Fulvous Enterprises Audit Report: Materiality, Risk, Procedures

VerifiedAdded on 2023/06/05

|11

|1640

|292

Report

AI Summary

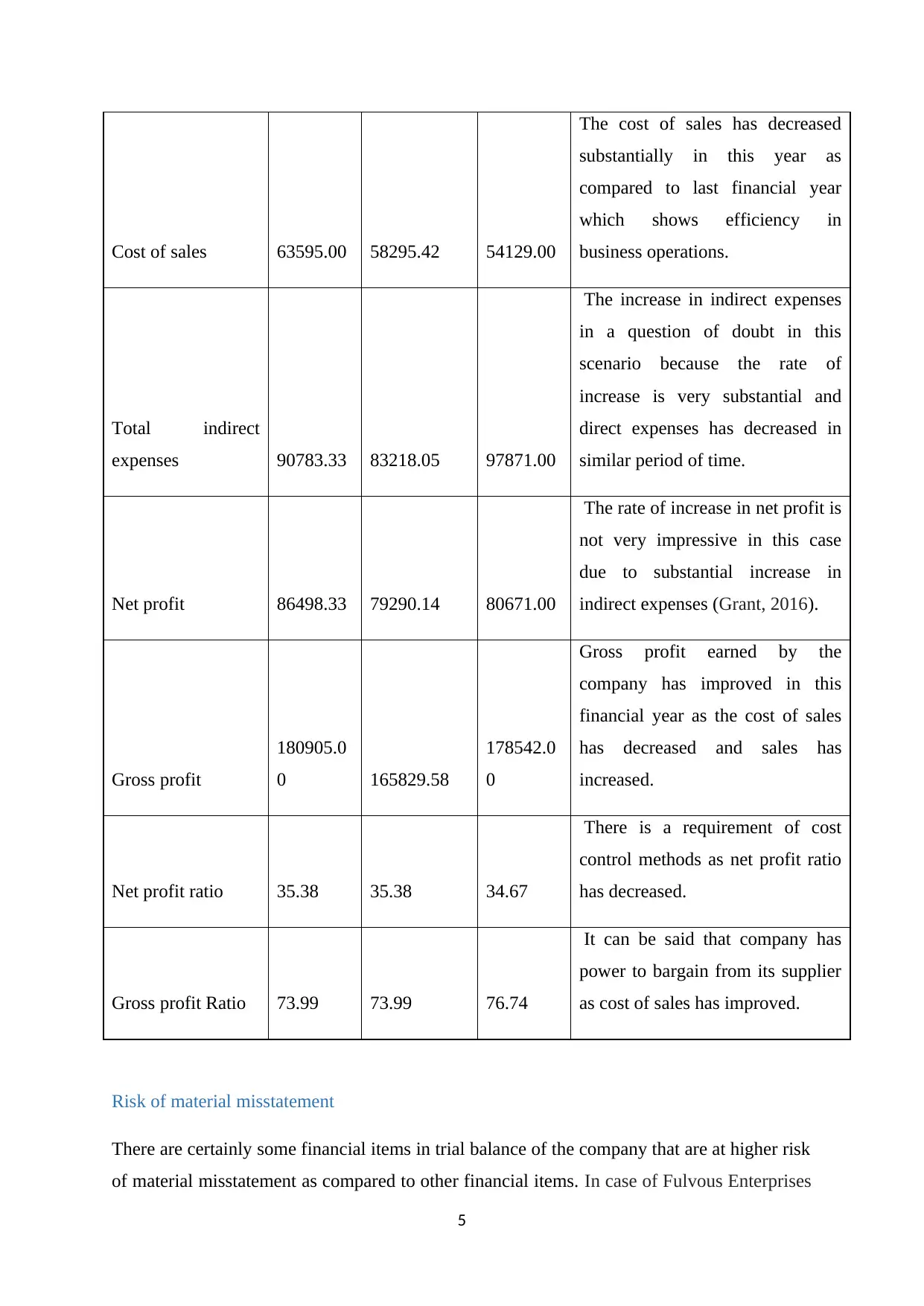

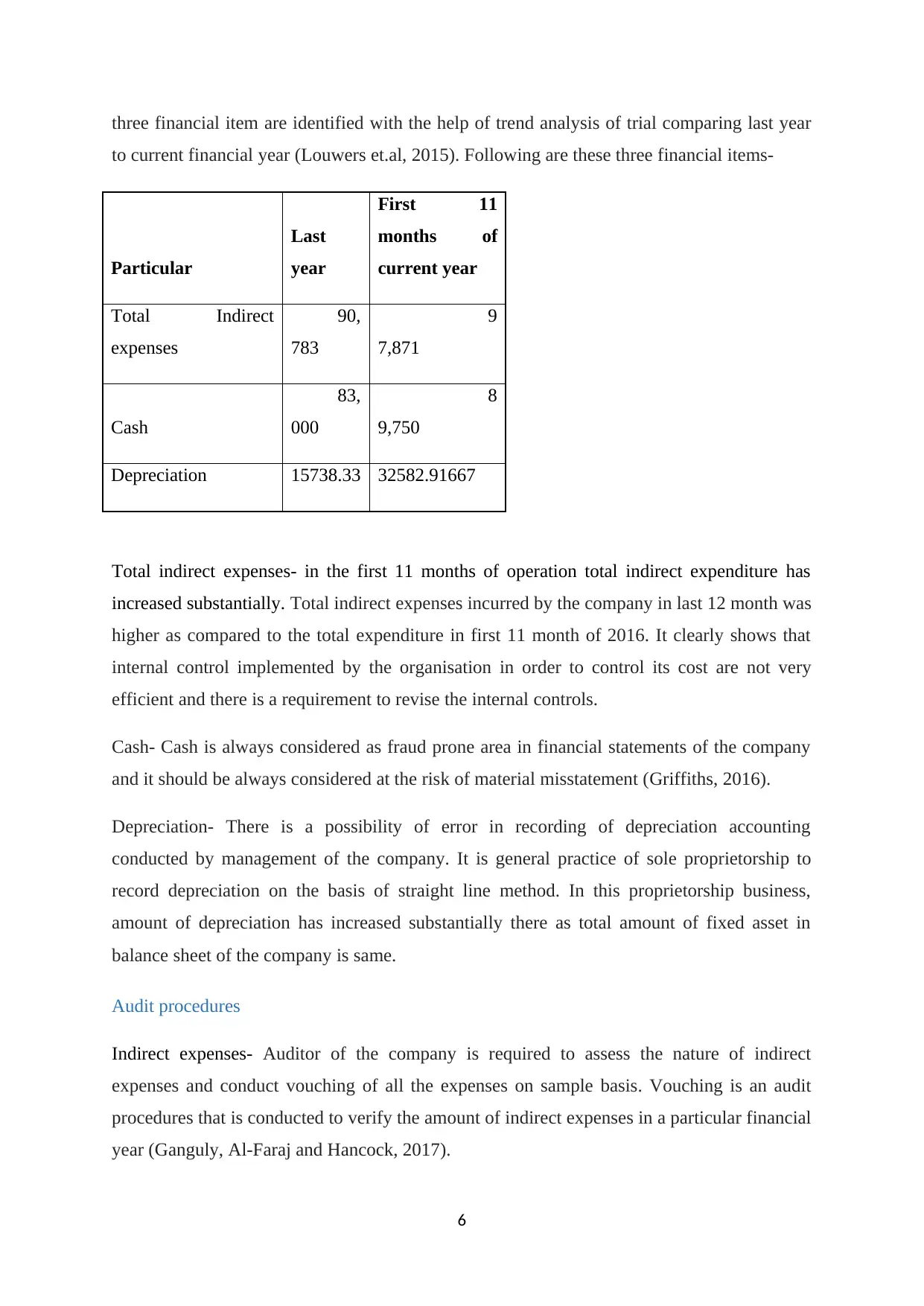

This report presents an independent audit of Fulvous Enterprises, a proprietorship, focusing on key aspects of financial auditing. It assesses the materiality of financial statements, conducting an analytical review to identify potential risks of material misstatement. The report highlights specific financial items, such as indirect expenses, cash, and depreciation, that pose a higher risk, and suggests appropriate audit procedures for each. It also addresses the importance of auditor skepticism in identifying fraud risks, cautioning against relying solely on management's helpfulness as audit evidence. The report concludes that the initial materiality assessment was too high and recommends a more rigorous approach to ensure accurate financial reporting. Access more solved assignments and past papers on Desklib.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.