Audit and Professional Practice Report: Cyan Enterprises, BUS000

VerifiedAdded on 2023/06/05

|11

|2616

|292

Report

AI Summary

This report presents an audit planning analysis for Cyan Enterprises, a small entity. It begins with an executive summary and table of contents, followed by an introduction outlining authorization, limitations, and scope. The report then delves into the inputs, including a trial balance and the determination of materiality using various financial metrics. Preliminary analytical reviews, such as variance analysis and common size income statements, are conducted. The discussion section analyzes key income statement accounts, identifies audit assertions and risks, and outlines appropriate audit procedures. The report emphasizes the importance of fraud risk analysis and provides recommendations for the audit process, including a call for mandatory fraud risk assessment and balance sheet analysis. The report references several academic sources to support its findings and recommendations.

University of the Sunshine Coast

Auditing and Professional Practice Assignment

BUS000, Tutor Name, Tutorial Time

Student Name, SID: 10101010

7-7-2017

Auditing and Professional Practice Assignment

BUS000, Tutor Name, Tutorial Time

Student Name, SID: 10101010

7-7-2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

A report has been prepared on the audit planning of one of the small entities named “Cyan

Enterprises”. The audit partner of the firm has requested the audit senior to prepare the

report and hand it over the same. The report starts with the calculation of the materiality

for the client and also highlights some of the audit procedures to be taken with respect to

the critical accounts. The risk and assertions of the management have also been mentioned

and the fraud risk analysis has also been done for the client.

i

A report has been prepared on the audit planning of one of the small entities named “Cyan

Enterprises”. The audit partner of the firm has requested the audit senior to prepare the

report and hand it over the same. The report starts with the calculation of the materiality

for the client and also highlights some of the audit procedures to be taken with respect to

the critical accounts. The risk and assertions of the management have also been mentioned

and the fraud risk analysis has also been done for the client.

i

Table of Contents

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................3

3. Discussion on the report................................................................................................................4

3.1. Income statement accounts to be analysed..........................................................................4

3.2. Audit procedures to be undertaken.......................................................................................5

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

Executive Summary................................................................................................................................i

Table of Contents...................................................................................................................................ii

1. Introduction...................................................................................................................................1

1.1. Authorisation.........................................................................................................................1

1.2. Limitations.............................................................................................................................1

1.3. Scope.....................................................................................................................................1

2. Inputs to the report - Analysis.......................................................................................................2

2.1. Trial balance input.................................................................................................................2

2.2. Determination of Materiality.................................................................................................2

2.3. Preliminary Analytical Review................................................................................................3

3. Discussion on the report................................................................................................................4

3.1. Income statement accounts to be analysed..........................................................................4

3.2. Audit procedures to be undertaken.......................................................................................5

4. Conclusion – Fraud Risk Analysis...................................................................................................6

5. Recommendations.........................................................................................................................6

References.............................................................................................................................................7

ii

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.Introduction

1.1. Authorisation

The audit planning report for Cyan Enterprises has been asked by the audit partner of the

firm along with the audit recommendations, the high risk critical accounts and the audit

procedure to be taken in respect of the same.

1.2. Limitations

Since the trial balance of the company which has been given for the year 2016 and 2017 is not

balanced in terms of the debit and the credit totals, the difference can be assumed to be the

suspense account and the same has not been considered in any of the preliminary analytical reviews

as the nature of the same is not known (Antonio 2014, pp.127-144)

.

1.3. Scope

The information and all the analysis including preliminary analytical review has been done

on the basis of the trial balance for the given entity. The scope of the project report includes

identifying the high risk critical accounts which require the audit attention, the audit

assertions in respect of the same and what the audit procedures to be taken to gather

sufficient and appropriate audit evidences to give opinion on financial statements

(Christensen, Glover and Wood 2013, pp.P36-P42).

1

1.1. Authorisation

The audit planning report for Cyan Enterprises has been asked by the audit partner of the

firm along with the audit recommendations, the high risk critical accounts and the audit

procedure to be taken in respect of the same.

1.2. Limitations

Since the trial balance of the company which has been given for the year 2016 and 2017 is not

balanced in terms of the debit and the credit totals, the difference can be assumed to be the

suspense account and the same has not been considered in any of the preliminary analytical reviews

as the nature of the same is not known (Antonio 2014, pp.127-144)

.

1.3. Scope

The information and all the analysis including preliminary analytical review has been done

on the basis of the trial balance for the given entity. The scope of the project report includes

identifying the high risk critical accounts which require the audit attention, the audit

assertions in respect of the same and what the audit procedures to be taken to gather

sufficient and appropriate audit evidences to give opinion on financial statements

(Christensen, Glover and Wood 2013, pp.P36-P42).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

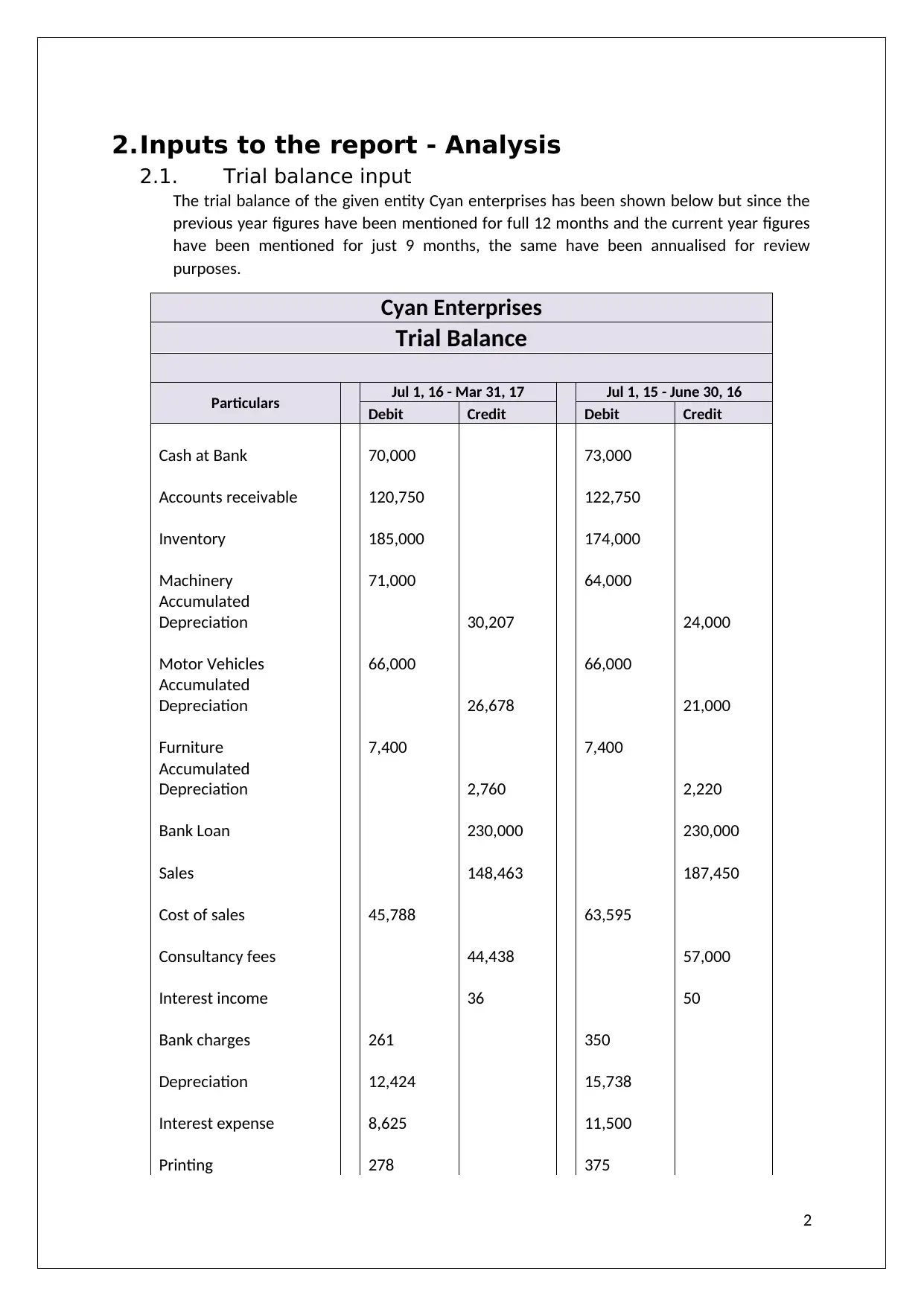

2.Inputs to the report - Analysis

2.1. Trial balance input

The trial balance of the given entity Cyan enterprises has been shown below but since the

previous year figures have been mentioned for full 12 months and the current year figures

have been mentioned for just 9 months, the same have been annualised for review

purposes.

Cyan Enterprises

Trial Balance

Particulars Jul 1, 16 - Mar 31, 17 Jul 1, 15 - June 30, 16

Debit Credit Debit Credit

Cash at Bank 70,000 73,000

Accounts receivable 120,750 122,750

Inventory 185,000 174,000

Machinery 71,000 64,000

Accumulated

Depreciation 30,207 24,000

Motor Vehicles 66,000 66,000

Accumulated

Depreciation 26,678 21,000

Furniture 7,400 7,400

Accumulated

Depreciation 2,760 2,220

Bank Loan 230,000 230,000

Sales 148,463 187,450

Cost of sales 45,788 63,595

Consultancy fees 44,438 57,000

Interest income 36 50

Bank charges 261 350

Depreciation 12,424 15,738

Interest expense 8,625 11,500

Printing 278 375

2

2.1. Trial balance input

The trial balance of the given entity Cyan enterprises has been shown below but since the

previous year figures have been mentioned for full 12 months and the current year figures

have been mentioned for just 9 months, the same have been annualised for review

purposes.

Cyan Enterprises

Trial Balance

Particulars Jul 1, 16 - Mar 31, 17 Jul 1, 15 - June 30, 16

Debit Credit Debit Credit

Cash at Bank 70,000 73,000

Accounts receivable 120,750 122,750

Inventory 185,000 174,000

Machinery 71,000 64,000

Accumulated

Depreciation 30,207 24,000

Motor Vehicles 66,000 66,000

Accumulated

Depreciation 26,678 21,000

Furniture 7,400 7,400

Accumulated

Depreciation 2,760 2,220

Bank Loan 230,000 230,000

Sales 148,463 187,450

Cost of sales 45,788 63,595

Consultancy fees 44,438 57,000

Interest income 36 50

Bank charges 261 350

Depreciation 12,424 15,738

Interest expense 8,625 11,500

Printing 278 375

2

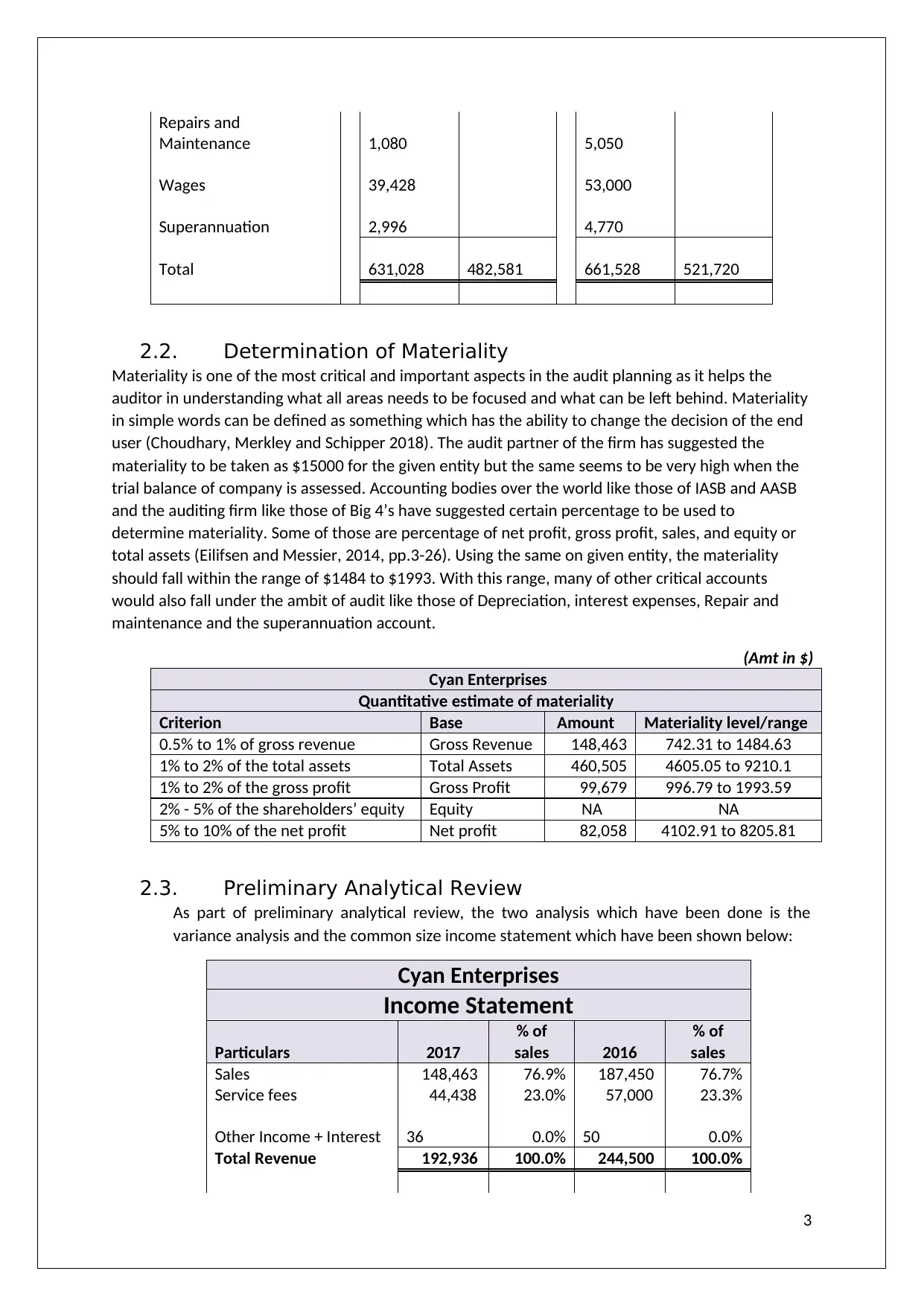

Repairs and

Maintenance 1,080 5,050

Wages 39,428 53,000

Superannuation 2,996 4,770

Total 631,028 482,581 661,528 521,720

2.2. Determination of Materiality

Materiality is one of the most critical and important aspects in the audit planning as it helps the

auditor in understanding what all areas needs to be focused and what can be left behind. Materiality

in simple words can be defined as something which has the ability to change the decision of the end

user (Choudhary, Merkley and Schipper 2018). The audit partner of the firm has suggested the

materiality to be taken as $15000 for the given entity but the same seems to be very high when the

trial balance of company is assessed. Accounting bodies over the world like those of IASB and AASB

and the auditing firm like those of Big 4’s have suggested certain percentage to be used to

determine materiality. Some of those are percentage of net profit, gross profit, sales, and equity or

total assets (Eilifsen and Messier, 2014, pp.3-26). Using the same on given entity, the materiality

should fall within the range of $1484 to $1993. With this range, many of other critical accounts

would also fall under the ambit of audit like those of Depreciation, interest expenses, Repair and

maintenance and the superannuation account.

(Amt in $)

Cyan Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 148,463 742.31 to 1484.63

1% to 2% of the total assets Total Assets 460,505 4605.05 to 9210.1

1% to 2% of the gross profit Gross Profit 99,679 996.79 to 1993.59

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 82,058 4102.91 to 8205.81

2.3. Preliminary Analytical Review

As part of preliminary analytical review, the two analysis which have been done is the

variance analysis and the common size income statement which have been shown below:

Cyan Enterprises

Income Statement

Particulars 2017

% of

sales 2016

% of

sales

Sales 148,463 76.9% 187,450 76.7%

Service fees 44,438 23.0% 57,000 23.3%

Other Income + Interest 36 0.0% 50 0.0%

Total Revenue 192,936 100.0% 244,500 100.0%

3

Maintenance 1,080 5,050

Wages 39,428 53,000

Superannuation 2,996 4,770

Total 631,028 482,581 661,528 521,720

2.2. Determination of Materiality

Materiality is one of the most critical and important aspects in the audit planning as it helps the

auditor in understanding what all areas needs to be focused and what can be left behind. Materiality

in simple words can be defined as something which has the ability to change the decision of the end

user (Choudhary, Merkley and Schipper 2018). The audit partner of the firm has suggested the

materiality to be taken as $15000 for the given entity but the same seems to be very high when the

trial balance of company is assessed. Accounting bodies over the world like those of IASB and AASB

and the auditing firm like those of Big 4’s have suggested certain percentage to be used to

determine materiality. Some of those are percentage of net profit, gross profit, sales, and equity or

total assets (Eilifsen and Messier, 2014, pp.3-26). Using the same on given entity, the materiality

should fall within the range of $1484 to $1993. With this range, many of other critical accounts

would also fall under the ambit of audit like those of Depreciation, interest expenses, Repair and

maintenance and the superannuation account.

(Amt in $)

Cyan Enterprises

Quantitative estimate of materiality

Criterion Base Amount Materiality level/range

0.5% to 1% of gross revenue Gross Revenue 148,463 742.31 to 1484.63

1% to 2% of the total assets Total Assets 460,505 4605.05 to 9210.1

1% to 2% of the gross profit Gross Profit 99,679 996.79 to 1993.59

2% - 5% of the shareholders’ equity Equity NA NA

5% to 10% of the net profit Net profit 82,058 4102.91 to 8205.81

2.3. Preliminary Analytical Review

As part of preliminary analytical review, the two analysis which have been done is the

variance analysis and the common size income statement which have been shown below:

Cyan Enterprises

Income Statement

Particulars 2017

% of

sales 2016

% of

sales

Sales 148,463 76.9% 187,450 76.7%

Service fees 44,438 23.0% 57,000 23.3%

Other Income + Interest 36 0.0% 50 0.0%

Total Revenue 192,936 100.0% 244,500 100.0%

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

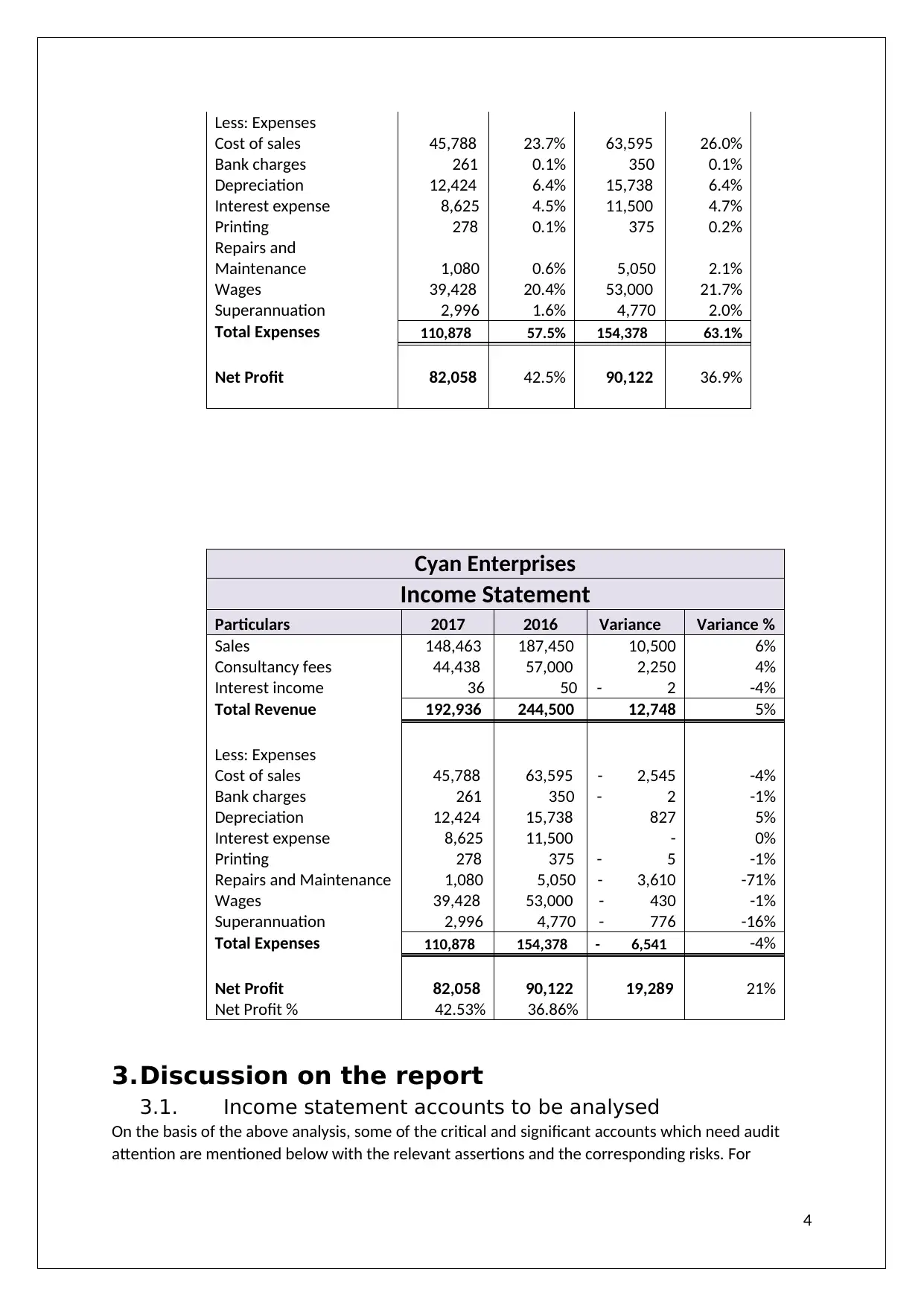

Less: Expenses

Cost of sales 45,788 23.7% 63,595 26.0%

Bank charges 261 0.1% 350 0.1%

Depreciation 12,424 6.4% 15,738 6.4%

Interest expense 8,625 4.5% 11,500 4.7%

Printing 278 0.1% 375 0.2%

Repairs and

Maintenance 1,080 0.6% 5,050 2.1%

Wages 39,428 20.4% 53,000 21.7%

Superannuation 2,996 1.6% 4,770 2.0%

Total Expenses 110,878 57.5% 154,378 63.1%

Net Profit 82,058 42.5% 90,122 36.9%

Cyan Enterprises

Income Statement

Particulars 2017 2016 Variance Variance %

Sales 148,463 187,450 10,500 6%

Consultancy fees 44,438 57,000 2,250 4%

Interest income 36 50 - 2 -4%

Total Revenue 192,936 244,500 12,748 5%

Less: Expenses

Cost of sales 45,788 63,595 - 2,545 -4%

Bank charges 261 350 - 2 -1%

Depreciation 12,424 15,738 827 5%

Interest expense 8,625 11,500 - 0%

Printing 278 375 - 5 -1%

Repairs and Maintenance 1,080 5,050 - 3,610 -71%

Wages 39,428 53,000 - 430 -1%

Superannuation 2,996 4,770 - 776 -16%

Total Expenses 110,878 154,378 - 6,541 -4%

Net Profit 82,058 90,122 19,289 21%

Net Profit % 42.53% 36.86%

3.Discussion on the report

3.1. Income statement accounts to be analysed

On the basis of the above analysis, some of the critical and significant accounts which need audit

attention are mentioned below with the relevant assertions and the corresponding risks. For

4

Cost of sales 45,788 23.7% 63,595 26.0%

Bank charges 261 0.1% 350 0.1%

Depreciation 12,424 6.4% 15,738 6.4%

Interest expense 8,625 4.5% 11,500 4.7%

Printing 278 0.1% 375 0.2%

Repairs and

Maintenance 1,080 0.6% 5,050 2.1%

Wages 39,428 20.4% 53,000 21.7%

Superannuation 2,996 1.6% 4,770 2.0%

Total Expenses 110,878 57.5% 154,378 63.1%

Net Profit 82,058 42.5% 90,122 36.9%

Cyan Enterprises

Income Statement

Particulars 2017 2016 Variance Variance %

Sales 148,463 187,450 10,500 6%

Consultancy fees 44,438 57,000 2,250 4%

Interest income 36 50 - 2 -4%

Total Revenue 192,936 244,500 12,748 5%

Less: Expenses

Cost of sales 45,788 63,595 - 2,545 -4%

Bank charges 261 350 - 2 -1%

Depreciation 12,424 15,738 827 5%

Interest expense 8,625 11,500 - 0%

Printing 278 375 - 5 -1%

Repairs and Maintenance 1,080 5,050 - 3,610 -71%

Wages 39,428 53,000 - 430 -1%

Superannuation 2,996 4,770 - 776 -16%

Total Expenses 110,878 154,378 - 6,541 -4%

Net Profit 82,058 90,122 19,289 21%

Net Profit % 42.53% 36.86%

3.Discussion on the report

3.1. Income statement accounts to be analysed

On the basis of the above analysis, some of the critical and significant accounts which need audit

attention are mentioned below with the relevant assertions and the corresponding risks. For

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

comparison sake, the accounts have been annualized and the variances have been measured

(Lessambo 2018, pp. 183-202).

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has increased by 6% as compared to last

year but it has been same in terms of the total

receipts. Therefore, the management assertion is this

respect as to whether all the sales has been recorded

needs to be checked by the auditor. Also, the revenue

recognition criteria need to be checked (Mock and

Fukukawa 2015, pp.75-84).

2 Cost of Sales The sales has increased by 6%, whereas the cost of

sales has decreased by 4%. In terms of total receipts,

the percentage of cost of sales has decreased from

26% to 23.7%. Therefore, it needs to be checked if the

management has ensured the completeness in

recording of the transaction and uniformity in the

policies (Kharisova and Kozlova 2014, p.180).

3 Repair and

maintenance

This is one expenses which has by 71% as compared to

the last year and in terms of percentage of total

receipts, it has fallen by nearly 2% and therefore it

needs to be checked requisite provisions have been

taken in books and something that needs to be

charged to P&L has not been capitalised (Titera 2013,

pp.325-331).

4 Depreciation Where most of the expenses of the company have

decreased, the depreciation expenses have increased

by 5% as compared to the last year and it needs to be

seen if the accounting estimates and the management

judgements with respect to the fixed assets have

changed (Coetzee and Lubbe 2014, pp.115-125).

3.2. Audit procedures to be undertaken

With respect to the above audit assertions and the audit risks, some of the audit

procedures which can be taken in respect of auditing these accounts are mentioned

below:

a. Sales: For checking the sales, the vouching of the sample invoices must be done

and the rates and prices mentioned in the system must be cross verified with

the invoice prices. Also, the total of the sales invoices must be checked with the

sales register to ensure completeness in recording. In addition to all this, the

revenue recognition criteria being used by the client needs to be verified and

audited (Glover and Prawitt 2014, pp.P1-P10).

b. Cost of Sales: the cost of sales has dropped drastically and thus the vouching of

sales invoices is warranted. Along with the same, it needs to be checked if the

decrease in costs is due to increase in efficiency or the lowering down of raw

5

(Lessambo 2018, pp. 183-202).

Sl. No. Account Name Audit Assertion and risk

1. Sales The sales has increased by 6% as compared to last

year but it has been same in terms of the total

receipts. Therefore, the management assertion is this

respect as to whether all the sales has been recorded

needs to be checked by the auditor. Also, the revenue

recognition criteria need to be checked (Mock and

Fukukawa 2015, pp.75-84).

2 Cost of Sales The sales has increased by 6%, whereas the cost of

sales has decreased by 4%. In terms of total receipts,

the percentage of cost of sales has decreased from

26% to 23.7%. Therefore, it needs to be checked if the

management has ensured the completeness in

recording of the transaction and uniformity in the

policies (Kharisova and Kozlova 2014, p.180).

3 Repair and

maintenance

This is one expenses which has by 71% as compared to

the last year and in terms of percentage of total

receipts, it has fallen by nearly 2% and therefore it

needs to be checked requisite provisions have been

taken in books and something that needs to be

charged to P&L has not been capitalised (Titera 2013,

pp.325-331).

4 Depreciation Where most of the expenses of the company have

decreased, the depreciation expenses have increased

by 5% as compared to the last year and it needs to be

seen if the accounting estimates and the management

judgements with respect to the fixed assets have

changed (Coetzee and Lubbe 2014, pp.115-125).

3.2. Audit procedures to be undertaken

With respect to the above audit assertions and the audit risks, some of the audit

procedures which can be taken in respect of auditing these accounts are mentioned

below:

a. Sales: For checking the sales, the vouching of the sample invoices must be done

and the rates and prices mentioned in the system must be cross verified with

the invoice prices. Also, the total of the sales invoices must be checked with the

sales register to ensure completeness in recording. In addition to all this, the

revenue recognition criteria being used by the client needs to be verified and

audited (Glover and Prawitt 2014, pp.P1-P10).

b. Cost of Sales: the cost of sales has dropped drastically and thus the vouching of

sales invoices is warranted. Along with the same, it needs to be checked if the

decrease in costs is due to increase in efficiency or the lowering down of raw

5

material costs. The auditor should also be the market prices with the actual

procurement price (Ruhnke and Schmidt 2014, pp.247-269).

c. Repair and Maintenance: Since there is a huge decline in repair and

maintenance expenses, first of the entire auditor should be checking the

accounting treatment as to whether these expenses are capitalised or charged

to P&L. Also, it should be verified if the company has ensured completeness in

booking of all the expenses and has followed accrual basis for taking requisite

provisions in books (Louwers et al. 2015).

d. Depreciation: Lastly the depreciation expenses also need to be verified with

respect to the accounting policies and judgements being used by the

management (Wali 2015, pp.82-97). The auditor should check the method and

rate of depreciation being used, the useful life assessment and whether the

company has made and acquisition or disposal during the year (Byrnes et al.

2015).

6

procurement price (Ruhnke and Schmidt 2014, pp.247-269).

c. Repair and Maintenance: Since there is a huge decline in repair and

maintenance expenses, first of the entire auditor should be checking the

accounting treatment as to whether these expenses are capitalised or charged

to P&L. Also, it should be verified if the company has ensured completeness in

booking of all the expenses and has followed accrual basis for taking requisite

provisions in books (Louwers et al. 2015).

d. Depreciation: Lastly the depreciation expenses also need to be verified with

respect to the accounting policies and judgements being used by the

management (Wali 2015, pp.82-97). The auditor should check the method and

rate of depreciation being used, the useful life assessment and whether the

company has made and acquisition or disposal during the year (Byrnes et al.

2015).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4.Conclusion – Fraud Risk Analysis

The last step which has been asked by the audit partner is fraud risk analysis but he has

recommended that the same need not be carried for the client in hand as Cyan Enterprises

is a trustworthy client. But this contention of the audit partner is completely wrong and

unjustified considering the principles of professional scepticism and the principles of ethics

laid down in APES 110. It is a well-established fact that all the clients need to be assessed for

fraud risk analysis irrespective of the fact that whether or not they are trustworthy. There

are some accounts which hints towards the possibility of fraud in the accounts like those of

depreciation and the repair and maintenance accounts for the reasons which have been

explained above. In addition, the superannuation account also needs to check as it has

decreased by 16% and therefore the employee register needs to be checked if there is a

decline in the number of employees.

5.Recommendations

Some of the recommendations with respect to the audit are:

The fraud risk analysis should be compulsorily done for the given client

Apart from the income statement analysis, the balance sheet analysis also needs to

be done and the opening balances should be checked.

7

The last step which has been asked by the audit partner is fraud risk analysis but he has

recommended that the same need not be carried for the client in hand as Cyan Enterprises

is a trustworthy client. But this contention of the audit partner is completely wrong and

unjustified considering the principles of professional scepticism and the principles of ethics

laid down in APES 110. It is a well-established fact that all the clients need to be assessed for

fraud risk analysis irrespective of the fact that whether or not they are trustworthy. There

are some accounts which hints towards the possibility of fraud in the accounts like those of

depreciation and the repair and maintenance accounts for the reasons which have been

explained above. In addition, the superannuation account also needs to check as it has

decreased by 16% and therefore the employee register needs to be checked if there is a

decline in the number of employees.

5.Recommendations

Some of the recommendations with respect to the audit are:

The fraud risk analysis should be compulsorily done for the given client

Apart from the income statement analysis, the balance sheet analysis also needs to

be done and the opening balances should be checked.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Antonio, G.R., 2014. Continuous auditing: Developing automated audit systems for fraud and error

detections. Journal of Economics, Business & Accountancy Ventura, 17(1), pp.127-144.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. and

Vasarhelyi, M., 2015. Evolution of auditing: From the traditional approach to the future audit. Audit

Analytics, 71.

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐based internal

audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality Judgments:

Properties and Implications for Financial Reporting Reliability.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and audit

assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. and Prawitt, D.F., 2014. Enhancing auditor professional skepticism: The professional

skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or preconditions)» In

audit of financial statement. Mediterranean Journal of Social Sciences, 5(24), p.180.

Lessambo, F.I., 2018. Audit Risks: Identification and Procedures. In Auditing, Assurance Services, and

Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing &

assurance services. McGraw-Hill Education.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation approach

and assertion framing. Behavioral Research in Accounting, 28(2), pp.75-84.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship between

inherent and control risk factors and audit adjustments. Auditing: A Journal of Practice &

Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of Information

Systems, 27(1), pp.325-331.

Wali, S., 2015. Mechanisms of corporate governance and fixed asset revaluation. International

Journal of Accounting and Finance, 5(1), pp.82-97.

8

Antonio, G.R., 2014. Continuous auditing: Developing automated audit systems for fraud and error

detections. Journal of Economics, Business & Accountancy Ventura, 17(1), pp.127-144.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. and

Vasarhelyi, M., 2015. Evolution of auditing: From the traditional approach to the future audit. Audit

Analytics, 71.

Coetzee, P. and Lubbe, D., 2014. Improving the efficiency and effectiveness of risk‐based internal

audit engagements. International Journal of Auditing, 18(2), pp.115-125.

Choudhary, P., Merkley, K.J. and Schipper, K., 2018. Auditors’ Quantitative Materiality Judgments:

Properties and Implications for Financial Reporting Reliability.

Christensen, B.E., Glover, S.M. and Wood, D.A., 2013. Extreme estimation uncertainty and audit

assurance. Current Issues in Auditing, 7(1), pp.P36-P42.

Eilifsen, A. and Messier Jr, W.F., 2014. Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), pp.3-26.

Glover, S.M. and Prawitt, D.F., 2014. Enhancing auditor professional skepticism: The professional

skepticism continuum. Current Issues in Auditing, 8(2), pp.P1-P10.

Kharisova, F.I. and Kozlova, N.N., 2014. Applying the category of «Assertions (or preconditions)» In

audit of financial statement. Mediterranean Journal of Social Sciences, 5(24), p.180.

Lessambo, F.I., 2018. Audit Risks: Identification and Procedures. In Auditing, Assurance Services, and

Forensics(pp. 183-202). Palgrave Macmillan, Cham.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing &

assurance services. McGraw-Hill Education.

Mock, T.J. and Fukukawa, H., 2015. Auditors' risk assessments: The effects of elicitation approach

and assertion framing. Behavioral Research in Accounting, 28(2), pp.75-84.

Ruhnke, K. and Schmidt, M., 2014. Misstatements in financial statements: The relationship between

inherent and control risk factors and audit adjustments. Auditing: A Journal of Practice &

Theory, 33(4), pp.247-269.

Titera, W.R., 2013. Updating audit standard—Enabling audit data analysis. Journal of Information

Systems, 27(1), pp.325-331.

Wali, S., 2015. Mechanisms of corporate governance and fixed asset revaluation. International

Journal of Accounting and Finance, 5(1), pp.82-97.

8

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.