Audit Program Development: Laserbond Ltd., Holmes Institute, T1 2019

VerifiedAdded on 2022/11/17

|10

|746

|336

Project

AI Summary

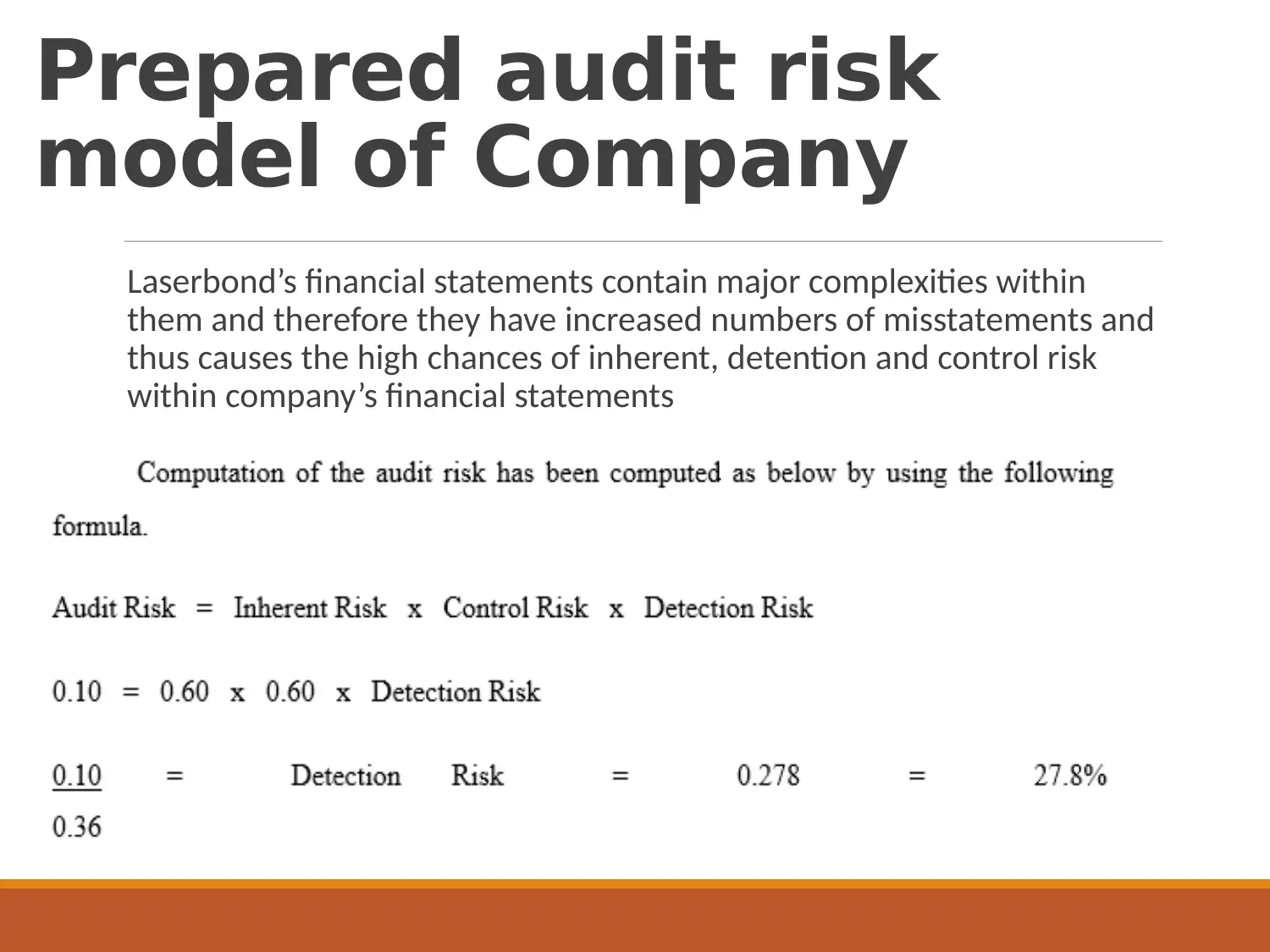

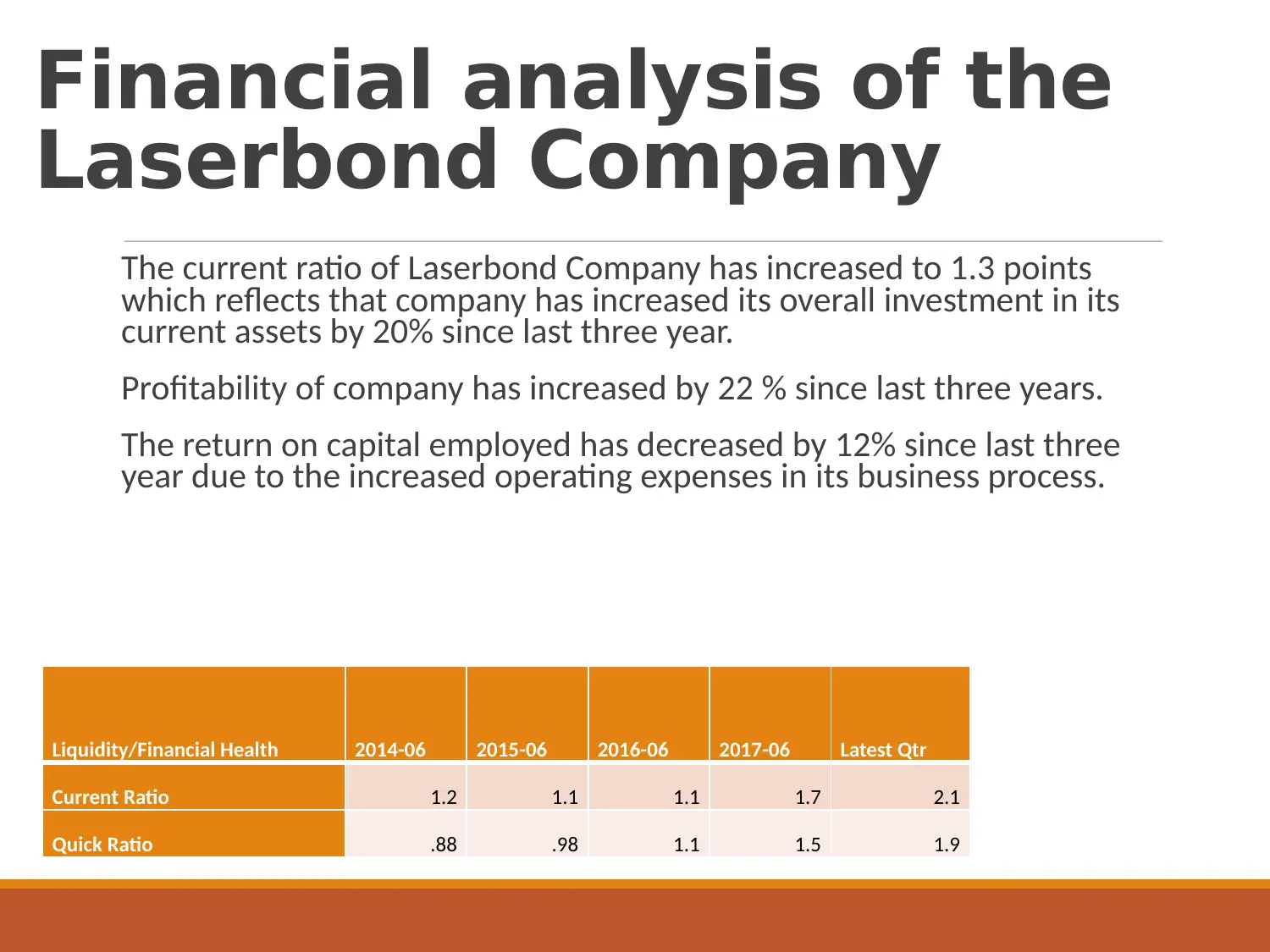

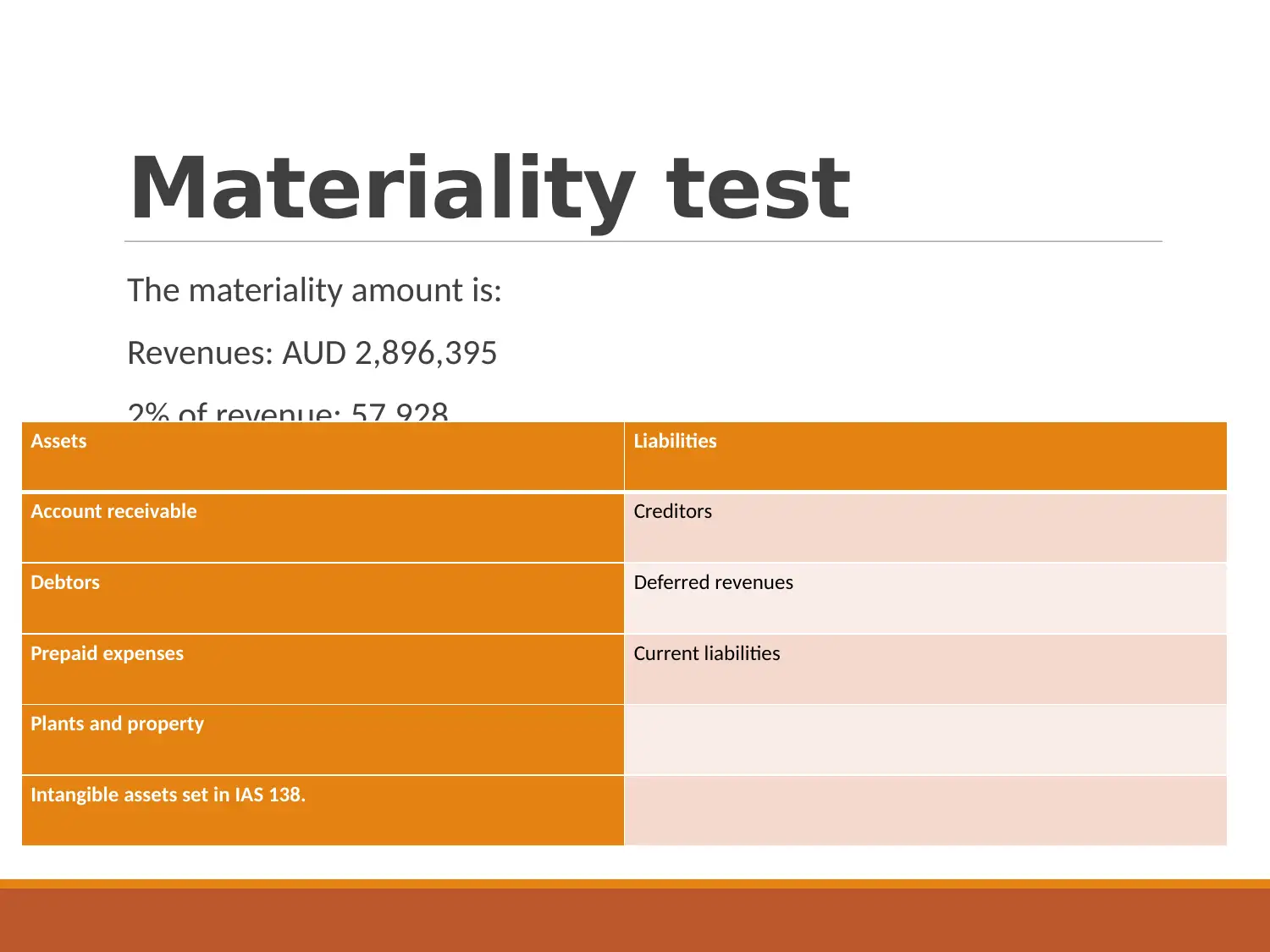

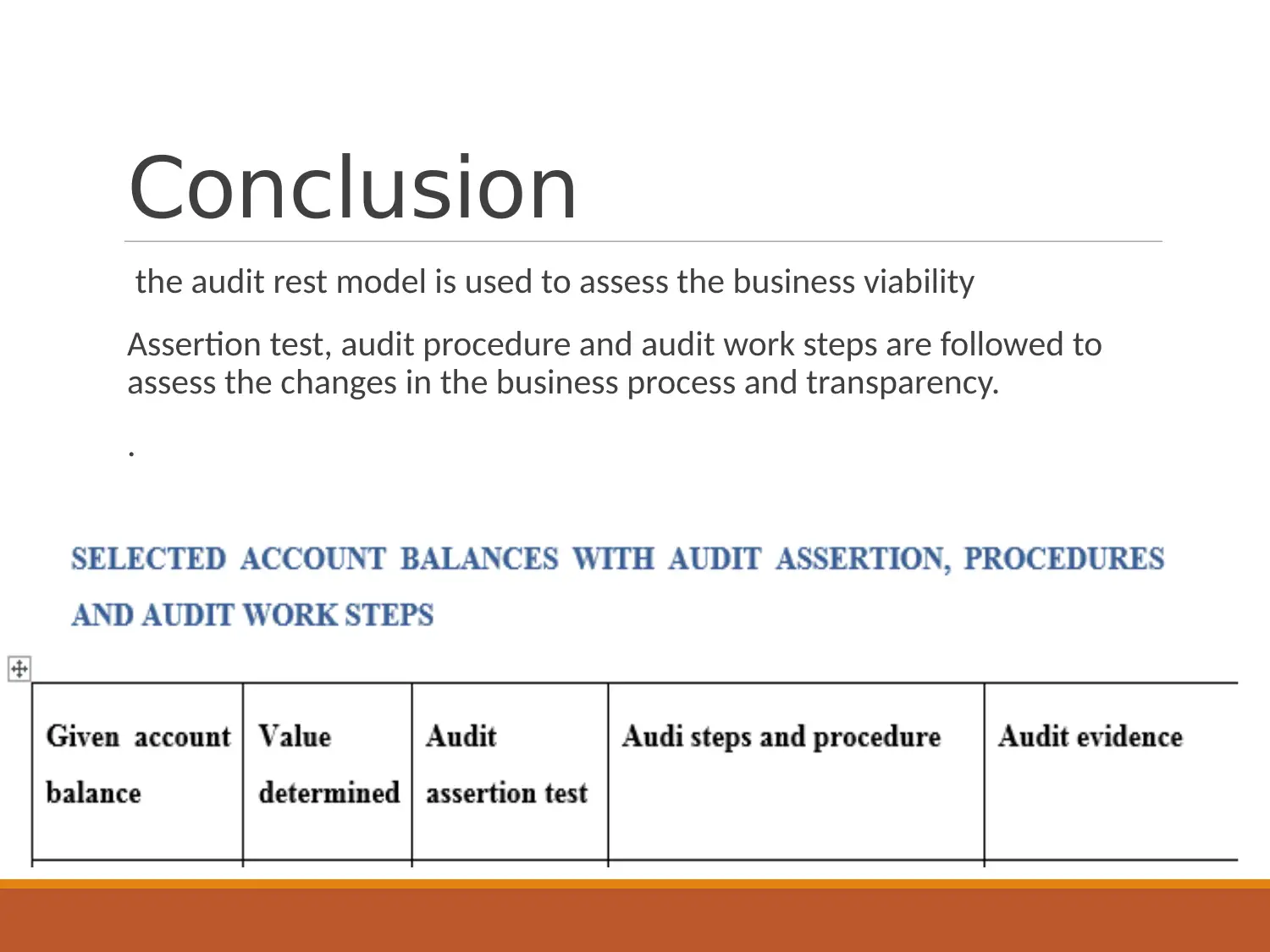

This assignment is a comprehensive audit program developed for Laserbond Ltd., a publicly listed company. It begins with an overview of the audit process, emphasizing the auditor's role in examining financial statements and related information. The project includes a financial analysis of Laserbond, highlighting key ratios and trends, followed by a discussion of materiality and its application in selecting account balances for detailed examination. The assignment details the use of materiality levels (2% of revenue) and the ASA 530 sampling method for audit sampling. It also addresses audit risk modeling, including inherent, detection, and control risks. Recommendations are provided, such as maintaining auditor independence and managing financial leverage. The assignment covers assertion tests, audit procedures, and work steps, providing a practical approach to assessing business processes and transparency. References to relevant literature are also included.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.