Audit Quality, Technology & the Restructured Code of Ethics

VerifiedAdded on 2022/08/24

|12

|2868

|33

Essay

AI Summary

This essay addresses the growing concerns surrounding audit quality and explores the potential of technology and the restructured Code of Ethics to enhance audit practices. It highlights the importance of reliable financial statements for stakeholders and examines instances where audit quality has been compromised, leading to corporate scandals. The essay discusses the conflict of interest that can arise between consulting businesses and audit firms, impacting auditor independence. It further investigates how technologies like artificial intelligence, robotic process automation, and data visualization can improve audit quality by managing unstructured data, automating routine transactions, and providing deeper insights. The restructured Code of Ethics is also examined for its role in promoting auditor independence, objectivity, and professional behavior, ultimately contributing to improved audit quality and public trust. This document is a student contribution and more solved assignments can be accessed on Desklib.

Audit & Assurance Service

1/18/2020

Student’s Name

1/18/2020

Student’s Name

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE SERVICE 1

In a financial statement of a business, different stakeholders have their interest involved

as they decide after reading and analyzing the information mentioned under the same. A reliable

financial statement is the one, which is appropriately and fairly audited. In recent years, many of

the cases have reported in the media where the quality of the audit was not according to the

standards. Even the former Chairman of the Australian Securities and Investments Commission

(ASIC) presented his concern about the quality of audit that has diminished during the past few

years. Some of the arguments have been made in the area according to which technologies can

improve help in improving quality of service. This essay is developed on the topic of audit

quality and the role of technology in the improvement of the same. In this essay, the discussion

will be made about the concern of poor audit quality. To understand the same, some real-world

examples will also be presented. In addition to the same, the ways in which IT can improve the

audit quality will also frame an important part of this essay.

Before moving the issues identified in audit quality and discussion made on the same,

first, the meaning of audit quality is required to be understood. This is to state that audit quality

contains the matter that contributes to the likelihood that the auditor will ensure that the financial

report presented by them is free from any misrepresentation, deficiencies of the same are

identified and properly communicated under the report itself (ASIC, 2019). The quality of the

audit is key for all the shareholders and investors. When the root of the audit is weak in the

company, it increases the chances of corporate scandals and collapses. Enroll is the biggest

example in support of this claim. Medcraft made it clear in his first broadcast interview after

retirement from the post of ASIC chairman made it clear that there would be no way to stop

Enrol similar scandals if auditing standards would continue to be poor (Ryan, 2019). He stated

that the big company like Enrol had immense issues in its financial yet the auditors failed to

In a financial statement of a business, different stakeholders have their interest involved

as they decide after reading and analyzing the information mentioned under the same. A reliable

financial statement is the one, which is appropriately and fairly audited. In recent years, many of

the cases have reported in the media where the quality of the audit was not according to the

standards. Even the former Chairman of the Australian Securities and Investments Commission

(ASIC) presented his concern about the quality of audit that has diminished during the past few

years. Some of the arguments have been made in the area according to which technologies can

improve help in improving quality of service. This essay is developed on the topic of audit

quality and the role of technology in the improvement of the same. In this essay, the discussion

will be made about the concern of poor audit quality. To understand the same, some real-world

examples will also be presented. In addition to the same, the ways in which IT can improve the

audit quality will also frame an important part of this essay.

Before moving the issues identified in audit quality and discussion made on the same,

first, the meaning of audit quality is required to be understood. This is to state that audit quality

contains the matter that contributes to the likelihood that the auditor will ensure that the financial

report presented by them is free from any misrepresentation, deficiencies of the same are

identified and properly communicated under the report itself (ASIC, 2019). The quality of the

audit is key for all the shareholders and investors. When the root of the audit is weak in the

company, it increases the chances of corporate scandals and collapses. Enroll is the biggest

example in support of this claim. Medcraft made it clear in his first broadcast interview after

retirement from the post of ASIC chairman made it clear that there would be no way to stop

Enrol similar scandals if auditing standards would continue to be poor (Ryan, 2019). He stated

that the big company like Enrol had immense issues in its financial yet the auditors failed to

AUDIT & ASSURANCE SERVICE 2

identify as well as notify the same. This kind of audit quality cannot be considered as good.

More often, there is a conflict of interest between the consulting business and the audit firm due

to the auditor does not fairly report deficiencies of financial statements. The seriousness of the

issue can be understood by the fact that global audit regulators have made questions regarding

25% of the audits. In addition to this, Medcraft also stated that auditor wants to make quick

money and therefore they move to consulting firms from auditing firms.

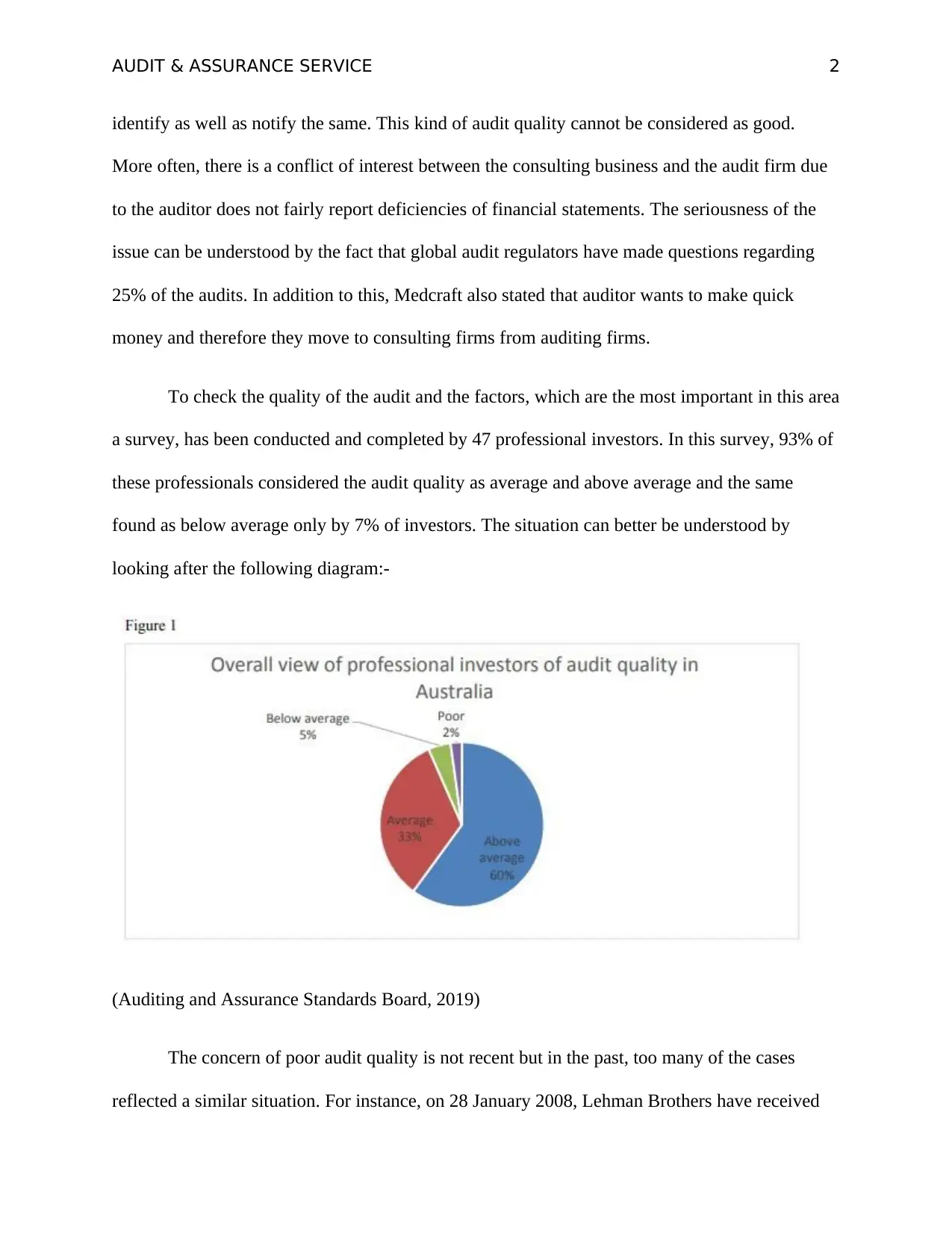

To check the quality of the audit and the factors, which are the most important in this area

a survey, has been conducted and completed by 47 professional investors. In this survey, 93% of

these professionals considered the audit quality as average and above average and the same

found as below average only by 7% of investors. The situation can better be understood by

looking after the following diagram:-

(Auditing and Assurance Standards Board, 2019)

The concern of poor audit quality is not recent but in the past, too many of the cases

reflected a similar situation. For instance, on 28 January 2008, Lehman Brothers have received

identify as well as notify the same. This kind of audit quality cannot be considered as good.

More often, there is a conflict of interest between the consulting business and the audit firm due

to the auditor does not fairly report deficiencies of financial statements. The seriousness of the

issue can be understood by the fact that global audit regulators have made questions regarding

25% of the audits. In addition to this, Medcraft also stated that auditor wants to make quick

money and therefore they move to consulting firms from auditing firms.

To check the quality of the audit and the factors, which are the most important in this area

a survey, has been conducted and completed by 47 professional investors. In this survey, 93% of

these professionals considered the audit quality as average and above average and the same

found as below average only by 7% of investors. The situation can better be understood by

looking after the following diagram:-

(Auditing and Assurance Standards Board, 2019)

The concern of poor audit quality is not recent but in the past, too many of the cases

reflected a similar situation. For instance, on 28 January 2008, Lehman Brothers have received

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE SERVICE 3

an unqualified audit opinion on its financial statements. In addition to this, a clean bill of health

has also received on its quarterly accounts. Nevertheless, the true financial situation of business

was worst, where the same started many financial difficulties by the early august and at last filed

bankruptcy in the September month of the same year. Another example can be taken of Bear

Stearns, the fifth-largest investment bank of America has received an unqualified opinion on the

financial statements on 28 January 2008, but in the month of March, the bank faced many

financial problems and later on sold to JP Morgan Chase. The numbers of similar cases are many

and it includes big names such as Carlyle Capital Corporation and Thornburg Mortgage. In the

quality of audit services, the lead question is related to the independence of the auditor. In the

case of Enron, similar issues have been raised by the US Senate Committee's report. The

committee outlined there is always a conflict of interest between the role of an auditor and other

works that a person may carry for the financial institution. The fee that auditors of distressed

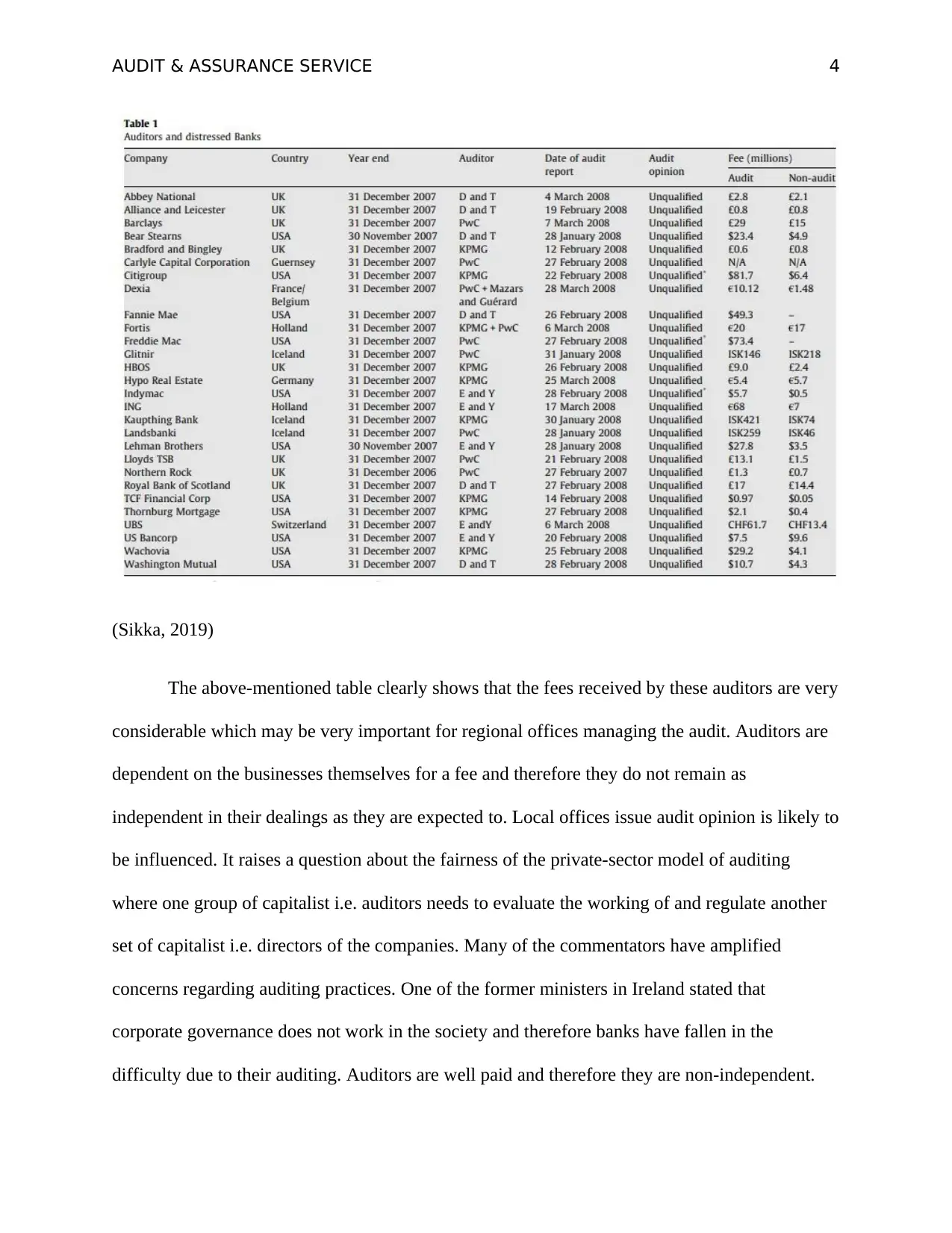

banks have received for their audits are mentioned in the given table:

an unqualified audit opinion on its financial statements. In addition to this, a clean bill of health

has also received on its quarterly accounts. Nevertheless, the true financial situation of business

was worst, where the same started many financial difficulties by the early august and at last filed

bankruptcy in the September month of the same year. Another example can be taken of Bear

Stearns, the fifth-largest investment bank of America has received an unqualified opinion on the

financial statements on 28 January 2008, but in the month of March, the bank faced many

financial problems and later on sold to JP Morgan Chase. The numbers of similar cases are many

and it includes big names such as Carlyle Capital Corporation and Thornburg Mortgage. In the

quality of audit services, the lead question is related to the independence of the auditor. In the

case of Enron, similar issues have been raised by the US Senate Committee's report. The

committee outlined there is always a conflict of interest between the role of an auditor and other

works that a person may carry for the financial institution. The fee that auditors of distressed

banks have received for their audits are mentioned in the given table:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE SERVICE 4

(Sikka, 2019)

The above-mentioned table clearly shows that the fees received by these auditors are very

considerable which may be very important for regional offices managing the audit. Auditors are

dependent on the businesses themselves for a fee and therefore they do not remain as

independent in their dealings as they are expected to. Local offices issue audit opinion is likely to

be influenced. It raises a question about the fairness of the private-sector model of auditing

where one group of capitalist i.e. auditors needs to evaluate the working of and regulate another

set of capitalist i.e. directors of the companies. Many of the commentators have amplified

concerns regarding auditing practices. One of the former ministers in Ireland stated that

corporate governance does not work in the society and therefore banks have fallen in the

difficulty due to their auditing. Auditors are well paid and therefore they are non-independent.

(Sikka, 2019)

The above-mentioned table clearly shows that the fees received by these auditors are very

considerable which may be very important for regional offices managing the audit. Auditors are

dependent on the businesses themselves for a fee and therefore they do not remain as

independent in their dealings as they are expected to. Local offices issue audit opinion is likely to

be influenced. It raises a question about the fairness of the private-sector model of auditing

where one group of capitalist i.e. auditors needs to evaluate the working of and regulate another

set of capitalist i.e. directors of the companies. Many of the commentators have amplified

concerns regarding auditing practices. One of the former ministers in Ireland stated that

corporate governance does not work in the society and therefore banks have fallen in the

difficulty due to their auditing. Auditors are well paid and therefore they are non-independent.

AUDIT & ASSURANCE SERVICE 5

Another commentator made an argument where he raised the question that why the big banks

pay millions of fees to auditors when they cannot even find the issues in the same. Are they paid

to show subprime assets as the valuable ones? Financial crises highlighted some old as well as

new questions related to the auditing practices. Traditionalists claim that the external audit is

useful for the creditability of financial statements but the same is not true because even after

taking services of external auditors, companies have suffered from loss due to the non-

presentation of material risk involved. Audit evidence is not available to the public, which puts a

big question mark on the creditability of the audits.

Another reason does also seem necessary to discuss here where the regulatory and

organizational politics define and manage the way of issuance of the audit report. In the previous

cases of banking failures, legislators have argued about the silence of auditors where they caused

major injury to innocent customers and investors. Different codes and standards have been

developed to promote fair auditing practices but no one of the same seems effective.

Very recently, PWC one of the four big auditing firms released the first balanced scorecard on

the audit quality of Australian companies. The scorecard also included results of audit inspection

finding of ASIC, according to which in 12% of the key audit areas, ASIC has not obtained any

reasonable assurance regarding the absence of material misstatement (Pwc, 2019). The concern

of audit quality is not a minor one and three of the big 4 auditing firms has failed to do sufficient

work to support and justify the audit opinions of all the significant aspect or at least one of the

client (Wootton, 2019). KPMG has disclosed to accounts daily that twenty-one percent of total

audits reviewed by the same lacked assurance of the fact that the whole financial statement is

free from error. Further BDO, one of the six largest firms disclosed that ASIC has identified 8

percent of key audit areas where a risk of material misstatement has found (Lian, 2019).

Another commentator made an argument where he raised the question that why the big banks

pay millions of fees to auditors when they cannot even find the issues in the same. Are they paid

to show subprime assets as the valuable ones? Financial crises highlighted some old as well as

new questions related to the auditing practices. Traditionalists claim that the external audit is

useful for the creditability of financial statements but the same is not true because even after

taking services of external auditors, companies have suffered from loss due to the non-

presentation of material risk involved. Audit evidence is not available to the public, which puts a

big question mark on the creditability of the audits.

Another reason does also seem necessary to discuss here where the regulatory and

organizational politics define and manage the way of issuance of the audit report. In the previous

cases of banking failures, legislators have argued about the silence of auditors where they caused

major injury to innocent customers and investors. Different codes and standards have been

developed to promote fair auditing practices but no one of the same seems effective.

Very recently, PWC one of the four big auditing firms released the first balanced scorecard on

the audit quality of Australian companies. The scorecard also included results of audit inspection

finding of ASIC, according to which in 12% of the key audit areas, ASIC has not obtained any

reasonable assurance regarding the absence of material misstatement (Pwc, 2019). The concern

of audit quality is not a minor one and three of the big 4 auditing firms has failed to do sufficient

work to support and justify the audit opinions of all the significant aspect or at least one of the

client (Wootton, 2019). KPMG has disclosed to accounts daily that twenty-one percent of total

audits reviewed by the same lacked assurance of the fact that the whole financial statement is

free from error. Further BDO, one of the six largest firms disclosed that ASIC has identified 8

percent of key audit areas where a risk of material misstatement has found (Lian, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE SERVICE 6

After the above-mentioned discussion, it is far clear that the concern of audit quality is, a serious

one and poor quality of audit contribute to the corporate scandals and collapse. Now moving the

discussion towards the solution of this issue is to state that the restructured code of ethics can

help in the same which also serves the public interest. The code of ethics provides the manner of

working and conducting practice for auditors. The new international code of ethics for

professional accountants has been effective from 15 June 2019. To understand the manner in

which this code works this is to stat that the same raises awareness regarding lead elements of

audit quality. In addition to this, it also motivates stakeholders to identify the ways in which

audit quality can be improved (ifac, 2019). The restructured code outlines the provisions related

to fees, gifts, and hospitality. Where it limits and puts an obligation on auditors with respect to

the acceptance of gifts, it improves their independence.

The code sets a higher standard for audit and ensures a quality review by the professional

body. It promotes fundamental principles in the behavior of auditors such as objectivity,

integrity, confidentiality, and professional behavior. The code reminds the auditors that they

need to remain independent while providing review, assurance and audit services. The highlight

of the new code is that independence rule has been moved to the new section namely

international independence standards. In addition to this, the revised code is easy to read and

understand and enhances clarity. It clearly makes a difference between requirements and

application material. On professional accounts, some special obligations have been imposed

which are mandatory to be complied with. As the rules are typical and more clear under the new

code, it is expected that the same will contribute to the improvement of audit quality. When

auditors would be more informed about their role and expectations of stakeholders, there will be

fewer chances of negligence as well as fraud in the audit process.

After the above-mentioned discussion, it is far clear that the concern of audit quality is, a serious

one and poor quality of audit contribute to the corporate scandals and collapse. Now moving the

discussion towards the solution of this issue is to state that the restructured code of ethics can

help in the same which also serves the public interest. The code of ethics provides the manner of

working and conducting practice for auditors. The new international code of ethics for

professional accountants has been effective from 15 June 2019. To understand the manner in

which this code works this is to stat that the same raises awareness regarding lead elements of

audit quality. In addition to this, it also motivates stakeholders to identify the ways in which

audit quality can be improved (ifac, 2019). The restructured code outlines the provisions related

to fees, gifts, and hospitality. Where it limits and puts an obligation on auditors with respect to

the acceptance of gifts, it improves their independence.

The code sets a higher standard for audit and ensures a quality review by the professional

body. It promotes fundamental principles in the behavior of auditors such as objectivity,

integrity, confidentiality, and professional behavior. The code reminds the auditors that they

need to remain independent while providing review, assurance and audit services. The highlight

of the new code is that independence rule has been moved to the new section namely

international independence standards. In addition to this, the revised code is easy to read and

understand and enhances clarity. It clearly makes a difference between requirements and

application material. On professional accounts, some special obligations have been imposed

which are mandatory to be complied with. As the rules are typical and more clear under the new

code, it is expected that the same will contribute to the improvement of audit quality. When

auditors would be more informed about their role and expectations of stakeholders, there will be

fewer chances of negligence as well as fraud in the audit process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE SERVICE 7

Some of the arguments have also been made in relation to information technology where

it was believed that the use of technology could improve the standard and quality of audit.

Several finance leaders who state that the quality of their external audit benefits by using these

technologies has also supported the argument. These technologies include cloud, data and

analytics, and artificial intelligence. In a recent KPMG survey conducted on 250 corporates, it

was revealed that 94% of companies have accepted that their audit quality has been improved by

using these technologies (Forbes, 2019). In the following discussion, some of these techniques

will be discussed and the manner in which the same improve audit quality will also be discussed.

The very first technology is artificial intelligence. A huge amount of unstructured data can be

found in every enterprise. AI helps here where the same can manages these unstructured and

internal sources from local and international contracts to all the vendor transactions with

suspicious features. The scope of AI is not limited up to internal sources but it can also monitor

and review external data sources such as audio sources as well as video sources such as media

such as television and social media. This monitoring helps in getting additional information that

contributes to the comprehensiveness of the audit.

The other technology is robotic process automation. This technology is commonly known

by its abbreviation i.e. RPA and the same capture a transaction by the use of the software. In

addition to capturing the data, the same also interpret that transaction and manipulate the data.

The same can automate communication with other processes. This technology is very much

suitable for reconciling routine transactions especially revenue-based transactions. Due to this

automation in the process, auditors get more time to focus on other areas such as a focus on

clients and gaining new insights from organizational information. In the CPA journal, Andrea M.

Rozario and Miklos A. Vasarhelyi wrote that the RPA based audit process might improve the

Some of the arguments have also been made in relation to information technology where

it was believed that the use of technology could improve the standard and quality of audit.

Several finance leaders who state that the quality of their external audit benefits by using these

technologies has also supported the argument. These technologies include cloud, data and

analytics, and artificial intelligence. In a recent KPMG survey conducted on 250 corporates, it

was revealed that 94% of companies have accepted that their audit quality has been improved by

using these technologies (Forbes, 2019). In the following discussion, some of these techniques

will be discussed and the manner in which the same improve audit quality will also be discussed.

The very first technology is artificial intelligence. A huge amount of unstructured data can be

found in every enterprise. AI helps here where the same can manages these unstructured and

internal sources from local and international contracts to all the vendor transactions with

suspicious features. The scope of AI is not limited up to internal sources but it can also monitor

and review external data sources such as audio sources as well as video sources such as media

such as television and social media. This monitoring helps in getting additional information that

contributes to the comprehensiveness of the audit.

The other technology is robotic process automation. This technology is commonly known

by its abbreviation i.e. RPA and the same capture a transaction by the use of the software. In

addition to capturing the data, the same also interpret that transaction and manipulate the data.

The same can automate communication with other processes. This technology is very much

suitable for reconciling routine transactions especially revenue-based transactions. Due to this

automation in the process, auditors get more time to focus on other areas such as a focus on

clients and gaining new insights from organizational information. In the CPA journal, Andrea M.

Rozario and Miklos A. Vasarhelyi wrote that the RPA based audit process might improve the

AUDIT & ASSURANCE SERVICE 8

effectiveness and efficiency of the audit. This technology has the ability to analyses 100% of the

dataset and therefore auditors are no more required to rely on sampling (Hoggett, Dubois,

O'Connor, Jamieson, 2019). Due to these technologies audit may become deeper.

The third technology is visualization. This technology works on the simple ground that

when the data is presented in the graphical form the same is a good option to absorb information.

A picture presents data more easily and just by looking after a diagram, one can get the price

trends and other aspects very quickly in comparison to other forms of data representation such as

tables and theory. If auditors receive the data available with the company in the graphical format,

they can complete their working in a time-bound manner and gets more insights into system,

trends, and transactions. It also helps auditors in making more realistic decisions and judgments.

Similarly, when auditors use charts and graphs in their audit reports, it makes easy for users of

financial data the true picture of the financial condition of the company.

It clearly shows that the use of advanced technology provides great promise to the audit.

Nevertheless, these technologies are good when the audit team guides them as well as analyzes

the results. Further, this should also be clear that these technologies are only helpful to the

working of auditors and cannot replace the expertise and manual judgment of auditors. Hence to

state that the fundamentals of the audit will not be changed.

To conclude the essay this is to state that the audit quality has decreased up to a

significant level in recent times and the lead reason is lack of independence of the auditors where

they do provide unqualified opinions even after knowing the poor status of finance and

deficiencies. Such poor and unprofessional audit practices lead the corporate collapse and

therefore there is an urgent need to remove these issues. One of the ways, which has been

effectiveness and efficiency of the audit. This technology has the ability to analyses 100% of the

dataset and therefore auditors are no more required to rely on sampling (Hoggett, Dubois,

O'Connor, Jamieson, 2019). Due to these technologies audit may become deeper.

The third technology is visualization. This technology works on the simple ground that

when the data is presented in the graphical form the same is a good option to absorb information.

A picture presents data more easily and just by looking after a diagram, one can get the price

trends and other aspects very quickly in comparison to other forms of data representation such as

tables and theory. If auditors receive the data available with the company in the graphical format,

they can complete their working in a time-bound manner and gets more insights into system,

trends, and transactions. It also helps auditors in making more realistic decisions and judgments.

Similarly, when auditors use charts and graphs in their audit reports, it makes easy for users of

financial data the true picture of the financial condition of the company.

It clearly shows that the use of advanced technology provides great promise to the audit.

Nevertheless, these technologies are good when the audit team guides them as well as analyzes

the results. Further, this should also be clear that these technologies are only helpful to the

working of auditors and cannot replace the expertise and manual judgment of auditors. Hence to

state that the fundamentals of the audit will not be changed.

To conclude the essay this is to state that the audit quality has decreased up to a

significant level in recent times and the lead reason is lack of independence of the auditors where

they do provide unqualified opinions even after knowing the poor status of finance and

deficiencies. Such poor and unprofessional audit practices lead the corporate collapse and

therefore there is an urgent need to remove these issues. One of the ways, which has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE SERVICE 9

identified, is the adoption of a restructured code of ethics that outlines the duties of auditors as

well as provisions of fee and gifts in a more detailed manner and removes the confusion that

could be seen in the earlier codes. In conjunction with the same use of IT, advanced technologies

in audit is also an important way. Some of the major IT technologies such as AI, RPA, and

visualization have been discussed. These technologies collect and evaluate data, in less time and

a more efficient manner that generates quick and reliable results out of an audit process. The

adoption of these technologies is a welcome step that the auditors should adopt in their workings

to improve the quality of their work.

identified, is the adoption of a restructured code of ethics that outlines the duties of auditors as

well as provisions of fee and gifts in a more detailed manner and removes the confusion that

could be seen in the earlier codes. In conjunction with the same use of IT, advanced technologies

in audit is also an important way. Some of the major IT technologies such as AI, RPA, and

visualization have been discussed. These technologies collect and evaluate data, in less time and

a more efficient manner that generates quick and reliable results out of an audit process. The

adoption of these technologies is a welcome step that the auditors should adopt in their workings

to improve the quality of their work.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE SERVICE 10

References

ASIC. (2019). Improving and maintaining audit quality. Retrieved From:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/improving-

and-maintaining-audit-quality/#what

Auditing and Assurance Standards Board. (2019). Audit Quality In Australia: The Perspectives

Of Professional Investors March 2019. Retrieved From:

https://cdn.tspace.gov.au/uploads/sites/21/2019/05/Audit_Qulaity_in_Australia_-

_The_Per.pdf

Forbes. (2019) How Advanced Technologies May Improve Audit Quality. Retrieved From:

https://www.forbes.com/sites/insights-kpmg/2019/03/04/how-advanced-technologies-

may-improve-audit-quality/#7354fa6c5632

Hoggett, E., Dubois, S., O'Connor, S., Jamieson, R. (2019). Improving audit quality with new

technology. https://home.kpmg/au/en/home/insights/2019/02/audit-technology-future-

technology-audit-quality.html

Ifac. (2019) Enhancing Audit Quality In The Public Interest. Retrieved From:

https://www.ifac.org/system/files/publications/files/IAASB-Overview-Invitation-to-

Comment-Enhancing-Audit-Quality.pdf

Lian, J. (2019) PwC, KPMG, EY, BDO reveal ASIC’s audit findings. Retrieved From:

https://www.accountantsdaily.com.au/tax-compliance/13080-pwc-kpmg-reveal-asic-s-

audit-findings

References

ASIC. (2019). Improving and maintaining audit quality. Retrieved From:

https://asic.gov.au/regulatory-resources/financial-reporting-and-audit/auditors/improving-

and-maintaining-audit-quality/#what

Auditing and Assurance Standards Board. (2019). Audit Quality In Australia: The Perspectives

Of Professional Investors March 2019. Retrieved From:

https://cdn.tspace.gov.au/uploads/sites/21/2019/05/Audit_Qulaity_in_Australia_-

_The_Per.pdf

Forbes. (2019) How Advanced Technologies May Improve Audit Quality. Retrieved From:

https://www.forbes.com/sites/insights-kpmg/2019/03/04/how-advanced-technologies-

may-improve-audit-quality/#7354fa6c5632

Hoggett, E., Dubois, S., O'Connor, S., Jamieson, R. (2019). Improving audit quality with new

technology. https://home.kpmg/au/en/home/insights/2019/02/audit-technology-future-

technology-audit-quality.html

Ifac. (2019) Enhancing Audit Quality In The Public Interest. Retrieved From:

https://www.ifac.org/system/files/publications/files/IAASB-Overview-Invitation-to-

Comment-Enhancing-Audit-Quality.pdf

Lian, J. (2019) PwC, KPMG, EY, BDO reveal ASIC’s audit findings. Retrieved From:

https://www.accountantsdaily.com.au/tax-compliance/13080-pwc-kpmg-reveal-asic-s-

audit-findings

AUDIT & ASSURANCE SERVICE 11

Pwc. (2019) PwC releases Australia’s first balanced scorecard on audit quality. Retrieved From:

https://www.pwc.com.au/press-room/2019/pwc-releases-balanced-scorecard.html

Ryan, P. (2019) Audit firms' conflicts of interest could spark Enron-style corporate collapse,

former ASIC boss warns. Retrieved From:

https://www.abc.net.au/news/2019-08-06/audit-firm-failures-could-spark-enron-style-

collapse-medcraft/11388164

Sikka, P. (2009). Financial crisis and the silence of the auditors. Accounting, Organizations and

Society, 34(6-7), 868-873.

Wootton, H. (2019) EY, Deloitte, KPMG fall short in audit quality. Retrieved From:

https://www.afr.com/companies/professional-services/0ey-deloitte-kpmg-fall-short-in-

audit-quality-20191215-p53k2l

Pwc. (2019) PwC releases Australia’s first balanced scorecard on audit quality. Retrieved From:

https://www.pwc.com.au/press-room/2019/pwc-releases-balanced-scorecard.html

Ryan, P. (2019) Audit firms' conflicts of interest could spark Enron-style corporate collapse,

former ASIC boss warns. Retrieved From:

https://www.abc.net.au/news/2019-08-06/audit-firm-failures-could-spark-enron-style-

collapse-medcraft/11388164

Sikka, P. (2009). Financial crisis and the silence of the auditors. Accounting, Organizations and

Society, 34(6-7), 868-873.

Wootton, H. (2019) EY, Deloitte, KPMG fall short in audit quality. Retrieved From:

https://www.afr.com/companies/professional-services/0ey-deloitte-kpmg-fall-short-in-

audit-quality-20191215-p53k2l

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.