Planning of Audit and Risk Analysis: Mayne Pharma Limited Report

VerifiedAdded on 2019/10/31

|14

|3595

|108

Report

AI Summary

This report provides a comprehensive analysis of audit planning and risk assessment for Mayne Pharma Limited. It begins with an executive summary, followed by an introduction outlining the objectives and scope of the report. The report delves into understanding Mayne Pharma's business operations, including its role in the pharmaceutical industry and the relevant regulations. It then analyzes the company's financial statements, including the balance sheet, profit and loss account, and cash flow statement, highlighting key changes and trends. The report identifies potential risks associated with the business and examines the going concern assumption and the company's approach to social responsibility. The analysis covers various aspects, such as trade receivables, current assets, payables, and loan interest, as well as revenue, expenses, and cash flow activities. The report concludes with a summary of the key findings and insights gained from the audit planning and risk analysis.

PLANNING OF AUDIT AND RISK ANALYSIS – MAYNE PHARMA LIMITED

Student Name: Student ID:

9/17/2017

Student Name: Student ID:

9/17/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The title of the report is planning of audit and the analysis of the risk. As the title suggests the

report has been flowed on the planning of the audit and what matters the auditor shall consider

while planning the audit. The first objective of the report is to plan the audit so that the audit

team can perform the audit function very effectively. The second objective of the report is to

analyze the annual report of the company very effectively and to analyze each and every item of

the financial statements critically so as to cover each and everything in the audit plan. With these

two major aims the study has been performed with separate headings and sub headings wherever

necessary.

The title of the report is planning of audit and the analysis of the risk. As the title suggests the

report has been flowed on the planning of the audit and what matters the auditor shall consider

while planning the audit. The first objective of the report is to plan the audit so that the audit

team can perform the audit function very effectively. The second objective of the report is to

analyze the annual report of the company very effectively and to analyze each and every item of

the financial statements critically so as to cover each and everything in the audit plan. With these

two major aims the study has been performed with separate headings and sub headings wherever

necessary.

Contents

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................4

UNDERSTANDING OF CLIENT’S BUISNESS....................................................................................................4

BUSINESS OPERATIONS...........................................................................................................................5

INDUSTRY IN WHICH IT OPERATES..........................................................................................................5

REGULATIONS FOR PHARMACEUTICAL GOODS...........................................................................................6

FINANCIAL STATEMENTS ANALYSIS.............................................................................................................7

BALANCE SHEET.......................................................................................................................................7

PROFIT AND LOSS....................................................................................................................................8

CASH FLOWS............................................................................................................................................9

IDENTIFICATION OF RISKS..........................................................................................................................10

GOING CONCERN ASSUMPTION................................................................................................................11

SOCIAL RESPONSIBILITY AND REPORTING.................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

EXECUTIVE SUMMARY.................................................................................................................................2

INTRODUCTION...........................................................................................................................................4

UNDERSTANDING OF CLIENT’S BUISNESS....................................................................................................4

BUSINESS OPERATIONS...........................................................................................................................5

INDUSTRY IN WHICH IT OPERATES..........................................................................................................5

REGULATIONS FOR PHARMACEUTICAL GOODS...........................................................................................6

FINANCIAL STATEMENTS ANALYSIS.............................................................................................................7

BALANCE SHEET.......................................................................................................................................7

PROFIT AND LOSS....................................................................................................................................8

CASH FLOWS............................................................................................................................................9

IDENTIFICATION OF RISKS..........................................................................................................................10

GOING CONCERN ASSUMPTION................................................................................................................11

SOCIAL RESPONSIBILITY AND REPORTING.................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is the activity which records the transaction of businesses on daily basis and results

are reported to the management of the company at the regular intervals. Auditing is an activity

through which the books of accounts are checked and verified by the independent third parties

appointed by the company and is known by the name of auditors of the company. Auditors are

required to plan their audit first depending upon the nature of the business of the company and

the size of the company. For the purpose of this report, Company – Mayne Pharma Limited has

been selected for the study. In this report, at first the understanding of the business of the client

has been discussed and how they are performing their functions. In the second section,

regulations and the rules that the pharmaceutical companies are required to comply with have

been detailed. In the third section, annual report of the company for the financial year ending two

thousand sixteen has been discussed in relation to the changes made in each item of the balance

sheet and profit and loss account. After that the risk associated with the business identified and

the going concern assumptions are verified. At the last the reference has been made to the

concept of social responsibility as to how the company has been performing the same. With this

the study has ended up with the conclusions.

UNDERSTANDING OF CLIENT’S BUISNESS

The beginning of every audit starts with the understanding of the business of the company as to

how the company’s main business activities and how does it functions. As per the recent

introduction of the auditing standard number 315 which states through the paragraph number

eleven that the auditor shall have the understanding of the nature of business of the prospective

client before proceeding to the conduct of an audit. In the given case following are the

Accounting is the activity which records the transaction of businesses on daily basis and results

are reported to the management of the company at the regular intervals. Auditing is an activity

through which the books of accounts are checked and verified by the independent third parties

appointed by the company and is known by the name of auditors of the company. Auditors are

required to plan their audit first depending upon the nature of the business of the company and

the size of the company. For the purpose of this report, Company – Mayne Pharma Limited has

been selected for the study. In this report, at first the understanding of the business of the client

has been discussed and how they are performing their functions. In the second section,

regulations and the rules that the pharmaceutical companies are required to comply with have

been detailed. In the third section, annual report of the company for the financial year ending two

thousand sixteen has been discussed in relation to the changes made in each item of the balance

sheet and profit and loss account. After that the risk associated with the business identified and

the going concern assumptions are verified. At the last the reference has been made to the

concept of social responsibility as to how the company has been performing the same. With this

the study has ended up with the conclusions.

UNDERSTANDING OF CLIENT’S BUISNESS

The beginning of every audit starts with the understanding of the business of the company as to

how the company’s main business activities and how does it functions. As per the recent

introduction of the auditing standard number 315 which states through the paragraph number

eleven that the auditor shall have the understanding of the nature of business of the prospective

client before proceeding to the conduct of an audit. In the given case following are the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

understandings that has been obtained from the Mayne Pharma group limited annual report

(AASB, 2006).

BUSINESS OPERATIONS

The company is the public limited company and listed in the Australian Stock Exchange. The

main focus on the company’s business is for supplying or transporting the medicines or the drugs

at the place where it is required. In other words, the main business of the company is to deliver

the medicines from the place of the manufacture to the place where it will be consumed. The

company delivers not only the branded medicines but also the non - branded or the generic

medicines across the globe. The second major business activity is to provide the development of

contract thereby manufacturing the drugs or the medicines for others. The company has the

distributors across different parts of the World including Asia, Europe, North America and

Australia. Therefore, the company is into the process of developing, manufacturing, marketing

and distributing the products in United States of America. In case of the specialty brands, the

company is engaged into the business of the marketing and distributing only of the products in

the United States of America. The company has the record of the last thirty years for the

development of the innovative ideas and new technologies which had helped the patients to have

the affordable medicines and also have developed the new oral drug delivery system. Thus, the

company is engaged in developing, manufacturing, marketing and distribution of the medicines

across the World (Singh, 2017’ Ullah, 2014).

INDUSTRY IN WHICH IT OPERATES

The company is operating in the pharmaceutical sector. In this sector, all the companies which

manufacture the drugs, medicines and thereby marketing and selling will be covered. Whenever

any comparison is made, then for the purpose of the benchmarking the strong performer will be

selected from the same industry and then comparison is made. The need for determining the

industry is correct in the sense that the industry data will provide whether the functions as \

performed by the particular company is as per the industry current market conditions and the

norms. In this way industry defining is very essential and the company is engaged in the

pharmaceuticals sector.

(AASB, 2006).

BUSINESS OPERATIONS

The company is the public limited company and listed in the Australian Stock Exchange. The

main focus on the company’s business is for supplying or transporting the medicines or the drugs

at the place where it is required. In other words, the main business of the company is to deliver

the medicines from the place of the manufacture to the place where it will be consumed. The

company delivers not only the branded medicines but also the non - branded or the generic

medicines across the globe. The second major business activity is to provide the development of

contract thereby manufacturing the drugs or the medicines for others. The company has the

distributors across different parts of the World including Asia, Europe, North America and

Australia. Therefore, the company is into the process of developing, manufacturing, marketing

and distributing the products in United States of America. In case of the specialty brands, the

company is engaged into the business of the marketing and distributing only of the products in

the United States of America. The company has the record of the last thirty years for the

development of the innovative ideas and new technologies which had helped the patients to have

the affordable medicines and also have developed the new oral drug delivery system. Thus, the

company is engaged in developing, manufacturing, marketing and distribution of the medicines

across the World (Singh, 2017’ Ullah, 2014).

INDUSTRY IN WHICH IT OPERATES

The company is operating in the pharmaceutical sector. In this sector, all the companies which

manufacture the drugs, medicines and thereby marketing and selling will be covered. Whenever

any comparison is made, then for the purpose of the benchmarking the strong performer will be

selected from the same industry and then comparison is made. The need for determining the

industry is correct in the sense that the industry data will provide whether the functions as \

performed by the particular company is as per the industry current market conditions and the

norms. In this way industry defining is very essential and the company is engaged in the

pharmaceuticals sector.

REGULATIONS FOR PHARMACEUTICAL GOODS

The pharmaceutical companies are managed by the department of health, Therapeutic Goods

Administration of Australia. From time to time they are bringing the arrangements as to how the

pharmaceutical goods are required to be controlled and managed. Following are the regulations

as prescribed by the Australian Government for pharmaceutical goods:

- Labeling and Packing - The Therapeutic Goods Administration of Australia has defined

the labeling and packaging guidelines as to how the pharmaceuticals shall be labeled and

packed. The department has issued two orders for labeling and packing which is required

to be fulfilled by the companies. One is for the prescription medicines issued under order

number 91 and the other is for the non prescription medicines issued under order number

90. Some of the common rules and regulations includes like the labels should be clearly

pasted in order to enhance the safety of the consumers, providing the dial dispense

packing wherever required so as to enable the customer to identify the number of the

dosages available in the pack, etc.

- Efficacy – It means that the medicine of the drug that will be given to the patients will be

effective for them rather than being an ineffective medicine. The companies have to

mention while licensing the new product as to how the medicine will be effective and up

to what percentage the same will be effective. It is because as per the common parlance

no medicine will provide hundred percent results but the medicine should be like that

which will in definite terms meets the criteria of the disease.

- Safety Norms – The companies are required to satisfy the safety norms as defined by the

Therapeutic Goods Administration of Australia. It states that the company shall produce

the medicine which will be effective and that will not in any case carries the side effects

or any other type of risks which can be harmful to the patients. The safety norms are

tested clinically and then only approval for listing of the medicine for further

manufacture and sale will be made available (DOI Australia, 2016; TGA, 2017).

- Advertising and Business Promotion – The companies though in other countries are

allowed to do the advertising and marketing of their medicines to health professionals

and to the patients but in actual the Therapeutic Goods Administration of Australia has

specified that the company shall not be allowed to do the advertising in the following

cases:

The pharmaceutical companies are managed by the department of health, Therapeutic Goods

Administration of Australia. From time to time they are bringing the arrangements as to how the

pharmaceutical goods are required to be controlled and managed. Following are the regulations

as prescribed by the Australian Government for pharmaceutical goods:

- Labeling and Packing - The Therapeutic Goods Administration of Australia has defined

the labeling and packaging guidelines as to how the pharmaceuticals shall be labeled and

packed. The department has issued two orders for labeling and packing which is required

to be fulfilled by the companies. One is for the prescription medicines issued under order

number 91 and the other is for the non prescription medicines issued under order number

90. Some of the common rules and regulations includes like the labels should be clearly

pasted in order to enhance the safety of the consumers, providing the dial dispense

packing wherever required so as to enable the customer to identify the number of the

dosages available in the pack, etc.

- Efficacy – It means that the medicine of the drug that will be given to the patients will be

effective for them rather than being an ineffective medicine. The companies have to

mention while licensing the new product as to how the medicine will be effective and up

to what percentage the same will be effective. It is because as per the common parlance

no medicine will provide hundred percent results but the medicine should be like that

which will in definite terms meets the criteria of the disease.

- Safety Norms – The companies are required to satisfy the safety norms as defined by the

Therapeutic Goods Administration of Australia. It states that the company shall produce

the medicine which will be effective and that will not in any case carries the side effects

or any other type of risks which can be harmful to the patients. The safety norms are

tested clinically and then only approval for listing of the medicine for further

manufacture and sale will be made available (DOI Australia, 2016; TGA, 2017).

- Advertising and Business Promotion – The companies though in other countries are

allowed to do the advertising and marketing of their medicines to health professionals

and to the patients but in actual the Therapeutic Goods Administration of Australia has

specified that the company shall not be allowed to do the advertising in the following

cases:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The advertisement so decided to be made is misleading

Will create negative impact in the future in case the medicine works

out as non effectives

The advertising is totally unreliable where the company is making

unnecessary claims like if by having this medicine the headache will

be gone definitely with hundred percent otherwise the whole amount

will be refunded.

Wrong advertising will always lead to the material risks to the life of the public and therefore the

company is required to follow all the rules and regulations as defined by the Therapeutic Goods

Administration of Australia.

FINANCIAL STATEMENTS ANALYSIS

The financial statement consists of the three statements. One is the statement of the balance sheet

which helps in determining the financial position of the company as on that date. Second is the

statement of the Profit and Loss which provides the financial performance that the company has

gained over the years and lastly is the statement of cash flows which provides the detail of the

cash inflows and cash outflows that the company has made during the year and helps in

determining as to how much has been cash and cash equivalents increased or decreased during

the year. In the following table, the changes in the major items of the financial statements of the

company for the last two years have been mentioned.

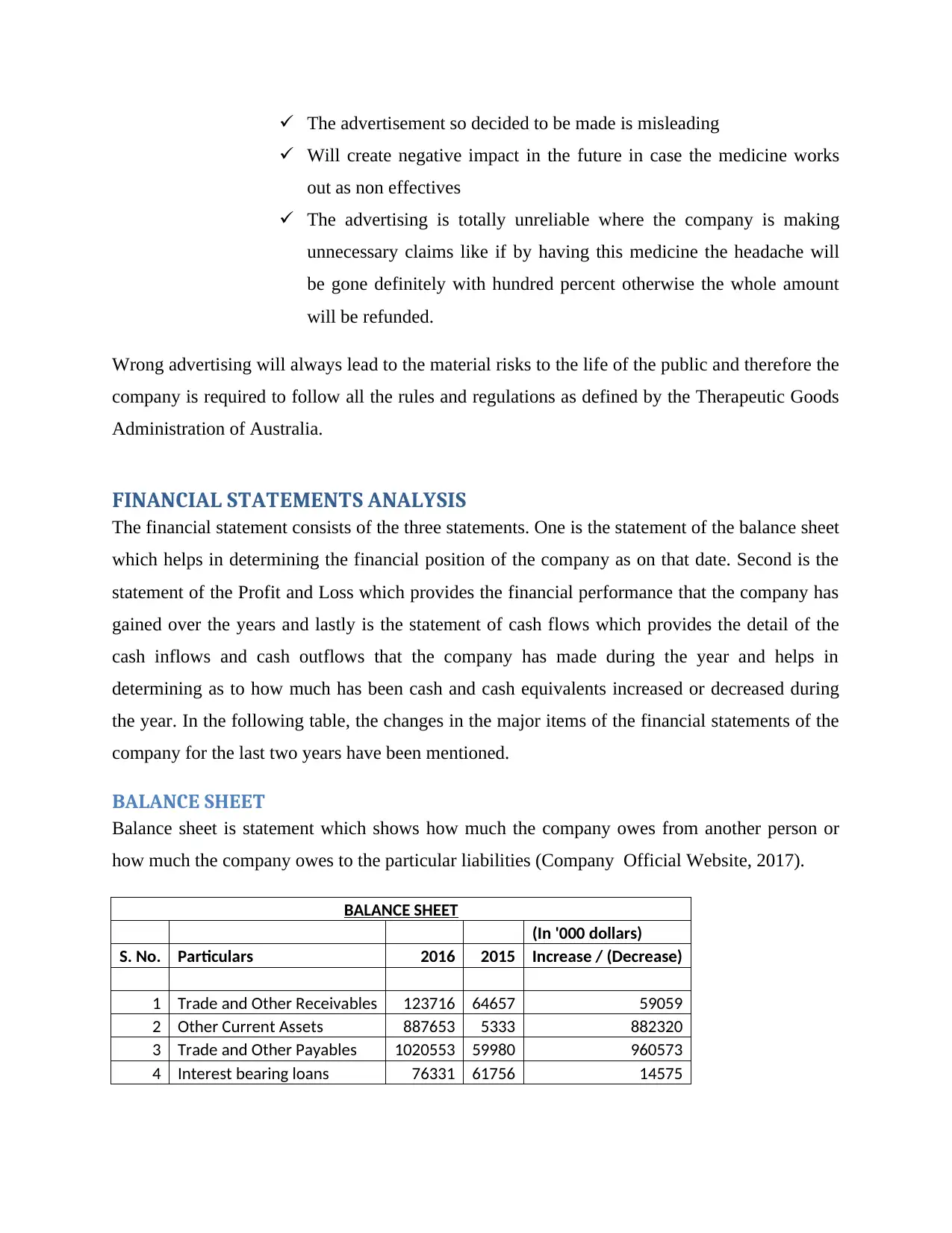

BALANCE SHEET

Balance sheet is statement which shows how much the company owes from another person or

how much the company owes to the particular liabilities (Company Official Website, 2017).

BALANCE SHEET

(In '000 dollars)

S. No. Particulars 2016 2015 Increase / (Decrease)

1 Trade and Other Receivables 123716 64657 59059

2 Other Current Assets 887653 5333 882320

3 Trade and Other Payables 1020553 59980 960573

4 Interest bearing loans 76331 61756 14575

Will create negative impact in the future in case the medicine works

out as non effectives

The advertising is totally unreliable where the company is making

unnecessary claims like if by having this medicine the headache will

be gone definitely with hundred percent otherwise the whole amount

will be refunded.

Wrong advertising will always lead to the material risks to the life of the public and therefore the

company is required to follow all the rules and regulations as defined by the Therapeutic Goods

Administration of Australia.

FINANCIAL STATEMENTS ANALYSIS

The financial statement consists of the three statements. One is the statement of the balance sheet

which helps in determining the financial position of the company as on that date. Second is the

statement of the Profit and Loss which provides the financial performance that the company has

gained over the years and lastly is the statement of cash flows which provides the detail of the

cash inflows and cash outflows that the company has made during the year and helps in

determining as to how much has been cash and cash equivalents increased or decreased during

the year. In the following table, the changes in the major items of the financial statements of the

company for the last two years have been mentioned.

BALANCE SHEET

Balance sheet is statement which shows how much the company owes from another person or

how much the company owes to the particular liabilities (Company Official Website, 2017).

BALANCE SHEET

(In '000 dollars)

S. No. Particulars 2016 2015 Increase / (Decrease)

1 Trade and Other Receivables 123716 64657 59059

2 Other Current Assets 887653 5333 882320

3 Trade and Other Payables 1020553 59980 960573

4 Interest bearing loans 76331 61756 14575

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above table, the following has been inferred:

- Trade and other receivables have been considerably increased by $59059 thousands

which represent approximately 95 percent of the value of the trade and other receivable

for the year 2015.

- The other current assets have been increased by $882320 thousand which is basically

increased by the recognition of contracts rights that has been arisen in relation to the

transaction made with Teva Pharmaceuticals Limited.

- Reason for selecting the trade payables is that it has been considerably increased by

$960573 thousand.

- The interest bearing loan has been increased by $14575 thousand and it depicts that the

company has been using the banking facilities.

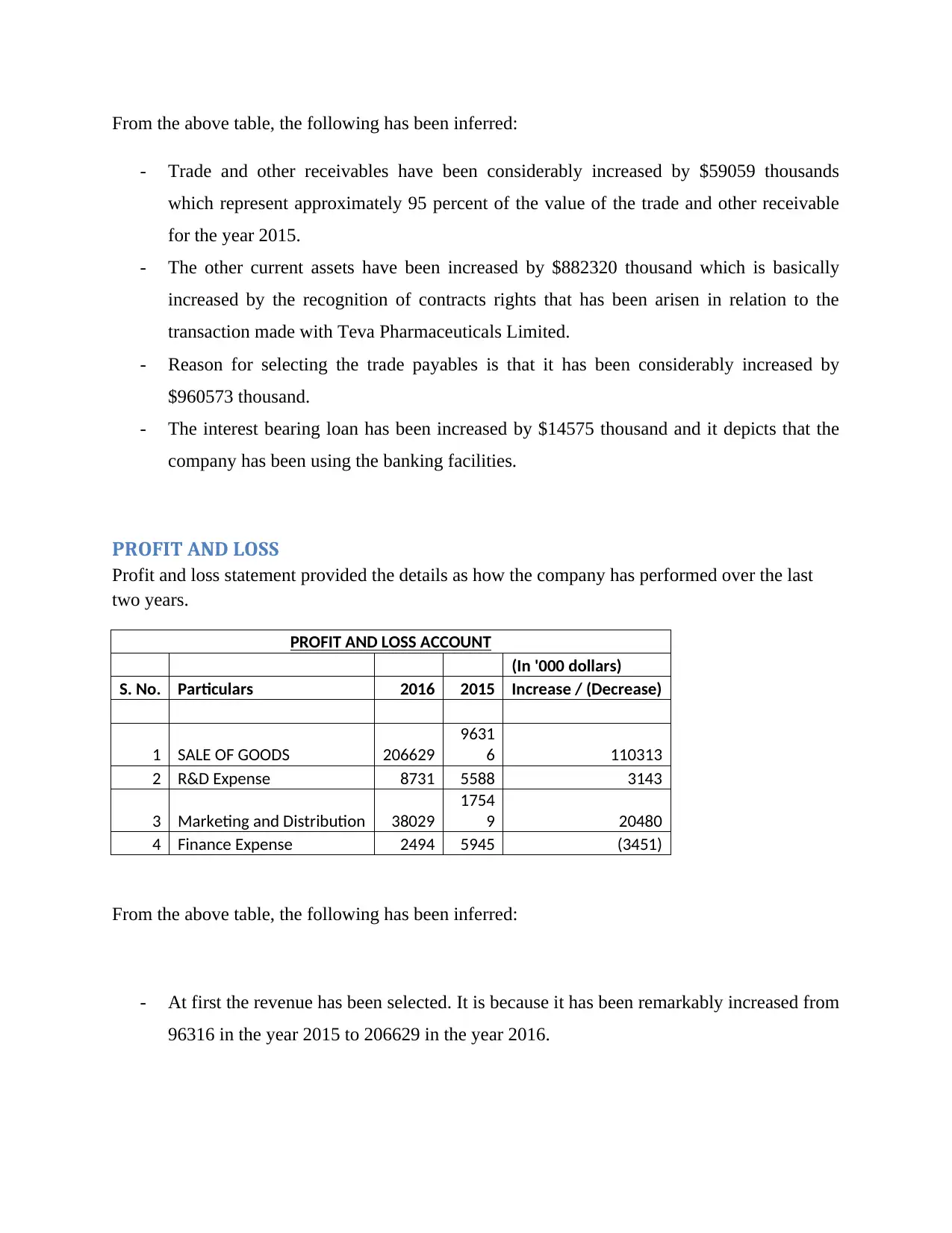

PROFIT AND LOSS

Profit and loss statement provided the details as how the company has performed over the last

two years.

PROFIT AND LOSS ACCOUNT

(In '000 dollars)

S. No. Particulars 2016 2015 Increase / (Decrease)

1 SALE OF GOODS 206629

9631

6 110313

2 R&D Expense 8731 5588 3143

3 Marketing and Distribution 38029

1754

9 20480

4 Finance Expense 2494 5945 (3451)

From the above table, the following has been inferred:

- At first the revenue has been selected. It is because it has been remarkably increased from

96316 in the year 2015 to 206629 in the year 2016.

- Trade and other receivables have been considerably increased by $59059 thousands

which represent approximately 95 percent of the value of the trade and other receivable

for the year 2015.

- The other current assets have been increased by $882320 thousand which is basically

increased by the recognition of contracts rights that has been arisen in relation to the

transaction made with Teva Pharmaceuticals Limited.

- Reason for selecting the trade payables is that it has been considerably increased by

$960573 thousand.

- The interest bearing loan has been increased by $14575 thousand and it depicts that the

company has been using the banking facilities.

PROFIT AND LOSS

Profit and loss statement provided the details as how the company has performed over the last

two years.

PROFIT AND LOSS ACCOUNT

(In '000 dollars)

S. No. Particulars 2016 2015 Increase / (Decrease)

1 SALE OF GOODS 206629

9631

6 110313

2 R&D Expense 8731 5588 3143

3 Marketing and Distribution 38029

1754

9 20480

4 Finance Expense 2494 5945 (3451)

From the above table, the following has been inferred:

- At first the revenue has been selected. It is because it has been remarkably increased from

96316 in the year 2015 to 206629 in the year 2016.

- The company has expended more in the research and development head which means

that the company might have undertaking the manufacturing or any other research

process.

- The marketing and the distribution expense have been incurred at the rate of more than

hundred percent increases as compared to the earlier year.

- The company has paid the finance expense with the high amount which shows that the

company’s liquidity position is strong.

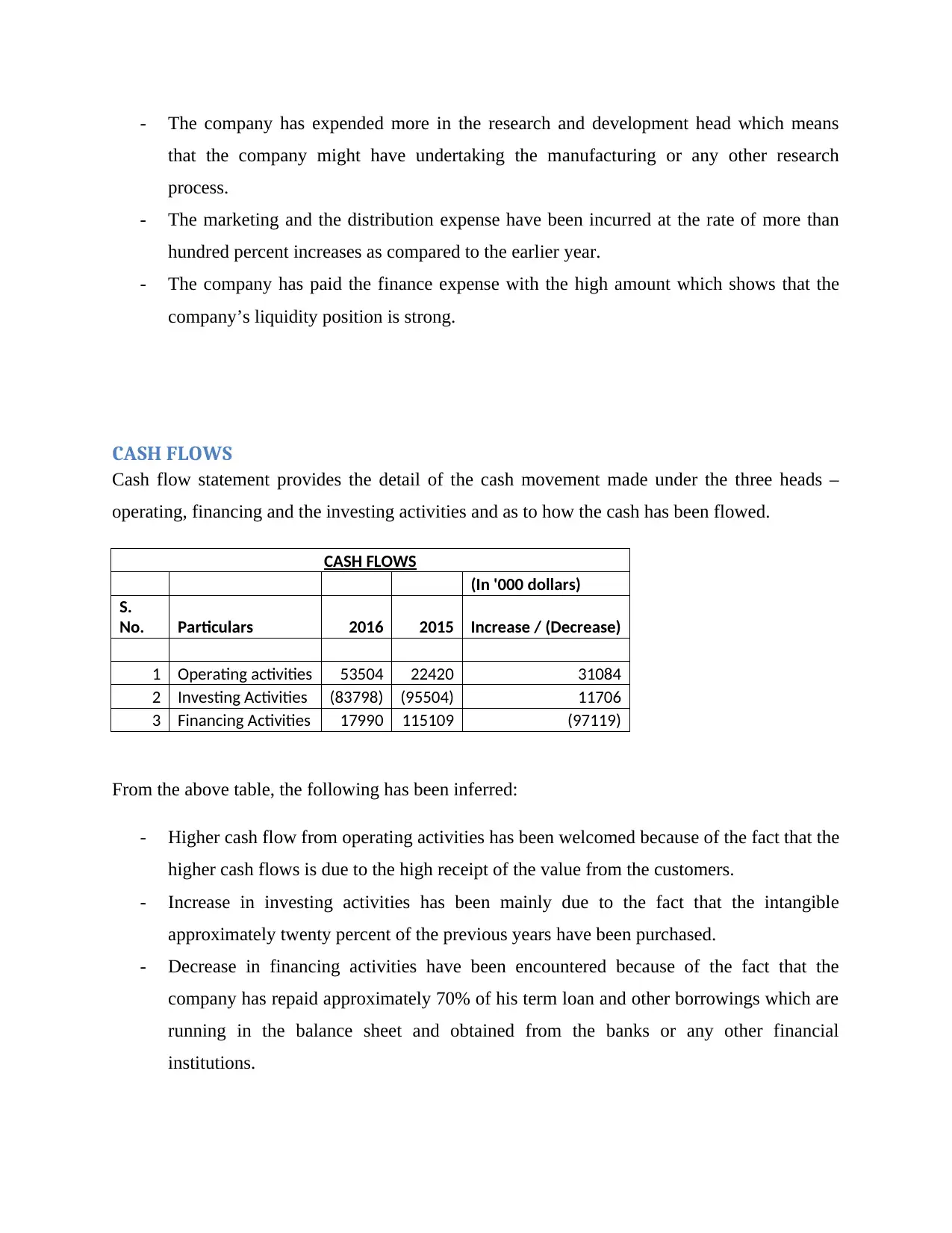

CASH FLOWS

Cash flow statement provides the detail of the cash movement made under the three heads –

operating, financing and the investing activities and as to how the cash has been flowed.

CASH FLOWS

(In '000 dollars)

S.

No. Particulars 2016 2015 Increase / (Decrease)

1 Operating activities 53504 22420 31084

2 Investing Activities (83798) (95504) 11706

3 Financing Activities 17990 115109 (97119)

From the above table, the following has been inferred:

- Higher cash flow from operating activities has been welcomed because of the fact that the

higher cash flows is due to the high receipt of the value from the customers.

- Increase in investing activities has been mainly due to the fact that the intangible

approximately twenty percent of the previous years have been purchased.

- Decrease in financing activities have been encountered because of the fact that the

company has repaid approximately 70% of his term loan and other borrowings which are

running in the balance sheet and obtained from the banks or any other financial

institutions.

that the company might have undertaking the manufacturing or any other research

process.

- The marketing and the distribution expense have been incurred at the rate of more than

hundred percent increases as compared to the earlier year.

- The company has paid the finance expense with the high amount which shows that the

company’s liquidity position is strong.

CASH FLOWS

Cash flow statement provides the detail of the cash movement made under the three heads –

operating, financing and the investing activities and as to how the cash has been flowed.

CASH FLOWS

(In '000 dollars)

S.

No. Particulars 2016 2015 Increase / (Decrease)

1 Operating activities 53504 22420 31084

2 Investing Activities (83798) (95504) 11706

3 Financing Activities 17990 115109 (97119)

From the above table, the following has been inferred:

- Higher cash flow from operating activities has been welcomed because of the fact that the

higher cash flows is due to the high receipt of the value from the customers.

- Increase in investing activities has been mainly due to the fact that the intangible

approximately twenty percent of the previous years have been purchased.

- Decrease in financing activities have been encountered because of the fact that the

company has repaid approximately 70% of his term loan and other borrowings which are

running in the balance sheet and obtained from the banks or any other financial

institutions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From the above analysis, it is very well established that both the financial years have drastic

change in the value of items reported in the balance sheet, profit and loss account and cash flows

of the company.

IDENTIFICATION OF RISKS

As pet the nature of the business of the company and the complexity of the case within which the

company is working, the following has been estimated as risks which are associated with the

revenue:

- Increase in the Revenue - One of the major risks that has been encountered by the

company is the increase in the value of revenue. It has created the shocking news for the

company in the market. On the one hand the company’s revenue has been increased

considerably over the last years and on the other hand the company has paid the

maximum of the amount of the loan outstanding in the books of accounts. If this is the

practice adopted by the company then there would have been the risk of utilizing the

short term funds against the payment of the long term funds. As per the generally

accepted accounting policies the company is not required to do so and in case it has been

done then it shall be mentioned in the auditor report. Thus, if the same practice is

followed then there will be the risk of liquidation in the future.

- Increase in the Expectation of the customer - In this current scenario, there is great

pressure from the customers regarding the new products that will be launch and when it

will get started to be available at the shops. The customers are ready to pay for their

better health but the company does not have sufficient knowledge and worth and thus will

bring down the reputation of the company.

- Poor Productivity –As per the industry norms, the level of output of the Pharma

companies is stable and stagnant. But the company have generated higher revenue which

details that the there might be some chances of the manipulative practices and has thus

increased the risk of having the material misstatements (AASB, 2013).

- Poor Management - In the current scenario, the nature of the work and the official climate

which the company has belongs to that of the traditional one which has increased the

change in the value of items reported in the balance sheet, profit and loss account and cash flows

of the company.

IDENTIFICATION OF RISKS

As pet the nature of the business of the company and the complexity of the case within which the

company is working, the following has been estimated as risks which are associated with the

revenue:

- Increase in the Revenue - One of the major risks that has been encountered by the

company is the increase in the value of revenue. It has created the shocking news for the

company in the market. On the one hand the company’s revenue has been increased

considerably over the last years and on the other hand the company has paid the

maximum of the amount of the loan outstanding in the books of accounts. If this is the

practice adopted by the company then there would have been the risk of utilizing the

short term funds against the payment of the long term funds. As per the generally

accepted accounting policies the company is not required to do so and in case it has been

done then it shall be mentioned in the auditor report. Thus, if the same practice is

followed then there will be the risk of liquidation in the future.

- Increase in the Expectation of the customer - In this current scenario, there is great

pressure from the customers regarding the new products that will be launch and when it

will get started to be available at the shops. The customers are ready to pay for their

better health but the company does not have sufficient knowledge and worth and thus will

bring down the reputation of the company.

- Poor Productivity –As per the industry norms, the level of output of the Pharma

companies is stable and stagnant. But the company have generated higher revenue which

details that the there might be some chances of the manipulative practices and has thus

increased the risk of having the material misstatements (AASB, 2013).

- Poor Management - In the current scenario, the nature of the work and the official climate

which the company has belongs to that of the traditional one which has increased the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

chances of having the violation of the accounting principle which in turn will be regarded

as the material misstatements (MSH, 2017).

Thus, in this manner the risks have been identified.

GOING CONCERN ASSUMPTION

No, there will not be the going concern issue.

As per the going concern assumption of the accounting principles, it has been mentioned that the

financial statements of the company shall be prepared and presented on the basis of the going

concern assumption. In other words it means the financial statements are prepared so as to give

impression that the company will exists and work for future years. There will not be any case

which leads to the closure of the operations of the company (Boyce, 2005).

In the given case, the company has recalled some of its major brand products and removed them

from sale. Although the company is having the major business of brand products but the

company will not be affected as the company’s main line of activity or the main line of business

would not stopped rater it will keep going. If the major brand products have been discontinued

then the company will still in the business of selling the products which are generic in nature and

are not branded. Thus, in this way the going concern assumption will not be affected.

SOCIAL RESPONSIBILITY AND REPORTING

Social responsibility plays the very important role in the success of ever organization whether it

is big or small, whether it is effective or non effective. Social responsibility is defined as the

responsibility of the company towards the society of the country within which the company is

operating. The corporations Act, 2001 along with the accounting standards, has prescribed that

the company is required to report the company’s policies and procedures in the report to ensure

that the company is not affecting the rights and the privileges of the society and also takes care of

the society. The report which is prepared is known as the corporate social responsibility (Shaw,

2008).

as the material misstatements (MSH, 2017).

Thus, in this manner the risks have been identified.

GOING CONCERN ASSUMPTION

No, there will not be the going concern issue.

As per the going concern assumption of the accounting principles, it has been mentioned that the

financial statements of the company shall be prepared and presented on the basis of the going

concern assumption. In other words it means the financial statements are prepared so as to give

impression that the company will exists and work for future years. There will not be any case

which leads to the closure of the operations of the company (Boyce, 2005).

In the given case, the company has recalled some of its major brand products and removed them

from sale. Although the company is having the major business of brand products but the

company will not be affected as the company’s main line of activity or the main line of business

would not stopped rater it will keep going. If the major brand products have been discontinued

then the company will still in the business of selling the products which are generic in nature and

are not branded. Thus, in this way the going concern assumption will not be affected.

SOCIAL RESPONSIBILITY AND REPORTING

Social responsibility plays the very important role in the success of ever organization whether it

is big or small, whether it is effective or non effective. Social responsibility is defined as the

responsibility of the company towards the society of the country within which the company is

operating. The corporations Act, 2001 along with the accounting standards, has prescribed that

the company is required to report the company’s policies and procedures in the report to ensure

that the company is not affecting the rights and the privileges of the society and also takes care of

the society. The report which is prepared is known as the corporate social responsibility (Shaw,

2008).

The company has issued the first sustainability reporting for the year ending 2016. Thus, in this

the first report will be analysed. The report has been prepared in accordance with the Global

Reporting Initiative standards. The report has contained the thirty eight clauses and each clause

has been detailed. The report has contained the bifurcation of the stakeholder detailing the

mechanism to be appointed for the engagement and the examples of the different key interest

that the stakeholders have in the business of the company. For instance customers are the main

stakeholders of the company. Their engagement with the business of the company has been

entered through the visits at the office or separate meetings. Their key interest in the working of

the company would be to have the good quality of product; the supply of the products shall be

timely delivered to the customers of the company and also the pricing strategy adopted by the

company. The bifurcation of other stakeholders has also been mentioned. In this manner the

social responsibility statement have been prepared.

As it is the first time of issuing the corporate social responsibility, the certificate of assurance

may be obtained from the external parties.

CONCLUSION

An auditing plays the significant role in the success of every company. The auditing helps in

verifying each and every function of the business of the company and reporting the discrepancies

if any to the management of the company. In the report the analysis have been made of the

financial statements of the company – Mayne Pharma Limited and how each item of the

financial statements of the company is important for the stakeholders of the company. Audit plan

has been detailed with the clear understanding of the business of the company and has been

ended up with the social responsibility of the company. Each item of the financial statements has

been detailed and the interpretation thereon has been made. In order to conclude, each and every

company shall represent the true and fair view of the state of affairs of the company and the

financial performance of the company and along with that the auditor shall report any material

misstatement to the management of the company and if requires shall be reported to stakeholders

as the key audit matters specified in New Auditing standard 701. .

the first report will be analysed. The report has been prepared in accordance with the Global

Reporting Initiative standards. The report has contained the thirty eight clauses and each clause

has been detailed. The report has contained the bifurcation of the stakeholder detailing the

mechanism to be appointed for the engagement and the examples of the different key interest

that the stakeholders have in the business of the company. For instance customers are the main

stakeholders of the company. Their engagement with the business of the company has been

entered through the visits at the office or separate meetings. Their key interest in the working of

the company would be to have the good quality of product; the supply of the products shall be

timely delivered to the customers of the company and also the pricing strategy adopted by the

company. The bifurcation of other stakeholders has also been mentioned. In this manner the

social responsibility statement have been prepared.

As it is the first time of issuing the corporate social responsibility, the certificate of assurance

may be obtained from the external parties.

CONCLUSION

An auditing plays the significant role in the success of every company. The auditing helps in

verifying each and every function of the business of the company and reporting the discrepancies

if any to the management of the company. In the report the analysis have been made of the

financial statements of the company – Mayne Pharma Limited and how each item of the

financial statements of the company is important for the stakeholders of the company. Audit plan

has been detailed with the clear understanding of the business of the company and has been

ended up with the social responsibility of the company. Each item of the financial statements has

been detailed and the interpretation thereon has been made. In order to conclude, each and every

company shall represent the true and fair view of the state of affairs of the company and the

financial performance of the company and along with that the auditor shall report any material

misstatement to the management of the company and if requires shall be reported to stakeholders

as the key audit matters specified in New Auditing standard 701. .

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.