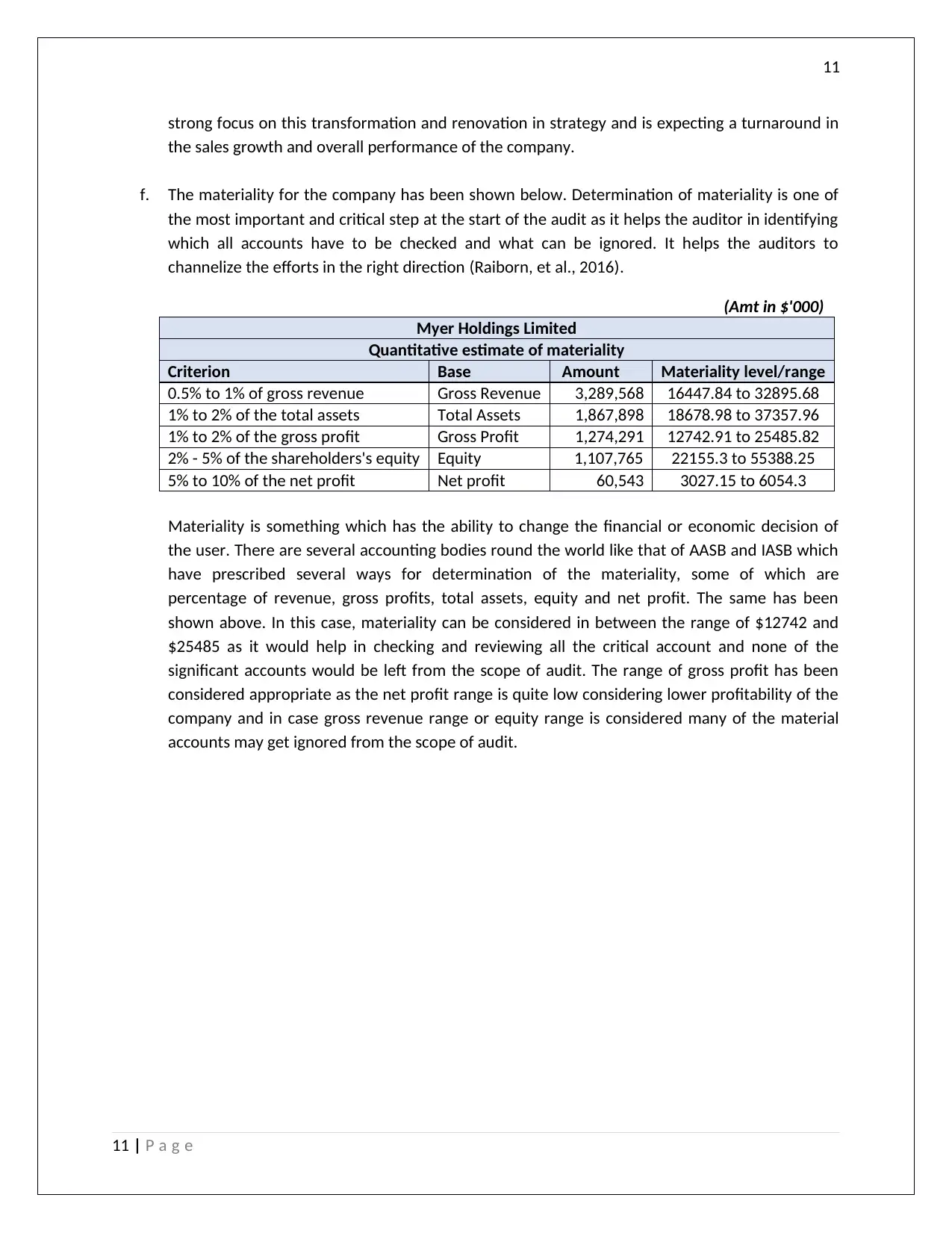

f. The materiality for the company has been shown below. Determination of materiality is one of

the most important and critical step at the start of the audit as it helps the auditor in identifying

which all accounts have to be checked and what can be ignored. It helps the auditors to

channelize the efforts in the right direction (Raiborn, et al., 2016).

(Amt in $'000)

Myer Holdings Limited

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 3,289,568 16447.84 to 32895.68

1% to 2% of the total assets Total Assets 1,867,898 18678.98 to 37357.96

1% to 2% of the gross profit Gross Profit 1,274,291 12742.91 to 25485.82

2% - 5% of the shareholders's equity Equity 1,107,765 22155.3 to 55388.25

5% to 10% of the net profit Net profit 60,543 3027.15 to 6054.3

Materiality is something which has the ability to change the financial or economic decision of

the user. There are several accounting bodies round the world like that of AASB and IASB which

have prescribed several ways for determination of the materiality, some of which are

percentage of revenue, gross profits, total assets, equity and net profit. The same has been

shown above. In this case, materiality can be considered in between the range of $12742 and

$25485 as it would help in checking and reviewing all the critical account and none of the

significant accounts would be left from the scope of audit. The range of gross profit has been

considered appropriate as the net profit range is quite low considering lower profitability of the

company and in case gross revenue range or equity range is considered many of the material

accounts may get ignored from the scope of audit.

11 | P a g e

strong focus on this transformation and renovation in strategy and is expecting a turnaround in

the sales growth and overall performance of the company.

f. The materiality for the company has been shown below. Determination of materiality is one of

the most important and critical step at the start of the audit as it helps the auditor in identifying

which all accounts have to be checked and what can be ignored. It helps the auditors to

channelize the efforts in the right direction (Raiborn, et al., 2016).

(Amt in $'000)

Myer Holdings Limited

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 3,289,568 16447.84 to 32895.68

1% to 2% of the total assets Total Assets 1,867,898 18678.98 to 37357.96

1% to 2% of the gross profit Gross Profit 1,274,291 12742.91 to 25485.82

2% - 5% of the shareholders's equity Equity 1,107,765 22155.3 to 55388.25

5% to 10% of the net profit Net profit 60,543 3027.15 to 6054.3

Materiality is something which has the ability to change the financial or economic decision of

the user. There are several accounting bodies round the world like that of AASB and IASB which

have prescribed several ways for determination of the materiality, some of which are

percentage of revenue, gross profits, total assets, equity and net profit. The same has been

shown above. In this case, materiality can be considered in between the range of $12742 and

$25485 as it would help in checking and reviewing all the critical account and none of the

significant accounts would be left from the scope of audit. The range of gross profit has been

considered appropriate as the net profit range is quite low considering lower profitability of the

company and in case gross revenue range or equity range is considered many of the material

accounts may get ignored from the scope of audit.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.