CQUniversity ACCT20075 Auditing and Ethics Assignment: Audit Report

VerifiedAdded on 2023/03/20

|14

|2387

|53

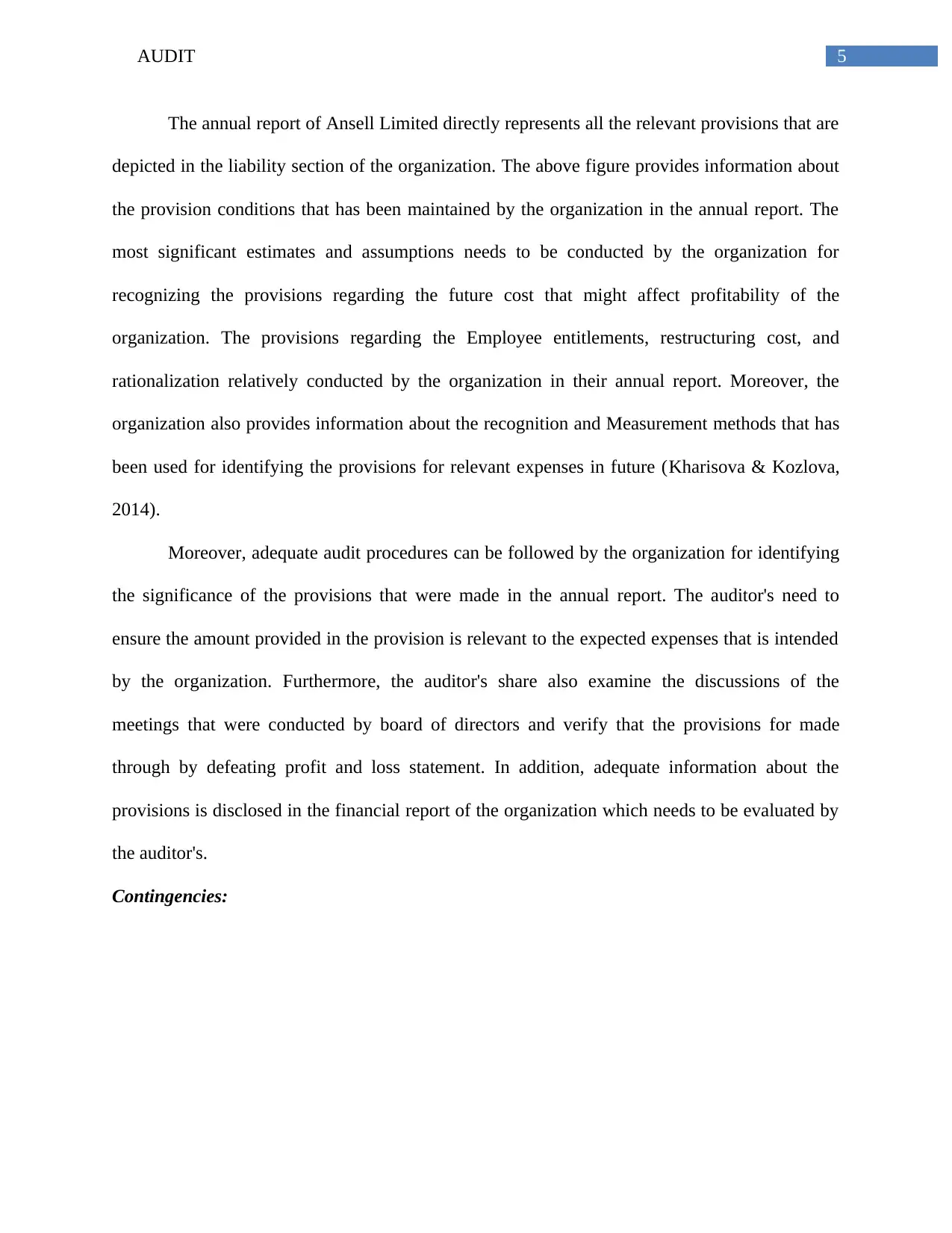

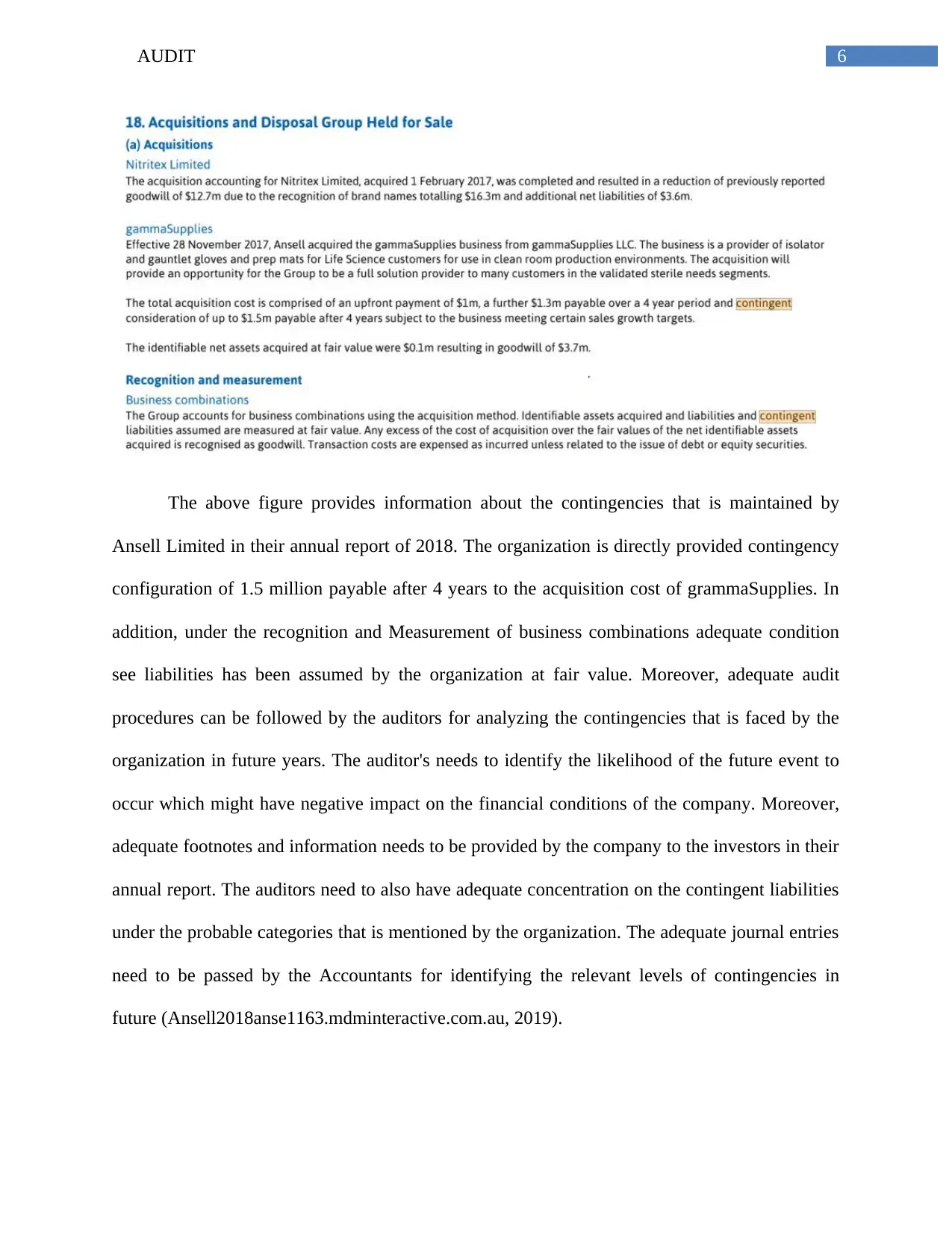

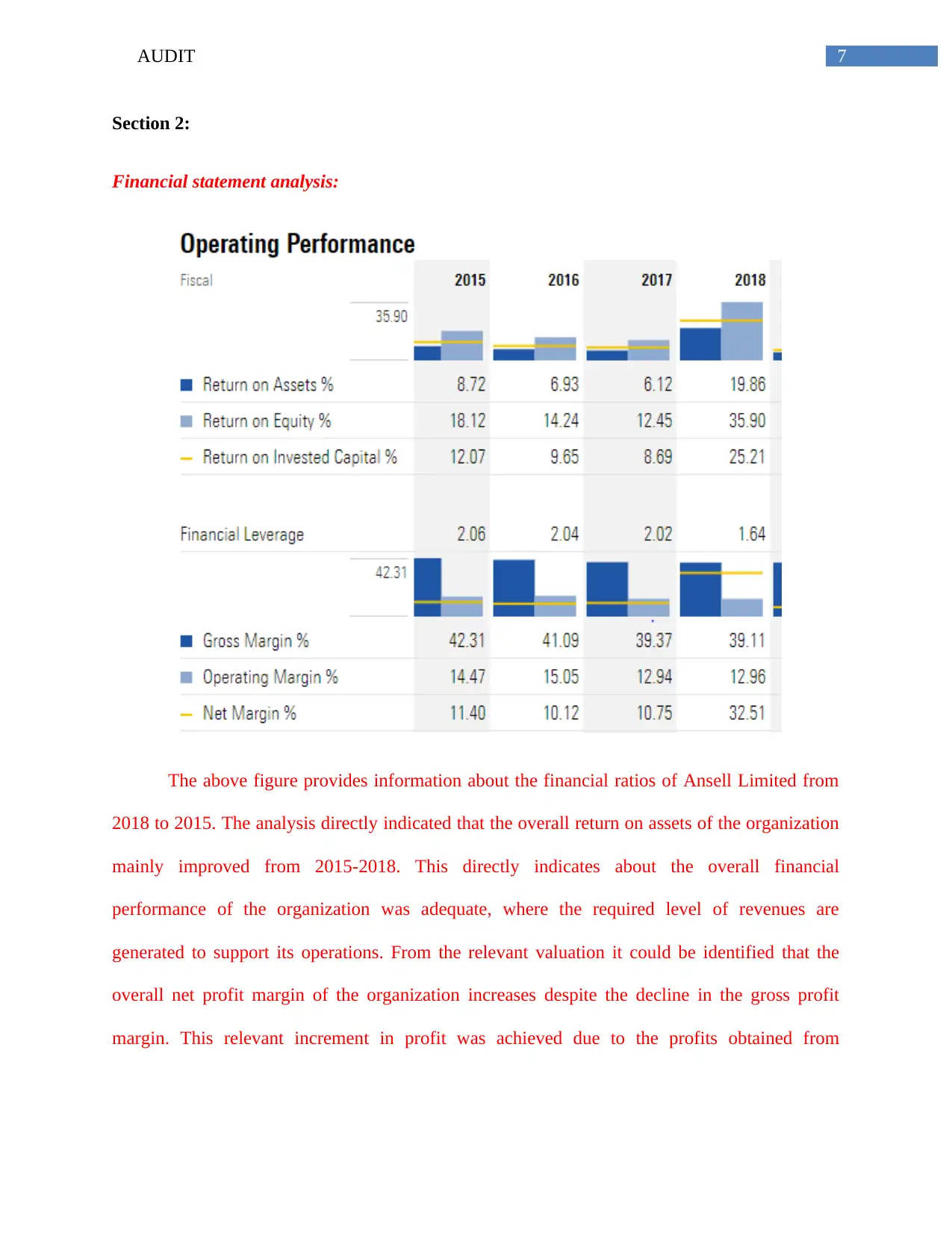

Report

AI Summary

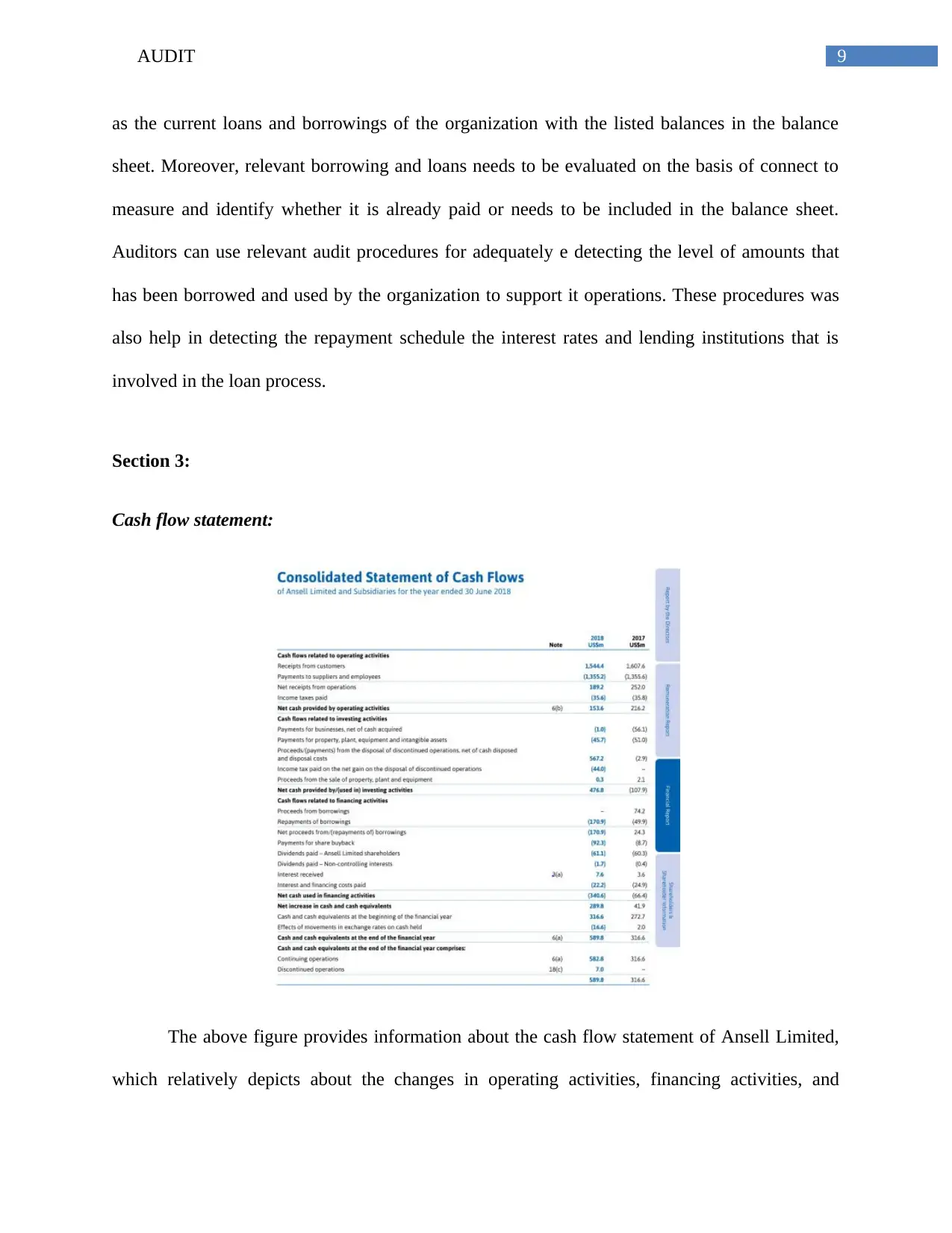

This report analyzes an audit engagement for a listed company, focusing on materiality assessment, financial statement analysis, and audit procedures. The report begins with an introduction to audit materiality and its significance in evaluating financial statements. It then delves into the calculation of materiality levels based on gross revenue, total assets, shareholder's equity, and net profit. The analysis includes a review of significant audit items like contingencies and provisions, detailing the audit procedures and disclosures. The report further examines the company's financial performance through ratio analysis, assessing return on assets, net profit margin, and financial leverage. It also discusses key assertions related to cash and interest-bearing loans and provides a cash flow statement analysis, highlighting changes in operating, investing, and financing activities. The report concludes with an evaluation of the audit report, emphasizing its adherence to relevant accounting standards and regulations. The report is a comprehensive overview of the audit process, offering insights into materiality assessment, financial statement analysis, and the role of audit procedures.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.