CQUniversity ACCT20075: Audit Report Analysis and Findings

VerifiedAdded on 2022/09/18

|13

|2576

|28

Report

AI Summary

This report provides an in-depth analysis of an audit report, focusing on the key elements of the audit process for a chosen listed company (I Shares). The report begins by exploring the concept of materiality and its scope within the audit, calculating planning materiality, and reviewing company disclosures. It then delves into the application of analytical procedures, examining various financial ratios to assess the company's financial performance. The analysis extends to the company's cash flow statement, highlighting its importance in understanding the financial health of the business. Finally, the report concludes with a review of the annual report, including the auditor's opinion and the application of auditing standards. The report emphasizes the auditor's role in ensuring accurate financial reporting and adherence to accounting standards. It also considers the application of analytical procedures to determine the key financial objectives and how they help the auditor gain proper knowledge of company financial statements.

Running head: AUDIT

AUDIT

Name of the Student

Name of the University

Author Note

AUDIT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality and Scope of Audit..............................................................................................2

Review of Company Disclosures...........................................................................................4

Section 2.....................................................................................................................................4

Application of Analytical Procedure......................................................................................4

Section 3.....................................................................................................................................6

Analysis of company cash flow.............................................................................................6

Review Annual Report...........................................................................................................6

Conclusion..................................................................................................................................7

AUDIT

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality and Scope of Audit..............................................................................................2

Review of Company Disclosures...........................................................................................4

Section 2.....................................................................................................................................4

Application of Analytical Procedure......................................................................................4

Section 3.....................................................................................................................................6

Analysis of company cash flow.............................................................................................6

Review Annual Report...........................................................................................................6

Conclusion..................................................................................................................................7

2

AUDIT

AUDIT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT

Introduction

Each company have to make proper accounting information so that the user will able

to get accurate information about the company financial statement. Company having proper

knowledge of presenting the information in company financial statement is check by the

process of audit1. The auditor is the one who inspect the financial statement properly so that it

can know whether the company is able to meet all the accounting standard or not. The

company should able to make proper adjustment in the business so it can show all the related

information about the company business in their financial statement. The report deals with

the company name I shares which is the family of exchange-traded fund and managed by

Black Rock. The report show different aspects of the company in regards of audit and how

the auditor is able to meet the requirement process of auditing in company financial

business2. Auditor should able to analysis all the company aspects so that it can get proper

detail of company financial statement so that the auditor is able to give proper opinion upon

the company financial statement.

Section 1

Materiality and Scope of Audit

The objective of these report to show the materiality and scope of audit about the

company I Shares3. The company financial report is been consider to carry the audit process

1 Alzeban, Abdulaziz, and David Gwilliam. "Factors affecting the internal audit effectiveness: A survey of the

Saudi public sector." Journal of International Accounting, Auditing and Taxation 23.2 (2014): 74-86.

2 Arena, Marika, and Kim Klarskov Jeppesen. "Practice variation in public sector internal

auditing: an institutional analysis." European Accounting Review 25.2 (2016): 319-345.

3 Baharud-din, Zulkifli, Alagan Shokiyah, and Mohd Serjana Ibrahim. "Factors that

contribute to the effectiveness of internal audit in public sector." International Proceedings

of Economics Development and Research 70 (2014): 126.

AUDIT

Introduction

Each company have to make proper accounting information so that the user will able

to get accurate information about the company financial statement. Company having proper

knowledge of presenting the information in company financial statement is check by the

process of audit1. The auditor is the one who inspect the financial statement properly so that it

can know whether the company is able to meet all the accounting standard or not. The

company should able to make proper adjustment in the business so it can show all the related

information about the company business in their financial statement. The report deals with

the company name I shares which is the family of exchange-traded fund and managed by

Black Rock. The report show different aspects of the company in regards of audit and how

the auditor is able to meet the requirement process of auditing in company financial

business2. Auditor should able to analysis all the company aspects so that it can get proper

detail of company financial statement so that the auditor is able to give proper opinion upon

the company financial statement.

Section 1

Materiality and Scope of Audit

The objective of these report to show the materiality and scope of audit about the

company I Shares3. The company financial report is been consider to carry the audit process

1 Alzeban, Abdulaziz, and David Gwilliam. "Factors affecting the internal audit effectiveness: A survey of the

Saudi public sector." Journal of International Accounting, Auditing and Taxation 23.2 (2014): 74-86.

2 Arena, Marika, and Kim Klarskov Jeppesen. "Practice variation in public sector internal

auditing: an institutional analysis." European Accounting Review 25.2 (2016): 319-345.

3 Baharud-din, Zulkifli, Alagan Shokiyah, and Mohd Serjana Ibrahim. "Factors that

contribute to the effectiveness of internal audit in public sector." International Proceedings

of Economics Development and Research 70 (2014): 126.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT

and to check whether the report is having any kind of materiality in the business or not. The

report is focusing upon the overall materiality in company business. Auditor have tom

ascertain the materiality attached with company statement as this help the auditor to gain

proper knowledge about the company financial statement. It help the auditor to ascertain the

audit process more easily in the company as if the company is having high amount of

materiality than the auditor have to ascertain proper process in regards of company financial

statement4. This also help the auditor to gather the audit evidence in the company financial

statement and help them to give proper opinion about the company financial statement in the

business. The auditor have to check each item in company financial statement so that t can

ascertain materiality in company business.

Auditor have to plan the materiality associated in company financial statement so that

it can plan the audit process keeping the materiality concept base upon it. It have to check all

the details of company information so it can know that the company is able to have true and

fair view or not. The first thing which the auditor have to do is to calculate the planning

materiality in the company financial statement. This is purely based on the judgement which

is taken by the auditor in regards of company financial statement as the auditor had to

estimate the same in company so that it will able to have proper analysis of the same in

company financial statement5. It basically depend on company transaction as it is based on

total asset, equity and sale of the company. The planning materiality is basically based upon

4 DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

5 Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing

a Company's Personality. Routledge, 2015.

AUDIT

and to check whether the report is having any kind of materiality in the business or not. The

report is focusing upon the overall materiality in company business. Auditor have tom

ascertain the materiality attached with company statement as this help the auditor to gain

proper knowledge about the company financial statement. It help the auditor to ascertain the

audit process more easily in the company as if the company is having high amount of

materiality than the auditor have to ascertain proper process in regards of company financial

statement4. This also help the auditor to gather the audit evidence in the company financial

statement and help them to give proper opinion about the company financial statement in the

business. The auditor have to check each item in company financial statement so that t can

ascertain materiality in company business.

Auditor have to plan the materiality associated in company financial statement so that

it can plan the audit process keeping the materiality concept base upon it. It have to check all

the details of company information so it can know that the company is able to have true and

fair view or not. The first thing which the auditor have to do is to calculate the planning

materiality in the company financial statement. This is purely based on the judgement which

is taken by the auditor in regards of company financial statement as the auditor had to

estimate the same in company so that it will able to have proper analysis of the same in

company financial statement5. It basically depend on company transaction as it is based on

total asset, equity and sale of the company. The planning materiality is basically based upon

4 DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

5 Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing

a Company's Personality. Routledge, 2015.

5

AUDIT

the highest amount of above mention items so as per the company financial statement the

value of total asset is the highest in the company financial statement so the total asset in 2018

was $407798880 on which planning materiality calculation is computed. The planning

materality calculation is show below:

Planning Materiality=Total Asset∗5 %

¿ $ 4.077 .98880 .000

¿ 5 %

¿ $ 20,289,944

The above calculation shows that about the company planning materiality in the

business. The planning materiality in the business is $20,289,944 on that the auditor will able

to plan the performance of company materiality and able to carry different audit procedure in

the company financial statement. These will help the auditor to take all the necessary

estimation in regards of company financial statement and how the company should able to

deal with materiality in their financial statement.

Review of Company Disclosures

The company annual report should able to have proper amount of disclosure in the

company financial statement so that this will help the company to know all the details in the

company financial statement 6. This should be properly analysed by the company so that it

will able to know the materiality aspects more properly in the business.

The company is an investment company so it is necessary for the company to consider

all the investment details in the business so this will help the company to gain proper

6 Griffiths, Phil. Risk-based auditing. Routledge, 2016.

AUDIT

the highest amount of above mention items so as per the company financial statement the

value of total asset is the highest in the company financial statement so the total asset in 2018

was $407798880 on which planning materiality calculation is computed. The planning

materality calculation is show below:

Planning Materiality=Total Asset∗5 %

¿ $ 4.077 .98880 .000

¿ 5 %

¿ $ 20,289,944

The above calculation shows that about the company planning materiality in the

business. The planning materiality in the business is $20,289,944 on that the auditor will able

to plan the performance of company materiality and able to carry different audit procedure in

the company financial statement. These will help the auditor to take all the necessary

estimation in regards of company financial statement and how the company should able to

deal with materiality in their financial statement.

Review of Company Disclosures

The company annual report should able to have proper amount of disclosure in the

company financial statement so that this will help the company to know all the details in the

company financial statement 6. This should be properly analysed by the company so that it

will able to know the materiality aspects more properly in the business.

The company is an investment company so it is necessary for the company to consider

all the investment details in the business so this will help the company to gain proper

6 Griffiths, Phil. Risk-based auditing. Routledge, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT

advantage in the business. Auditor should able to have proper analysis of the company

investment which will it to know how the company is able to carry its business activities in

the business.

Section 2

Application of Analytical Procedure

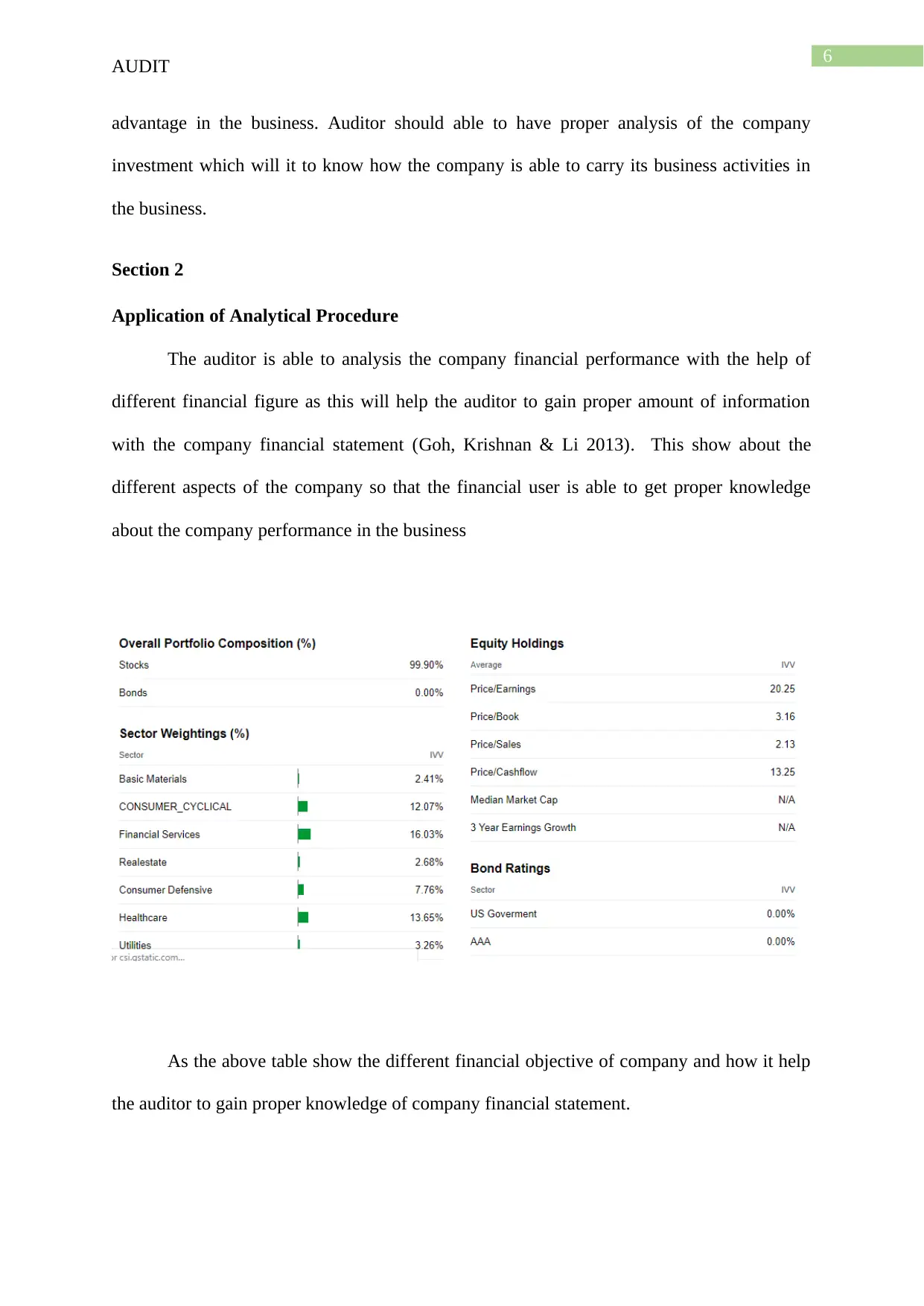

The auditor is able to analysis the company financial performance with the help of

different financial figure as this will help the auditor to gain proper amount of information

with the company financial statement (Goh, Krishnan & Li 2013). This show about the

different aspects of the company so that the financial user is able to get proper knowledge

about the company performance in the business

As the above table show the different financial objective of company and how it help

the auditor to gain proper knowledge of company financial statement.

AUDIT

advantage in the business. Auditor should able to have proper analysis of the company

investment which will it to know how the company is able to carry its business activities in

the business.

Section 2

Application of Analytical Procedure

The auditor is able to analysis the company financial performance with the help of

different financial figure as this will help the auditor to gain proper amount of information

with the company financial statement (Goh, Krishnan & Li 2013). This show about the

different aspects of the company so that the financial user is able to get proper knowledge

about the company performance in the business

As the above table show the different financial objective of company and how it help

the auditor to gain proper knowledge of company financial statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT

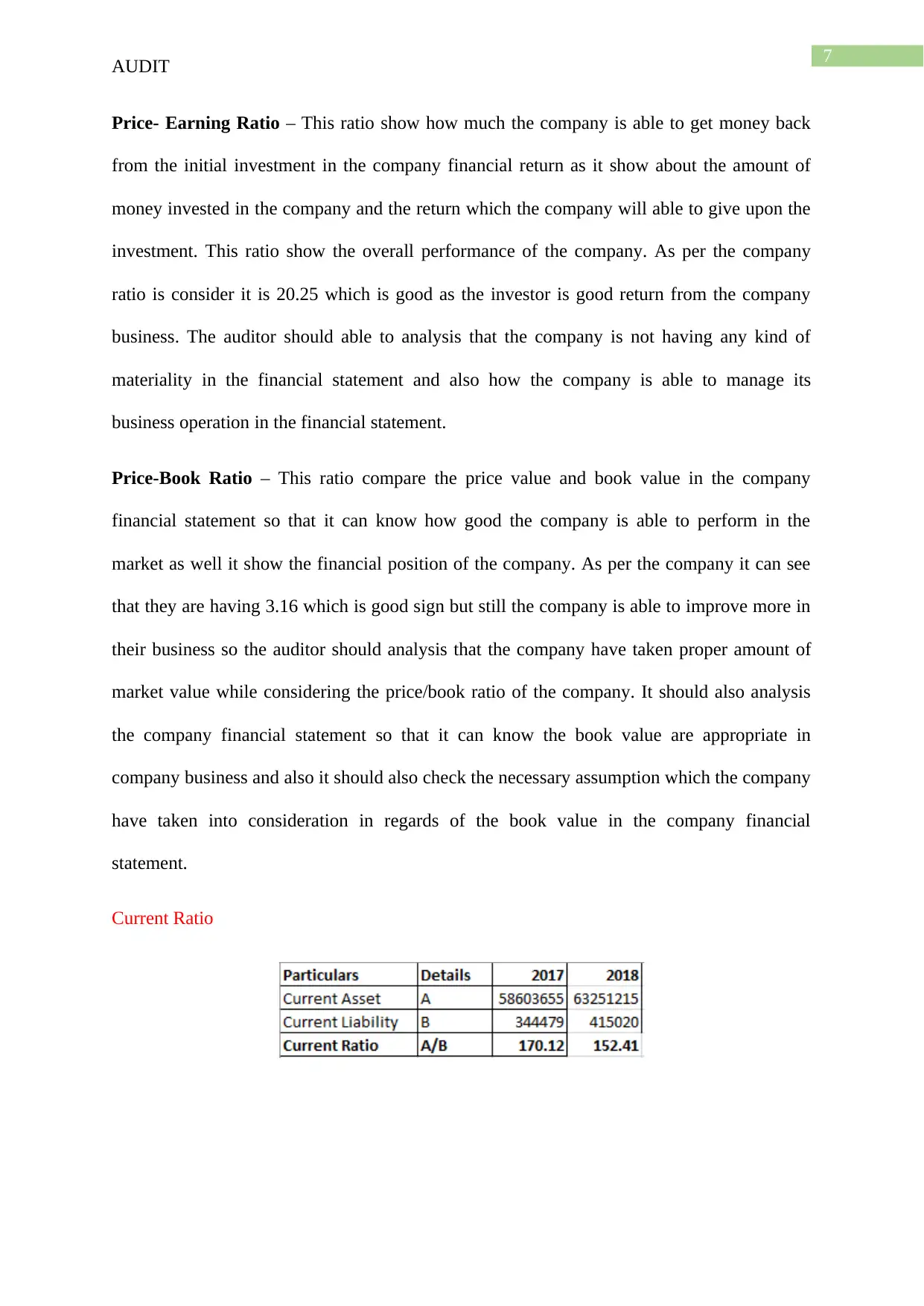

Price- Earning Ratio – This ratio show how much the company is able to get money back

from the initial investment in the company financial return as it show about the amount of

money invested in the company and the return which the company will able to give upon the

investment. This ratio show the overall performance of the company. As per the company

ratio is consider it is 20.25 which is good as the investor is good return from the company

business. The auditor should able to analysis that the company is not having any kind of

materiality in the financial statement and also how the company is able to manage its

business operation in the financial statement.

Price-Book Ratio – This ratio compare the price value and book value in the company

financial statement so that it can know how good the company is able to perform in the

market as well it show the financial position of the company. As per the company it can see

that they are having 3.16 which is good sign but still the company is able to improve more in

their business so the auditor should analysis that the company have taken proper amount of

market value while considering the price/book ratio of the company. It should also analysis

the company financial statement so that it can know the book value are appropriate in

company business and also it should also check the necessary assumption which the company

have taken into consideration in regards of the book value in the company financial

statement.

Current Ratio

AUDIT

Price- Earning Ratio – This ratio show how much the company is able to get money back

from the initial investment in the company financial return as it show about the amount of

money invested in the company and the return which the company will able to give upon the

investment. This ratio show the overall performance of the company. As per the company

ratio is consider it is 20.25 which is good as the investor is good return from the company

business. The auditor should able to analysis that the company is not having any kind of

materiality in the financial statement and also how the company is able to manage its

business operation in the financial statement.

Price-Book Ratio – This ratio compare the price value and book value in the company

financial statement so that it can know how good the company is able to perform in the

market as well it show the financial position of the company. As per the company it can see

that they are having 3.16 which is good sign but still the company is able to improve more in

their business so the auditor should analysis that the company have taken proper amount of

market value while considering the price/book ratio of the company. It should also analysis

the company financial statement so that it can know the book value are appropriate in

company business and also it should also check the necessary assumption which the company

have taken into consideration in regards of the book value in the company financial

statement.

Current Ratio

8

AUDIT

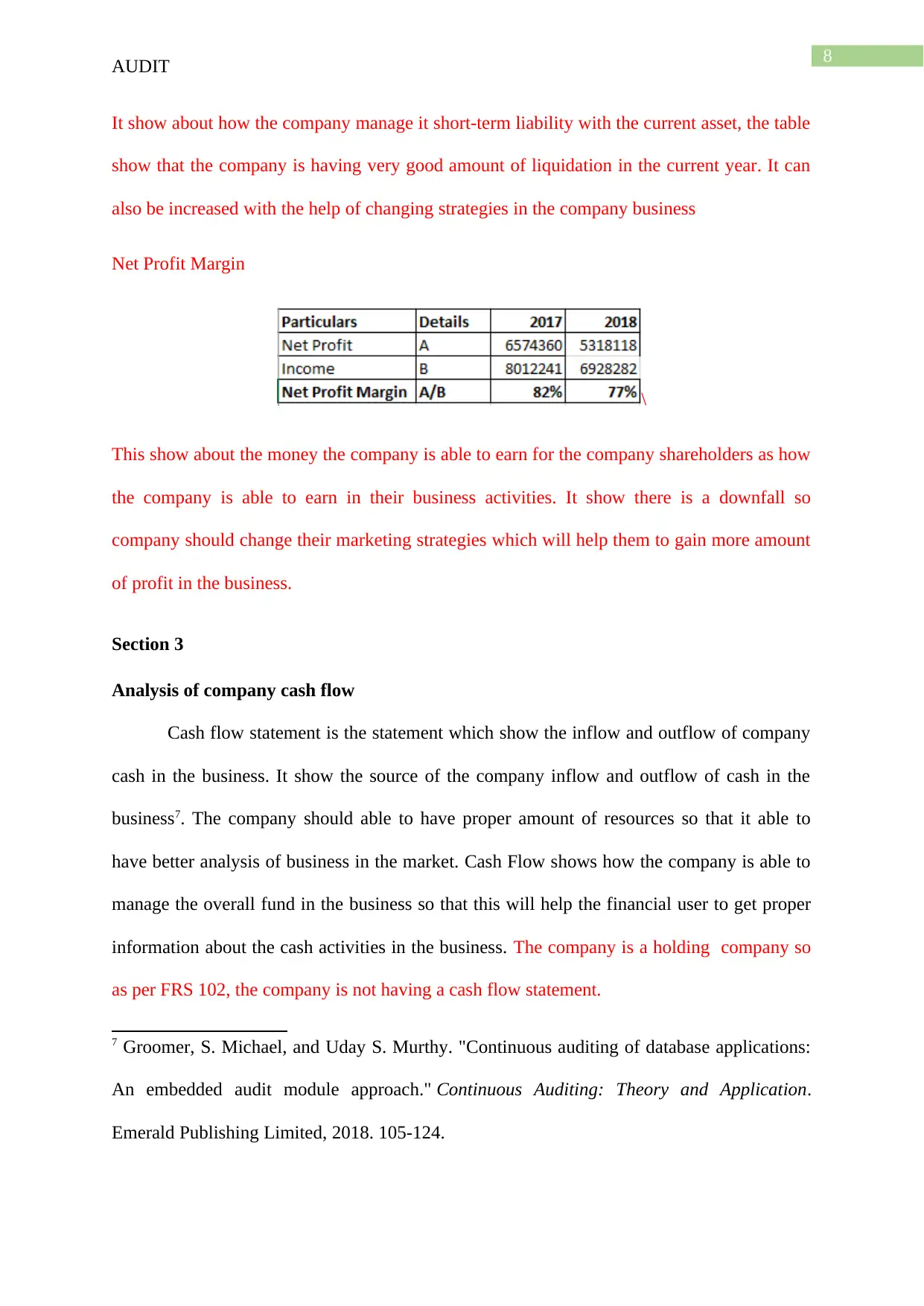

It show about how the company manage it short-term liability with the current asset, the table

show that the company is having very good amount of liquidation in the current year. It can

also be increased with the help of changing strategies in the company business

Net Profit Margin

\

This show about the money the company is able to earn for the company shareholders as how

the company is able to earn in their business activities. It show there is a downfall so

company should change their marketing strategies which will help them to gain more amount

of profit in the business.

Section 3

Analysis of company cash flow

Cash flow statement is the statement which show the inflow and outflow of company

cash in the business. It show the source of the company inflow and outflow of cash in the

business7. The company should able to have proper amount of resources so that it able to

have better analysis of business in the market. Cash Flow shows how the company is able to

manage the overall fund in the business so that this will help the financial user to get proper

information about the cash activities in the business. The company is a holding company so

as per FRS 102, the company is not having a cash flow statement.

7 Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

AUDIT

It show about how the company manage it short-term liability with the current asset, the table

show that the company is having very good amount of liquidation in the current year. It can

also be increased with the help of changing strategies in the company business

Net Profit Margin

\

This show about the money the company is able to earn for the company shareholders as how

the company is able to earn in their business activities. It show there is a downfall so

company should change their marketing strategies which will help them to gain more amount

of profit in the business.

Section 3

Analysis of company cash flow

Cash flow statement is the statement which show the inflow and outflow of company

cash in the business. It show the source of the company inflow and outflow of cash in the

business7. The company should able to have proper amount of resources so that it able to

have better analysis of business in the market. Cash Flow shows how the company is able to

manage the overall fund in the business so that this will help the financial user to get proper

information about the cash activities in the business. The company is a holding company so

as per FRS 102, the company is not having a cash flow statement.

7 Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT

Company having proper cash flow signify that it able to have proper working capital

and able to carry its business operation easily and effectively. Company should able to

manage the inflow and outflow so that it have proper liquidity in the business. As the

company is finance based business so it will have more effect on cash from financing

activities rather than investing activities. Company should able to give proper analysis of

financial statement so that the user is able to get better knowledge of inflow and outflow of

cash. As the source of cash also help the user to know how the company is able to carry its

business activities. The source show the business activities in the company so this help to

invest properly in the company business.

Review Annual Report

Each company have to prepare annual report in the company so that the user will able

to get proper knowledge about the company financial statement. Company should able to

follow all the rules and regulation while preparing the financial statement of the business.

auditor have to do proper review of company financial statement so that it will help the

company user to know more about of company information in the business.

The auditor report show that the company is able to apply all the rules and regulation

in company financial statement so that this show that the company is having true and fair

view in the business. As per the auditor report it show that the auditing company have

followed all the rules and regulation in the procedure of carrying the audit process of the

financial statement.

The auditor stated that in the auditor report that they perform different activity to

know the risk of material mis-statement in the business. Material mis-statement are the error

and omission which the company have in their financial information so these show that the

company is able to have material misstatement in business. It also did the analysis of

AUDIT

Company having proper cash flow signify that it able to have proper working capital

and able to carry its business operation easily and effectively. Company should able to

manage the inflow and outflow so that it have proper liquidity in the business. As the

company is finance based business so it will have more effect on cash from financing

activities rather than investing activities. Company should able to give proper analysis of

financial statement so that the user is able to get better knowledge of inflow and outflow of

cash. As the source of cash also help the user to know how the company is able to carry its

business activities. The source show the business activities in the company so this help to

invest properly in the company business.

Review Annual Report

Each company have to prepare annual report in the company so that the user will able

to get proper knowledge about the company financial statement. Company should able to

follow all the rules and regulation while preparing the financial statement of the business.

auditor have to do proper review of company financial statement so that it will help the

company user to know more about of company information in the business.

The auditor report show that the company is able to apply all the rules and regulation

in company financial statement so that this show that the company is having true and fair

view in the business. As per the auditor report it show that the auditing company have

followed all the rules and regulation in the procedure of carrying the audit process of the

financial statement.

The auditor stated that in the auditor report that they perform different activity to

know the risk of material mis-statement in the business. Material mis-statement are the error

and omission which the company have in their financial information so these show that the

company is able to have material misstatement in business. It also did the analysis of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT

company fraud so that the company is able to have less amount of materiality. Company

estimation are also been analysis by the auditor that there been taken proper assumption in

company financial statement.

Key audit matters are not there in the company financial statement as these are the

matter which the auditor have to show in the annual report which show the risk that are been

associated in company financial statement.

Conclusion

The report concludes about the audit process in the company financial statement, the

auditor are the one who analysis the company financial statement and show that the company

is having proper formulation of accounting standard or not. Company should able to have

proper application of all the rules and regulation while preparation of company financial

statement. Auditor have to analysis all the company process so that it can know the ascertain

of company information so that it can give proper opinion in the financial statement. It

conclude about the company materiality aspects as it show that there is any misstatement in

the company financial statement. It also conclude about the financial ratio of the company so

that to show the performance of the company, as it help the auditor to ascertain the risk in the

company financial statement. Lastly the report conclude about the review of annual report as

it show how the company is able to have auditor report in the business. It show the opinion

which the auditor is able to give to the company as well as the procedure which the auditor

have to follow in regards of company financial statement.

AUDIT

company fraud so that the company is able to have less amount of materiality. Company

estimation are also been analysis by the auditor that there been taken proper assumption in

company financial statement.

Key audit matters are not there in the company financial statement as these are the

matter which the auditor have to show in the annual report which show the risk that are been

associated in company financial statement.

Conclusion

The report concludes about the audit process in the company financial statement, the

auditor are the one who analysis the company financial statement and show that the company

is having proper formulation of accounting standard or not. Company should able to have

proper application of all the rules and regulation while preparation of company financial

statement. Auditor have to analysis all the company process so that it can know the ascertain

of company information so that it can give proper opinion in the financial statement. It

conclude about the company materiality aspects as it show that there is any misstatement in

the company financial statement. It also conclude about the financial ratio of the company so

that to show the performance of the company, as it help the auditor to ascertain the risk in the

company financial statement. Lastly the report conclude about the review of annual report as

it show how the company is able to have auditor report in the business. It show the opinion

which the auditor is able to give to the company as well as the procedure which the auditor

have to follow in regards of company financial statement.

11

AUDIT

Reference and Bibliography

Alzeban, Abdulaziz, and David Gwilliam. "Factors affecting the internal audit effectiveness:

A survey of the Saudi public sector." Journal of International Accounting, Auditing and

Taxation 23.2 (2014): 74-86.

Arena, Marika, and Kim Klarskov Jeppesen. "Practice variation in public sector internal

auditing: an institutional analysis." European Accounting Review 25.2 (2016): 319-345.

Baharud-din, Zulkifli, Alagan Shokiyah, and Mohd Serjana Ibrahim. "Factors that contribute

to the effectiveness of internal audit in public sector." International Proceedings of

Economics Development and Research 70 (2014): 126.

DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge, 2015.

Griffiths, Phil. Risk-based auditing. Routledge, 2016.

Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

Hall, James A. Information technology auditing. Cengage Learning, 2015.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge, 2016.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge, 2016.

AUDIT

Reference and Bibliography

Alzeban, Abdulaziz, and David Gwilliam. "Factors affecting the internal audit effectiveness:

A survey of the Saudi public sector." Journal of International Accounting, Auditing and

Taxation 23.2 (2014): 74-86.

Arena, Marika, and Kim Klarskov Jeppesen. "Practice variation in public sector internal

auditing: an institutional analysis." European Accounting Review 25.2 (2016): 319-345.

Baharud-din, Zulkifli, Alagan Shokiyah, and Mohd Serjana Ibrahim. "Factors that contribute

to the effectiveness of internal audit in public sector." International Proceedings of

Economics Development and Research 70 (2014): 126.

DeFond, Mark, and Jieying Zhang. "A review of archival auditing research." Journal of

Accounting and Economics58.2-3 (2014): 275-326.

Furnham, Adrian, and Barrie Gunter. Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge, 2015.

Griffiths, Phil. Risk-based auditing. Routledge, 2016.

Groomer, S. Michael, and Uday S. Murthy. "Continuous auditing of database applications:

An embedded audit module approach." Continuous Auditing: Theory and Application.

Emerald Publishing Limited, 2018. 105-124.

Hall, James A. Information technology auditing. Cengage Learning, 2015.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge, 2016.

Knechel, W. Robert, and Steven E. Salterio. Auditing: Assurance and risk. Routledge, 2016.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.