Audit Planning Report: Financial Statement Analysis and Procedures

VerifiedAdded on 2020/03/16

|18

|3335

|102

Report

AI Summary

This report delves into the core principles of audit planning, commencing with an overview of the audit process and the auditor's responsibility to develop a comprehensive audit plan. It explores the importance of analytical review, the assessment of materiality, and the application of audit procedures to key accounts. The report examines specific accounts such as inventory, accounts receivables, sales, owner's equity, motor vehicles, interest expense, and superannuation, providing rationales for their selection, outlining management assertions, and recommending appropriate audit procedures. Furthermore, it incorporates comparative financial statements, including income statements and balance sheets, to highlight financial performance and position. The report emphasizes the importance of understanding inherent risks, implementing effective internal controls, and conducting thorough audit procedures to mitigate the risks of material misstatements. The report concludes by highlighting the significance of audit planning in ensuring the accuracy and reliability of financial statements.

Running head: audit planning

AUDIT PLANNING

AUDIT PLANNING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit planning 1

Contents

Audit Planning.............................................................................................................................................3

Analytical Review...................................................................................................................................3

Preliminary Judgement of materiality......................................................................................................3

Inventory.....................................................................................................................................................4

Rationale for selection.............................................................................................................................4

Assertion and explanation........................................................................................................................4

Recommended audit procedure...............................................................................................................4

Accounts Receivables..................................................................................................................................4

Rationale for selection.............................................................................................................................4

Assertions and explanations....................................................................................................................5

Recommend audit procedure...................................................................................................................5

Sales............................................................................................................................................................5

Rationale for selection.............................................................................................................................5

Assertions and explanation......................................................................................................................5

Recommended audit procedure...............................................................................................................5

Owner’s equity............................................................................................................................................6

Rationale for selection.............................................................................................................................6

Assertions and explanations....................................................................................................................6

Recommended audit procedure...............................................................................................................6

Motor vehicles.............................................................................................................................................6

Rationale for selection.............................................................................................................................6

Assertions and explanations....................................................................................................................6

Recommended audit procedure...............................................................................................................7

Interest expense...........................................................................................................................................7

Rationale for selection.............................................................................................................................7

Assertions and explanations....................................................................................................................7

Recommended audit procedure...............................................................................................................7

Superannuation............................................................................................................................................8

Rationale for selection.............................................................................................................................8

Assertions and explanations....................................................................................................................8

Recommended audit procedure...............................................................................................................8

Contents

Audit Planning.............................................................................................................................................3

Analytical Review...................................................................................................................................3

Preliminary Judgement of materiality......................................................................................................3

Inventory.....................................................................................................................................................4

Rationale for selection.............................................................................................................................4

Assertion and explanation........................................................................................................................4

Recommended audit procedure...............................................................................................................4

Accounts Receivables..................................................................................................................................4

Rationale for selection.............................................................................................................................4

Assertions and explanations....................................................................................................................5

Recommend audit procedure...................................................................................................................5

Sales............................................................................................................................................................5

Rationale for selection.............................................................................................................................5

Assertions and explanation......................................................................................................................5

Recommended audit procedure...............................................................................................................5

Owner’s equity............................................................................................................................................6

Rationale for selection.............................................................................................................................6

Assertions and explanations....................................................................................................................6

Recommended audit procedure...............................................................................................................6

Motor vehicles.............................................................................................................................................6

Rationale for selection.............................................................................................................................6

Assertions and explanations....................................................................................................................6

Recommended audit procedure...............................................................................................................7

Interest expense...........................................................................................................................................7

Rationale for selection.............................................................................................................................7

Assertions and explanations....................................................................................................................7

Recommended audit procedure...............................................................................................................7

Superannuation............................................................................................................................................8

Rationale for selection.............................................................................................................................8

Assertions and explanations....................................................................................................................8

Recommended audit procedure...............................................................................................................8

Audit planning 2

Comparative income statement....................................................................................................................9

Balance sheet.............................................................................................................................................11

References.................................................................................................................................................14

Comparative income statement....................................................................................................................9

Balance sheet.............................................................................................................................................11

References.................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit planning 3

Audit Planning

Audit planning is the beginning of the procedure of auditing. It is an auditor’s responsibility to

plan audit properly. As the planning include forming the strategies to develop an audit plan

which takes in particular planning the risk assessing procedures and plan the resultants to the

risks associated with the material misstatement (Hayes, 2014). Audit planning is the continuous

process starts after the previous audit ends. The whole plan includes nature, time and extent of

the procedures to be followed for the assessment of risk and various tests are to be done on these

procedures and its controls. Auditor makes sure to plan in alignment of the business standards

(Knechel, 2016).

Analytical Review

As it is clear from the name analytical review is a review of extensive ratios and trends in the

income statement and balance sheet. It basically investigates any unusual activity or fluctuation

of the items in the said income statement and balance sheet. The dependency an auditor places

on the results of the analytical review based on the facts which includes materiality, control risks

and assessment. This review assist auditor in planning the nature and extent of the audit

procedures to improve the effectiveness and reduces the detection risk for some specific financial

statement. The main purpose of analytical review is the review of financial statement in the final

stage overall (Frost, 2017).

Preliminary Judgement of materiality

It is one of the major step in applying materiality where judgements are required to be made to

the clients in regard to the materiality. At first auditor establish a preliminary judgement that

what base can be chosen and multiplied by the percentage factor in order to determine

quantitative judgement which can be further adjusted for qualitative factors about materiality.

Secondly the preliminary judgement of materiality is allocated to the classes of transactions and

make possible for auditor to plan the scope of procedures. Lastly the estimation are made for

misstatements and being compared to the judgement about materiality (Bahr, 2014).

Audit Planning

Audit planning is the beginning of the procedure of auditing. It is an auditor’s responsibility to

plan audit properly. As the planning include forming the strategies to develop an audit plan

which takes in particular planning the risk assessing procedures and plan the resultants to the

risks associated with the material misstatement (Hayes, 2014). Audit planning is the continuous

process starts after the previous audit ends. The whole plan includes nature, time and extent of

the procedures to be followed for the assessment of risk and various tests are to be done on these

procedures and its controls. Auditor makes sure to plan in alignment of the business standards

(Knechel, 2016).

Analytical Review

As it is clear from the name analytical review is a review of extensive ratios and trends in the

income statement and balance sheet. It basically investigates any unusual activity or fluctuation

of the items in the said income statement and balance sheet. The dependency an auditor places

on the results of the analytical review based on the facts which includes materiality, control risks

and assessment. This review assist auditor in planning the nature and extent of the audit

procedures to improve the effectiveness and reduces the detection risk for some specific financial

statement. The main purpose of analytical review is the review of financial statement in the final

stage overall (Frost, 2017).

Preliminary Judgement of materiality

It is one of the major step in applying materiality where judgements are required to be made to

the clients in regard to the materiality. At first auditor establish a preliminary judgement that

what base can be chosen and multiplied by the percentage factor in order to determine

quantitative judgement which can be further adjusted for qualitative factors about materiality.

Secondly the preliminary judgement of materiality is allocated to the classes of transactions and

make possible for auditor to plan the scope of procedures. Lastly the estimation are made for

misstatements and being compared to the judgement about materiality (Bahr, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit planning 4

Inventory

1. Inventory has been selected from the given trial balance as the inventory account can be

seen at-risk of material misstatement.

Rationale for selection

The audit of inventory carries significant risks along with it as inventories represent a major

portion in the current assets and inventory is known to be the base from where all the valuation

methods are used and it directly impact the cost of goods sold. There is an inherent complexity in

determining the quality and value of inventory. In the income statement the percentage change

can be seen which is negative (Krishnan, 2014).

Assertion and explanation

For inventory there are five management assertions while an audit takes place. The occurrence

tests taken by having the samples of purchase vouchers and vouch them to requisitions it is

basically tracing of vouchers to support the document. Then completeness is being evaluated as

completeness in inventory process is of higher risk as it may lead to the occurrence of poor

inventory controls. The third is authorization which addresses whether proper internal control is

followed and by selecting a sample of inventory the authorization can be checked. Fourth is

accuracy, it addresses whether the purchase transactions are containing any error or not. Last is

cutoff which involves the reporting of transactions that they are being correctly recorded or not

(Lenz, 2014).

Recommended audit procedure

Here as per the study of trial balance the audit procedure which can be followed would be

reconciling the inventory count with the general ledger it helps in observing the physical count of

inventory (Cannon, 2016).

Accounts Receivables

2. Account receivables is been selected from the given trial balance as it represents audit

risk and other problems.

Rationale for selection

There are several potential problems exist while auditing, it could create material misstatement.

The material misstatement may have some errors and few would indicate frauds. There can be

Inventory

1. Inventory has been selected from the given trial balance as the inventory account can be

seen at-risk of material misstatement.

Rationale for selection

The audit of inventory carries significant risks along with it as inventories represent a major

portion in the current assets and inventory is known to be the base from where all the valuation

methods are used and it directly impact the cost of goods sold. There is an inherent complexity in

determining the quality and value of inventory. In the income statement the percentage change

can be seen which is negative (Krishnan, 2014).

Assertion and explanation

For inventory there are five management assertions while an audit takes place. The occurrence

tests taken by having the samples of purchase vouchers and vouch them to requisitions it is

basically tracing of vouchers to support the document. Then completeness is being evaluated as

completeness in inventory process is of higher risk as it may lead to the occurrence of poor

inventory controls. The third is authorization which addresses whether proper internal control is

followed and by selecting a sample of inventory the authorization can be checked. Fourth is

accuracy, it addresses whether the purchase transactions are containing any error or not. Last is

cutoff which involves the reporting of transactions that they are being correctly recorded or not

(Lenz, 2014).

Recommended audit procedure

Here as per the study of trial balance the audit procedure which can be followed would be

reconciling the inventory count with the general ledger it helps in observing the physical count of

inventory (Cannon, 2016).

Accounts Receivables

2. Account receivables is been selected from the given trial balance as it represents audit

risk and other problems.

Rationale for selection

There are several potential problems exist while auditing, it could create material misstatement.

The material misstatement may have some errors and few would indicate frauds. There can be

Audit planning 5

many errors involved while auditing account receivables as it consists of all amounts which

could have been manipulated and result into frauds (Arens et al., 2016).

Assertions and explanations

The company can place a system to record the related transactions and make proper shipment,

control and collect the receivables which helps in preventing errors and frauds. All the entries are

to be mount up and forwarded to the general accounts department (Moroney et al., 2014).

Recommend audit procedure

By performing analytical procedure auditor can identify the client figures and auditor’s

expectations and they help in assessing the inherent risks associated with the account receivables.

The completeness should be tested in the procedure adopted (Johnstone, 2013).

Sales

3. There is always a chance that sales could be false. The income shown reduced in order to

show the report of income down.

Rationale for selection

Sales is one of the most fraudulent account occurred in many companies. As sales affect most

the financial statement of the business which directly impact the profits of the company,

salaries of the workers and creates a market share which attract stakeholders to invest more.

Assertions and explanation

It needs a basic internal control strategy where customer invoice is compare and send to the

sales department to keep the record properly and cross check whenever required. If balance

still doesn’t match up with the actual records then both collection and receivable department

are filed and actions planned for the same (Arena, 2016).

Recommended audit procedure

By looking at the overall balance of sales, the returns and the debts and being compare it to

the past years to check the accuracy and the completeness which later on verify the actual

transactions.

many errors involved while auditing account receivables as it consists of all amounts which

could have been manipulated and result into frauds (Arens et al., 2016).

Assertions and explanations

The company can place a system to record the related transactions and make proper shipment,

control and collect the receivables which helps in preventing errors and frauds. All the entries are

to be mount up and forwarded to the general accounts department (Moroney et al., 2014).

Recommend audit procedure

By performing analytical procedure auditor can identify the client figures and auditor’s

expectations and they help in assessing the inherent risks associated with the account receivables.

The completeness should be tested in the procedure adopted (Johnstone, 2013).

Sales

3. There is always a chance that sales could be false. The income shown reduced in order to

show the report of income down.

Rationale for selection

Sales is one of the most fraudulent account occurred in many companies. As sales affect most

the financial statement of the business which directly impact the profits of the company,

salaries of the workers and creates a market share which attract stakeholders to invest more.

Assertions and explanation

It needs a basic internal control strategy where customer invoice is compare and send to the

sales department to keep the record properly and cross check whenever required. If balance

still doesn’t match up with the actual records then both collection and receivable department

are filed and actions planned for the same (Arena, 2016).

Recommended audit procedure

By looking at the overall balance of sales, the returns and the debts and being compare it to

the past years to check the accuracy and the completeness which later on verify the actual

transactions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit planning 6

Owner’s equity

4. The said account is chosen from the trial balance as owner’s equity are known to be an

important aspect in financial statement and they are the riskier in audit procedure. The

fall in owner’s equity can be evident in the comparative balance sheet here under.

Rationale for selection

Equity is to be known as the pivotal part of the financial statement which indicates the flow

of liquidity in the account balances of bank and the organizations. It is also one of the major

element where frauds and errors are detected and result into inaccurate cash position of a

company.

Assertions and explanations

The existence needs to be checked by proofing the cash receipts which have been deposited

into the bank. Secondly determining the checks whether there are any missing or outstanding

checks left which can affect the cash balance understated or over stated.

Recommended audit procedure

The audit procedure for equity account can be analytical only. Where the prior owner’s

equity is being compared to current year’s balance and make necessary provisions for the

same.

Motor vehicles

5. Motor vehicles do consider various inherent risks of misstatements and materiality. The

management of fixed asset process helps in identifying risks and provide control.

Rationale for selection

Fixed assets generally create difficulty while audit takes place because of the complexity

presented in the accounting transactions. Every organization has different aspect of

calculating costs of their fixed assets which creates problems for auditor on how to measure

the accuracy.

Assertions and explanations

By recording the purchase cost on the cost basis it is to be checked that any repairs or

maintenance are added up in the account under the fixed assets. The complexities of knowing

what major repairs are needed to add under the head fixed assets. Most of the fixed asset

Owner’s equity

4. The said account is chosen from the trial balance as owner’s equity are known to be an

important aspect in financial statement and they are the riskier in audit procedure. The

fall in owner’s equity can be evident in the comparative balance sheet here under.

Rationale for selection

Equity is to be known as the pivotal part of the financial statement which indicates the flow

of liquidity in the account balances of bank and the organizations. It is also one of the major

element where frauds and errors are detected and result into inaccurate cash position of a

company.

Assertions and explanations

The existence needs to be checked by proofing the cash receipts which have been deposited

into the bank. Secondly determining the checks whether there are any missing or outstanding

checks left which can affect the cash balance understated or over stated.

Recommended audit procedure

The audit procedure for equity account can be analytical only. Where the prior owner’s

equity is being compared to current year’s balance and make necessary provisions for the

same.

Motor vehicles

5. Motor vehicles do consider various inherent risks of misstatements and materiality. The

management of fixed asset process helps in identifying risks and provide control.

Rationale for selection

Fixed assets generally create difficulty while audit takes place because of the complexity

presented in the accounting transactions. Every organization has different aspect of

calculating costs of their fixed assets which creates problems for auditor on how to measure

the accuracy.

Assertions and explanations

By recording the purchase cost on the cost basis it is to be checked that any repairs or

maintenance are added up in the account under the fixed assets. The complexities of knowing

what major repairs are needed to add under the head fixed assets. Most of the fixed asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit planning 7

calculations are easier and straightforward and can be recorded on the cost basis directly but

there are lease accounting which are not purchased they carry complex accounting issues and

creates inherent risks while auditing.

Recommended audit procedure

In order to avoid such complexities and inherent risks while auditing fixed assets there is an

audit procedure which is required to be followed is verifying the ownership of the asset

whether it is the machinery, furniture, motor vehicles as mentioned in the given trial balance.

The ownership is being examined and confirmed by the title of documents of the said

property as mentioned above gives the proper proof which helps in verifying the costs

attached to it.

Interest expense

6. Interest expense is one of the unique expense who involve such inherent risks while

taking up the auditing.

Rationale for selection

Interest expense involve few risks which are quite unique in nature. The inherent and control

risk associated with such expense relates to the material misstatement as there are few

expense who are less riskier than others it shows a complexity while auditing the interest

expense. In the comparative balance it can be seen that it shows a percentage decrease.

Assertions and explanations

The identification of some specific but known misstatements are being carried on and

concluded that if any such misstatement exists or not. Then if required the substantive

analytical procedures are followed which indicates the errors in the class of transactions and

balances of accounts. The expenses are compared their intensity of risks associated are

compared and on the basis of the intensity the auditor verify the expenses.

Recommended audit procedure

The recommended audit procedure for the audit of interest expense account is a detailed

observation into the account details to check the level of intensity an expense is having as it

shows the cash outflow so it is important to not to ignore the fact.

calculations are easier and straightforward and can be recorded on the cost basis directly but

there are lease accounting which are not purchased they carry complex accounting issues and

creates inherent risks while auditing.

Recommended audit procedure

In order to avoid such complexities and inherent risks while auditing fixed assets there is an

audit procedure which is required to be followed is verifying the ownership of the asset

whether it is the machinery, furniture, motor vehicles as mentioned in the given trial balance.

The ownership is being examined and confirmed by the title of documents of the said

property as mentioned above gives the proper proof which helps in verifying the costs

attached to it.

Interest expense

6. Interest expense is one of the unique expense who involve such inherent risks while

taking up the auditing.

Rationale for selection

Interest expense involve few risks which are quite unique in nature. The inherent and control

risk associated with such expense relates to the material misstatement as there are few

expense who are less riskier than others it shows a complexity while auditing the interest

expense. In the comparative balance it can be seen that it shows a percentage decrease.

Assertions and explanations

The identification of some specific but known misstatements are being carried on and

concluded that if any such misstatement exists or not. Then if required the substantive

analytical procedures are followed which indicates the errors in the class of transactions and

balances of accounts. The expenses are compared their intensity of risks associated are

compared and on the basis of the intensity the auditor verify the expenses.

Recommended audit procedure

The recommended audit procedure for the audit of interest expense account is a detailed

observation into the account details to check the level of intensity an expense is having as it

shows the cash outflow so it is important to not to ignore the fact.

Audit planning 8

Superannuation

7. Superannuation are the direct investments to gain a control of the portfolio. It is a cash

outflow which needs to be shown in the balance sheet accurately to maintain fair records

of the company.

Rationale for selection

Investment are considered to be one of the most malicious audit risk component. The

inherent risk involve in investment cannot be easily avoided while carrying audit. The cash

outflow directly affects balance sheet so to maintain a fair picture of financial records it

needs a special attention (Barndt et al., 2016).

Assertions and explanations

A proper audit training is provided and create controls in the process of audit. The control risks

are realized when a financial misstatement occurs in it. It requires a proper accounting control to

save it from errors and frauds.

Recommended audit procedure

As explained above cash carries higher degree of risk involve in it so the audit procedure for the

same is proper training in audit and forming and engagement strategy to keep a regular check on

self-investments or superannuation.

Superannuation

7. Superannuation are the direct investments to gain a control of the portfolio. It is a cash

outflow which needs to be shown in the balance sheet accurately to maintain fair records

of the company.

Rationale for selection

Investment are considered to be one of the most malicious audit risk component. The

inherent risk involve in investment cannot be easily avoided while carrying audit. The cash

outflow directly affects balance sheet so to maintain a fair picture of financial records it

needs a special attention (Barndt et al., 2016).

Assertions and explanations

A proper audit training is provided and create controls in the process of audit. The control risks

are realized when a financial misstatement occurs in it. It requires a proper accounting control to

save it from errors and frauds.

Recommended audit procedure

As explained above cash carries higher degree of risk involve in it so the audit procedure for the

same is proper training in audit and forming and engagement strategy to keep a regular check on

self-investments or superannuation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

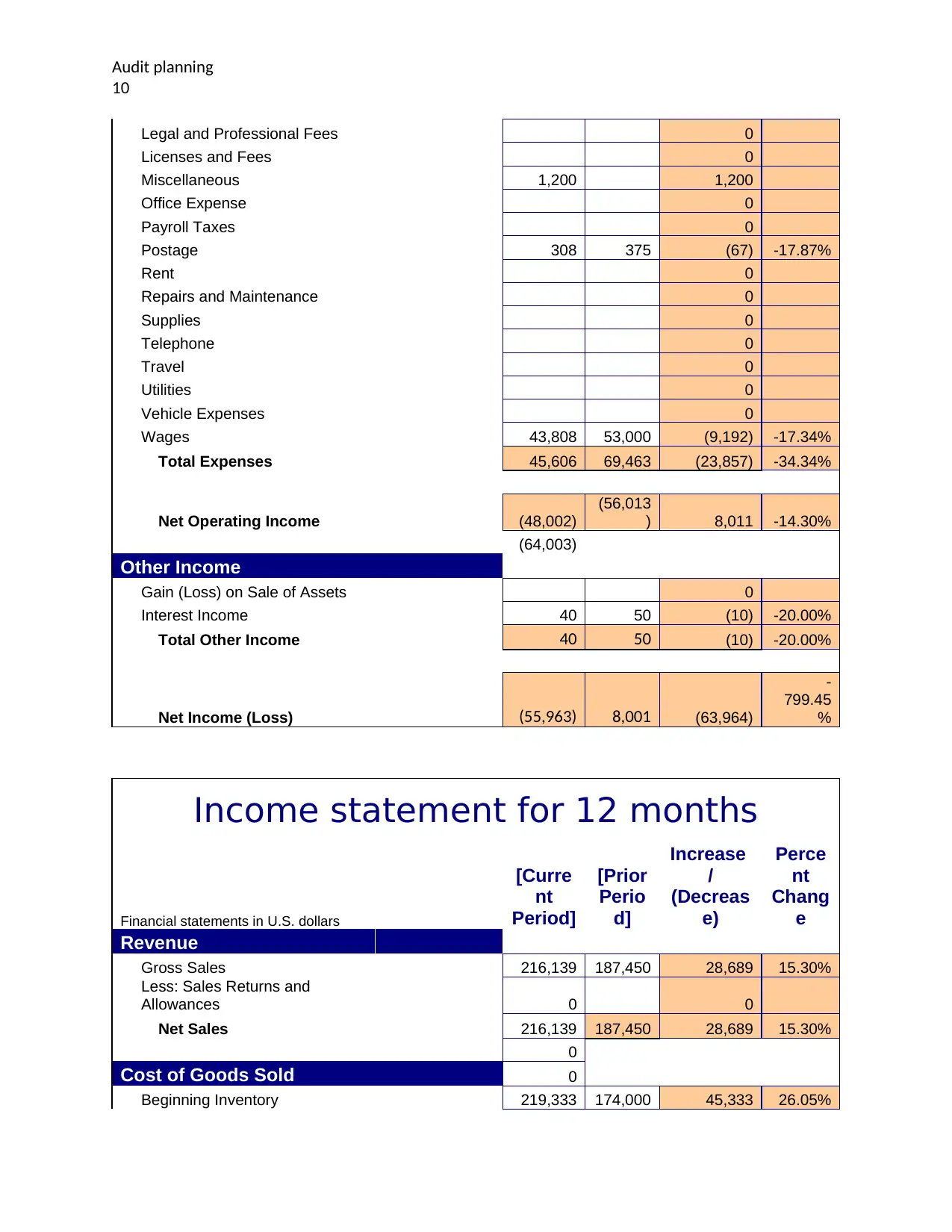

Audit planning 9

Comparative income statement

Income statement for 9 months

[Curre

nt

Period]

[Prior

Perio

d]

Increase

/

(Decreas

e)

Perce

nt

Chang

e

Revenue

Gross Sales 162,104 187,450 (25,346) -13.52%

Less: Sales Returns and

Allowances 0

Net Sales 162,104 187,450 (25,346) -13.52%

Cost of Goods Sold

Beginning Inventory 164,500 174,000 (9,500) -5.46%

Add: Purchases 0

Freight-in 0

Direct Labor 0

Indirect

Expenses 0

Inventory Available 164,500 174,000 (9,500) -5.46%

Less: Ending Inventory 0

Cost of Goods Sold 164,500 174,000 (9,500) -5.46%

Gross Profit (Loss) (2,396) 13,450 (15,846)

-

117.81

%

Expenses

Advertising 0

Amortization 0

Bad Debts 0

Bank Charges 290 350 (60) -17.14%

Charitable Contributions 0

Commissions 0

Contract Labor 0

Depreciation 15,738 (15,738)

-

100.00

%

Dues and Subscriptions 0

Employee Benefit Programs 0

Insurance 0

Interest 0

Comparative income statement

Income statement for 9 months

[Curre

nt

Period]

[Prior

Perio

d]

Increase

/

(Decreas

e)

Perce

nt

Chang

e

Revenue

Gross Sales 162,104 187,450 (25,346) -13.52%

Less: Sales Returns and

Allowances 0

Net Sales 162,104 187,450 (25,346) -13.52%

Cost of Goods Sold

Beginning Inventory 164,500 174,000 (9,500) -5.46%

Add: Purchases 0

Freight-in 0

Direct Labor 0

Indirect

Expenses 0

Inventory Available 164,500 174,000 (9,500) -5.46%

Less: Ending Inventory 0

Cost of Goods Sold 164,500 174,000 (9,500) -5.46%

Gross Profit (Loss) (2,396) 13,450 (15,846)

-

117.81

%

Expenses

Advertising 0

Amortization 0

Bad Debts 0

Bank Charges 290 350 (60) -17.14%

Charitable Contributions 0

Commissions 0

Contract Labor 0

Depreciation 15,738 (15,738)

-

100.00

%

Dues and Subscriptions 0

Employee Benefit Programs 0

Insurance 0

Interest 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit planning

10

Legal and Professional Fees 0

Licenses and Fees 0

Miscellaneous 1,200 1,200

Office Expense 0

Payroll Taxes 0

Postage 308 375 (67) -17.87%

Rent 0

Repairs and Maintenance 0

Supplies 0

Telephone 0

Travel 0

Utilities 0

Vehicle Expenses 0

Wages 43,808 53,000 (9,192) -17.34%

Total Expenses 45,606 69,463 (23,857) -34.34%

Net Operating Income (48,002)

(56,013

) 8,011 -14.30%

(64,003)

Other Income

Gain (Loss) on Sale of Assets 0

Interest Income 40 50 (10) -20.00%

Total Other Income 40 50 (10) -20.00%

Net Income (Loss) (55,963) 8,001 (63,964)

-

799.45

%

Income statement for 12 months

Financial statements in U.S. dollars

[Curre

nt

Period]

[Prior

Perio

d]

Increase

/

(Decreas

e)

Perce

nt

Chang

e

Revenue

Gross Sales 216,139 187,450 28,689 15.30%

Less: Sales Returns and

Allowances 0 0

Net Sales 216,139 187,450 28,689 15.30%

0

Cost of Goods Sold 0

Beginning Inventory 219,333 174,000 45,333 26.05%

10

Legal and Professional Fees 0

Licenses and Fees 0

Miscellaneous 1,200 1,200

Office Expense 0

Payroll Taxes 0

Postage 308 375 (67) -17.87%

Rent 0

Repairs and Maintenance 0

Supplies 0

Telephone 0

Travel 0

Utilities 0

Vehicle Expenses 0

Wages 43,808 53,000 (9,192) -17.34%

Total Expenses 45,606 69,463 (23,857) -34.34%

Net Operating Income (48,002)

(56,013

) 8,011 -14.30%

(64,003)

Other Income

Gain (Loss) on Sale of Assets 0

Interest Income 40 50 (10) -20.00%

Total Other Income 40 50 (10) -20.00%

Net Income (Loss) (55,963) 8,001 (63,964)

-

799.45

%

Income statement for 12 months

Financial statements in U.S. dollars

[Curre

nt

Period]

[Prior

Perio

d]

Increase

/

(Decreas

e)

Perce

nt

Chang

e

Revenue

Gross Sales 216,139 187,450 28,689 15.30%

Less: Sales Returns and

Allowances 0 0

Net Sales 216,139 187,450 28,689 15.30%

0

Cost of Goods Sold 0

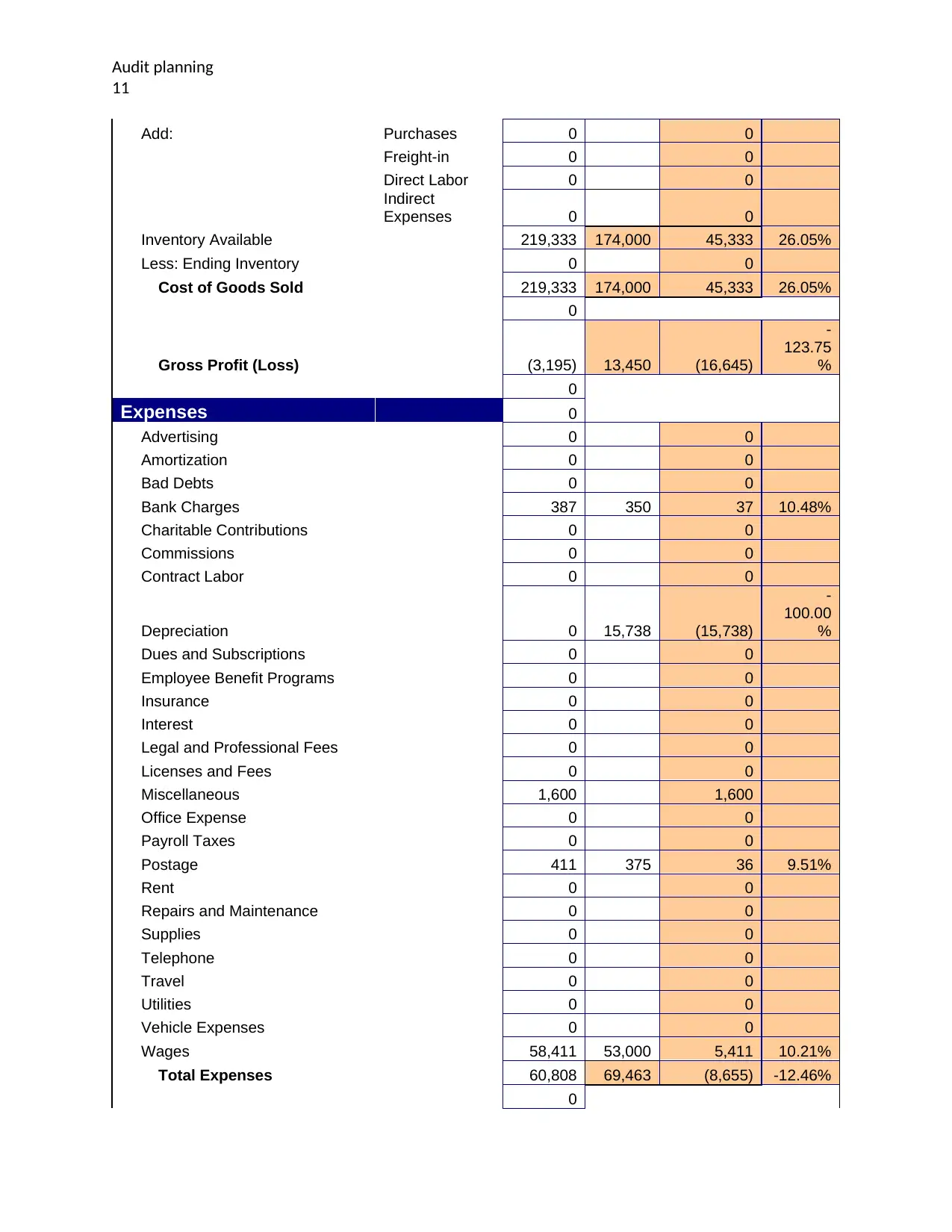

Beginning Inventory 219,333 174,000 45,333 26.05%

Audit planning

11

Add: Purchases 0 0

Freight-in 0 0

Direct Labor 0 0

Indirect

Expenses 0 0

Inventory Available 219,333 174,000 45,333 26.05%

Less: Ending Inventory 0 0

Cost of Goods Sold 219,333 174,000 45,333 26.05%

0

Gross Profit (Loss) (3,195) 13,450 (16,645)

-

123.75

%

0

Expenses 0

Advertising 0 0

Amortization 0 0

Bad Debts 0 0

Bank Charges 387 350 37 10.48%

Charitable Contributions 0 0

Commissions 0 0

Contract Labor 0 0

Depreciation 0 15,738 (15,738)

-

100.00

%

Dues and Subscriptions 0 0

Employee Benefit Programs 0 0

Insurance 0 0

Interest 0 0

Legal and Professional Fees 0 0

Licenses and Fees 0 0

Miscellaneous 1,600 1,600

Office Expense 0 0

Payroll Taxes 0 0

Postage 411 375 36 9.51%

Rent 0 0

Repairs and Maintenance 0 0

Supplies 0 0

Telephone 0 0

Travel 0 0

Utilities 0 0

Vehicle Expenses 0 0

Wages 58,411 53,000 5,411 10.21%

Total Expenses 60,808 69,463 (8,655) -12.46%

0

11

Add: Purchases 0 0

Freight-in 0 0

Direct Labor 0 0

Indirect

Expenses 0 0

Inventory Available 219,333 174,000 45,333 26.05%

Less: Ending Inventory 0 0

Cost of Goods Sold 219,333 174,000 45,333 26.05%

0

Gross Profit (Loss) (3,195) 13,450 (16,645)

-

123.75

%

0

Expenses 0

Advertising 0 0

Amortization 0 0

Bad Debts 0 0

Bank Charges 387 350 37 10.48%

Charitable Contributions 0 0

Commissions 0 0

Contract Labor 0 0

Depreciation 0 15,738 (15,738)

-

100.00

%

Dues and Subscriptions 0 0

Employee Benefit Programs 0 0

Insurance 0 0

Interest 0 0

Legal and Professional Fees 0 0

Licenses and Fees 0 0

Miscellaneous 1,600 1,600

Office Expense 0 0

Payroll Taxes 0 0

Postage 411 375 36 9.51%

Rent 0 0

Repairs and Maintenance 0 0

Supplies 0 0

Telephone 0 0

Travel 0 0

Utilities 0 0

Vehicle Expenses 0 0

Wages 58,411 53,000 5,411 10.21%

Total Expenses 60,808 69,463 (8,655) -12.46%

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.