BAO3306 Audit Report: Audit Planning for Murray River Organics 2018

VerifiedAdded on 2023/06/04

|20

|4685

|285

Report

AI Summary

This report details the audit planning process for Murray River Organics, focusing on key aspects such as understanding the client's business, assessing significant accounts, determining planning materiality, and evaluating potential risks. The report identifies trade and other receivables, inventories, property, plant & equipment, trade and other payables, and borrowings as significant accounts. Materiality is calculated based on total revenues, and an assessment of what could go wrong in these accounts is provided, aligning with Australian Auditing Standards. The analysis uses publicly available information from Murray River Organics' annual report to formulate a comprehensive audit plan, emphasizing the importance of audit and assurance for stakeholder confidence and sustainable business practices. Desklib provides access to this and many other solved assignments.

ASSIGNMENT

BAO3306 AUDITING

REPORT

Semester 2, 2018

BAO3306 AUDITING

REPORT

Semester 2, 2018

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Executive summary

The report prepared below highlights the need of audit and assurance work that is

required at the basic level nowadays in any corporate organisation. Irrespective of the level at

which the organisation is working, it is mandatory for it to get its financial accounts and

related reports assured by an independent accountant. Through this report, focus is to bring in

limelight the basic audit planning requirements. The contents of the report include the

discussions regarding the audit materiality, and the selected Murray River Organic’s

significant accounts that are considered material as per the discussion of the concerned and

calculated materiality. All the risks related to the material accounts identified are thoroughly

mentioned. The report is well framed with a concluding note in the end.

The report prepared below highlights the need of audit and assurance work that is

required at the basic level nowadays in any corporate organisation. Irrespective of the level at

which the organisation is working, it is mandatory for it to get its financial accounts and

related reports assured by an independent accountant. Through this report, focus is to bring in

limelight the basic audit planning requirements. The contents of the report include the

discussions regarding the audit materiality, and the selected Murray River Organic’s

significant accounts that are considered material as per the discussion of the concerned and

calculated materiality. All the risks related to the material accounts identified are thoroughly

mentioned. The report is well framed with a concluding note in the end.

2. Introduction

To gain confidence among the shareholders and the other stakeholders, as well as to

retain them, and to further call for new investments from potential shareholders, the Murray

River Organics is required to give some sort of assurance. This assurance can never be

generated as long as the Murray River Organics resorts to its publicity blindly. A faithful

opinion is always relied over as compared to any other medium. This opinion on an

independent basis is provided by the auditor, for the requirement of the company (Prentice,

Bills, and Peters, 2018). This report focused on the audit report of Murray River Organics

(Murray River Organic Group Limited, (2018).

The report is in a research based format that includes a study of the company Murray

River Organics. The study is done for the purpose of gathering information related to audit

engagement assignment. A calculation for the materiality purpose is made using revenues as

the base amount. Depending upon the nature of risk and the materiality certain account

balances have been spotted as being high risk areas. Risk that is related to all these account

balances is theoretically explained. It is analysed as what can go wrong in these accounts, i.e.

what kind of risk may be present in these significant account balances. The report is

formulated using the information which has been made available from the annual report that

the Murray River Organics has publically presented on its official website. But, first of all

before any finding is gathered, a complete client understanding is presented regarding its

business and working profile (Murray River Organic Group Limited, (2018).All the research

that is done on the Murray River Organic’s audit requirements is done and the resulting audit

plan is made as per the requirements of the relevant Australian Auditing Standards. Murray

River Organics needs to implement the proper audit and assurance program if it wants to

sustain its business in long run (Murray River Organic Group Limited, (2018).

To gain confidence among the shareholders and the other stakeholders, as well as to

retain them, and to further call for new investments from potential shareholders, the Murray

River Organics is required to give some sort of assurance. This assurance can never be

generated as long as the Murray River Organics resorts to its publicity blindly. A faithful

opinion is always relied over as compared to any other medium. This opinion on an

independent basis is provided by the auditor, for the requirement of the company (Prentice,

Bills, and Peters, 2018). This report focused on the audit report of Murray River Organics

(Murray River Organic Group Limited, (2018).

The report is in a research based format that includes a study of the company Murray

River Organics. The study is done for the purpose of gathering information related to audit

engagement assignment. A calculation for the materiality purpose is made using revenues as

the base amount. Depending upon the nature of risk and the materiality certain account

balances have been spotted as being high risk areas. Risk that is related to all these account

balances is theoretically explained. It is analysed as what can go wrong in these accounts, i.e.

what kind of risk may be present in these significant account balances. The report is

formulated using the information which has been made available from the annual report that

the Murray River Organics has publically presented on its official website. But, first of all

before any finding is gathered, a complete client understanding is presented regarding its

business and working profile (Murray River Organic Group Limited, (2018).All the research

that is done on the Murray River Organic’s audit requirements is done and the resulting audit

plan is made as per the requirements of the relevant Australian Auditing Standards. Murray

River Organics needs to implement the proper audit and assurance program if it wants to

sustain its business in long run (Murray River Organic Group Limited, (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Key information

a. Our understanding of the client

Murray River Organics has harnessed the highly trending opportunity generated from

the demand of organic products all over the world. It has successfully set up its roots in the

field of supplying vine fruit globally and that too organic. The Murray River Organics has set

up offices in several geographic areas including, Melbourne, Europe, Japan, Sydney, USA,

and China (Murray River Organic Group Limited, (2018). The products of the company

include varied categories like table grapes, dried vine fruit, chia seeds, dried berries, dried

ginger, prunes, quinoa, rice, coconut products, dried mango, dried berries, and nuts (Murray

River Organic Group Limited, (2018).

The aim of the Murray River Organics is to achieve sustainable growth through the

implementation of business practices that are environmentally sound. As far as Australia is

concerned, Murray River Organics has been recognised as the largest producer of dried vine

fruit. The most significant criteria that make the Murray River Organics operate successfully

are the presence of 4400 acres of land that has been certified for organic work. The brands

under the name of which the Murray River Organics operates business are Pacific Organics,

Premium Australian Clusters, Nutritious Foods, and Gobble (Prentice, Bills, and Peters,

2018).

Years of successful operation of the organisation have not been a bubble. The Murray

River Organics has worked hard and has been certified on various grounds. The various

organisations or the certificates that has been credited to the organisation include (Murray

River Organic Group Limited, (2018).

Australian Certified Organic (ACO)

Australian Grown

Safe Quality Food Program

Freshcare

Japanese Agriculture Standard

Hazard Analysis Critical Control Point

Chinese National Organic Products Certification

EU Organic Farming

South Korean Organic Standard Accreditation

United States Department Of Agriculture

a. Our understanding of the client

Murray River Organics has harnessed the highly trending opportunity generated from

the demand of organic products all over the world. It has successfully set up its roots in the

field of supplying vine fruit globally and that too organic. The Murray River Organics has set

up offices in several geographic areas including, Melbourne, Europe, Japan, Sydney, USA,

and China (Murray River Organic Group Limited, (2018). The products of the company

include varied categories like table grapes, dried vine fruit, chia seeds, dried berries, dried

ginger, prunes, quinoa, rice, coconut products, dried mango, dried berries, and nuts (Murray

River Organic Group Limited, (2018).

The aim of the Murray River Organics is to achieve sustainable growth through the

implementation of business practices that are environmentally sound. As far as Australia is

concerned, Murray River Organics has been recognised as the largest producer of dried vine

fruit. The most significant criteria that make the Murray River Organics operate successfully

are the presence of 4400 acres of land that has been certified for organic work. The brands

under the name of which the Murray River Organics operates business are Pacific Organics,

Premium Australian Clusters, Nutritious Foods, and Gobble (Prentice, Bills, and Peters,

2018).

Years of successful operation of the organisation have not been a bubble. The Murray

River Organics has worked hard and has been certified on various grounds. The various

organisations or the certificates that has been credited to the organisation include (Murray

River Organic Group Limited, (2018).

Australian Certified Organic (ACO)

Australian Grown

Safe Quality Food Program

Freshcare

Japanese Agriculture Standard

Hazard Analysis Critical Control Point

Chinese National Organic Products Certification

EU Organic Farming

South Korean Organic Standard Accreditation

United States Department Of Agriculture

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Kosher Food

Halal

B corporation

b. Our assessment of significant accounts

As per the engagement and agreement of audit done in accordance with the ASA 210

Agreeing the Terms of Audit, the auditor accepts the audit and claims the responsibility of

conducting audit professionally (Carson, Zhang, and Fargher, 2014). However, as per ASA

300, planning an audit of Financial Statements, the auditor plans the audit initially. The

planning phase requires the auditor to gather an understanding about the different parameters

that can affect the entity. They may include the entity’s internal control and the environment

of operation (Murray River Organic Group Limited, (2018). However, from the basic

understanding that has been gathered from the understanding of entity, the auditor

preliminarily suspects some of the significant areas that may attract and prove to be highly

risky points for the auditor. Murray River Organics has followed proper CSR program by

adding 5% of its 3 years average profit. It also helps organization to align the interest of the

stakeholders with the development of the business organization. It is found that audit and

assurance program analyse all the information shown in the financial statement of company

(Murray River Organic Group Limited, (2018).

As per the working environment of the organisation and the industry in which the entity is

operating, it is important to switch to early identification of high materially misstated areas of

the concern. For the company Murray River Organics, the significant accounts as per the

judgement of the auditor are identified as follows (Carson, Zhang, and Fargher, 2014).

Trade and other Receivables

Inventories

Property, plant & equipment

Trade and other payables

Borrowings

Now the materiality for these account balances shall be checked in the next step

(Murray River Organic Group Limited, (2018).

Halal

B corporation

b. Our assessment of significant accounts

As per the engagement and agreement of audit done in accordance with the ASA 210

Agreeing the Terms of Audit, the auditor accepts the audit and claims the responsibility of

conducting audit professionally (Carson, Zhang, and Fargher, 2014). However, as per ASA

300, planning an audit of Financial Statements, the auditor plans the audit initially. The

planning phase requires the auditor to gather an understanding about the different parameters

that can affect the entity. They may include the entity’s internal control and the environment

of operation (Murray River Organic Group Limited, (2018). However, from the basic

understanding that has been gathered from the understanding of entity, the auditor

preliminarily suspects some of the significant areas that may attract and prove to be highly

risky points for the auditor. Murray River Organics has followed proper CSR program by

adding 5% of its 3 years average profit. It also helps organization to align the interest of the

stakeholders with the development of the business organization. It is found that audit and

assurance program analyse all the information shown in the financial statement of company

(Murray River Organic Group Limited, (2018).

As per the working environment of the organisation and the industry in which the entity is

operating, it is important to switch to early identification of high materially misstated areas of

the concern. For the company Murray River Organics, the significant accounts as per the

judgement of the auditor are identified as follows (Carson, Zhang, and Fargher, 2014).

Trade and other Receivables

Inventories

Property, plant & equipment

Trade and other payables

Borrowings

Now the materiality for these account balances shall be checked in the next step

(Murray River Organic Group Limited, (2018).

c. Our planning materiality

When any auditor is appointed by the Murray River Organics to provide an assurance

over the accounts of the company, he needs to check the financial information that the entity

has presented. Although a concrete opinion can be framed only when all the business

transactions that took place in the entity are checked by the auditor. However, the practical

world around is not framed on theoretical basis (Murray River Organic Group Limited,

(2018). When real businesses run, they work in deeper ranges. The transactions that take

place are innumerable and cannot be checked as it is by the auditor. A filter is required to be

applied by the auditor which shall help him to identify the most crucial transactions that are

must to be checked for framing an opinion (Lakis, and Masiulevičius, 2017).

However, materiality too is not a term that can be described in the word language of books.

When it comes to the audit of financial statements, the auditor is required to formulate an

audit plan at the start of the audit itself (Murray River Organic Group Limited, (2018). The

audit plan is prepared after the auditor gathers complete knowledge into the operations of the

entity and the external environment which directly or indirectly affects the entity’s

operations. This is done to gain knowledge about the risk that can strike or has already struck

the organisation. It falls in the risk assessment category (Murray River Organic Group

Limited, (2018). The requirements and objectives of ASA 315, Identifying and assessing the

risks of Material Misstatement through Understanding the Entity and its Environment have

specified the same (Eilifsen, Hamilton, and Messier , 2017).

As per ASA 320 Materiality in Planning and Performing an Audit has specified the

significance of planning materiality. However, for audit purposes quantification of planning

materiality is must (Christensen, et. al., 2018). While quantifying materiality certain steps are

sequentially followed. There are following steps would be followed to identify the materiality

level of the identified financial assets and liabilities of the Murray River Organics (Lakis, and

Masiulevičius, 2017).

STEP 1:

The first step is to decide an account balance from which materiality is to be

calculated. The basic thing to be kept in mind while deciding the same is that the selected

base should be stable and least volatile. The base is selected mainly one out of the revenues,

expenses, net income, and equity (Murray River Organic Group Limited, (2018). For Murray

River Organics, the base selected is total revenues. The amount provided for the same is $ 68

million. The total revenue has been selected with a view to evaluate the materiality level and

When any auditor is appointed by the Murray River Organics to provide an assurance

over the accounts of the company, he needs to check the financial information that the entity

has presented. Although a concrete opinion can be framed only when all the business

transactions that took place in the entity are checked by the auditor. However, the practical

world around is not framed on theoretical basis (Murray River Organic Group Limited,

(2018). When real businesses run, they work in deeper ranges. The transactions that take

place are innumerable and cannot be checked as it is by the auditor. A filter is required to be

applied by the auditor which shall help him to identify the most crucial transactions that are

must to be checked for framing an opinion (Lakis, and Masiulevičius, 2017).

However, materiality too is not a term that can be described in the word language of books.

When it comes to the audit of financial statements, the auditor is required to formulate an

audit plan at the start of the audit itself (Murray River Organic Group Limited, (2018). The

audit plan is prepared after the auditor gathers complete knowledge into the operations of the

entity and the external environment which directly or indirectly affects the entity’s

operations. This is done to gain knowledge about the risk that can strike or has already struck

the organisation. It falls in the risk assessment category (Murray River Organic Group

Limited, (2018). The requirements and objectives of ASA 315, Identifying and assessing the

risks of Material Misstatement through Understanding the Entity and its Environment have

specified the same (Eilifsen, Hamilton, and Messier , 2017).

As per ASA 320 Materiality in Planning and Performing an Audit has specified the

significance of planning materiality. However, for audit purposes quantification of planning

materiality is must (Christensen, et. al., 2018). While quantifying materiality certain steps are

sequentially followed. There are following steps would be followed to identify the materiality

level of the identified financial assets and liabilities of the Murray River Organics (Lakis, and

Masiulevičius, 2017).

STEP 1:

The first step is to decide an account balance from which materiality is to be

calculated. The basic thing to be kept in mind while deciding the same is that the selected

base should be stable and least volatile. The base is selected mainly one out of the revenues,

expenses, net income, and equity (Murray River Organic Group Limited, (2018). For Murray

River Organics, the base selected is total revenues. The amount provided for the same is $ 68

million. The total revenue has been selected with a view to evaluate the materiality level and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

changing business condition which would be used to set up the audit risk, detention risk and

control risk of the financial statements.

STEP 2:

After successfully choosing the base account balance a percentage is to be applied to

the selected base. Different percentage range has been specified for different sort of account

balances and are listed as follows:

Revenue : 0.5% - 2%

Expenses : 0.5% - 2%

Net income : 5% - 10%

Equity : 0.5% - 2%

For the company, Murray River Organics, the selected percentage is 0.5%. The

percentage is lowered owing to high risk that has been observed when the material account

balances are checked (Eilifsen, Hamilton, and Messier Jr, 2017).

STEP 3:

The materiality level is calculated by multiplying the base with the percentage

amount. So as per the discussions made above, the materiality decided is:

$ 68 million x 0.5%

= $ 340,016 (Murray River Organic Group Limited, (2018).

Looking at the part (b) above, it gets evident that the significant account balance does comply

with the materiality level that has been set here. All the identified significant account balance

falls in the material region criteria also. All those significant account balances are in this

manner material and need a detailed check by the auditor (Christensen, Eilifsen, Glover, and

Messier, 2018).

From the significant account balances that are observed and checked material are listed below

with their financial account balance (Murray River Organic Group Limited, (2018).

ACCOUNT BALANCE AMOUNT

Trade and other receivables 6,729,000

Inventories 16,194,000

control risk of the financial statements.

STEP 2:

After successfully choosing the base account balance a percentage is to be applied to

the selected base. Different percentage range has been specified for different sort of account

balances and are listed as follows:

Revenue : 0.5% - 2%

Expenses : 0.5% - 2%

Net income : 5% - 10%

Equity : 0.5% - 2%

For the company, Murray River Organics, the selected percentage is 0.5%. The

percentage is lowered owing to high risk that has been observed when the material account

balances are checked (Eilifsen, Hamilton, and Messier Jr, 2017).

STEP 3:

The materiality level is calculated by multiplying the base with the percentage

amount. So as per the discussions made above, the materiality decided is:

$ 68 million x 0.5%

= $ 340,016 (Murray River Organic Group Limited, (2018).

Looking at the part (b) above, it gets evident that the significant account balance does comply

with the materiality level that has been set here. All the identified significant account balance

falls in the material region criteria also. All those significant account balances are in this

manner material and need a detailed check by the auditor (Christensen, Eilifsen, Glover, and

Messier, 2018).

From the significant account balances that are observed and checked material are listed below

with their financial account balance (Murray River Organic Group Limited, (2018).

ACCOUNT BALANCE AMOUNT

Trade and other receivables 6,729,000

Inventories 16,194,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Property, plant and equipment 67,610,000

Trade and other payables 11,825,000

Borrowings 47,161,000

(Murray River Organic Group Limited, (2018).

These five assets and liabilities have been determined on the basis of the financial

information shown in the annual report of Murray River Organics (Murray River Organic

Group Limited, (2018).

d. Our assessment of what can go wrong

Whenever, an audit commences, it is expected out of the auditor that he shall be

sceptical regarding the activities of the entity. When it comes to framing an opinion, there

also the language requires the auditor to state that he has conducted the audit in accordance

with the best of his understanding and knowledge (Murray River Organic Group Limited,

(2018). ASA 315, Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and its Environment, requires the auditor to assess the entity’s

environment and work on identify the highly risky areas. This understanding also involves

assessing the risk, i.e. understanding what can happen wrong in the organisation and where

(Murray River Organic Group Limited, (2018). It is the basic knowledge that the auditor

requires to pave the way for conducting the audit in the most efficient manner. In addition to

this, audit risk model is also used by the auditors to determine the audit risk associated with

the financial statement of Murray River Organics. It is based on the detention risk and control

risk of the financial statement (Barr-Pulliam, Brown-Liburd, and Sanderson, 2017).

The audit risk assessment is done in accordance with the judgement that the auditor

frames for the organisation. This judgement helps him to formulate certain questions and

thrive for answers to resolve his doubts to reassure himself that the financials are not

materially misstated. The audit risk is highly based on the control risk and detention risk of

the financial statement (Murray River Organic Group Limited, (2018).

Trade and other payables 11,825,000

Borrowings 47,161,000

(Murray River Organic Group Limited, (2018).

These five assets and liabilities have been determined on the basis of the financial

information shown in the annual report of Murray River Organics (Murray River Organic

Group Limited, (2018).

d. Our assessment of what can go wrong

Whenever, an audit commences, it is expected out of the auditor that he shall be

sceptical regarding the activities of the entity. When it comes to framing an opinion, there

also the language requires the auditor to state that he has conducted the audit in accordance

with the best of his understanding and knowledge (Murray River Organic Group Limited,

(2018). ASA 315, Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and its Environment, requires the auditor to assess the entity’s

environment and work on identify the highly risky areas. This understanding also involves

assessing the risk, i.e. understanding what can happen wrong in the organisation and where

(Murray River Organic Group Limited, (2018). It is the basic knowledge that the auditor

requires to pave the way for conducting the audit in the most efficient manner. In addition to

this, audit risk model is also used by the auditors to determine the audit risk associated with

the financial statement of Murray River Organics. It is based on the detention risk and control

risk of the financial statement (Barr-Pulliam, Brown-Liburd, and Sanderson, 2017).

The audit risk assessment is done in accordance with the judgement that the auditor

frames for the organisation. This judgement helps him to formulate certain questions and

thrive for answers to resolve his doubts to reassure himself that the financials are not

materially misstated. The audit risk is highly based on the control risk and detention risk of

the financial statement (Murray River Organic Group Limited, (2018).

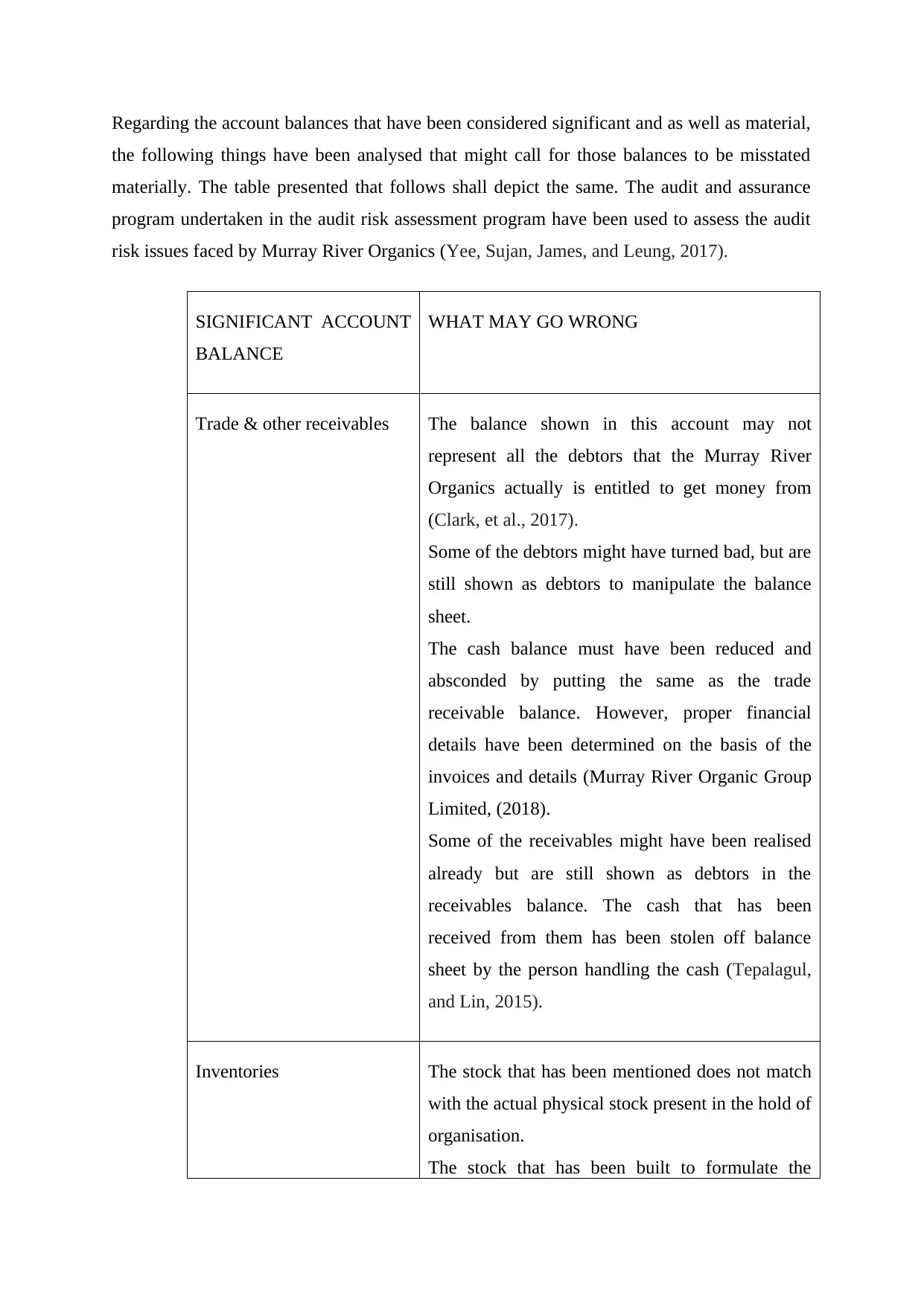

Regarding the account balances that have been considered significant and as well as material,

the following things have been analysed that might call for those balances to be misstated

materially. The table presented that follows shall depict the same. The audit and assurance

program undertaken in the audit risk assessment program have been used to assess the audit

risk issues faced by Murray River Organics (Yee, Sujan, James, and Leung, 2017).

SIGNIFICANT ACCOUNT

BALANCE

WHAT MAY GO WRONG

Trade & other receivables The balance shown in this account may not

represent all the debtors that the Murray River

Organics actually is entitled to get money from

(Clark, et al., 2017).

Some of the debtors might have turned bad, but are

still shown as debtors to manipulate the balance

sheet.

The cash balance must have been reduced and

absconded by putting the same as the trade

receivable balance. However, proper financial

details have been determined on the basis of the

invoices and details (Murray River Organic Group

Limited, (2018).

Some of the receivables might have been realised

already but are still shown as debtors in the

receivables balance. The cash that has been

received from them has been stolen off balance

sheet by the person handling the cash (Tepalagul,

and Lin, 2015).

Inventories The stock that has been mentioned does not match

with the actual physical stock present in the hold of

organisation.

The stock that has been built to formulate the

the following things have been analysed that might call for those balances to be misstated

materially. The table presented that follows shall depict the same. The audit and assurance

program undertaken in the audit risk assessment program have been used to assess the audit

risk issues faced by Murray River Organics (Yee, Sujan, James, and Leung, 2017).

SIGNIFICANT ACCOUNT

BALANCE

WHAT MAY GO WRONG

Trade & other receivables The balance shown in this account may not

represent all the debtors that the Murray River

Organics actually is entitled to get money from

(Clark, et al., 2017).

Some of the debtors might have turned bad, but are

still shown as debtors to manipulate the balance

sheet.

The cash balance must have been reduced and

absconded by putting the same as the trade

receivable balance. However, proper financial

details have been determined on the basis of the

invoices and details (Murray River Organic Group

Limited, (2018).

Some of the receivables might have been realised

already but are still shown as debtors in the

receivables balance. The cash that has been

received from them has been stolen off balance

sheet by the person handling the cash (Tepalagul,

and Lin, 2015).

Inventories The stock that has been mentioned does not match

with the actual physical stock present in the hold of

organisation.

The stock that has been built to formulate the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

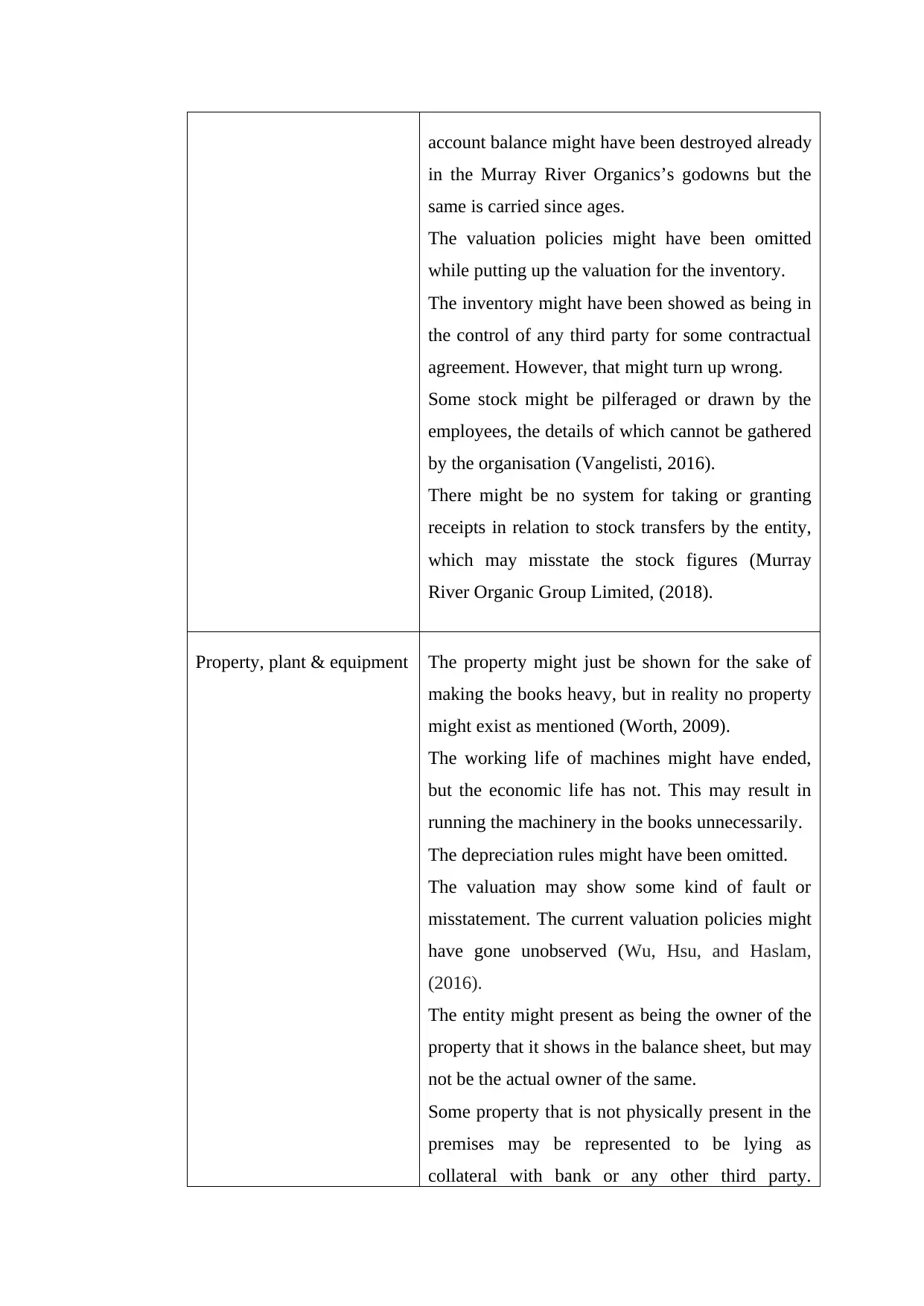

account balance might have been destroyed already

in the Murray River Organics’s godowns but the

same is carried since ages.

The valuation policies might have been omitted

while putting up the valuation for the inventory.

The inventory might have been showed as being in

the control of any third party for some contractual

agreement. However, that might turn up wrong.

Some stock might be pilferaged or drawn by the

employees, the details of which cannot be gathered

by the organisation (Vangelisti, 2016).

There might be no system for taking or granting

receipts in relation to stock transfers by the entity,

which may misstate the stock figures (Murray

River Organic Group Limited, (2018).

Property, plant & equipment The property might just be shown for the sake of

making the books heavy, but in reality no property

might exist as mentioned (Worth, 2009).

The working life of machines might have ended,

but the economic life has not. This may result in

running the machinery in the books unnecessarily.

The depreciation rules might have been omitted.

The valuation may show some kind of fault or

misstatement. The current valuation policies might

have gone unobserved (Wu, Hsu, and Haslam,

(2016).

The entity might present as being the owner of the

property that it shows in the balance sheet, but may

not be the actual owner of the same.

Some property that is not physically present in the

premises may be represented to be lying as

collateral with bank or any other third party.

in the Murray River Organics’s godowns but the

same is carried since ages.

The valuation policies might have been omitted

while putting up the valuation for the inventory.

The inventory might have been showed as being in

the control of any third party for some contractual

agreement. However, that might turn up wrong.

Some stock might be pilferaged or drawn by the

employees, the details of which cannot be gathered

by the organisation (Vangelisti, 2016).

There might be no system for taking or granting

receipts in relation to stock transfers by the entity,

which may misstate the stock figures (Murray

River Organic Group Limited, (2018).

Property, plant & equipment The property might just be shown for the sake of

making the books heavy, but in reality no property

might exist as mentioned (Worth, 2009).

The working life of machines might have ended,

but the economic life has not. This may result in

running the machinery in the books unnecessarily.

The depreciation rules might have been omitted.

The valuation may show some kind of fault or

misstatement. The current valuation policies might

have gone unobserved (Wu, Hsu, and Haslam,

(2016).

The entity might present as being the owner of the

property that it shows in the balance sheet, but may

not be the actual owner of the same.

Some property that is not physically present in the

premises may be represented to be lying as

collateral with bank or any other third party.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

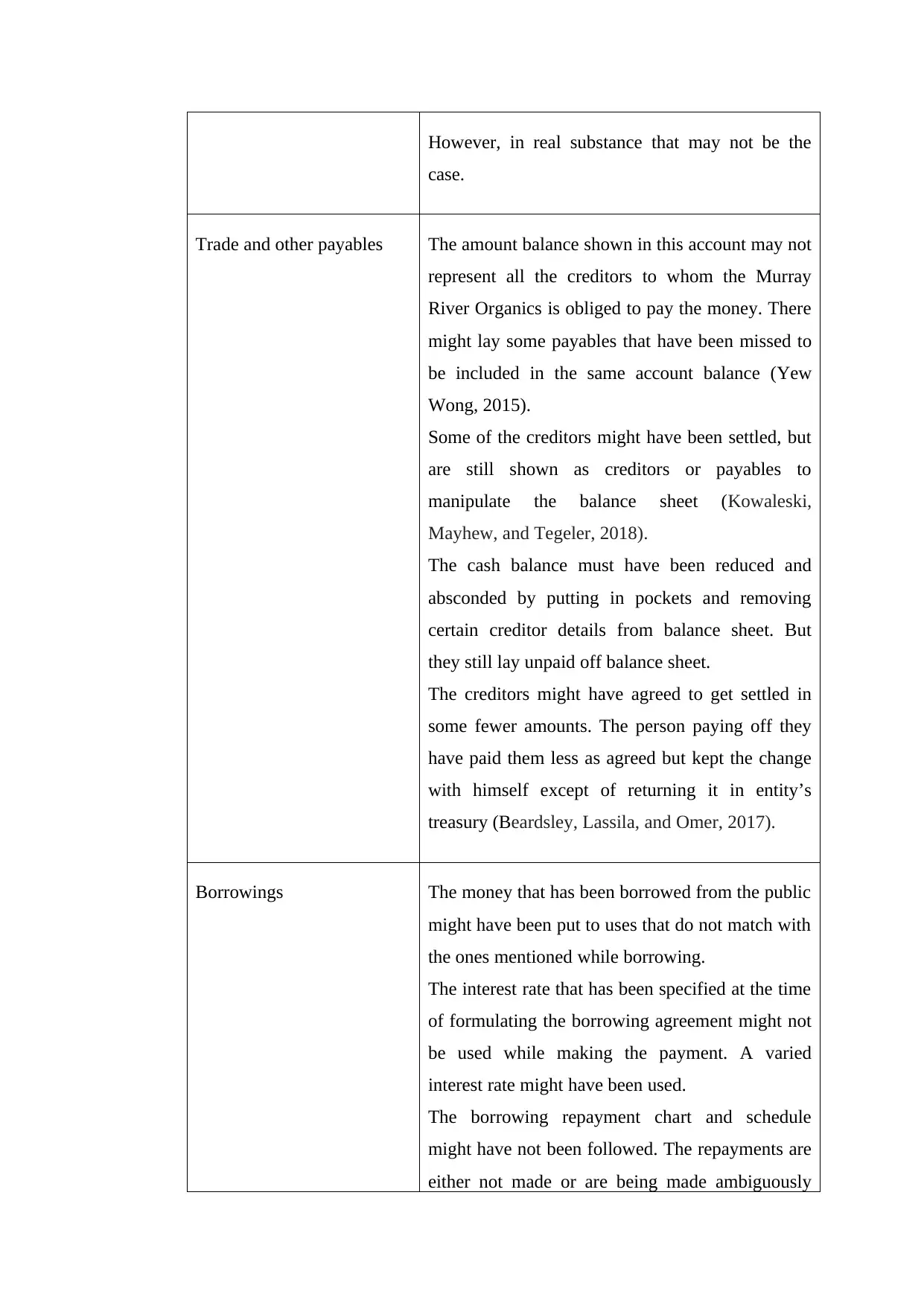

However, in real substance that may not be the

case.

Trade and other payables The amount balance shown in this account may not

represent all the creditors to whom the Murray

River Organics is obliged to pay the money. There

might lay some payables that have been missed to

be included in the same account balance (Yew

Wong, 2015).

Some of the creditors might have been settled, but

are still shown as creditors or payables to

manipulate the balance sheet (Kowaleski,

Mayhew, and Tegeler, 2018).

The cash balance must have been reduced and

absconded by putting in pockets and removing

certain creditor details from balance sheet. But

they still lay unpaid off balance sheet.

The creditors might have agreed to get settled in

some fewer amounts. The person paying off they

have paid them less as agreed but kept the change

with himself except of returning it in entity’s

treasury (Beardsley, Lassila, and Omer, 2017).

Borrowings The money that has been borrowed from the public

might have been put to uses that do not match with

the ones mentioned while borrowing.

The interest rate that has been specified at the time

of formulating the borrowing agreement might not

be used while making the payment. A varied

interest rate might have been used.

The borrowing repayment chart and schedule

might have not been followed. The repayments are

either not made or are being made ambiguously

case.

Trade and other payables The amount balance shown in this account may not

represent all the creditors to whom the Murray

River Organics is obliged to pay the money. There

might lay some payables that have been missed to

be included in the same account balance (Yew

Wong, 2015).

Some of the creditors might have been settled, but

are still shown as creditors or payables to

manipulate the balance sheet (Kowaleski,

Mayhew, and Tegeler, 2018).

The cash balance must have been reduced and

absconded by putting in pockets and removing

certain creditor details from balance sheet. But

they still lay unpaid off balance sheet.

The creditors might have agreed to get settled in

some fewer amounts. The person paying off they

have paid them less as agreed but kept the change

with himself except of returning it in entity’s

treasury (Beardsley, Lassila, and Omer, 2017).

Borrowings The money that has been borrowed from the public

might have been put to uses that do not match with

the ones mentioned while borrowing.

The interest rate that has been specified at the time

of formulating the borrowing agreement might not

be used while making the payment. A varied

interest rate might have been used.

The borrowing repayment chart and schedule

might have not been followed. The repayments are

either not made or are being made ambiguously

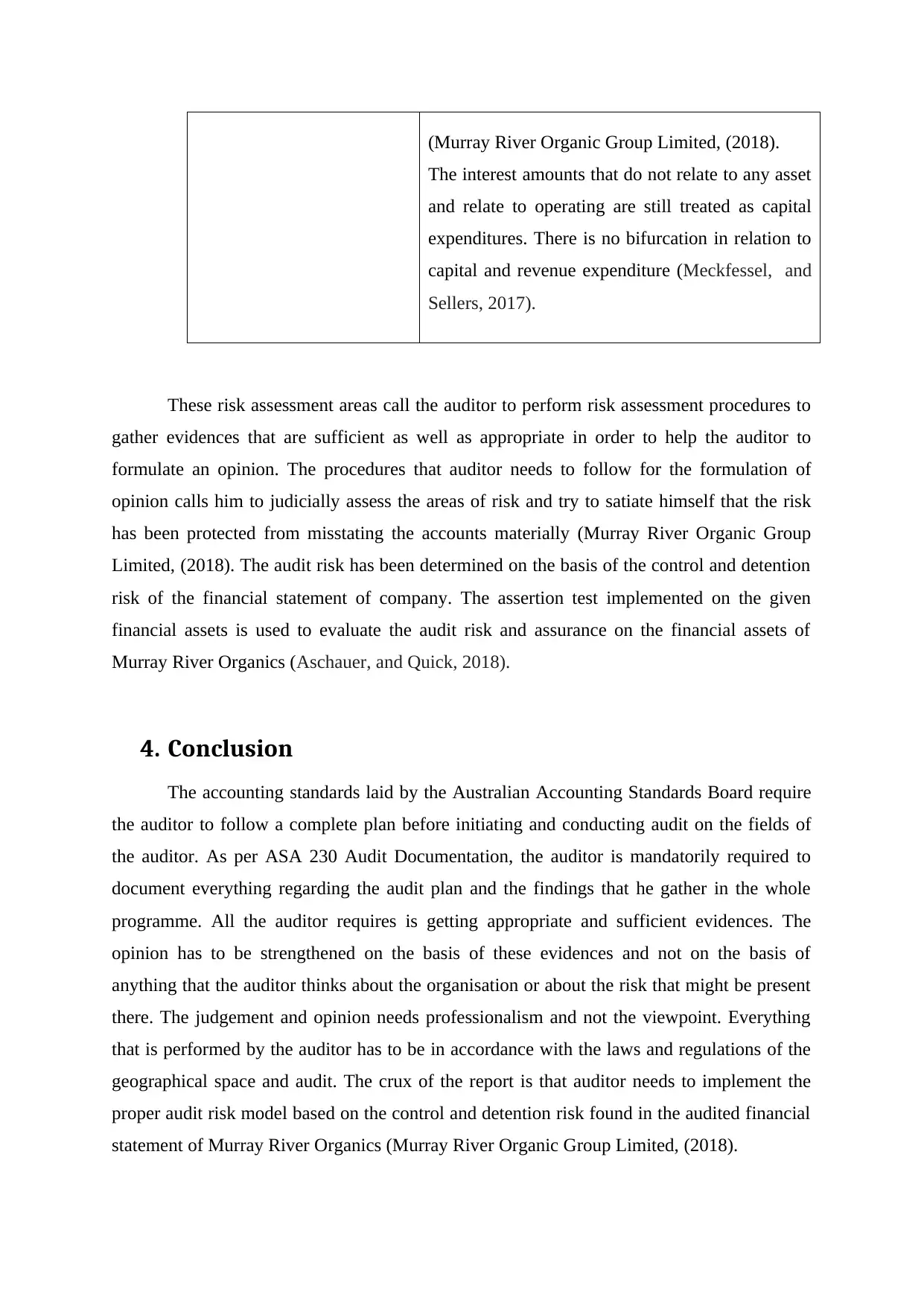

(Murray River Organic Group Limited, (2018).

The interest amounts that do not relate to any asset

and relate to operating are still treated as capital

expenditures. There is no bifurcation in relation to

capital and revenue expenditure (Meckfessel, and

Sellers, 2017).

These risk assessment areas call the auditor to perform risk assessment procedures to

gather evidences that are sufficient as well as appropriate in order to help the auditor to

formulate an opinion. The procedures that auditor needs to follow for the formulation of

opinion calls him to judicially assess the areas of risk and try to satiate himself that the risk

has been protected from misstating the accounts materially (Murray River Organic Group

Limited, (2018). The audit risk has been determined on the basis of the control and detention

risk of the financial statement of company. The assertion test implemented on the given

financial assets is used to evaluate the audit risk and assurance on the financial assets of

Murray River Organics (Aschauer, and Quick, 2018).

4. Conclusion

The accounting standards laid by the Australian Accounting Standards Board require

the auditor to follow a complete plan before initiating and conducting audit on the fields of

the auditor. As per ASA 230 Audit Documentation, the auditor is mandatorily required to

document everything regarding the audit plan and the findings that he gather in the whole

programme. All the auditor requires is getting appropriate and sufficient evidences. The

opinion has to be strengthened on the basis of these evidences and not on the basis of

anything that the auditor thinks about the organisation or about the risk that might be present

there. The judgement and opinion needs professionalism and not the viewpoint. Everything

that is performed by the auditor has to be in accordance with the laws and regulations of the

geographical space and audit. The crux of the report is that auditor needs to implement the

proper audit risk model based on the control and detention risk found in the audited financial

statement of Murray River Organics (Murray River Organic Group Limited, (2018).

The interest amounts that do not relate to any asset

and relate to operating are still treated as capital

expenditures. There is no bifurcation in relation to

capital and revenue expenditure (Meckfessel, and

Sellers, 2017).

These risk assessment areas call the auditor to perform risk assessment procedures to

gather evidences that are sufficient as well as appropriate in order to help the auditor to

formulate an opinion. The procedures that auditor needs to follow for the formulation of

opinion calls him to judicially assess the areas of risk and try to satiate himself that the risk

has been protected from misstating the accounts materially (Murray River Organic Group

Limited, (2018). The audit risk has been determined on the basis of the control and detention

risk of the financial statement of company. The assertion test implemented on the given

financial assets is used to evaluate the audit risk and assurance on the financial assets of

Murray River Organics (Aschauer, and Quick, 2018).

4. Conclusion

The accounting standards laid by the Australian Accounting Standards Board require

the auditor to follow a complete plan before initiating and conducting audit on the fields of

the auditor. As per ASA 230 Audit Documentation, the auditor is mandatorily required to

document everything regarding the audit plan and the findings that he gather in the whole

programme. All the auditor requires is getting appropriate and sufficient evidences. The

opinion has to be strengthened on the basis of these evidences and not on the basis of

anything that the auditor thinks about the organisation or about the risk that might be present

there. The judgement and opinion needs professionalism and not the viewpoint. Everything

that is performed by the auditor has to be in accordance with the laws and regulations of the

geographical space and audit. The crux of the report is that auditor needs to implement the

proper audit risk model based on the control and detention risk found in the audited financial

statement of Murray River Organics (Murray River Organic Group Limited, (2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.