Audit, Assurance, and Compliance: Financial Statement Analysis Report

VerifiedAdded on 2020/02/18

|6

|1244

|225

Report

AI Summary

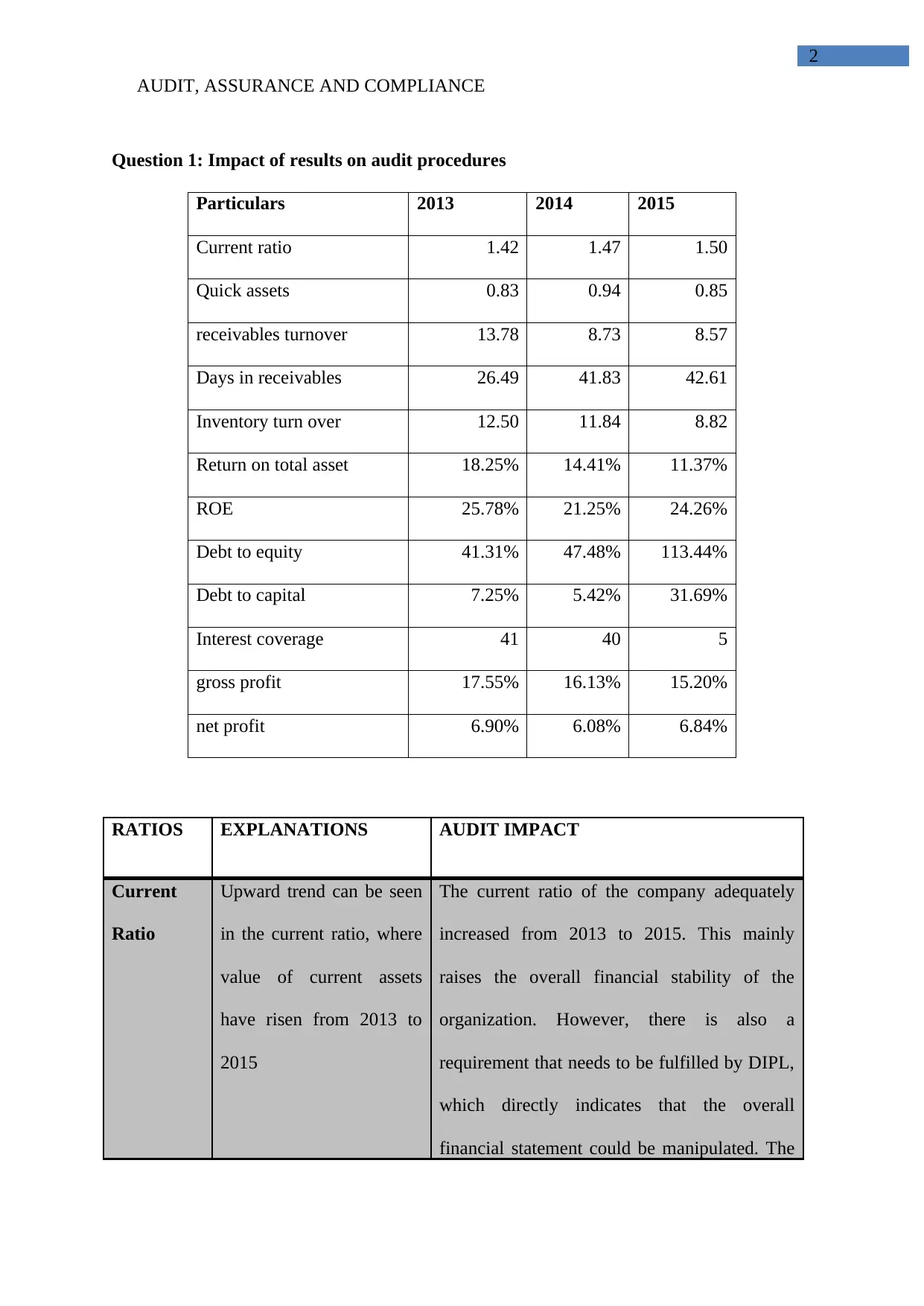

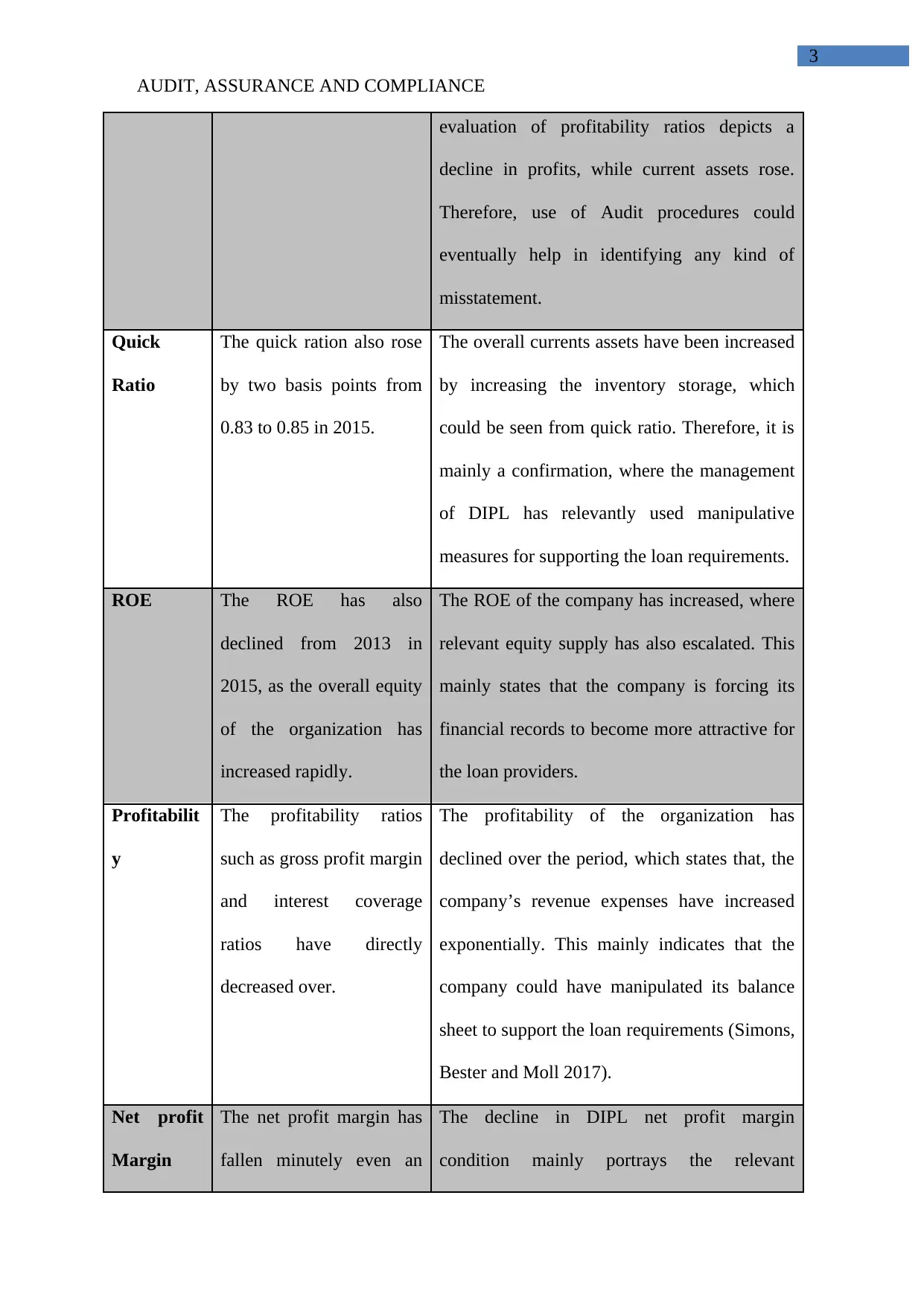

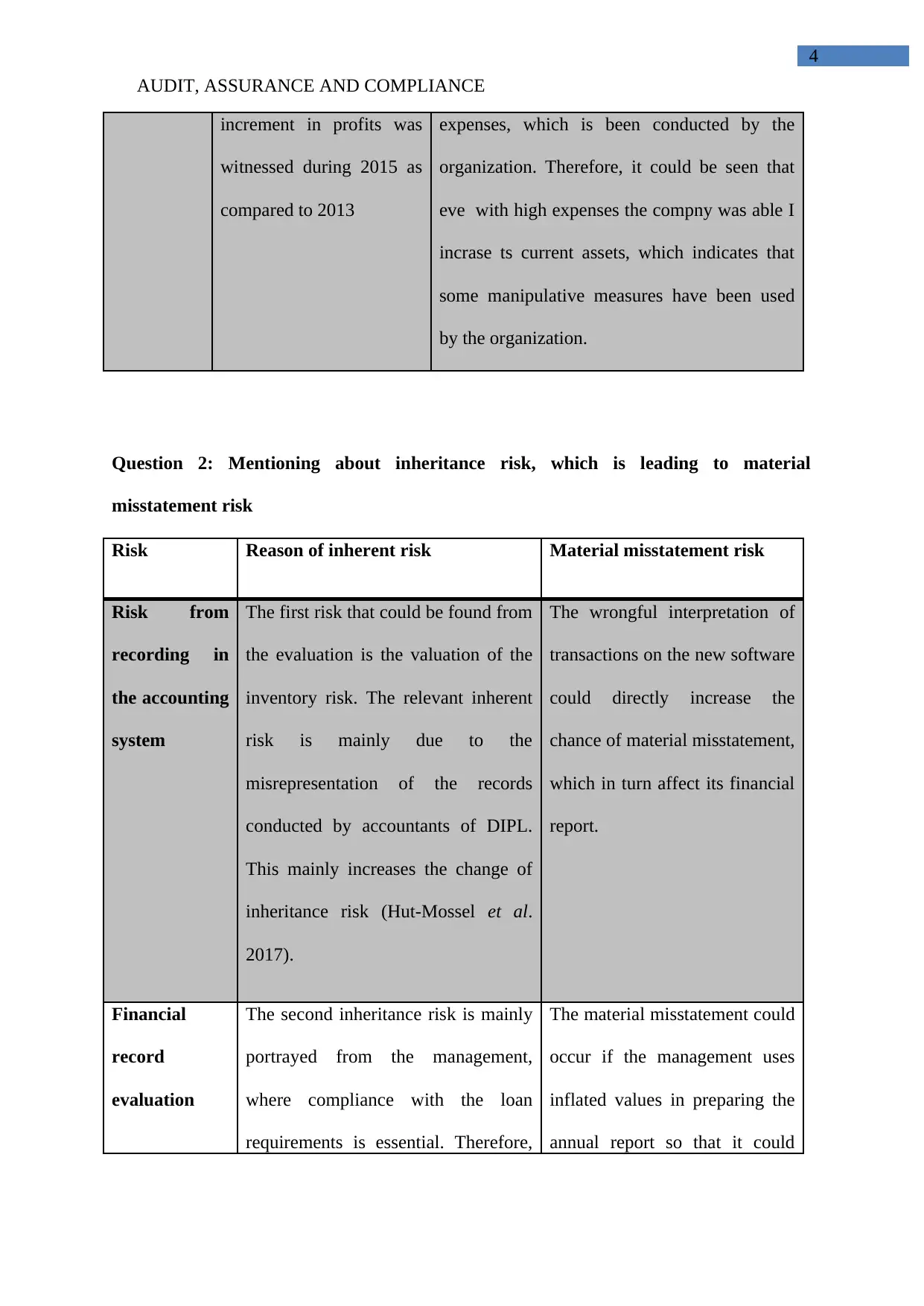

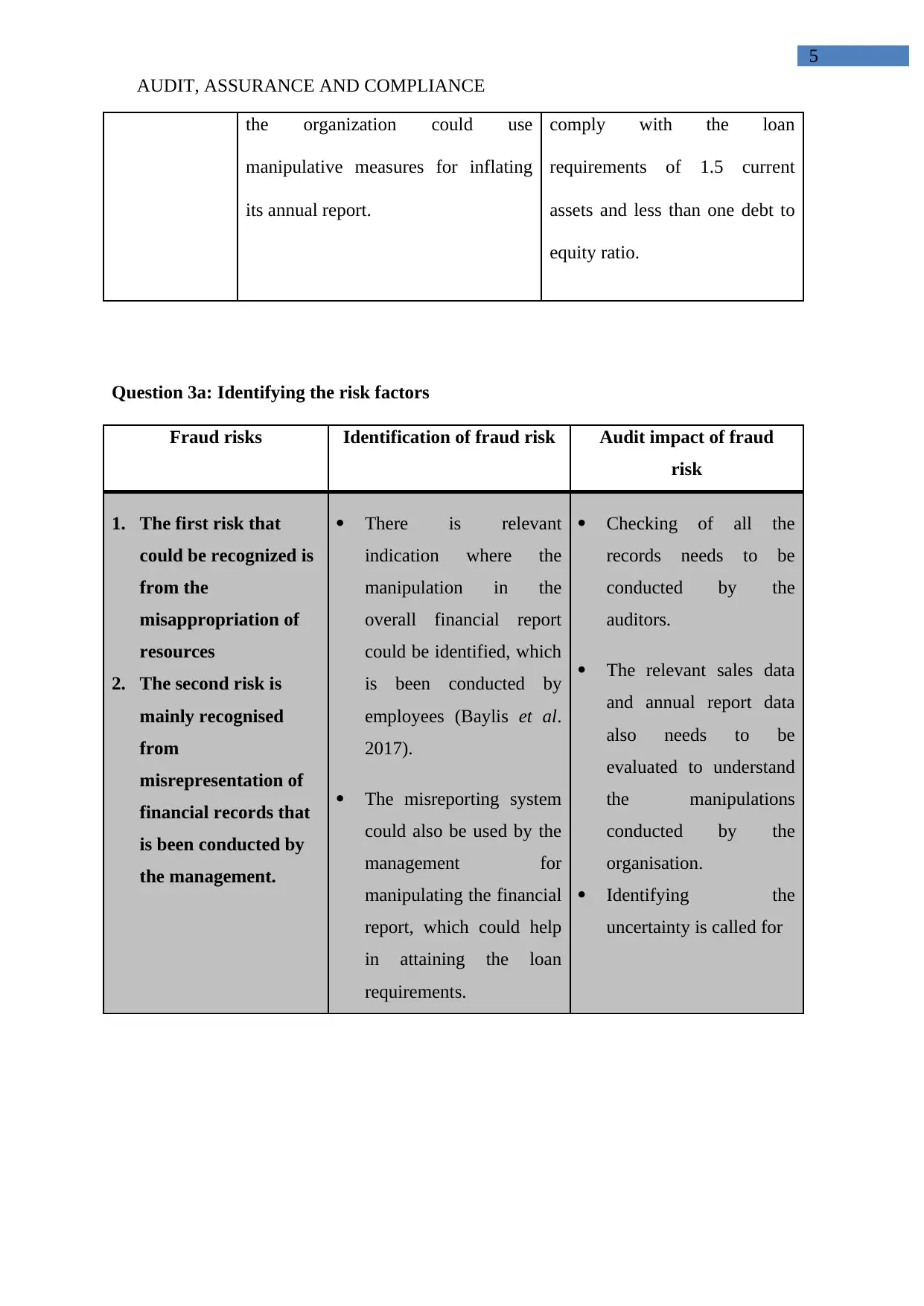

This report analyzes the financial performance of a company (DIPL) from 2013 to 2015, using various financial ratios such as current ratio, quick ratio, ROE, and profitability ratios. The analysis reveals trends and potential areas of concern, including declining profitability and increasing debt. The report identifies inherent risks, particularly the valuation of inventory and management's potential manipulation of financial records to meet loan requirements, which could lead to material misstatements. Furthermore, it highlights fraud risks related to misappropriation of resources and misrepresentation of financial data. The report emphasizes the importance of cynical audit procedures to identify and mitigate these risks, including careful examination of sales data and annual reports. The report concludes that the company's use of an average costing method may be manipulative, thus warranting thorough audit procedures to ensure accuracy and compliance.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.