ACCT20075 - Audit & Ethics: Financial Analysis of Newcrest Mining

VerifiedAdded on 2023/06/07

|12

|2632

|200

Report

AI Summary

This report provides a comprehensive analysis of Newcrest Mining Corporation's audit and ethics practices. It begins with an examination of the principle of materiality and its application within the company's financial statements, considering both quantitative and qualitative aspects. The report then reviews draft notes and disclosures, focusing on impairment of non-financial assets, provisions, contingent liabilities, and financial leases. An analytical evaluation of the financial statements follows, with a detailed analysis of profitability, efficiency, and liquidity ratios over a four-year period. The report also includes an analysis of the cash flow statement, categorizing cash flows from operating, investing, and financing activities, and assesses the company's going concern concept. Finally, the report reviews the auditor's report, highlighting key audit matters such as the assessment of asset carrying value, multiple taxation, and mine rehabilitation provisions, concluding that the financial statements adhere to relevant accounting principles and standards.

Running head: AUDIT AND ETHICS

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Audit and Ethics

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Review of Draft notes and Disclosures.......................................................................................3

Section 2..........................................................................................................................................4

Analytical evaluation of the financial statements........................................................................4

Section 3..........................................................................................................................................8

Analysis of Cash Flow Statement................................................................................................8

Review of the Auditor Report......................................................................................................9

Reference.......................................................................................................................................10

AUDIT AND ETHICS

Table of Contents

Section 1..........................................................................................................................................2

Materiality and Scope of Audit....................................................................................................2

Review of Draft notes and Disclosures.......................................................................................3

Section 2..........................................................................................................................................4

Analytical evaluation of the financial statements........................................................................4

Section 3..........................................................................................................................................8

Analysis of Cash Flow Statement................................................................................................8

Review of the Auditor Report......................................................................................................9

Reference.......................................................................................................................................10

2

AUDIT AND ETHICS

Section 1

Materiality and Scope of Audit

The primary aim of undertaking this assignment on the Newcrest Mining Corporation of

Australia is to carefully scrutinize the different auditing procedures for the purpose of reviewing

the different aspects of the principle of materiality and its adherence by the Newcrest Mining

Corporation. The principle of materiality helps in assessing the true and fairness of the financial

statements (Simnett & Huggins, 2014). The principle of materiality is considered as a prominent

part of the auditing and accounting principles which are considered necessary in the preparation

of the financial statements. Here the major and the minor misstatements are considered after

initial analysis. Thereafter the significant misstatements are carefully considered on the level of

materiality, and how it is going to affect the company’s decision making (Lobo & Zhao, 2013).

For this particular assignment is the Newcrest Mining Corporation, which is based in Australia.

It is engaged in the exploration, mining, development and selling of gold and gold copper

concentrate. It is Australia’s leading company in terms of mining and it operates beyond

Australia and has many international markets.

Materiality is a crucial part of the entire auditing operation and is a significant part of the

auditor as it is his responsibility of ensuring if it is followed by the company management or not.

In the case of materiality, the auditor considers two aspects, the quantitative and the qualitative

aspects (Morningstar.com, 2018). In the quantitative aspect, the auditor scrutinizes the estimated

percentages on the different financial items in the financial statements and in the case of the

qualitative aspect, the auditor looks into the important financial aspects such as inventory, net

profit and various other similar items. The auditor computes the planning of the materiality at the

AUDIT AND ETHICS

Section 1

Materiality and Scope of Audit

The primary aim of undertaking this assignment on the Newcrest Mining Corporation of

Australia is to carefully scrutinize the different auditing procedures for the purpose of reviewing

the different aspects of the principle of materiality and its adherence by the Newcrest Mining

Corporation. The principle of materiality helps in assessing the true and fairness of the financial

statements (Simnett & Huggins, 2014). The principle of materiality is considered as a prominent

part of the auditing and accounting principles which are considered necessary in the preparation

of the financial statements. Here the major and the minor misstatements are considered after

initial analysis. Thereafter the significant misstatements are carefully considered on the level of

materiality, and how it is going to affect the company’s decision making (Lobo & Zhao, 2013).

For this particular assignment is the Newcrest Mining Corporation, which is based in Australia.

It is engaged in the exploration, mining, development and selling of gold and gold copper

concentrate. It is Australia’s leading company in terms of mining and it operates beyond

Australia and has many international markets.

Materiality is a crucial part of the entire auditing operation and is a significant part of the

auditor as it is his responsibility of ensuring if it is followed by the company management or not.

In the case of materiality, the auditor considers two aspects, the quantitative and the qualitative

aspects (Morningstar.com, 2018). In the quantitative aspect, the auditor scrutinizes the estimated

percentages on the different financial items in the financial statements and in the case of the

qualitative aspect, the auditor looks into the important financial aspects such as inventory, net

profit and various other similar items. The auditor computes the planning of the materiality at the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT AND ETHICS

initial stage, and on its basis, approximate performance materiality of different items are

calculated.

Various bases which are accounted for are based on important items which are shown in

the financial statements of the organization. For the Profit and loss account, the net profit before

tax, aggregate sales are taken as bases and in the case of the balance sheet, the aggregate assets

are considered.

The annual report of Newcrest has been analyzed. The revenue has improved from

FY16’. It is the general norm of considering the item having the highest value for estimating

bases. Here the aggregate assets can be considered for considering the planning materiality. For

FY 17, it is $11, 583 and the percentage for calculating planning material is assumed to be at 5%

(Asx.com.au 2018). The calculation of planning materiality is below:

Planning material= (Total assets*5%)

= ($11,583*5%) = $579.15

Review of Draft notes and Disclosures

The draft and disclosures notes contains information about the way of treatment of

certain items, which are very important for the auditors. The most important items under this

head have been provided below:

Impairment of non-financial assets: The impairment tests for indicating the impairment

of the non-financial assets have been mentioned in this section (Adenergy.com.au, 2018).

The different basis of impairment and the impairment reversal calculations have also

been mentioned.

AUDIT AND ETHICS

initial stage, and on its basis, approximate performance materiality of different items are

calculated.

Various bases which are accounted for are based on important items which are shown in

the financial statements of the organization. For the Profit and loss account, the net profit before

tax, aggregate sales are taken as bases and in the case of the balance sheet, the aggregate assets

are considered.

The annual report of Newcrest has been analyzed. The revenue has improved from

FY16’. It is the general norm of considering the item having the highest value for estimating

bases. Here the aggregate assets can be considered for considering the planning materiality. For

FY 17, it is $11, 583 and the percentage for calculating planning material is assumed to be at 5%

(Asx.com.au 2018). The calculation of planning materiality is below:

Planning material= (Total assets*5%)

= ($11,583*5%) = $579.15

Review of Draft notes and Disclosures

The draft and disclosures notes contains information about the way of treatment of

certain items, which are very important for the auditors. The most important items under this

head have been provided below:

Impairment of non-financial assets: The impairment tests for indicating the impairment

of the non-financial assets have been mentioned in this section (Adenergy.com.au, 2018).

The different basis of impairment and the impairment reversal calculations have also

been mentioned.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT AND ETHICS

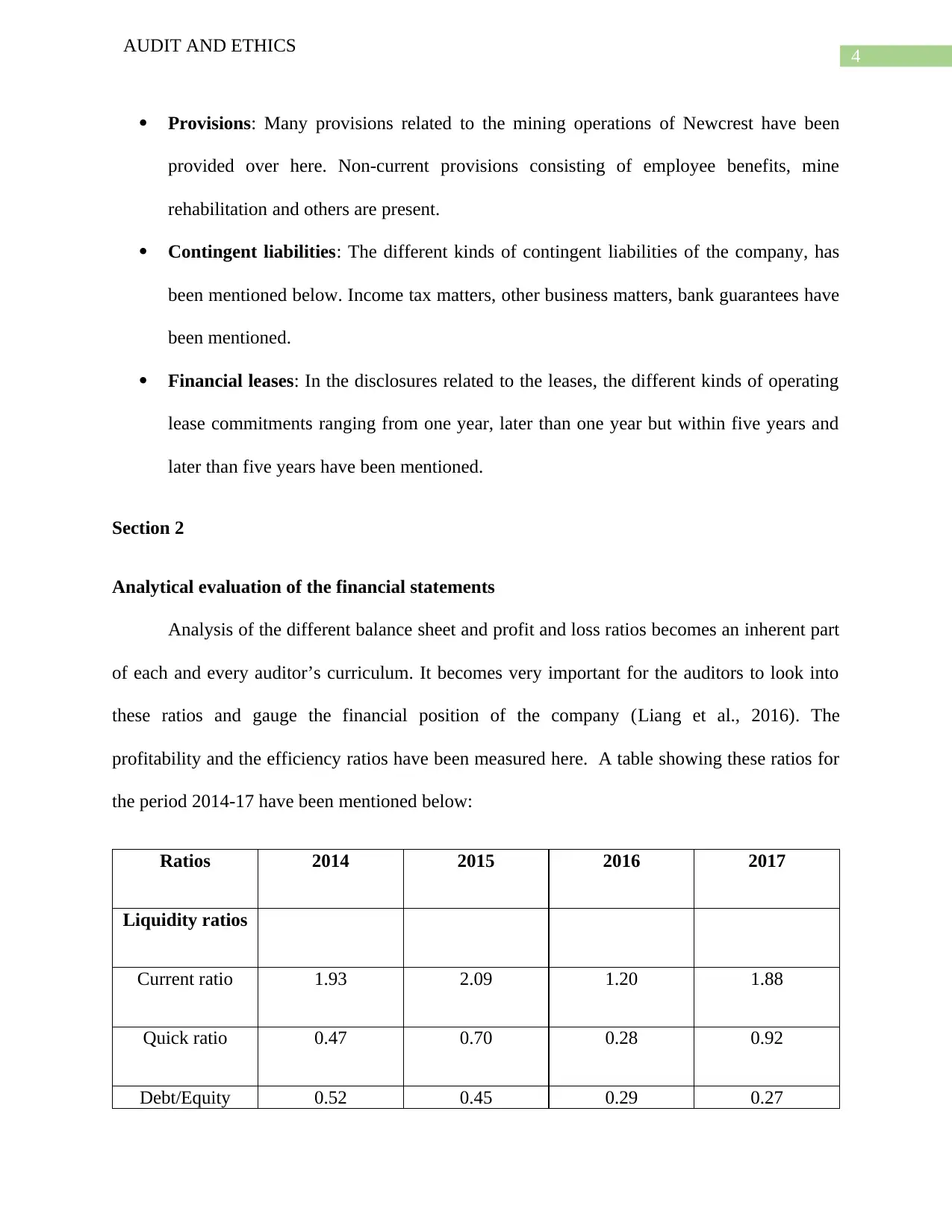

Provisions: Many provisions related to the mining operations of Newcrest have been

provided over here. Non-current provisions consisting of employee benefits, mine

rehabilitation and others are present.

Contingent liabilities: The different kinds of contingent liabilities of the company, has

been mentioned below. Income tax matters, other business matters, bank guarantees have

been mentioned.

Financial leases: In the disclosures related to the leases, the different kinds of operating

lease commitments ranging from one year, later than one year but within five years and

later than five years have been mentioned.

Section 2

Analytical evaluation of the financial statements

Analysis of the different balance sheet and profit and loss ratios becomes an inherent part

of each and every auditor’s curriculum. It becomes very important for the auditors to look into

these ratios and gauge the financial position of the company (Liang et al., 2016). The

profitability and the efficiency ratios have been measured here. A table showing these ratios for

the period 2014-17 have been mentioned below:

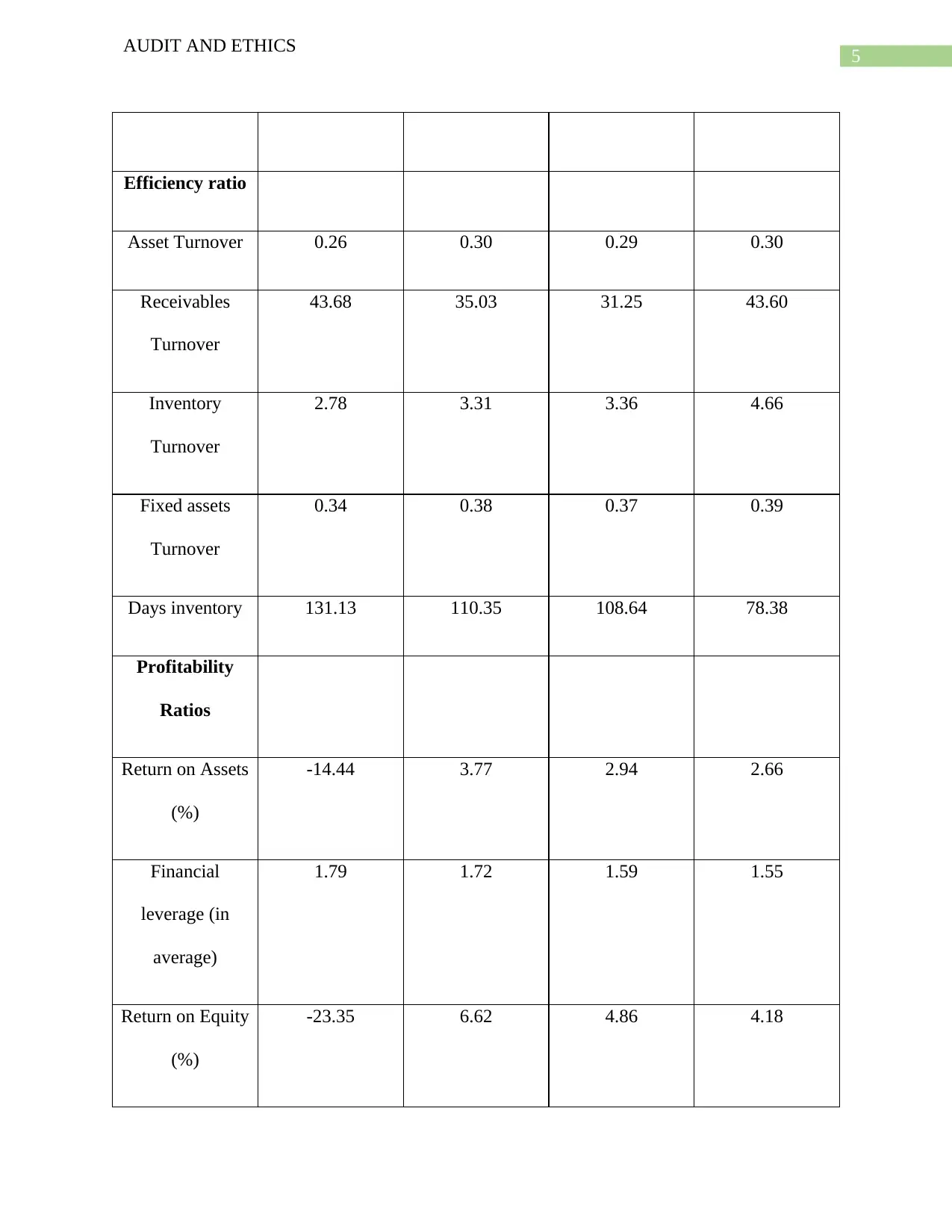

Ratios 2014 2015 2016 2017

Liquidity ratios

Current ratio 1.93 2.09 1.20 1.88

Quick ratio 0.47 0.70 0.28 0.92

Debt/Equity 0.52 0.45 0.29 0.27

AUDIT AND ETHICS

Provisions: Many provisions related to the mining operations of Newcrest have been

provided over here. Non-current provisions consisting of employee benefits, mine

rehabilitation and others are present.

Contingent liabilities: The different kinds of contingent liabilities of the company, has

been mentioned below. Income tax matters, other business matters, bank guarantees have

been mentioned.

Financial leases: In the disclosures related to the leases, the different kinds of operating

lease commitments ranging from one year, later than one year but within five years and

later than five years have been mentioned.

Section 2

Analytical evaluation of the financial statements

Analysis of the different balance sheet and profit and loss ratios becomes an inherent part

of each and every auditor’s curriculum. It becomes very important for the auditors to look into

these ratios and gauge the financial position of the company (Liang et al., 2016). The

profitability and the efficiency ratios have been measured here. A table showing these ratios for

the period 2014-17 have been mentioned below:

Ratios 2014 2015 2016 2017

Liquidity ratios

Current ratio 1.93 2.09 1.20 1.88

Quick ratio 0.47 0.70 0.28 0.92

Debt/Equity 0.52 0.45 0.29 0.27

5

AUDIT AND ETHICS

Efficiency ratio

Asset Turnover 0.26 0.30 0.29 0.30

Receivables

Turnover

43.68 35.03 31.25 43.60

Inventory

Turnover

2.78 3.31 3.36 4.66

Fixed assets

Turnover

0.34 0.38 0.37 0.39

Days inventory 131.13 110.35 108.64 78.38

Profitability

Ratios

Return on Assets

(%)

-14.44 3.77 2.94 2.66

Financial

leverage (in

average)

1.79 1.72 1.59 1.55

Return on Equity

(%)

-23.35 6.62 4.86 4.18

AUDIT AND ETHICS

Efficiency ratio

Asset Turnover 0.26 0.30 0.29 0.30

Receivables

Turnover

43.68 35.03 31.25 43.60

Inventory

Turnover

2.78 3.31 3.36 4.66

Fixed assets

Turnover

0.34 0.38 0.37 0.39

Days inventory 131.13 110.35 108.64 78.38

Profitability

Ratios

Return on Assets

(%)

-14.44 3.77 2.94 2.66

Financial

leverage (in

average)

1.79 1.72 1.59 1.55

Return on Equity

(%)

-23.35 6.62 4.86 4.18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT AND ETHICS

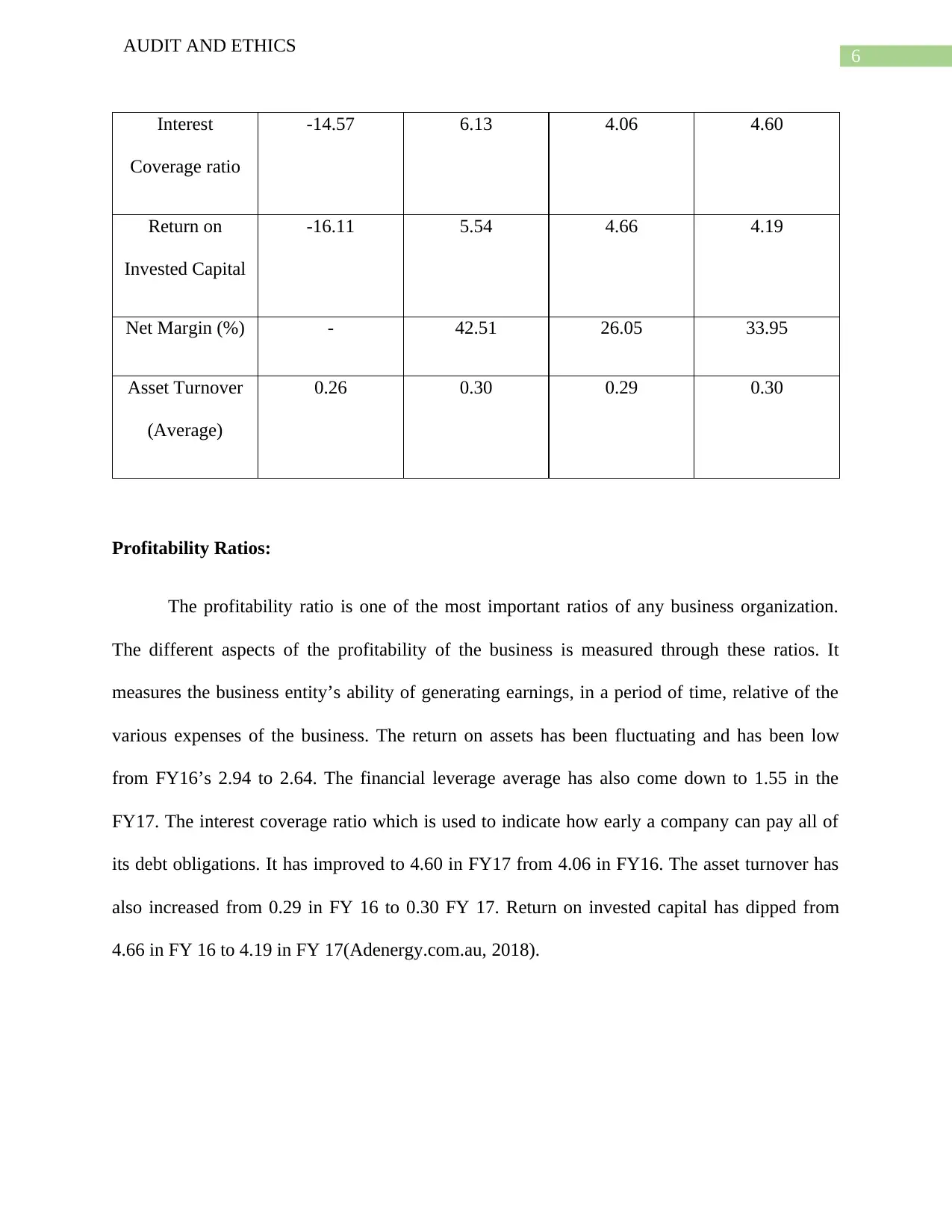

Interest

Coverage ratio

-14.57 6.13 4.06 4.60

Return on

Invested Capital

-16.11 5.54 4.66 4.19

Net Margin (%) - 42.51 26.05 33.95

Asset Turnover

(Average)

0.26 0.30 0.29 0.30

Profitability Ratios:

The profitability ratio is one of the most important ratios of any business organization.

The different aspects of the profitability of the business is measured through these ratios. It

measures the business entity’s ability of generating earnings, in a period of time, relative of the

various expenses of the business. The return on assets has been fluctuating and has been low

from FY16’s 2.94 to 2.64. The financial leverage average has also come down to 1.55 in the

FY17. The interest coverage ratio which is used to indicate how early a company can pay all of

its debt obligations. It has improved to 4.60 in FY17 from 4.06 in FY16. The asset turnover has

also increased from 0.29 in FY 16 to 0.30 FY 17. Return on invested capital has dipped from

4.66 in FY 16 to 4.19 in FY 17(Adenergy.com.au, 2018).

AUDIT AND ETHICS

Interest

Coverage ratio

-14.57 6.13 4.06 4.60

Return on

Invested Capital

-16.11 5.54 4.66 4.19

Net Margin (%) - 42.51 26.05 33.95

Asset Turnover

(Average)

0.26 0.30 0.29 0.30

Profitability Ratios:

The profitability ratio is one of the most important ratios of any business organization.

The different aspects of the profitability of the business is measured through these ratios. It

measures the business entity’s ability of generating earnings, in a period of time, relative of the

various expenses of the business. The return on assets has been fluctuating and has been low

from FY16’s 2.94 to 2.64. The financial leverage average has also come down to 1.55 in the

FY17. The interest coverage ratio which is used to indicate how early a company can pay all of

its debt obligations. It has improved to 4.60 in FY17 from 4.06 in FY16. The asset turnover has

also increased from 0.29 in FY 16 to 0.30 FY 17. Return on invested capital has dipped from

4.66 in FY 16 to 4.19 in FY 17(Adenergy.com.au, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT AND ETHICS

Efficiency Ratios:

Efficiency ratio is primarily used for the purpose of analyzing how well a business entity

uses its assets and liabilities. It can be used for the purpose of calculating turnover of receivables,

repayment of liabilities, quality and the utility of equities and for the general usage of the

inventory of the business entity. Receivables turnover which is used to analyze how well a

company utilizes its assets has shown an increase from 35 to 44 in the FY17. Assets turnover

has also improved from 0.29 to 0.30 in FY17. Inventory turnover had significantly improved

from 3.66 in FY16 to 4.66 in FY 17 (Delen, Kuzey & Uyar, 2013). More or less, in the four year

period it was always on an increasing trend.

Liquidity ratio:

Liquidity ratios are again forms a part of any business entity’s financial prospects. It is

normally used for analysis and measurement of the liquidity position of the business entity. It is

mainly intended to explore the relationship between the current assets and current liabilities of

the business. They mainly include the current, quick ratio, and various others. In the case of

Newcrest, the current ratio has been on a very fluctuating trend, dipping from 2.09 in FY 15 to

1.20 in FY16 and slightly increasing to 1.88 in FY17. In the case of the quick ratio, some

interesting aspects have been seen. The quick ratio was 0.47 in FY 14 after which it increased to

0.70 in FY15, again dipping very low to 0.28 in FY 16, which again had increased to 0.92 in FY

17(Adenergy.com.au, 2018).

It becomes very important for the auditor to have a closer look into the different aspects

of these financial reports specially the fluctuating trends, which have been seen in the case of the

liquidity ratios specifically. Considering the present state of the financial affairs of the company,

AUDIT AND ETHICS

Efficiency Ratios:

Efficiency ratio is primarily used for the purpose of analyzing how well a business entity

uses its assets and liabilities. It can be used for the purpose of calculating turnover of receivables,

repayment of liabilities, quality and the utility of equities and for the general usage of the

inventory of the business entity. Receivables turnover which is used to analyze how well a

company utilizes its assets has shown an increase from 35 to 44 in the FY17. Assets turnover

has also improved from 0.29 to 0.30 in FY17. Inventory turnover had significantly improved

from 3.66 in FY16 to 4.66 in FY 17 (Delen, Kuzey & Uyar, 2013). More or less, in the four year

period it was always on an increasing trend.

Liquidity ratio:

Liquidity ratios are again forms a part of any business entity’s financial prospects. It is

normally used for analysis and measurement of the liquidity position of the business entity. It is

mainly intended to explore the relationship between the current assets and current liabilities of

the business. They mainly include the current, quick ratio, and various others. In the case of

Newcrest, the current ratio has been on a very fluctuating trend, dipping from 2.09 in FY 15 to

1.20 in FY16 and slightly increasing to 1.88 in FY17. In the case of the quick ratio, some

interesting aspects have been seen. The quick ratio was 0.47 in FY 14 after which it increased to

0.70 in FY15, again dipping very low to 0.28 in FY 16, which again had increased to 0.92 in FY

17(Adenergy.com.au, 2018).

It becomes very important for the auditor to have a closer look into the different aspects

of these financial reports specially the fluctuating trends, which have been seen in the case of the

liquidity ratios specifically. Considering the present state of the financial affairs of the company,

8

AUDIT AND ETHICS

the auditor must check the previous audit reports, the balance sheet items, the profit and loss

accounts, and the cash flow statement of Newcrest. The auditor must ask the management about

such fluctuating trends in the businesses. The auditor must inspect the books of accounts closely,

scrutinize them and if required ask for some extra information from the management and the

internal auditors of the company, which would help in making the picture much clearer. The

auditor has the complete freedom to ask for any kind of information from the business’s

management, and the entity is accountable towards providing each and every kind of information

required by the auditor.

Section 3

Analysis of Cash Flow Statement

The cash flow statement of any business entity is one of the most important statements,

which tells about the present liquidity of the company. It provides the cash position of the

company. The cash flow statement of Newcrest has been classified into three major categories

mainly consisting of cash from operating, investing and financing activities. The cash from

operating was $1467 million, investing activity was $ (728) and the cash from financing

activities was $(300) million for the FY 17. The category of cash from operating was the highest

(Adenergy.com.au, 2018).

The primary cash receipts were interest received, receipts from customers and the major

cash payments included buying of fixed assets like plant and machinery, mining under

construction, payments made to suppliers and employees and payment of bank borrowings. The

AUDIT AND ETHICS

the auditor must check the previous audit reports, the balance sheet items, the profit and loss

accounts, and the cash flow statement of Newcrest. The auditor must ask the management about

such fluctuating trends in the businesses. The auditor must inspect the books of accounts closely,

scrutinize them and if required ask for some extra information from the management and the

internal auditors of the company, which would help in making the picture much clearer. The

auditor has the complete freedom to ask for any kind of information from the business’s

management, and the entity is accountable towards providing each and every kind of information

required by the auditor.

Section 3

Analysis of Cash Flow Statement

The cash flow statement of any business entity is one of the most important statements,

which tells about the present liquidity of the company. It provides the cash position of the

company. The cash flow statement of Newcrest has been classified into three major categories

mainly consisting of cash from operating, investing and financing activities. The cash from

operating was $1467 million, investing activity was $ (728) and the cash from financing

activities was $(300) million for the FY 17. The category of cash from operating was the highest

(Adenergy.com.au, 2018).

The primary cash receipts were interest received, receipts from customers and the major

cash payments included buying of fixed assets like plant and machinery, mining under

construction, payments made to suppliers and employees and payment of bank borrowings. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT AND ETHICS

primary cash financial and investing activities included payment for plant and equipment’s and

the receipts from the customers.

The going concern concept of accounting is one of the most significant aspect of

accounting which influences any business. It is the responsibility to bring any item which

influences the going concern of any company to its management’s attention. The liquidity

position is one of the most effective areas, which directly impacts the longevity of any business.

In case of Newcrest it has been seen that the entity has lagged behind in the liquidity department

and has been suffering from fluctuating liquidity trends (Simnett & Huggins, 2014). Although it

has been higher than the liquidity ratios of FY 16, but it has been inconsistent. The cash from the

investing and financing activities have been running on negative balances, which seriously

causes concerns regarding going concern of the entity. It can be seen that the signs propose that

the going concern state of the company might get influenced. The auditor must strongly advise

the management to improve the liquidity and the financial position of the entity.

Review of the Auditor Report

The auditor of Newcrest Mining is one of the big four auditing companies Ernest &

Young which has created the audit report of the business. As per the report of the auditor, the

financial statements of the company have followed all the important and relevant accounting

principles and standards of the company. The Auditors have concluded that Newcrest has

followed all the relevant provisions of the AASB, IASB, and the Corporation Act 2001

(Czerney, Schmidt & Thompson, 2014). It has been assured by the auditors that all the different

aspects of financial statements of Newcrest is free from any kind of financial misstatement.

AUDIT AND ETHICS

primary cash financial and investing activities included payment for plant and equipment’s and

the receipts from the customers.

The going concern concept of accounting is one of the most significant aspect of

accounting which influences any business. It is the responsibility to bring any item which

influences the going concern of any company to its management’s attention. The liquidity

position is one of the most effective areas, which directly impacts the longevity of any business.

In case of Newcrest it has been seen that the entity has lagged behind in the liquidity department

and has been suffering from fluctuating liquidity trends (Simnett & Huggins, 2014). Although it

has been higher than the liquidity ratios of FY 16, but it has been inconsistent. The cash from the

investing and financing activities have been running on negative balances, which seriously

causes concerns regarding going concern of the entity. It can be seen that the signs propose that

the going concern state of the company might get influenced. The auditor must strongly advise

the management to improve the liquidity and the financial position of the entity.

Review of the Auditor Report

The auditor of Newcrest Mining is one of the big four auditing companies Ernest &

Young which has created the audit report of the business. As per the report of the auditor, the

financial statements of the company have followed all the important and relevant accounting

principles and standards of the company. The Auditors have concluded that Newcrest has

followed all the relevant provisions of the AASB, IASB, and the Corporation Act 2001

(Czerney, Schmidt & Thompson, 2014). It has been assured by the auditors that all the different

aspects of financial statements of Newcrest is free from any kind of financial misstatement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT AND ETHICS

The key audit matters of the company consists of many different matters, ranging from

assessment of the carrying value of assets. Here the auditor evaluated the group’s assessment of

the indicators of impairment or impairment reversal to address this. Multiple taxation is another

key audit matter, which required the attention of the auditors and was resolved by testing the

group’s calculations for tax provisions or tax receivables in each jurisdiction. Mine rehabilitation

provisions regarding the protection and responsibility of the environment is another matter,

which was solved by the auditor by testing the group’s calculations for mine rehabilitation

provision at each time.

Reference:

Adenergy.com.au/, A. (2018). Annual reports | Newcrest Mining Limited. Retrieved from

http://www.newcrest.com.au/investors/reports/annual/

Asx.com.au (2018). Retrieved from

https://www.asx.com.au/asx/share-price-research/company/NCM/details

Czerney, K., Schmidt, J. J., & Thompson, A. M. (2014). Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

c Measuring firm performance using financial ratios: A decision tree approach. Expert Systems

with Applications, 40(10), 3970-3983.

Investing.com (2018). (NCM), N. Newcrest Mining (NCM) Financial Ratios. Retrieved from

https://www.investing.com/equities/newcrest-mining-limited-ratios

AUDIT AND ETHICS

The key audit matters of the company consists of many different matters, ranging from

assessment of the carrying value of assets. Here the auditor evaluated the group’s assessment of

the indicators of impairment or impairment reversal to address this. Multiple taxation is another

key audit matter, which required the attention of the auditors and was resolved by testing the

group’s calculations for tax provisions or tax receivables in each jurisdiction. Mine rehabilitation

provisions regarding the protection and responsibility of the environment is another matter,

which was solved by the auditor by testing the group’s calculations for mine rehabilitation

provision at each time.

Reference:

Adenergy.com.au/, A. (2018). Annual reports | Newcrest Mining Limited. Retrieved from

http://www.newcrest.com.au/investors/reports/annual/

Asx.com.au (2018). Retrieved from

https://www.asx.com.au/asx/share-price-research/company/NCM/details

Czerney, K., Schmidt, J. J., & Thompson, A. M. (2014). Does auditor explanatory language in

unqualified audit reports indicate increased financial misstatement risk?. The Accounting

Review, 89(6), 2115-2149.

c Measuring firm performance using financial ratios: A decision tree approach. Expert Systems

with Applications, 40(10), 3970-3983.

Investing.com (2018). (NCM), N. Newcrest Mining (NCM) Financial Ratios. Retrieved from

https://www.investing.com/equities/newcrest-mining-limited-ratios

11

AUDIT AND ETHICS

Liang, D., Lu, C. C., Tsai, C. F., & Shih, G. A. (2016). Financial ratios and corporate governance

indicators in bankruptcy prediction: A comprehensive study. European Journal of Operational

Research, 252(2), 561-572.

Lobo, G. J., & Zhao, Y. (2013). Relation between audit effort and financial report misstatements:

Evidence from quarterly and annual restatements. The Accounting Review, 88(4), 1385-1412.

Morningstar.com (2018) Income Statement for Newcrest Mining Ltd (NCM) from

Morningstar.com. . Retrieved from https://financials.morningstar.com/income-statement/is.html?

t=0P00006WQO&culture=en-US&ops=clear

Morningstar.com. (2018). Growth, Profitability, and Financial Ratios for Newcrest Mining Ltd

(NCM) from Morningstar.com. . Retrieved from http://financials.morningstar.com/ratios/r.html?

t=NCM

Marketwatch.com (2018). Newcrest Mining Ltd. Retrieved from

https://www.marketwatch.com/investing/stock/ncmgf/profile

Reuters.com (2018). Editorial, R. ${Instrument_CompanyName} ${Instrument_Ric} Financials

| Reuters.com. Retrieved from

https://www.reuters.com/finance/stocks/financial-highlights/NCM.AX

Simnett, R., & Huggins, A. (2014). Enhancing the auditor's report: to what extent is there support

for the IAASB's proposed changes?. Accounting Horizons, 28(4), 719-747.

Wsj.com (2018). NCM.AU Financial Statements - Newcrest Mining Ltd. - Wall Street Journal.

(2018). Retrieved from https://quotes.wsj.com/AU/XASX/NCM/financials

AUDIT AND ETHICS

Liang, D., Lu, C. C., Tsai, C. F., & Shih, G. A. (2016). Financial ratios and corporate governance

indicators in bankruptcy prediction: A comprehensive study. European Journal of Operational

Research, 252(2), 561-572.

Lobo, G. J., & Zhao, Y. (2013). Relation between audit effort and financial report misstatements:

Evidence from quarterly and annual restatements. The Accounting Review, 88(4), 1385-1412.

Morningstar.com (2018) Income Statement for Newcrest Mining Ltd (NCM) from

Morningstar.com. . Retrieved from https://financials.morningstar.com/income-statement/is.html?

t=0P00006WQO&culture=en-US&ops=clear

Morningstar.com. (2018). Growth, Profitability, and Financial Ratios for Newcrest Mining Ltd

(NCM) from Morningstar.com. . Retrieved from http://financials.morningstar.com/ratios/r.html?

t=NCM

Marketwatch.com (2018). Newcrest Mining Ltd. Retrieved from

https://www.marketwatch.com/investing/stock/ncmgf/profile

Reuters.com (2018). Editorial, R. ${Instrument_CompanyName} ${Instrument_Ric} Financials

| Reuters.com. Retrieved from

https://www.reuters.com/finance/stocks/financial-highlights/NCM.AX

Simnett, R., & Huggins, A. (2014). Enhancing the auditor's report: to what extent is there support

for the IAASB's proposed changes?. Accounting Horizons, 28(4), 719-747.

Wsj.com (2018). NCM.AU Financial Statements - Newcrest Mining Ltd. - Wall Street Journal.

(2018). Retrieved from https://quotes.wsj.com/AU/XASX/NCM/financials

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.