Audit Report for DIPL

VerifiedAdded on 2020/03/01

|10

|2094

|40

Report

AI Summary

This report presents a comprehensive audit analysis for DIPL, focusing on financial statements, analytical procedures, inherent risks, and fraud risk factors. It discusses the implications of these factors on audit planning and decision-making, providing insights into the company's financial health and compliance with auditing standards.

Running head: AUDIT

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

AUDIT

Answer to Question 1

Applying analytical procedures to the financial information for DIPL for the last three

years

The Analytical procedures is conducted on the financial report of companies such as

DIPL are properly explained in this question. The development of plan for audit activities are

assisted by the financial reports of the company. While undertaking the audit function, the audit

plan which is used as a specific guideline should be followed strictly. It is very an important role

of the assessor that to check that costs of audit at a reasonable level. In addition to this, the

assessor must also assist in reducing the probability of misunderstanding with the customers. In

the financial declarations for the firm DIPL analytical process should be used this refers to the

broadcasting of such information which can be accessed from the financial declaration of the

business enterprise. By the utilization of a variety of mechanisms the given process are needed to

be evaluated. It is very important to study the financial declarations where several accountants

and financial analysts gather information that in turn assists in arriving at final decision-making

activities on using the analytical approach (Sarens 2015).

The main objective of analytical approach of common sizing is to evaluate the financial

declarations based on a common specific point. Further, it helps in comparing the financial

statement for a particular given period of time. Checking the type of reporting and to look after

the different line of items which are already mentioned in the financial report is an important

responsibility of the assessor. For example, it depends on the facts that how items are recorded

such as net assets, net liabilities which goes along with the equity of the owner as presented in

the financial reporting and also scrutinizing the detour after comparing with the normal activities.

Moreover, one of the important analytical procedure which are present during analyzing the plan

AUDIT

Answer to Question 1

Applying analytical procedures to the financial information for DIPL for the last three

years

The Analytical procedures is conducted on the financial report of companies such as

DIPL are properly explained in this question. The development of plan for audit activities are

assisted by the financial reports of the company. While undertaking the audit function, the audit

plan which is used as a specific guideline should be followed strictly. It is very an important role

of the assessor that to check that costs of audit at a reasonable level. In addition to this, the

assessor must also assist in reducing the probability of misunderstanding with the customers. In

the financial declarations for the firm DIPL analytical process should be used this refers to the

broadcasting of such information which can be accessed from the financial declaration of the

business enterprise. By the utilization of a variety of mechanisms the given process are needed to

be evaluated. It is very important to study the financial declarations where several accountants

and financial analysts gather information that in turn assists in arriving at final decision-making

activities on using the analytical approach (Sarens 2015).

The main objective of analytical approach of common sizing is to evaluate the financial

declarations based on a common specific point. Further, it helps in comparing the financial

statement for a particular given period of time. Checking the type of reporting and to look after

the different line of items which are already mentioned in the financial report is an important

responsibility of the assessor. For example, it depends on the facts that how items are recorded

such as net assets, net liabilities which goes along with the equity of the owner as presented in

the financial reporting and also scrutinizing the detour after comparing with the normal activities.

Moreover, one of the important analytical procedure which are present during analyzing the plan

3

AUDIT

of audit is benchmarking. Apart from this, deviation of original financial declaration from that of

the benchmark targets at identifying deviation and the reason for any detected variance for the

purpose of defining actual problem (Rao 2017).

Thus for assessing the plan of audit activities and essential analytical approach in order to

compare financial declarations, ratio analysis can be used as one of the important and effective

tool.

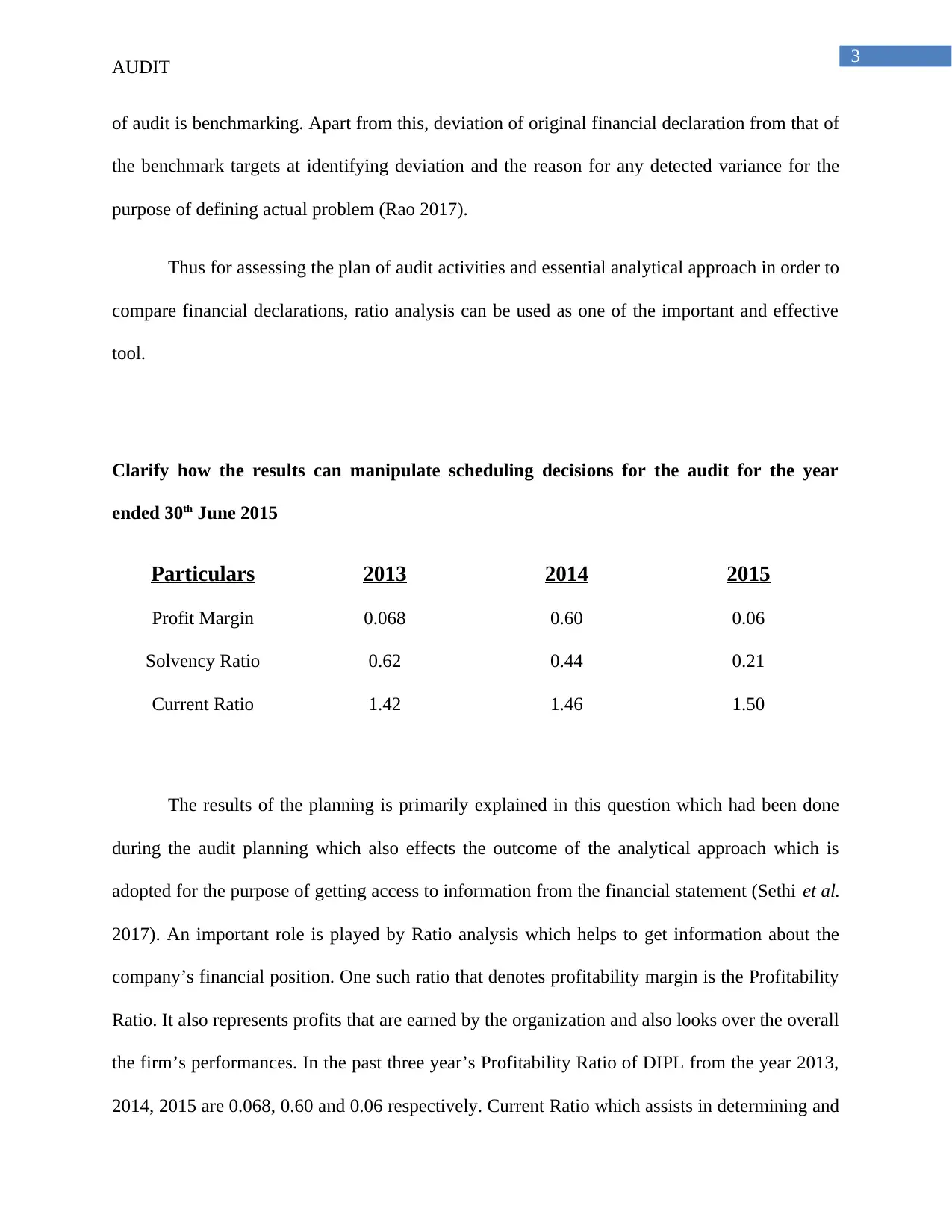

Clarify how the results can manipulate scheduling decisions for the audit for the year

ended 30th June 2015

Particulars 2013 2014 2015

Profit Margin 0.068 0.60 0.06

Solvency Ratio 0.62 0.44 0.21

Current Ratio 1.42 1.46 1.50

The results of the planning is primarily explained in this question which had been done

during the audit planning which also effects the outcome of the analytical approach which is

adopted for the purpose of getting access to information from the financial statement (Sethi et al.

2017). An important role is played by Ratio analysis which helps to get information about the

company’s financial position. One such ratio that denotes profitability margin is the Profitability

Ratio. It also represents profits that are earned by the organization and also looks over the overall

the firm’s performances. In the past three year’s Profitability Ratio of DIPL from the year 2013,

2014, 2015 are 0.068, 0.60 and 0.06 respectively. Current Ratio which assists in determining and

AUDIT

of audit is benchmarking. Apart from this, deviation of original financial declaration from that of

the benchmark targets at identifying deviation and the reason for any detected variance for the

purpose of defining actual problem (Rao 2017).

Thus for assessing the plan of audit activities and essential analytical approach in order to

compare financial declarations, ratio analysis can be used as one of the important and effective

tool.

Clarify how the results can manipulate scheduling decisions for the audit for the year

ended 30th June 2015

Particulars 2013 2014 2015

Profit Margin 0.068 0.60 0.06

Solvency Ratio 0.62 0.44 0.21

Current Ratio 1.42 1.46 1.50

The results of the planning is primarily explained in this question which had been done

during the audit planning which also effects the outcome of the analytical approach which is

adopted for the purpose of getting access to information from the financial statement (Sethi et al.

2017). An important role is played by Ratio analysis which helps to get information about the

company’s financial position. One such ratio that denotes profitability margin is the Profitability

Ratio. It also represents profits that are earned by the organization and also looks over the overall

the firm’s performances. In the past three year’s Profitability Ratio of DIPL from the year 2013,

2014, 2015 are 0.068, 0.60 and 0.06 respectively. Current Ratio which assists in determining and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

AUDIT

assessing the position of liquidity of DIPL for the year 2013, 2014 and 2015 stands at 1.42, 1.46

and 1.5 respectively. Generally, 2:1 is considered to be the ideal current ratio.

Then comes the solvency ratio of DIPL for the year 2013, 2014, 2015 that are 0.62, 0.44

and 0.21 respectively. It is found that the overall cash flow remains adequate for meeting both

short term and as well as the long term liabilities for DIPL after comparing the results of the ratio

for the three consecutive years which are 2013, 2014 and 2015.

Thus, it can be said that it is the assessor’s responsibility to understand the firm’s relative

positive for three successive years and analyzing all those factors that may or might lead to some

undesirable or unfavorable situation of business enterprise.

Answer to Question 2.

Identifying two inherent risk factor that arise from the nature of DIPL trade process

The two inherent risk factors that are faced by DIPL in their business operations are

required to be identified in this question. One of the most significant factors that also needs

serious concern during conducting audit is the material misstated figures that are present in the

financial declaration of the business (Carnegie and O’Connell 2014). In order to get accustomed

with different systematic and unsystematic risks it is very important to identify the financial

declaration which are mentioned in the financial statements. A true and fair view of the financial

statement which are either financial or non-financial can be drawn from these statements. Hence,

evaluation of different types of risk is an important role of the assessor.

AUDIT

assessing the position of liquidity of DIPL for the year 2013, 2014 and 2015 stands at 1.42, 1.46

and 1.5 respectively. Generally, 2:1 is considered to be the ideal current ratio.

Then comes the solvency ratio of DIPL for the year 2013, 2014, 2015 that are 0.62, 0.44

and 0.21 respectively. It is found that the overall cash flow remains adequate for meeting both

short term and as well as the long term liabilities for DIPL after comparing the results of the ratio

for the three consecutive years which are 2013, 2014 and 2015.

Thus, it can be said that it is the assessor’s responsibility to understand the firm’s relative

positive for three successive years and analyzing all those factors that may or might lead to some

undesirable or unfavorable situation of business enterprise.

Answer to Question 2.

Identifying two inherent risk factor that arise from the nature of DIPL trade process

The two inherent risk factors that are faced by DIPL in their business operations are

required to be identified in this question. One of the most significant factors that also needs

serious concern during conducting audit is the material misstated figures that are present in the

financial declaration of the business (Carnegie and O’Connell 2014). In order to get accustomed

with different systematic and unsystematic risks it is very important to identify the financial

declaration which are mentioned in the financial statements. A true and fair view of the financial

statement which are either financial or non-financial can be drawn from these statements. Hence,

evaluation of different types of risk is an important role of the assessor.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

AUDIT

One amongst many other risks that may leads to substantial error which results from

activities such as operation, environment and nature of accounts is the Inherent risk. All though

there are several different types of risks that might have some substantial impression on the

financial statement. The bookkeeper cannot predict the risk after the omission is correlated as

diverse error (Zhang 2017).

It is noted from the case study that several transactions that were overlooked by the

management of DIPL had been misplaced by the accounts. Ineffective planning of sales and also

ineffective marketing activities which lead to inconsistencies are found. It is found that DIPL’s

financial declaration analysis favors the profit level which is produced out of revenue. The

failures which needs adjustments in the functionalities and also in identification of requirement

which are necessary for maintaining the required profit may also be faced by the management.

The Macro and Micro economic factors needs to be identified by the management in terms of

social, political and others as the business faced failure. The poor sales figures of DIPL can be

found at the inherent level of risk that leads to risk while analyzing the financial declarations

(McKee 2015).

The different factors can be found which leads to inherent risk into numerous sectors.

Material misstatement can be spotted in business enterprise due to falsification of different items

and also due to some external factors which concerns the environment.

Risk that affect the risk of material misstatement in the financial report

There are some risk which are identified and those are needed to be considered as

vulnerability in connotation with the misstatement of material for given assertion. Some of those

risks are stated below:

AUDIT

One amongst many other risks that may leads to substantial error which results from

activities such as operation, environment and nature of accounts is the Inherent risk. All though

there are several different types of risks that might have some substantial impression on the

financial statement. The bookkeeper cannot predict the risk after the omission is correlated as

diverse error (Zhang 2017).

It is noted from the case study that several transactions that were overlooked by the

management of DIPL had been misplaced by the accounts. Ineffective planning of sales and also

ineffective marketing activities which lead to inconsistencies are found. It is found that DIPL’s

financial declaration analysis favors the profit level which is produced out of revenue. The

failures which needs adjustments in the functionalities and also in identification of requirement

which are necessary for maintaining the required profit may also be faced by the management.

The Macro and Micro economic factors needs to be identified by the management in terms of

social, political and others as the business faced failure. The poor sales figures of DIPL can be

found at the inherent level of risk that leads to risk while analyzing the financial declarations

(McKee 2015).

The different factors can be found which leads to inherent risk into numerous sectors.

Material misstatement can be spotted in business enterprise due to falsification of different items

and also due to some external factors which concerns the environment.

Risk that affect the risk of material misstatement in the financial report

There are some risk which are identified and those are needed to be considered as

vulnerability in connotation with the misstatement of material for given assertion. Some of those

risks are stated below:

6

AUDIT

Excessive pressure on employees and also on the management is one of such identified

inherent risk. Poor bookkeeping is the result of excessive load of work upon the staff

members of the business. Certain qualities that causes issues relating to cash flow along

with poor operating outcomes of the business can be found accompanied by poor

liquidity.

Misinterpreted error or risk of errors is another risk of the identified inherent risk.

Reliability and also complexity is hampered by error or misrepresentation.

As said earlier, unusual work load or pressure on management is another identified

inherent risk. Sometimes it might happen that the management may get inducements or

incentives for their job and it is not stated in the financial declaration (Soh et al. 2015).

Integrity among the complete management is one of the identified inherent risk.

Management of DIPL severely lacks required integrity and expects to be prepared for the

loss of prestige or reputation in the overall community of the business.

Nature of entity business is another inherent risk which is also identified. Growth of

major economic and competitive environments are the outcome of business operations at

DIPL. Apart from these, several risk can also be noted that lead to the business entity’s

general inherent risk.

AUDIT

Excessive pressure on employees and also on the management is one of such identified

inherent risk. Poor bookkeeping is the result of excessive load of work upon the staff

members of the business. Certain qualities that causes issues relating to cash flow along

with poor operating outcomes of the business can be found accompanied by poor

liquidity.

Misinterpreted error or risk of errors is another risk of the identified inherent risk.

Reliability and also complexity is hampered by error or misrepresentation.

As said earlier, unusual work load or pressure on management is another identified

inherent risk. Sometimes it might happen that the management may get inducements or

incentives for their job and it is not stated in the financial declaration (Soh et al. 2015).

Integrity among the complete management is one of the identified inherent risk.

Management of DIPL severely lacks required integrity and expects to be prepared for the

loss of prestige or reputation in the overall community of the business.

Nature of entity business is another inherent risk which is also identified. Growth of

major economic and competitive environments are the outcome of business operations at

DIPL. Apart from these, several risk can also be noted that lead to the business entity’s

general inherent risk.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

AUDIT

Answer to Question 3

Part A

Identify two key fraud risk factors relating to misstatement that arise from fraudulent

financial coverage to which DIPL may be susceptible

The substantial loss may be encountered by a business entity due to their assets that are

the results of several fraudulent actions. Apart from this, when the workers are not satisfied then

such fraud in business might occur which results in excessive workloads. Moreover, as a result

of the management as also due to pressure from different investors, who for the purpose of

attaining definite goal reports pecuniary outcomes, the business entity might meet high degree of

fraud risk.

In DIPL case study, in real the company suffers risk that occurs from the nature of

operating and instigating the staff for engaging in fraudulent actions due to high dissatisfaction

level. This is the outcome of the fact that the novel system of accounting had increased pressure

and workloads on the staff members and on workers (Tang 2017). During the installation process

of IT system at DIPL, it faces several fraudulent activities which in turn increases unnecessary

and extreme pressure on employees.

AUDIT

Answer to Question 3

Part A

Identify two key fraud risk factors relating to misstatement that arise from fraudulent

financial coverage to which DIPL may be susceptible

The substantial loss may be encountered by a business entity due to their assets that are

the results of several fraudulent actions. Apart from this, when the workers are not satisfied then

such fraud in business might occur which results in excessive workloads. Moreover, as a result

of the management as also due to pressure from different investors, who for the purpose of

attaining definite goal reports pecuniary outcomes, the business entity might meet high degree of

fraud risk.

In DIPL case study, in real the company suffers risk that occurs from the nature of

operating and instigating the staff for engaging in fraudulent actions due to high dissatisfaction

level. This is the outcome of the fact that the novel system of accounting had increased pressure

and workloads on the staff members and on workers (Tang 2017). During the installation process

of IT system at DIPL, it faces several fraudulent activities which in turn increases unnecessary

and extreme pressure on employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

AUDIT

Part B

Clarify how the risk factors recognized that influence the conduct of the audit

The identification of risk that are related along with application of novel IT system of

accounting for observing the happenings at different levels is the responsibility of the auditor. As

the cost of paper is higher than the companies average cost, the process of raw material valuation

is adopted by DIPL. For the purpose of evaluating and monitoring financial statements and

various mechanisms the auditors are held responsible (Kend et al. 2014). As a result, for any

business enterprise it assists in detection of risks in the financial statement in the early stages.

AUDIT

Part B

Clarify how the risk factors recognized that influence the conduct of the audit

The identification of risk that are related along with application of novel IT system of

accounting for observing the happenings at different levels is the responsibility of the auditor. As

the cost of paper is higher than the companies average cost, the process of raw material valuation

is adopted by DIPL. For the purpose of evaluating and monitoring financial statements and

various mechanisms the auditors are held responsible (Kend et al. 2014). As a result, for any

business enterprise it assists in detection of risks in the financial statement in the early stages.

9

AUDIT

Reference

Askary, S. and Van Sant, R., 2014. An educational theory for teaching auditing and assurance

after Enron. International Journal of Management in Education, 8(3), pp.302-320.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

McKee, D., 2015. New external audit report standards are game changing. Governance

Directions, 67(4), p.222.

Rao, S., 2017. CURRENT STATE OF ASSURANCE ON SUSTAINABILITY REPORTS. CPA

Journal.

Sarens, G., 2015. Guest editorial on internal assurance: a concept in evolution. Managerial

Auditing Journal, 30(1).

Sethi, S.P., Martell, T.F. and Demir, M., 2017. Enhancing the role and effectiveness of corporate

social responsibility (CSR) reports: The missing element of content verification and integrity

assurance. Journal of Business Ethics, 144(1), pp.59-82.

AUDIT

Reference

Askary, S. and Van Sant, R., 2014. An educational theory for teaching auditing and assurance

after Enron. International Journal of Management in Education, 8(3), pp.302-320.

Carnegie, G.D. and O’Connell, B.T., 2014. A longitudinal study of the interplay of corporate

collapse, accounting failure and governance change in Australia: Early 1890s to early

2000s. Critical Perspectives on Accounting, 25(6), pp.446-468.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

McKee, D., 2015. New external audit report standards are game changing. Governance

Directions, 67(4), p.222.

Rao, S., 2017. CURRENT STATE OF ASSURANCE ON SUSTAINABILITY REPORTS. CPA

Journal.

Sarens, G., 2015. Guest editorial on internal assurance: a concept in evolution. Managerial

Auditing Journal, 30(1).

Sethi, S.P., Martell, T.F. and Demir, M., 2017. Enhancing the role and effectiveness of corporate

social responsibility (CSR) reports: The missing element of content verification and integrity

assurance. Journal of Business Ethics, 144(1), pp.59-82.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

AUDIT

Soh, D.S., Leung, P. and Leong, S., 2015. The development of integrated reporting and the role

of the accounting and auditing profession. In Social Audit Regulation (pp. 33-57). Springer

International Publishing.

Tang, Q., 2017. Institutional Influence, Transition Management, and the Demand for Carbon

Auditing: The Chinese Experience.

Zhang, Y., 2017. Corporate Social Responsibility Assurance. Encyclopedia of Business and

Professional Ethics, pp.1-5.

AUDIT

Soh, D.S., Leung, P. and Leong, S., 2015. The development of integrated reporting and the role

of the accounting and auditing profession. In Social Audit Regulation (pp. 33-57). Springer

International Publishing.

Tang, Q., 2017. Institutional Influence, Transition Management, and the Demand for Carbon

Auditing: The Chinese Experience.

Zhang, Y., 2017. Corporate Social Responsibility Assurance. Encyclopedia of Business and

Professional Ethics, pp.1-5.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.