2019 Audit Theory and Practice: Audit Report on API's Finances

VerifiedAdded on 2023/01/04

|17

|4000

|42

Report

AI Summary

This report presents an audit analysis of Always Precise Instruments Pty Limited, focusing on financial performance and internal controls. The analysis includes a detailed examination of various financial ratios such as current ratio, quick ratio, return on equity, return on total assets, gross margin, marketing expenses, administrative expenses, times interest earned, days in inventory, days in accounts receivable, and debt to equity ratio. Each ratio is assessed for its audit risk level and the corresponding audit procedures. The report also identifies and evaluates internal control weaknesses, proposing audit procedures to mitigate the associated risks, particularly in the areas of purchase order generation and inventory management. The report concludes with an overview of the audit process and its significance in risk management, providing insights into the company's financial health and operational efficiency.

AUDIT THEORY AND PRACTICE

2019

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

Executive Summary

The organizations in the present scenario are bound to have a high level of audit procedure

because it is in direct tune to the company’s functioning. The audit procedure is a mandate

that helps the company to function effectively. In this report, analysis of the items has been

done together with the audit procedure. Further, internal control and weakness has been

studied in the light of Always Precise Instruments Pty Limited.

2

Executive Summary

The organizations in the present scenario are bound to have a high level of audit procedure

because it is in direct tune to the company’s functioning. The audit procedure is a mandate

that helps the company to function effectively. In this report, analysis of the items has been

done together with the audit procedure. Further, internal control and weakness has been

studied in the light of Always Precise Instruments Pty Limited.

2

Audit

Contents

Introduction...........................................................................................................................................3

Requirement 1.......................................................................................................................................3

Requirement 2.....................................................................................................................................10

Requirement 3.....................................................................................................................................14

Conclusion...........................................................................................................................................15

References...........................................................................................................................................16

3

Contents

Introduction...........................................................................................................................................3

Requirement 1.......................................................................................................................................3

Requirement 2.....................................................................................................................................10

Requirement 3.....................................................................................................................................14

Conclusion...........................................................................................................................................15

References...........................................................................................................................................16

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

Introduction

Audit strategy, as well as the process of audit plays a dominating role in the identification of

risks of material nature in the organization. This can help the company in steering ahead in

the area of complications and challenges. This report stress upon the fact that audit is an

essential function of the organization and plays a dominating role is the process of risk

management (Wright & Charles, 2012). The report further sheds light upon the mechanism

of risks management together with the process of internal control. Internal control weakness

can hamper the movement of the company and it is though the audit function that the same

can mitigated.

Requirement 1

Ratio Analysis Audit

Risk

Audit

procedure

Current ratio: This ratio is very useful for calculation of short term liquidity

position of the organization. Liquidity is the state of an

individual on an organization to repay the debts as soon as

possible. After observing the business of Always Precise

Instruments Private Limited it can be stated that the higher

volume of sales and reduced trade receivables make it necessary

for the organization to have an increasing current ratio so that

they can increase the cash flows which will further help them to

increase the sales. In order to make it possible for the

organization to improve the sales and decrease the debts at the

same time, it is very necessary for the company to improvise the

cash flow position so as to move the current assets and liabilities

at the same pace. This will keep the organization free from any

kind of loans because of which it can earn more revenue. For the

year 2018, it was observed that the current ratio improves from

1.54 to 1.64 which is very appreciable in nature. This ratio is not

sufficient in accordance with the industry average but the small

Low Risk In this

scenario

analytical

procedure

should be used

by the auditor

to compare the

current assets

and current

liabilities.

The ratio

comparison

should be

same over the

period of time

unless the

company

4

Introduction

Audit strategy, as well as the process of audit plays a dominating role in the identification of

risks of material nature in the organization. This can help the company in steering ahead in

the area of complications and challenges. This report stress upon the fact that audit is an

essential function of the organization and plays a dominating role is the process of risk

management (Wright & Charles, 2012). The report further sheds light upon the mechanism

of risks management together with the process of internal control. Internal control weakness

can hamper the movement of the company and it is though the audit function that the same

can mitigated.

Requirement 1

Ratio Analysis Audit

Risk

Audit

procedure

Current ratio: This ratio is very useful for calculation of short term liquidity

position of the organization. Liquidity is the state of an

individual on an organization to repay the debts as soon as

possible. After observing the business of Always Precise

Instruments Private Limited it can be stated that the higher

volume of sales and reduced trade receivables make it necessary

for the organization to have an increasing current ratio so that

they can increase the cash flows which will further help them to

increase the sales. In order to make it possible for the

organization to improve the sales and decrease the debts at the

same time, it is very necessary for the company to improvise the

cash flow position so as to move the current assets and liabilities

at the same pace. This will keep the organization free from any

kind of loans because of which it can earn more revenue. For the

year 2018, it was observed that the current ratio improves from

1.54 to 1.64 which is very appreciable in nature. This ratio is not

sufficient in accordance with the industry average but the small

Low Risk In this

scenario

analytical

procedure

should be used

by the auditor

to compare the

current assets

and current

liabilities.

The ratio

comparison

should be

same over the

period of time

unless the

company

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

woman attraction from the past year has made sufficient

budgetary changes. Hence, this becomes an area with low risk.

altered the

position.

Quick asset

ratio:

The quick ratio is also termed as the asset test ratio. It can be

calculated by comparing the total of liquid assets to a total of

liquid liabilities. It was observed for the year 2018 that the quick

ratio of the company improved just like the current ratio. Also

after analyzing this, it can be suggested that the current assets are

sufficient in order to fulfil the debts of current liabilities or they

are moving at a much-increased rate when compared to the

current liabilities which is very good for the organization. It is

very important for the order to check the current ratio and quick

ratio of the organization Always Price Instruments Private

Limited because of their increasing rates which may further help

the organization to improve the cash and cash equivalents and

also remove the debts. Hence, this can be termed as a low-risk

area.

Low Risk Similar

observation

will be made

in this case

where the

auditor should

have an

analytical

procedure. A

comparison

with the

previous year

data will fetch

a good

response in

terms of

evaluation.

Return on

equity %

Return on equity percentage is set to indicate the net profit after

tax as a percentage of the net worth of the organization. For this

particular case of Always Precise Instruments Private Limited, it

was observed that day equity return for the year 2017 was 16.6%

while the budgeted return on equity was stated to be 18.4%. The

unaudited figures were amounting to 14.7% but the industry

average is observed to be 17.3% because of which it doesn't

seem favourable for the organization. This value clearly suggests

that the management of the organization is not able to achieve

the target or goals certified by them in the budget. Hence, this

will call for an evaluation and study so that the projected area

can be clearly observed for vulnerabilities because of which the

company has failed to achieve the targets. Hence, this area will

Moderate

Risk

An

observation

should be

done by the

auditor in the

area of equity

return. An

evaluation and

study needs to

be done so

that the

projected area

can be clearly

5

woman attraction from the past year has made sufficient

budgetary changes. Hence, this becomes an area with low risk.

altered the

position.

Quick asset

ratio:

The quick ratio is also termed as the asset test ratio. It can be

calculated by comparing the total of liquid assets to a total of

liquid liabilities. It was observed for the year 2018 that the quick

ratio of the company improved just like the current ratio. Also

after analyzing this, it can be suggested that the current assets are

sufficient in order to fulfil the debts of current liabilities or they

are moving at a much-increased rate when compared to the

current liabilities which is very good for the organization. It is

very important for the order to check the current ratio and quick

ratio of the organization Always Price Instruments Private

Limited because of their increasing rates which may further help

the organization to improve the cash and cash equivalents and

also remove the debts. Hence, this can be termed as a low-risk

area.

Low Risk Similar

observation

will be made

in this case

where the

auditor should

have an

analytical

procedure. A

comparison

with the

previous year

data will fetch

a good

response in

terms of

evaluation.

Return on

equity %

Return on equity percentage is set to indicate the net profit after

tax as a percentage of the net worth of the organization. For this

particular case of Always Precise Instruments Private Limited, it

was observed that day equity return for the year 2017 was 16.6%

while the budgeted return on equity was stated to be 18.4%. The

unaudited figures were amounting to 14.7% but the industry

average is observed to be 17.3% because of which it doesn't

seem favourable for the organization. This value clearly suggests

that the management of the organization is not able to achieve

the target or goals certified by them in the budget. Hence, this

will call for an evaluation and study so that the projected area

can be clearly observed for vulnerabilities because of which the

company has failed to achieve the targets. Hence, this area will

Moderate

Risk

An

observation

should be

done by the

auditor in the

area of equity

return. An

evaluation and

study needs to

be done so

that the

projected area

can be clearly

5

Audit

be of moderate risk. observed for

vulnerabilities

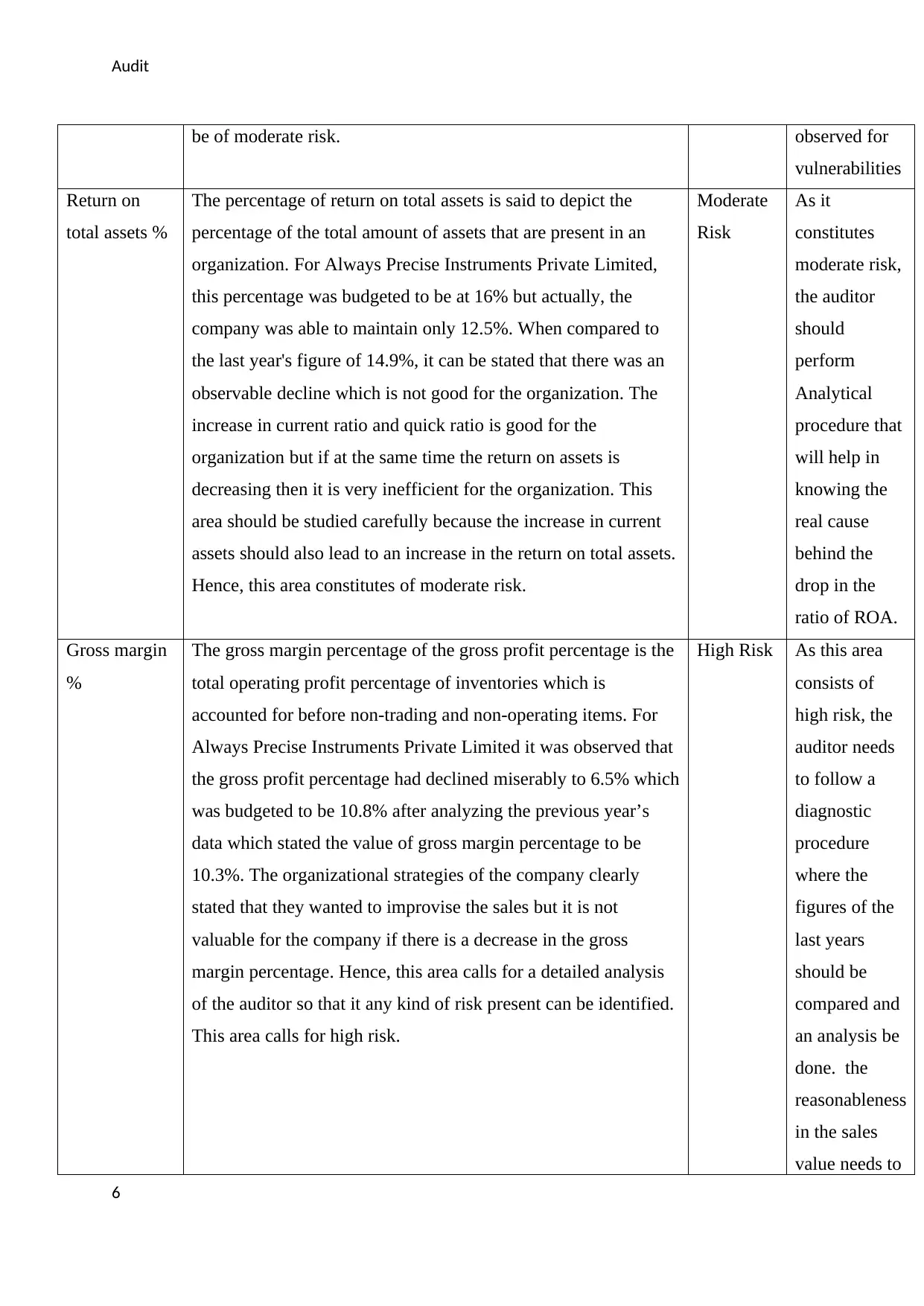

Return on

total assets %

The percentage of return on total assets is said to depict the

percentage of the total amount of assets that are present in an

organization. For Always Precise Instruments Private Limited,

this percentage was budgeted to be at 16% but actually, the

company was able to maintain only 12.5%. When compared to

the last year's figure of 14.9%, it can be stated that there was an

observable decline which is not good for the organization. The

increase in current ratio and quick ratio is good for the

organization but if at the same time the return on assets is

decreasing then it is very inefficient for the organization. This

area should be studied carefully because the increase in current

assets should also lead to an increase in the return on total assets.

Hence, this area constitutes of moderate risk.

Moderate

Risk

As it

constitutes

moderate risk,

the auditor

should

perform

Analytical

procedure that

will help in

knowing the

real cause

behind the

drop in the

ratio of ROA.

Gross margin

%

The gross margin percentage of the gross profit percentage is the

total operating profit percentage of inventories which is

accounted for before non-trading and non-operating items. For

Always Precise Instruments Private Limited it was observed that

the gross profit percentage had declined miserably to 6.5% which

was budgeted to be 10.8% after analyzing the previous year’s

data which stated the value of gross margin percentage to be

10.3%. The organizational strategies of the company clearly

stated that they wanted to improvise the sales but it is not

valuable for the company if there is a decrease in the gross

margin percentage. Hence, this area calls for a detailed analysis

of the auditor so that it any kind of risk present can be identified.

This area calls for high risk.

High Risk As this area

consists of

high risk, the

auditor needs

to follow a

diagnostic

procedure

where the

figures of the

last years

should be

compared and

an analysis be

done. the

reasonableness

in the sales

value needs to

6

be of moderate risk. observed for

vulnerabilities

Return on

total assets %

The percentage of return on total assets is said to depict the

percentage of the total amount of assets that are present in an

organization. For Always Precise Instruments Private Limited,

this percentage was budgeted to be at 16% but actually, the

company was able to maintain only 12.5%. When compared to

the last year's figure of 14.9%, it can be stated that there was an

observable decline which is not good for the organization. The

increase in current ratio and quick ratio is good for the

organization but if at the same time the return on assets is

decreasing then it is very inefficient for the organization. This

area should be studied carefully because the increase in current

assets should also lead to an increase in the return on total assets.

Hence, this area constitutes of moderate risk.

Moderate

Risk

As it

constitutes

moderate risk,

the auditor

should

perform

Analytical

procedure that

will help in

knowing the

real cause

behind the

drop in the

ratio of ROA.

Gross margin

%

The gross margin percentage of the gross profit percentage is the

total operating profit percentage of inventories which is

accounted for before non-trading and non-operating items. For

Always Precise Instruments Private Limited it was observed that

the gross profit percentage had declined miserably to 6.5% which

was budgeted to be 10.8% after analyzing the previous year’s

data which stated the value of gross margin percentage to be

10.3%. The organizational strategies of the company clearly

stated that they wanted to improvise the sales but it is not

valuable for the company if there is a decrease in the gross

margin percentage. Hence, this area calls for a detailed analysis

of the auditor so that it any kind of risk present can be identified.

This area calls for high risk.

High Risk As this area

consists of

high risk, the

auditor needs

to follow a

diagnostic

procedure

where the

figures of the

last years

should be

compared and

an analysis be

done. the

reasonableness

in the sales

value needs to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

be ascertained.

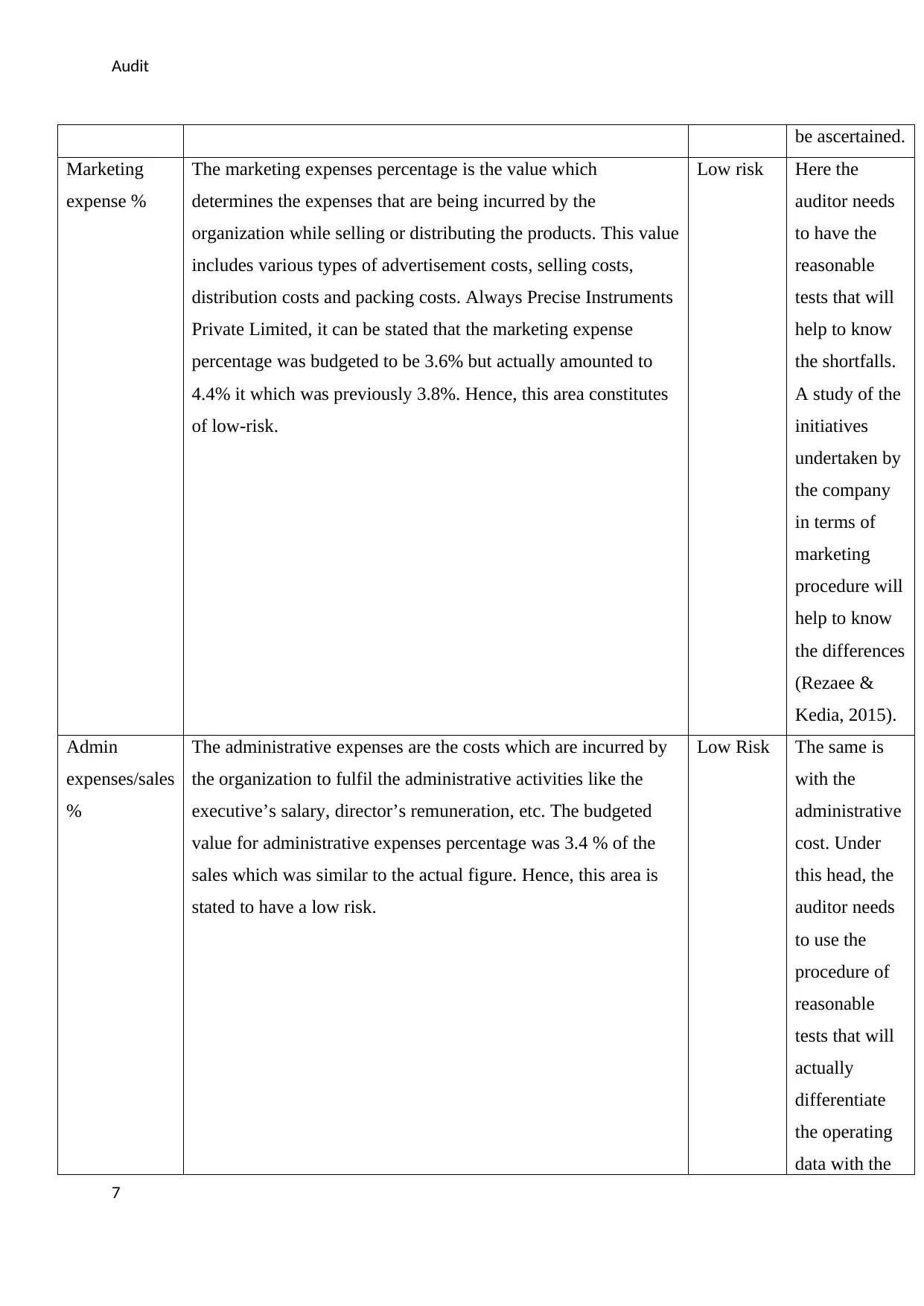

Marketing

expense %

The marketing expenses percentage is the value which

determines the expenses that are being incurred by the

organization while selling or distributing the products. This value

includes various types of advertisement costs, selling costs,

distribution costs and packing costs. Always Precise Instruments

Private Limited, it can be stated that the marketing expense

percentage was budgeted to be 3.6% but actually amounted to

4.4% it which was previously 3.8%. Hence, this area constitutes

of low-risk.

Low risk Here the

auditor needs

to have the

reasonable

tests that will

help to know

the shortfalls.

A study of the

initiatives

undertaken by

the company

in terms of

marketing

procedure will

help to know

the differences

(Rezaee &

Kedia, 2015).

Admin

expenses/sales

%

The administrative expenses are the costs which are incurred by

the organization to fulfil the administrative activities like the

executive’s salary, director’s remuneration, etc. The budgeted

value for administrative expenses percentage was 3.4 % of the

sales which was similar to the actual figure. Hence, this area is

stated to have a low risk.

Low Risk The same is

with the

administrative

cost. Under

this head, the

auditor needs

to use the

procedure of

reasonable

tests that will

actually

differentiate

the operating

data with the

7

be ascertained.

Marketing

expense %

The marketing expenses percentage is the value which

determines the expenses that are being incurred by the

organization while selling or distributing the products. This value

includes various types of advertisement costs, selling costs,

distribution costs and packing costs. Always Precise Instruments

Private Limited, it can be stated that the marketing expense

percentage was budgeted to be 3.6% but actually amounted to

4.4% it which was previously 3.8%. Hence, this area constitutes

of low-risk.

Low risk Here the

auditor needs

to have the

reasonable

tests that will

help to know

the shortfalls.

A study of the

initiatives

undertaken by

the company

in terms of

marketing

procedure will

help to know

the differences

(Rezaee &

Kedia, 2015).

Admin

expenses/sales

%

The administrative expenses are the costs which are incurred by

the organization to fulfil the administrative activities like the

executive’s salary, director’s remuneration, etc. The budgeted

value for administrative expenses percentage was 3.4 % of the

sales which was similar to the actual figure. Hence, this area is

stated to have a low risk.

Low Risk The same is

with the

administrative

cost. Under

this head, the

auditor needs

to use the

procedure of

reasonable

tests that will

actually

differentiate

the operating

data with the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

one that is

attained

(Roach, 2010).

Times interest

earned

The times of interest earned amounted to 3.6 times which was

budgeted to be at a level of 6.3 Times. Previously, in the last year

figures, it was 4.6 times while the industry average is stated to be

at 4.2. Therefore, this can be a very important cause that can

reduce profits and increase the debts of the organization. Hence,

this area constitutes a high risk (Parrino, Kidwell & Bates,

2012).

High risk As it is an area

of high risk

the auditor

should use the

analytical

procedure that

will help in

knowing the

changes that

happened in

the times

interest earned

and to trace

the weakness

in the area.

Days in

inventory

The number of days for which the inventory was on hold was

also observed to increase to 34.9 against the budgeted level of

previously in the last year figures this amounted to 32.9. Hence,

this area is suggested to have a low risk.

Low risk The trend

analysis can

be used by the

auditor to

understand

why the days

in inventory

increased

(Peirson et. al,

2015).

Days in

accounts

receivable

A total number of days for which the account receivables were

observed are 53 while the deposited level was 49.8 days. The

industry average for this is supposed to be 46.9. For Always

Precise Instruments Private Limited, total debt collection is very

High risk The auditor

should assess

a trend line of

bad debt

8

one that is

attained

(Roach, 2010).

Times interest

earned

The times of interest earned amounted to 3.6 times which was

budgeted to be at a level of 6.3 Times. Previously, in the last year

figures, it was 4.6 times while the industry average is stated to be

at 4.2. Therefore, this can be a very important cause that can

reduce profits and increase the debts of the organization. Hence,

this area constitutes a high risk (Parrino, Kidwell & Bates,

2012).

High risk As it is an area

of high risk

the auditor

should use the

analytical

procedure that

will help in

knowing the

changes that

happened in

the times

interest earned

and to trace

the weakness

in the area.

Days in

inventory

The number of days for which the inventory was on hold was

also observed to increase to 34.9 against the budgeted level of

previously in the last year figures this amounted to 32.9. Hence,

this area is suggested to have a low risk.

Low risk The trend

analysis can

be used by the

auditor to

understand

why the days

in inventory

increased

(Peirson et. al,

2015).

Days in

accounts

receivable

A total number of days for which the account receivables were

observed are 53 while the deposited level was 49.8 days. The

industry average for this is supposed to be 46.9. For Always

Precise Instruments Private Limited, total debt collection is very

High risk The auditor

should assess

a trend line of

bad debt

8

Audit

ineffective in value and hence is unable to meet the budgeted

efficiency levels. Hence, this area requires special attention of

the auditor. Therefore, this area is suggested to have high risk.

expenses and

the amount

should depict

a relation with

sales. If that

does not

happen then it

might be a

wrong practice

by the

management.

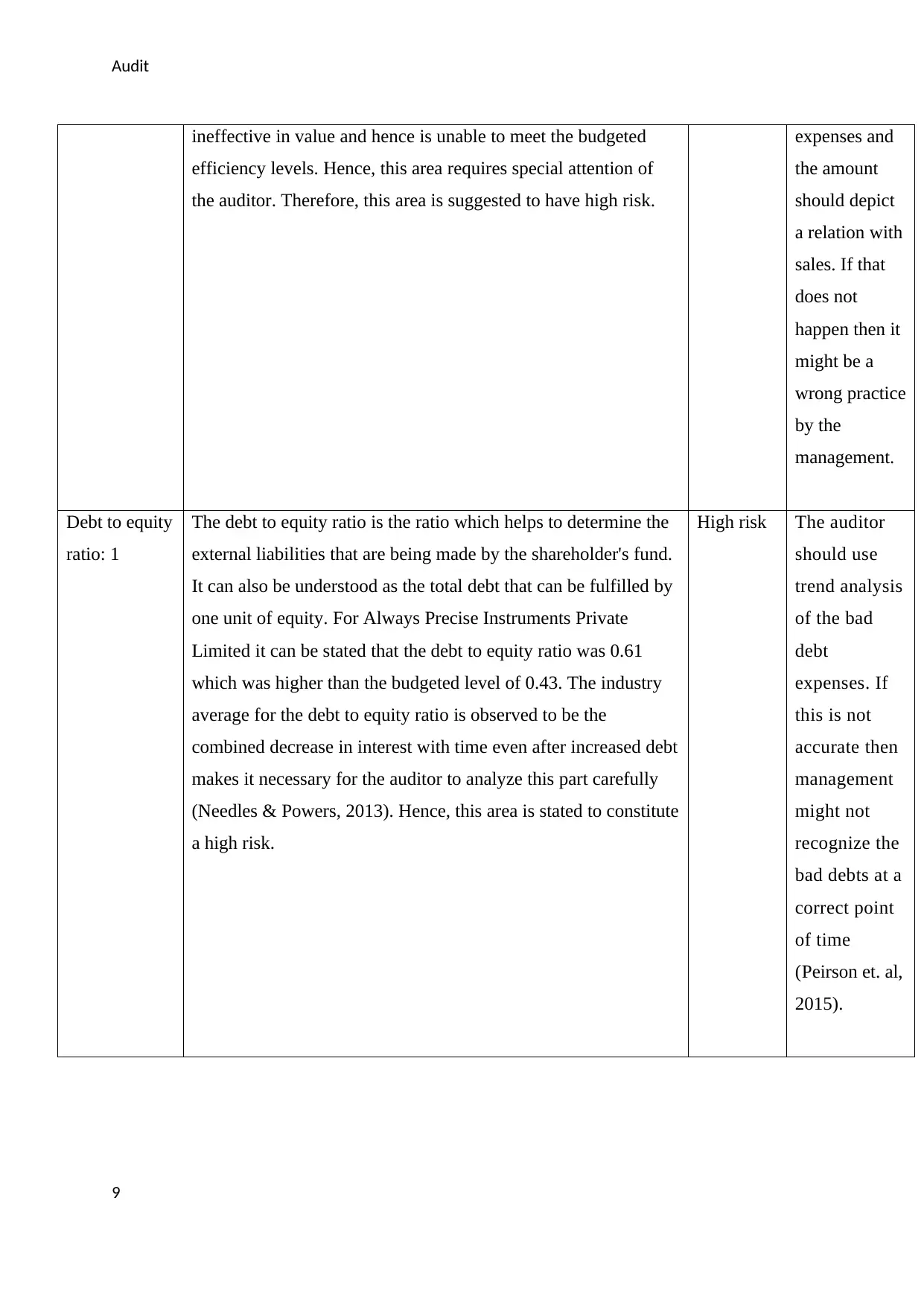

Debt to equity

ratio: 1

The debt to equity ratio is the ratio which helps to determine the

external liabilities that are being made by the shareholder's fund.

It can also be understood as the total debt that can be fulfilled by

one unit of equity. For Always Precise Instruments Private

Limited it can be stated that the debt to equity ratio was 0.61

which was higher than the budgeted level of 0.43. The industry

average for the debt to equity ratio is observed to be the

combined decrease in interest with time even after increased debt

makes it necessary for the auditor to analyze this part carefully

(Needles & Powers, 2013). Hence, this area is stated to constitute

a high risk.

High risk The auditor

should use

trend analysis

of the bad

debt

expenses. If

this is not

accurate then

management

might not

recognize the

bad debts at a

correct point

of time

(Peirson et. al,

2015).

9

ineffective in value and hence is unable to meet the budgeted

efficiency levels. Hence, this area requires special attention of

the auditor. Therefore, this area is suggested to have high risk.

expenses and

the amount

should depict

a relation with

sales. If that

does not

happen then it

might be a

wrong practice

by the

management.

Debt to equity

ratio: 1

The debt to equity ratio is the ratio which helps to determine the

external liabilities that are being made by the shareholder's fund.

It can also be understood as the total debt that can be fulfilled by

one unit of equity. For Always Precise Instruments Private

Limited it can be stated that the debt to equity ratio was 0.61

which was higher than the budgeted level of 0.43. The industry

average for the debt to equity ratio is observed to be the

combined decrease in interest with time even after increased debt

makes it necessary for the auditor to analyze this part carefully

(Needles & Powers, 2013). Hence, this area is stated to constitute

a high risk.

High risk The auditor

should use

trend analysis

of the bad

debt

expenses. If

this is not

accurate then

management

might not

recognize the

bad debts at a

correct point

of time

(Peirson et. al,

2015).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit

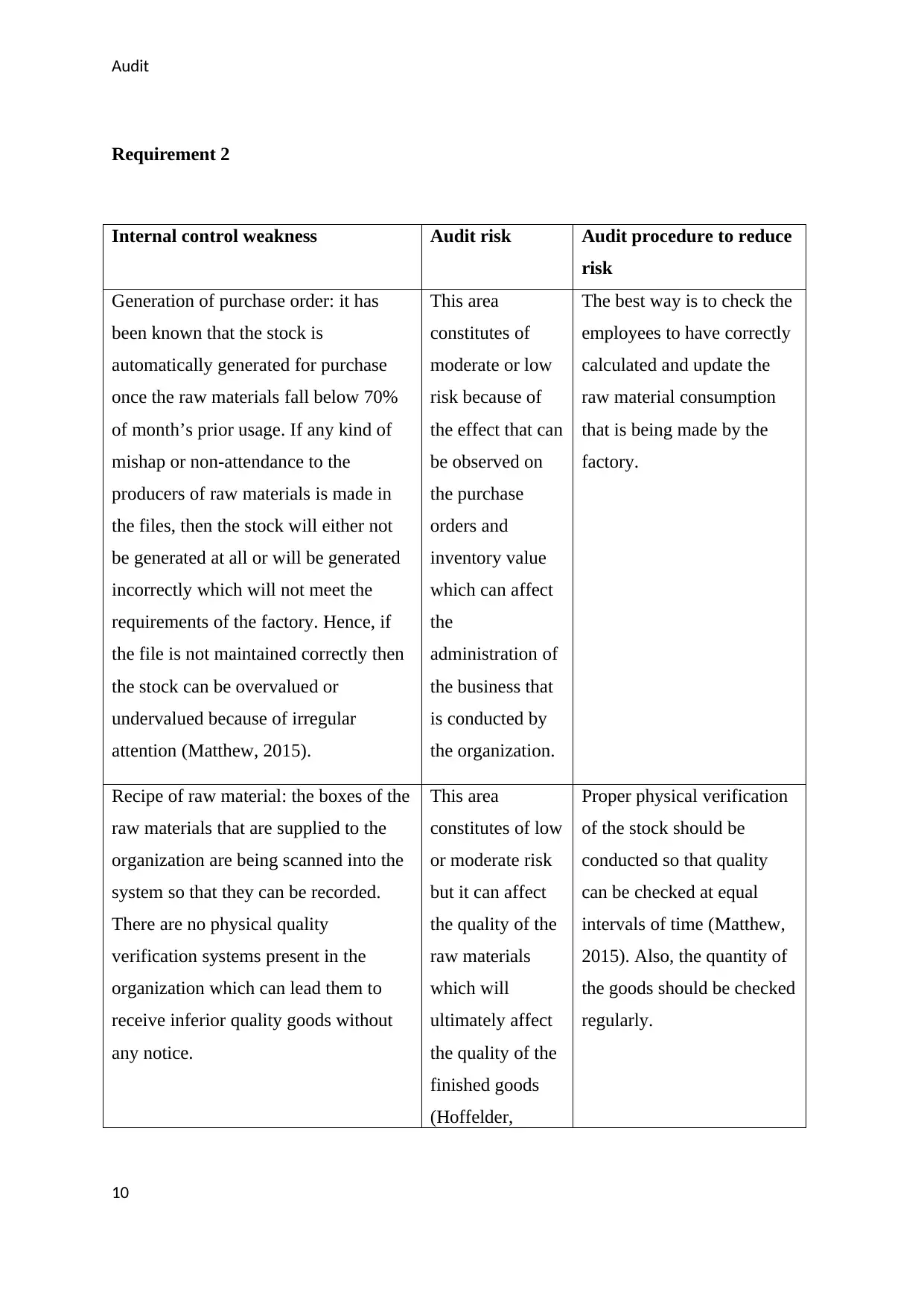

Requirement 2

Internal control weakness Audit risk Audit procedure to reduce

risk

Generation of purchase order: it has

been known that the stock is

automatically generated for purchase

once the raw materials fall below 70%

of month’s prior usage. If any kind of

mishap or non-attendance to the

producers of raw materials is made in

the files, then the stock will either not

be generated at all or will be generated

incorrectly which will not meet the

requirements of the factory. Hence, if

the file is not maintained correctly then

the stock can be overvalued or

undervalued because of irregular

attention (Matthew, 2015).

This area

constitutes of

moderate or low

risk because of

the effect that can

be observed on

the purchase

orders and

inventory value

which can affect

the

administration of

the business that

is conducted by

the organization.

The best way is to check the

employees to have correctly

calculated and update the

raw material consumption

that is being made by the

factory.

Recipe of raw material: the boxes of the

raw materials that are supplied to the

organization are being scanned into the

system so that they can be recorded.

There are no physical quality

verification systems present in the

organization which can lead them to

receive inferior quality goods without

any notice.

This area

constitutes of low

or moderate risk

but it can affect

the quality of the

raw materials

which will

ultimately affect

the quality of the

finished goods

(Hoffelder,

Proper physical verification

of the stock should be

conducted so that quality

can be checked at equal

intervals of time (Matthew,

2015). Also, the quantity of

the goods should be checked

regularly.

10

Requirement 2

Internal control weakness Audit risk Audit procedure to reduce

risk

Generation of purchase order: it has

been known that the stock is

automatically generated for purchase

once the raw materials fall below 70%

of month’s prior usage. If any kind of

mishap or non-attendance to the

producers of raw materials is made in

the files, then the stock will either not

be generated at all or will be generated

incorrectly which will not meet the

requirements of the factory. Hence, if

the file is not maintained correctly then

the stock can be overvalued or

undervalued because of irregular

attention (Matthew, 2015).

This area

constitutes of

moderate or low

risk because of

the effect that can

be observed on

the purchase

orders and

inventory value

which can affect

the

administration of

the business that

is conducted by

the organization.

The best way is to check the

employees to have correctly

calculated and update the

raw material consumption

that is being made by the

factory.

Recipe of raw material: the boxes of the

raw materials that are supplied to the

organization are being scanned into the

system so that they can be recorded.

There are no physical quality

verification systems present in the

organization which can lead them to

receive inferior quality goods without

any notice.

This area

constitutes of low

or moderate risk

but it can affect

the quality of the

raw materials

which will

ultimately affect

the quality of the

finished goods

(Hoffelder,

Proper physical verification

of the stock should be

conducted so that quality

can be checked at equal

intervals of time (Matthew,

2015). Also, the quantity of

the goods should be checked

regularly.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

2012).

Lack of emergency inventory options:

internal control system of the

organization is said to have options for

emergency inventory. There can be

situations where the supplier is not able

to fulfil the demand of the raw material

required by the organization and at the

same time, the inventory at the

warehouse exhausted. This can lead to a

situation where the company may face

huge loss because of the exhausted

stock aero material (Gay & Simnet,

2015).

High or moderate

risk is involved

because this can

affect the value

of the inventory

is direct because

of which the

administration of

business can be

hampered.

The emergency stock level

should always be maintained

in order to prevent the

organization from future

problems.

Production of finished goods- the order

is generated after the total value of the

finished goods fall below 60% of the

previous month sales. There may be

situations where the demand may arise

and certainly because of which the need

for finished goods will arise. And the

company may not be able to accept such

unnatural big order.

This area

constitutes of

high or moderate

risk because it

can affect the

sales department

of the

organization

drastically.

The production controller

should always be ready for

the generation of production

orders so that the future of

the organization can be kept

secured (Geoffrey, Joleen,

Kelli & David, 2016). The

production controller should

also keep in mind the auto-

generation of the production

order.

The production orders are observed to

be sent only to the raw material store so

as to pick up the slips that are to be

filled up by the production controllers.

The third copy should also be generated

so as to keep it in the stores as a record

of the finished goods. This will help the

This area

constitutes of low

risk and does not

affect the

administration of

business at large

Three copies of the

production order should be

made in order to keep the

proper required of the

finished goods. The first

copy should be handed over

to the raw materials to II to

11

2012).

Lack of emergency inventory options:

internal control system of the

organization is said to have options for

emergency inventory. There can be

situations where the supplier is not able

to fulfil the demand of the raw material

required by the organization and at the

same time, the inventory at the

warehouse exhausted. This can lead to a

situation where the company may face

huge loss because of the exhausted

stock aero material (Gay & Simnet,

2015).

High or moderate

risk is involved

because this can

affect the value

of the inventory

is direct because

of which the

administration of

business can be

hampered.

The emergency stock level

should always be maintained

in order to prevent the

organization from future

problems.

Production of finished goods- the order

is generated after the total value of the

finished goods fall below 60% of the

previous month sales. There may be

situations where the demand may arise

and certainly because of which the need

for finished goods will arise. And the

company may not be able to accept such

unnatural big order.

This area

constitutes of

high or moderate

risk because it

can affect the

sales department

of the

organization

drastically.

The production controller

should always be ready for

the generation of production

orders so that the future of

the organization can be kept

secured (Geoffrey, Joleen,

Kelli & David, 2016). The

production controller should

also keep in mind the auto-

generation of the production

order.

The production orders are observed to

be sent only to the raw material store so

as to pick up the slips that are to be

filled up by the production controllers.

The third copy should also be generated

so as to keep it in the stores as a record

of the finished goods. This will help the

This area

constitutes of low

risk and does not

affect the

administration of

business at large

Three copies of the

production order should be

made in order to keep the

proper required of the

finished goods. The first

copy should be handed over

to the raw materials to II to

11

Audit

store manager to know the expected

delivery date of the next lot of finished

goods so that he could manage stock in

his department accordingly.

scale. the department head and the

third to the general

administrator of the business

so that a clear and

transparent view can be

created.

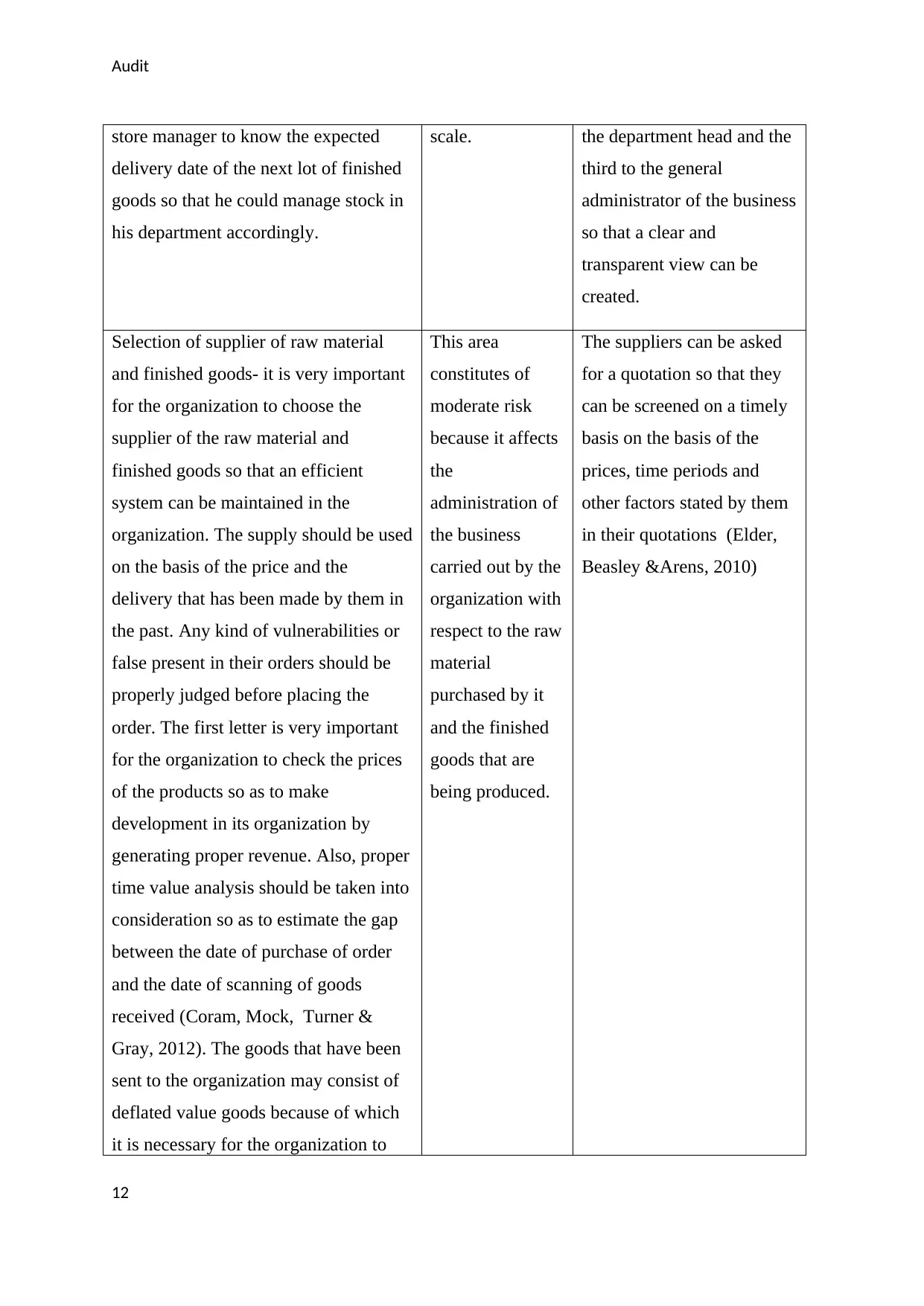

Selection of supplier of raw material

and finished goods- it is very important

for the organization to choose the

supplier of the raw material and

finished goods so that an efficient

system can be maintained in the

organization. The supply should be used

on the basis of the price and the

delivery that has been made by them in

the past. Any kind of vulnerabilities or

false present in their orders should be

properly judged before placing the

order. The first letter is very important

for the organization to check the prices

of the products so as to make

development in its organization by

generating proper revenue. Also, proper

time value analysis should be taken into

consideration so as to estimate the gap

between the date of purchase of order

and the date of scanning of goods

received (Coram, Mock, Turner &

Gray, 2012). The goods that have been

sent to the organization may consist of

deflated value goods because of which

it is necessary for the organization to

This area

constitutes of

moderate risk

because it affects

the

administration of

the business

carried out by the

organization with

respect to the raw

material

purchased by it

and the finished

goods that are

being produced.

The suppliers can be asked

for a quotation so that they

can be screened on a timely

basis on the basis of the

prices, time periods and

other factors stated by them

in their quotations (Elder,

Beasley &Arens, 2010)

12

store manager to know the expected

delivery date of the next lot of finished

goods so that he could manage stock in

his department accordingly.

scale. the department head and the

third to the general

administrator of the business

so that a clear and

transparent view can be

created.

Selection of supplier of raw material

and finished goods- it is very important

for the organization to choose the

supplier of the raw material and

finished goods so that an efficient

system can be maintained in the

organization. The supply should be used

on the basis of the price and the

delivery that has been made by them in

the past. Any kind of vulnerabilities or

false present in their orders should be

properly judged before placing the

order. The first letter is very important

for the organization to check the prices

of the products so as to make

development in its organization by

generating proper revenue. Also, proper

time value analysis should be taken into

consideration so as to estimate the gap

between the date of purchase of order

and the date of scanning of goods

received (Coram, Mock, Turner &

Gray, 2012). The goods that have been

sent to the organization may consist of

deflated value goods because of which

it is necessary for the organization to

This area

constitutes of

moderate risk

because it affects

the

administration of

the business

carried out by the

organization with

respect to the raw

material

purchased by it

and the finished

goods that are

being produced.

The suppliers can be asked

for a quotation so that they

can be screened on a timely

basis on the basis of the

prices, time periods and

other factors stated by them

in their quotations (Elder,

Beasley &Arens, 2010)

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.