Detailed Audit Plan Report for Reliable Printer Ltd. - 2015 Audit

VerifiedAdded on 2022/12/27

|12

|2476

|79

Report

AI Summary

This report outlines the audit plan for Reliable Printer Ltd. for the year ending June 30, 2015, prepared to guide inexperienced staff and provide evidence of proper planning and execution. The report details the audit strategy, which focuses on lowering the assessed level of control risk through a predominantly substantive approach. The plan includes classification, occurrence, and valuation testing, and the use of analytical procedures like ratio and trend analysis to assess the reasonableness of account balances. Specific procedures are outlined for inventory, e-book revenue, fixed assets, purchases, print-on-demand revenue, and cash revenue, with details on testing frequency and sample sizes. The report also covers staff assignment and scheduling, including coordinating with the client and determining the involvement of specialists. Furthermore, it analyzes financial ratios (liquidity, profitability, efficiency, and solvency) and trends in income statements and balance sheets to provide a comprehensive overview of the company's financial performance.

Running head: AUDIT PLAN

AUDIT PLAN

Name of the Student:

Name of the University:

Author Note

AUDIT PLAN

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDIT PLAN

Table of Contents

Purpose of report........................................................................................................................2

The Audit Strategy.....................................................................................................................2

Audit plan...................................................................................................................................3

Assigning and scheduling staff..................................................................................................4

Analytical procedure..................................................................................................................5

Ratio.......................................................................................................................................5

Trend analysis........................................................................................................................6

References..................................................................................................................................7

Appendix....................................................................................................................................9

Trend analysis........................................................................................................................9

Ratio computation................................................................................................................10

Table of Contents

Purpose of report........................................................................................................................2

The Audit Strategy.....................................................................................................................2

Audit plan...................................................................................................................................3

Assigning and scheduling staff..................................................................................................4

Analytical procedure..................................................................................................................5

Ratio.......................................................................................................................................5

Trend analysis........................................................................................................................6

References..................................................................................................................................7

Appendix....................................................................................................................................9

Trend analysis........................................................................................................................9

Ratio computation................................................................................................................10

2AUDIT PLAN

Purpose of report

The report is prepared to present the audit plan for Reliable Printer Ltd. for the year

ended 30th June 2015. This report provides the evidence of proper planning of the audit work

including the guidance to the inexperienced staff. Further, this report provides the evidence of

work performed and consideration of the internal control in relation to proposed procedures

of the audit (Adler et al. 2018). This report also means of controlling time spent on the

engagement. The report will also consider the level of control risk and the predominantly

substantive approach. On the other hand, the main purpose of the report of this report is to

develop the audit strategy, audit plan and assigning the staff.

The Audit Strategy

If the control risk can be assesses lower than there is less chance of material

misstatement occurring. Here the material misstatement is referred to those material

misstatements that are not identified and fixed or prevented by the internal control system of

the firm. Hence, the audit would not need to consider the as much evidence that the control

activities are efficiently performing (Griffiths 2016). The strategy of this audit is to lower the

assessed level of control risk by identifying the material misstatement and solving them. For

this the auditor should use the various audit procedure and the principles. The lower level of

control risks assessed are associated with the purchase and the inventory as the firm

purchases 50% of inventory form Australia and 50% from the Asia at different prices but the

recording of the inventory are not made separately and moreover valued at the average cost.

Similarly, the cash receipts are also associated with lower level of assessed control risks as

some payment received by the firm in cheques though the mail but accountant does not pass

the proper entry of this event (Louwers et al. 2015).

Purpose of report

The report is prepared to present the audit plan for Reliable Printer Ltd. for the year

ended 30th June 2015. This report provides the evidence of proper planning of the audit work

including the guidance to the inexperienced staff. Further, this report provides the evidence of

work performed and consideration of the internal control in relation to proposed procedures

of the audit (Adler et al. 2018). This report also means of controlling time spent on the

engagement. The report will also consider the level of control risk and the predominantly

substantive approach. On the other hand, the main purpose of the report of this report is to

develop the audit strategy, audit plan and assigning the staff.

The Audit Strategy

If the control risk can be assesses lower than there is less chance of material

misstatement occurring. Here the material misstatement is referred to those material

misstatements that are not identified and fixed or prevented by the internal control system of

the firm. Hence, the audit would not need to consider the as much evidence that the control

activities are efficiently performing (Griffiths 2016). The strategy of this audit is to lower the

assessed level of control risk by identifying the material misstatement and solving them. For

this the auditor should use the various audit procedure and the principles. The lower level of

control risks assessed are associated with the purchase and the inventory as the firm

purchases 50% of inventory form Australia and 50% from the Asia at different prices but the

recording of the inventory are not made separately and moreover valued at the average cost.

Similarly, the cash receipts are also associated with lower level of assessed control risks as

some payment received by the firm in cheques though the mail but accountant does not pass

the proper entry of this event (Louwers et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDIT PLAN

Hence, the auditor shall perform the classification test in respect of this to identify and

resolve the risks associated with purchase and inventory. Recording of inventory shall be

made using proper valuation method cost or market value and shall be separated on the basis

of the country from where it is received. Further, in respect of risk associated with cash the

auditor shall try to resolve this risk by recommending the proper accounting entry to

accountant of the firm for such type of revenues. Cheque received through mail shall be

recorded properly at the bank book and shall be reconciled on regular interval. The auditor

shall also review various areas of the firm and resolve it by recommending proper accounting

procedures and principles (William, Glover and Prawitt 2016)

The audit follows the substantive audit approach. In this, the auditors verified the

transaction and event in the financial statement by considering the maximum possible volume

of those transaction and events. Hence, this audit will also follow the same strategy and

perform the verification of transaction and the financial event by covering the maximum

possible volume of the transaction and events. This allow the auditor to reach and identifies

the each material misstatement while also reduces the probability of uncovered material

misstatements. The strategy is based on the principle First one is that the auditor review the

internal control program, which affect the financial reporting system or the areas being

audited (Kim, Baikand Cho 2016). While, the second principle the auditor assures that the all

control area of the organisation should perform properly. Then, the auditor analyse the

control areas of the firm, as they are reliable or not. If the areas become reliable then it means

that the material misstatement risk, which are not easily identified by the auditor are become

low.

Audit plan

The audit procedure is an activity used by the auditor to identify the quality of the

financial information by the clients. There are various procedures available to analyse and

Hence, the auditor shall perform the classification test in respect of this to identify and

resolve the risks associated with purchase and inventory. Recording of inventory shall be

made using proper valuation method cost or market value and shall be separated on the basis

of the country from where it is received. Further, in respect of risk associated with cash the

auditor shall try to resolve this risk by recommending the proper accounting entry to

accountant of the firm for such type of revenues. Cheque received through mail shall be

recorded properly at the bank book and shall be reconciled on regular interval. The auditor

shall also review various areas of the firm and resolve it by recommending proper accounting

procedures and principles (William, Glover and Prawitt 2016)

The audit follows the substantive audit approach. In this, the auditors verified the

transaction and event in the financial statement by considering the maximum possible volume

of those transaction and events. Hence, this audit will also follow the same strategy and

perform the verification of transaction and the financial event by covering the maximum

possible volume of the transaction and events. This allow the auditor to reach and identifies

the each material misstatement while also reduces the probability of uncovered material

misstatements. The strategy is based on the principle First one is that the auditor review the

internal control program, which affect the financial reporting system or the areas being

audited (Kim, Baikand Cho 2016). While, the second principle the auditor assures that the all

control area of the organisation should perform properly. Then, the auditor analyse the

control areas of the firm, as they are reliable or not. If the areas become reliable then it means

that the material misstatement risk, which are not easily identified by the auditor are become

low.

Audit plan

The audit procedure is an activity used by the auditor to identify the quality of the

financial information by the clients. There are various procedures available to analyse and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDIT PLAN

examine the quality of the provided information. Here the auditor uses the classification

testing, Occurrence testing and the valuation test to perform the audit. In the classification

testing, the auditor examines that the transaction and events are classified properly or not. In

the occurrence testing the auditor examines whether the claimed transaction or event of the

client is actually occurred or not (Sultanaet al. 2015). Lastly, in the valuation testing the

auditor ensures the valuation of the assets and liabilities are properly performed or not. The

main purpose of the audit is to identify the material misstatement and solve them by applying

the proper accounting principles and procedure. The auditor also performs the specific

analytical procedure while performing the audit of the organisation. The procedure helps the

auditor to understand the business of the client and the chances in the business. This will also

help the auditor to determine the major risk areas to plan the other audit plan. In this the

auditor analyse the past financial report of the firm as well as the forecasted report of the

firm. After that auditor, compare these reports of the firm with the other firms of the same

industry (Knechel and Salterio 2016). This report consist the various financial ratios as well

as the sustainability and non-financial information of the firm.

Here, the auditor will perform the valuation test in respect of the inventory, e-book

revenue and fixed asset by using the 10% of the available data. In respect of the purchases,

the auditor shall perform the occurrence and allocation test along with the substantive test.

For print on demand revenue the auditor, perform the risk assessment test and detailed

balanced test with the sample size of 15% data. For e-book revenue the auditor, perform the

analytical procedure test, occurrence test and classification test with the 10% of the all

transaction data. Regarding the appointment of the new CEO, auditor exercises the dual-

purpose test and the analytical procedure test (Leitch 2016). In context of the new it system

the auditor applies the dual- purpose testing, risk assessment test and the substantive test. For

financial part the auditor perform the ratio analysis of the different periods and also compare

examine the quality of the provided information. Here the auditor uses the classification

testing, Occurrence testing and the valuation test to perform the audit. In the classification

testing, the auditor examines that the transaction and events are classified properly or not. In

the occurrence testing the auditor examines whether the claimed transaction or event of the

client is actually occurred or not (Sultanaet al. 2015). Lastly, in the valuation testing the

auditor ensures the valuation of the assets and liabilities are properly performed or not. The

main purpose of the audit is to identify the material misstatement and solve them by applying

the proper accounting principles and procedure. The auditor also performs the specific

analytical procedure while performing the audit of the organisation. The procedure helps the

auditor to understand the business of the client and the chances in the business. This will also

help the auditor to determine the major risk areas to plan the other audit plan. In this the

auditor analyse the past financial report of the firm as well as the forecasted report of the

firm. After that auditor, compare these reports of the firm with the other firms of the same

industry (Knechel and Salterio 2016). This report consist the various financial ratios as well

as the sustainability and non-financial information of the firm.

Here, the auditor will perform the valuation test in respect of the inventory, e-book

revenue and fixed asset by using the 10% of the available data. In respect of the purchases,

the auditor shall perform the occurrence and allocation test along with the substantive test.

For print on demand revenue the auditor, perform the risk assessment test and detailed

balanced test with the sample size of 15% data. For e-book revenue the auditor, perform the

analytical procedure test, occurrence test and classification test with the 10% of the all

transaction data. Regarding the appointment of the new CEO, auditor exercises the dual-

purpose test and the analytical procedure test (Leitch 2016). In context of the new it system

the auditor applies the dual- purpose testing, risk assessment test and the substantive test. For

financial part the auditor perform the ratio analysis of the different periods and also compare

5AUDIT PLAN

them with the ratios of the other firm from the same industry. Lastly, for the cash revenue, the

auditor shall perform the valuation test, substantive test and the dual- purpose tests by using

the 20% of the available data. The testing of the purchase and inventory is performed in

quarterly basis while the testing of the revenues of the print on demand is performed on the

half- yearly basis (Brasel et al. 2016). The e- book revenue is also tested in the quarterly

basis. The cash revenue is tested in the monthly basis. While, the fixed assets and the

finances are tested two times in the year, one is in between the year and another is in the end.

Appointment of new CEO and the IT system is tested at the time of the adoption.

Assigning and scheduling staff

The auditor shall also co-ordinate with the client in the data preparation by helping

them to assign the proper or specified staff in the different internal control areas of the

organisation. The auditor also helps the client to identify the requirement of the consultant or

any other specialist (Blocki 2015). Therefore, the client can easily identify and solve the

material misstatement and also increase the efficiencies of the business operation.

Analytical procedure

Analytical review in the accounting and auditing aspect is carried out the auditors for

accessing the reasonableness of the account balances. Within the broad concept, analytical

procedure can be carried out through using various ratios, trend analysis and certain financial

as well as non financial information.

Ratio

It is the form of analysing the financial statement for obtaining quick indication of the

company’s financial performances in different key areas including liquidity ratio, profitability

ratio, efficiency ratio and solvency ratio.

them with the ratios of the other firm from the same industry. Lastly, for the cash revenue, the

auditor shall perform the valuation test, substantive test and the dual- purpose tests by using

the 20% of the available data. The testing of the purchase and inventory is performed in

quarterly basis while the testing of the revenues of the print on demand is performed on the

half- yearly basis (Brasel et al. 2016). The e- book revenue is also tested in the quarterly

basis. The cash revenue is tested in the monthly basis. While, the fixed assets and the

finances are tested two times in the year, one is in between the year and another is in the end.

Appointment of new CEO and the IT system is tested at the time of the adoption.

Assigning and scheduling staff

The auditor shall also co-ordinate with the client in the data preparation by helping

them to assign the proper or specified staff in the different internal control areas of the

organisation. The auditor also helps the client to identify the requirement of the consultant or

any other specialist (Blocki 2015). Therefore, the client can easily identify and solve the

material misstatement and also increase the efficiencies of the business operation.

Analytical procedure

Analytical review in the accounting and auditing aspect is carried out the auditors for

accessing the reasonableness of the account balances. Within the broad concept, analytical

procedure can be carried out through using various ratios, trend analysis and certain financial

as well as non financial information.

Ratio

It is the form of analysing the financial statement for obtaining quick indication of the

company’s financial performances in different key areas including liquidity ratio, profitability

ratio, efficiency ratio and solvency ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDIT PLAN

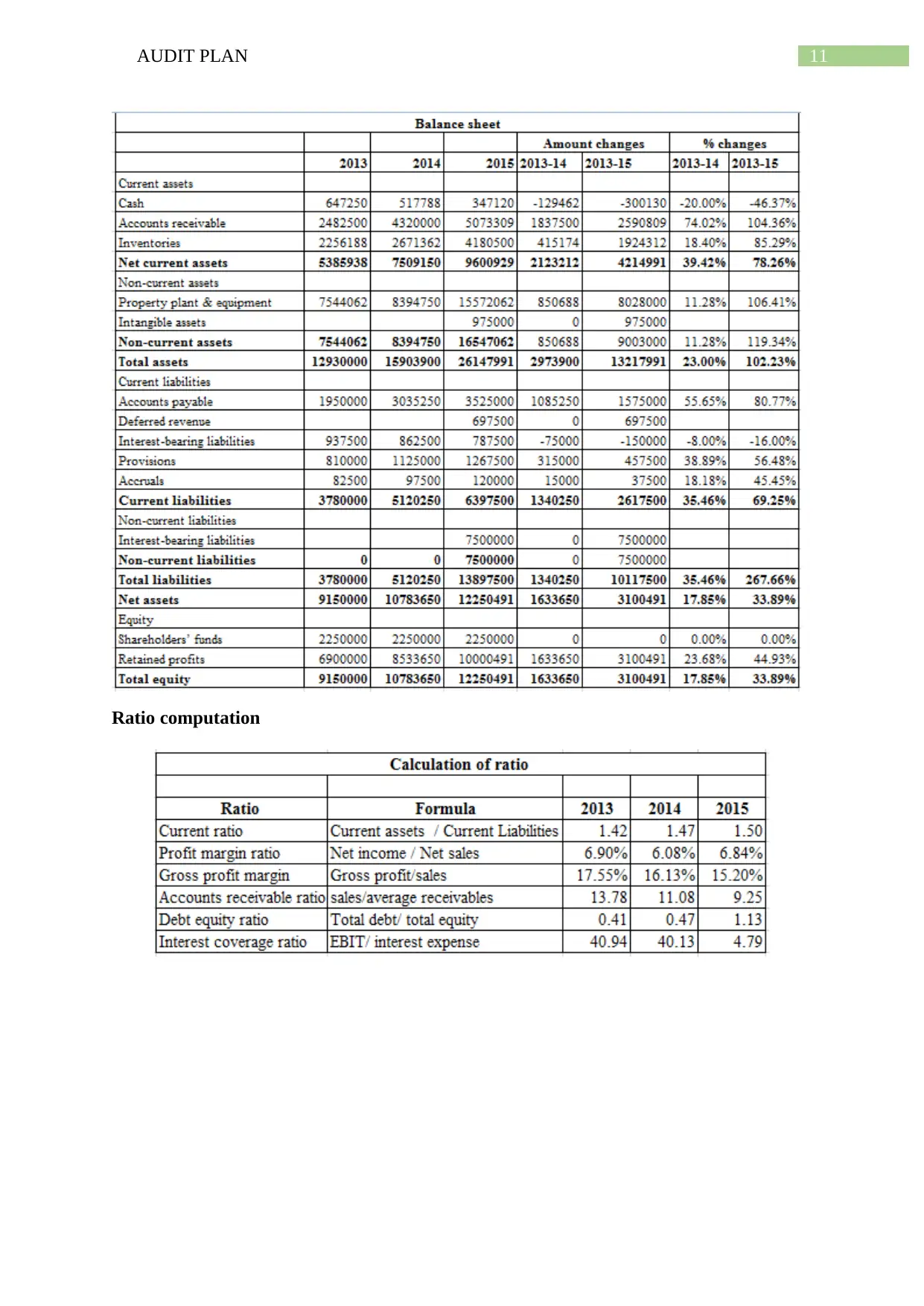

Liquidity ratio – liquidity status of the company measured through the current ratio that

measures the ability of the company to meet its short term obligations upon becoming due.

Generally, the current ratio of more than 1 signifies that the short term obligations can be

sufficiently paid off from the current assets (Ruhnke and Schmidt 2014). Looking into the

current ratio of the company it can be stated that the company’s current ratio is in improving

trend. It signifies that the liquidity position of the entity has been improved

Profitability ratio – profitability ratio measures the ability of the company to convert its

revenue into earning. Positive earning represents that the company is able to generate earning

for its shareholders (Ruhnke and Schmidt 2014). Looking into the profitability position of the

company it can be identified that though the gross profit margin of the entity reduced over the

year the company was able to improve the net profit margin over the years from 2014 to

2015.

Efficiency ratio – efficiency ratio measures the ability of the company to convert its balance

sheet items into income statement item. Account receivable ratio represents the time taken by

the company to collect the dues. Looking into the account receivable ratio of the company it

can be stated that the company’s efficiency in context of collecting the dues is in improving

trend and the time required has reduced from 13.78 days to 9.25 days. It signifies that the

efficiency of the entity in terms of collection of dues has been improved (Titera 2013)

Solvency ratio – it represents the company’s leverage position and thereby the long term

solvency status. It can be identified that the in over the years from 2014 to 2015 the company

has significantly became dependent upon outside borrowing which in turn also reduced the

interest coverage ratio from 40.13 to 4.79 times (Titera 2013)

Liquidity ratio – liquidity status of the company measured through the current ratio that

measures the ability of the company to meet its short term obligations upon becoming due.

Generally, the current ratio of more than 1 signifies that the short term obligations can be

sufficiently paid off from the current assets (Ruhnke and Schmidt 2014). Looking into the

current ratio of the company it can be stated that the company’s current ratio is in improving

trend. It signifies that the liquidity position of the entity has been improved

Profitability ratio – profitability ratio measures the ability of the company to convert its

revenue into earning. Positive earning represents that the company is able to generate earning

for its shareholders (Ruhnke and Schmidt 2014). Looking into the profitability position of the

company it can be identified that though the gross profit margin of the entity reduced over the

year the company was able to improve the net profit margin over the years from 2014 to

2015.

Efficiency ratio – efficiency ratio measures the ability of the company to convert its balance

sheet items into income statement item. Account receivable ratio represents the time taken by

the company to collect the dues. Looking into the account receivable ratio of the company it

can be stated that the company’s efficiency in context of collecting the dues is in improving

trend and the time required has reduced from 13.78 days to 9.25 days. It signifies that the

efficiency of the entity in terms of collection of dues has been improved (Titera 2013)

Solvency ratio – it represents the company’s leverage position and thereby the long term

solvency status. It can be identified that the in over the years from 2014 to 2015 the company

has significantly became dependent upon outside borrowing which in turn also reduced the

interest coverage ratio from 40.13 to 4.79 times (Titera 2013)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDIT PLAN

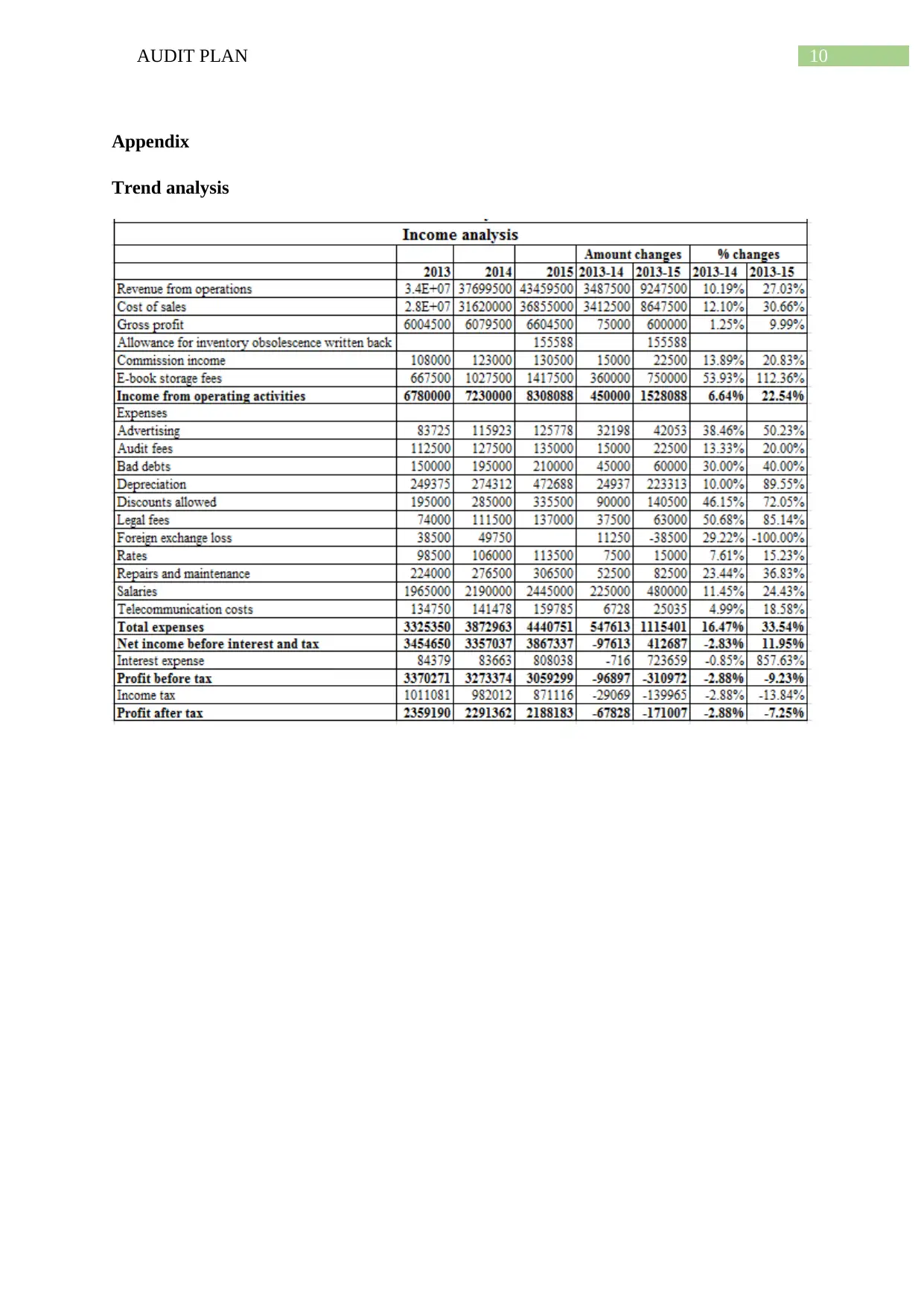

Trend analysis

Income statement – looking into the trend of the income statement it can be identified

that sales as well as gross profit of the company are in improving trend and the gross

profit is increased by 9.99% in 2015 if 2013 is taken as the base year. However, the

net profit is in reducing trend as the expenses of the company are in increasing trend

that reduced the net earnings (Robinson et al. 2015).

Balance sheet – looking into the trend of balance sheet it can be stated that current

assets as well as current liabilities both are in increasing trend. In the same way, total

assets as well as total liabilities both are in increasing trend. Moreover, the equity of

the company is also in increasing trend (Dalnial et al. 2014).

Trend analysis

Income statement – looking into the trend of the income statement it can be identified

that sales as well as gross profit of the company are in improving trend and the gross

profit is increased by 9.99% in 2015 if 2013 is taken as the base year. However, the

net profit is in reducing trend as the expenses of the company are in increasing trend

that reduced the net earnings (Robinson et al. 2015).

Balance sheet – looking into the trend of balance sheet it can be stated that current

assets as well as current liabilities both are in increasing trend. In the same way, total

assets as well as total liabilities both are in increasing trend. Moreover, the equity of

the company is also in increasing trend (Dalnial et al. 2014).

8AUDIT PLAN

References

Adler, P., Falk, C., Friedler, S.A., Nix, T., Rybeck, G., Scheidegger, C., Smith, B. and

Venkatasubramanian, S., 2018. Auditing black-box models for indirect influence. Knowledge

and Information Systems, 54(1), pp.95-122.

Blocki, J., Christin, N., Datta, A., Procaccia, A.D. and Sinha, A., 2015, February. Audit

games with multiple defender resources. In Twenty-Ninth AAAI Conference on Artificial

Intelligence.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Dalnial, H., Kamaluddin, A., Sanusi, Z.M. and Khairuddin, K.S., 2014. Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science, 2(1).

Griffiths, P., 2016. Risk-based auditing. Routledge.

Kim, Y.J., Baik, B. and Cho, S., 2016. Detecting financial misstatements with fraud intention

using multi-class cost-sensitive learning. Expert Systems with Applications, 62, pp.32-43.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Leitch, M., 2016. Intelligent internal control and risk management: designing high-

performance risk control systems. Routledge.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

References

Adler, P., Falk, C., Friedler, S.A., Nix, T., Rybeck, G., Scheidegger, C., Smith, B. and

Venkatasubramanian, S., 2018. Auditing black-box models for indirect influence. Knowledge

and Information Systems, 54(1), pp.95-122.

Blocki, J., Christin, N., Datta, A., Procaccia, A.D. and Sinha, A., 2015, February. Audit

games with multiple defender resources. In Twenty-Ninth AAAI Conference on Artificial

Intelligence.

Brasel, K., Doxey, M.M., Grenier, J.H. and Reffett, A., 2016. Risk disclosure preceding

negative outcomes: The effects of reporting critical audit matters on judgments of auditor

liability. The Accounting Review, 91(5), pp.1345-1362.

Dalnial, H., Kamaluddin, A., Sanusi, Z.M. and Khairuddin, K.S., 2014. Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced Management

Science, 2(1).

Griffiths, P., 2016. Risk-based auditing. Routledge.

Kim, Y.J., Baik, B. and Cho, S., 2016. Detecting financial misstatements with fraud intention

using multi-class cost-sensitive learning. Expert Systems with Applications, 62, pp.32-43.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Leitch, M., 2016. Intelligent internal control and risk management: designing high-

performance risk control systems. Routledge.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C.,

2015. Auditing & assurance services. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDIT PLAN

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Sultana, N., Singh, H. and Van der Zahn, J.L.M., 2015. Audit committee characteristics and

audit report lag. International Journal of Auditing, 19(2), pp.72-87.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Robinson, T.R., Henry, E., Pirie, W.L. and Broihahn, M.A., 2015. International financial

statement analysis. John Wiley & Sons.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship

between inherent and control risk factors and audit adjustments. Auditing: A Journal of

Practice & Theory, 33(4), pp.247-269.

Sultana, N., Singh, H. and Van der Zahn, J.L.M., 2015. Audit committee characteristics and

audit report lag. International Journal of Auditing, 19(2), pp.72-87.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of

Information Systems, 27(1), pp.325-331.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDIT PLAN

Appendix

Trend analysis

Appendix

Trend analysis

11AUDIT PLAN

Ratio computation

Ratio computation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.