CQUniversity ACCT20075: Audit Report for Regis Resources Limited

VerifiedAdded on 2022/10/04

|13

|2785

|23

Report

AI Summary

This report presents an audit analysis of Regis Resources Limited, a publicly listed gold operation company. The report begins by examining materiality and the scope of the audit, including the calculation of planning materiality. It then delves into analytical procedures applied to the company's financial statements, focusing on liquidity, profitability, and leverage ratios. The analysis includes a review of the company's cash flow statement, highlighting key inflows and outflows. Finally, the report assesses the auditor's report, including compliance with regulations and key audit matters. The report aims to provide a comprehensive overview of the auditing process and the company's financial performance.

Running head: AUDIT

AUDIT

Name of the Student

Name of the University

Author Note

AUDIT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDIT

Table of Contents

Introduction................................................................................................................................3

Section 1.....................................................................................................................................3

Materiality and Scope of Audit..............................................................................................3

Review of Draft and disclosure..............................................................................................4

Section 2.....................................................................................................................................5

Analytical Procedure in Company.........................................................................................5

Section 3.....................................................................................................................................9

Analysis of Cash Flow Statement..........................................................................................9

Review of Auditor’s Report...................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

AUDIT

Table of Contents

Introduction................................................................................................................................3

Section 1.....................................................................................................................................3

Materiality and Scope of Audit..............................................................................................3

Review of Draft and disclosure..............................................................................................4

Section 2.....................................................................................................................................5

Analytical Procedure in Company.........................................................................................5

Section 3.....................................................................................................................................9

Analysis of Cash Flow Statement..........................................................................................9

Review of Auditor’s Report...................................................................................................9

Conclusion................................................................................................................................10

Reference..................................................................................................................................11

2

AUDIT

AUDIT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDIT

Introduction

Auditing help the company to gain proper analysing of their financial statement so

that this help them to give all the required information to all the financial user of the

company. Auditor have to check all the aspects of company so that it can know that the

company is able to perform all the activity properly and effectively in company business

(Coppage & Shastri 2014). This help the financial user to know the performance of the

company in business. Auditor have to carry many types of procedure which help it to know

about the different aspects of company so this can lead to give proper experience of

misstatement in regards of company business. The report deal with the company name Regis

Resources Limited which is ab public listed company and carry its business operation in gold

operation in the company, it mainly carry its business in Australia and Africa (DeFond &

Zhang 2014).

Section 1

Materiality and Scope of Audit

The purpose of this part it to show about the scope of audit and materiality which is

involve in company financial statement. The company is carrying different operation in gold

operation which involve high amount of complexity so this may also involve some kind of

error and omission in company business (Eilifsen & Messier Jr 2014). The report of the

company is been based in regards of the computation and analysis of the materiality involve

in company financial statement. The auditor have to ascertain all the materiality aspects in the

financial statement so it can give proper amount of opinion in regards of company financial

information. This information which the auditor is able to get help it to know about the

process which it to follow in the audit process of the company. It also able to analysis the

AUDIT

Introduction

Auditing help the company to gain proper analysing of their financial statement so

that this help them to give all the required information to all the financial user of the

company. Auditor have to check all the aspects of company so that it can know that the

company is able to perform all the activity properly and effectively in company business

(Coppage & Shastri 2014). This help the financial user to know the performance of the

company in business. Auditor have to carry many types of procedure which help it to know

about the different aspects of company so this can lead to give proper experience of

misstatement in regards of company business. The report deal with the company name Regis

Resources Limited which is ab public listed company and carry its business operation in gold

operation in the company, it mainly carry its business in Australia and Africa (DeFond &

Zhang 2014).

Section 1

Materiality and Scope of Audit

The purpose of this part it to show about the scope of audit and materiality which is

involve in company financial statement. The company is carrying different operation in gold

operation which involve high amount of complexity so this may also involve some kind of

error and omission in company business (Eilifsen & Messier Jr 2014). The report of the

company is been based in regards of the computation and analysis of the materiality involve

in company financial statement. The auditor have to ascertain all the materiality aspects in the

financial statement so it can give proper amount of opinion in regards of company financial

information. This information which the auditor is able to get help it to know about the

process which it to follow in the audit process of the company. It also able to analysis the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDIT

planning materiality so that the company is able to gain proper knowledge in regards of

financial statement, it should consider the same in company business (Elder et al., 2013).

Materiality concept is to taken very seriously so that the auditor able to know the risk

which is associated in the company financial statement. Company should able to give proper

assumption and estimation which they have taken in regards of its business operation.

Auditor should plan the materiality in the planning stage so that it can base the same to

assertion the amount of audit process which it to carry in the business operation. The auditor

have to plan the amount of, materiality which is involve in the same so that it can know how

much risk is associated in the business. It should take into consideration the sales, equity and

total asset while calculating the planning materiality in the business (Furnham & Gunter

2015). Planning Materiality shall be computed upon the highest figure in the business as it

should consider the total asset figure in company so that the auditor is able to know the

misstatement in the company. So the calculation of planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 822530

¿ 5 %

¿ $ 41126.5

The above calculation show about the planning materiality in the company as it is

$41126.5 so this should be consider by the auditor in regards of company financial statement

so that the it can know the risk which is associated by the company and how the auditor is

able to carry different procedure in company business activities.

AUDIT

planning materiality so that the company is able to gain proper knowledge in regards of

financial statement, it should consider the same in company business (Elder et al., 2013).

Materiality concept is to taken very seriously so that the auditor able to know the risk

which is associated in the company financial statement. Company should able to give proper

assumption and estimation which they have taken in regards of its business operation.

Auditor should plan the materiality in the planning stage so that it can base the same to

assertion the amount of audit process which it to carry in the business operation. The auditor

have to plan the amount of, materiality which is involve in the same so that it can know how

much risk is associated in the business. It should take into consideration the sales, equity and

total asset while calculating the planning materiality in the business (Furnham & Gunter

2015). Planning Materiality shall be computed upon the highest figure in the business as it

should consider the total asset figure in company so that the auditor is able to know the

misstatement in the company. So the calculation of planning materiality is shown below:

Planning Materiality=Total Asset∗5 %

¿ $ 822530

¿ 5 %

¿ $ 41126.5

The above calculation show about the planning materiality in the company as it is

$41126.5 so this should be consider by the auditor in regards of company financial statement

so that the it can know the risk which is associated by the company and how the auditor is

able to carry different procedure in company business activities.

5

AUDIT

Review of Draft and disclosure

The company should able to carry many assumptions in the company business so this

the auditor should able to analysis the company information and see whether all the

requirement which are there are meant by the auditor or not (Goh, Krishnan & Li 2013). It

should analysis each aspects of company disclosure so that this will help the company to gain

more amount of advantage in company financial statement. Auditor is not able to find proper

disclosure than it should record the same in the company annual report and should also base

its opinion upon the company financial statement.

Section 2

Analytical Procedure in Company

Auditor have to analysis the company financial statement properly so that it can able

to give proper opinion upon the company financial statement. It should carry financial

analysis in company as the auditor is able to know the company performance with the help of

financial ratio of the company. The financial ratio help the company to know about the

different aspects and also show how the company is carrying its activities in the business.

Liquidity Ratio

This ratio show about the company liquidity position in the business as it take into

consideration how the company is able to pay short term liability with the help of liquidity

asset. It show the proper liquidity position of company financial statement as if company is

having good liquidity position so this signify that the company is able to carry its operation

more easily and effectively in business (Griffiths 2016). The ratio is divided into three parts

as current ratio, quick ratio and cash ratio.

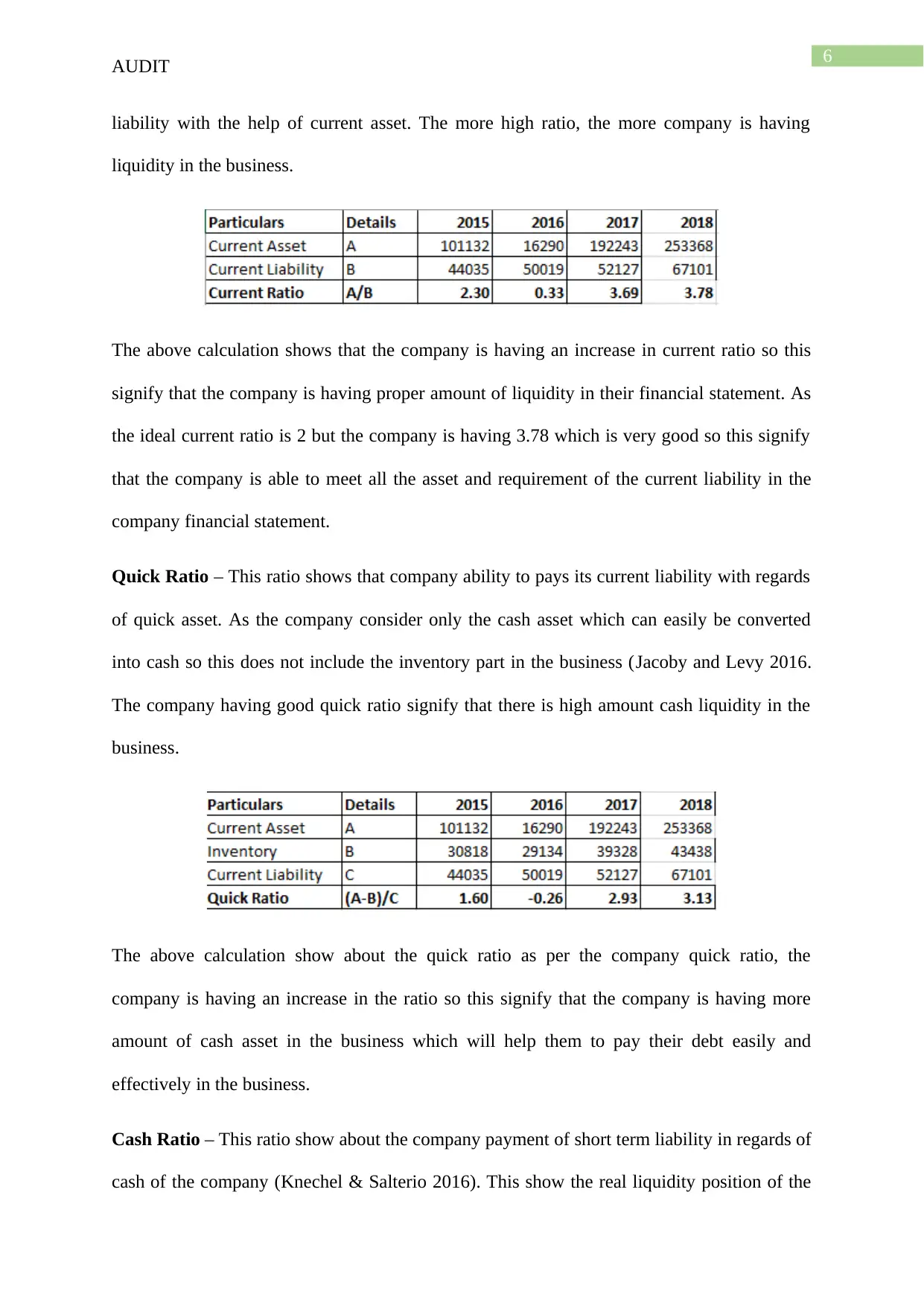

Current Ratio – This ratio show about the company paying capabilities in regards of its

current liability with current asset. This ratio show how the company is able to pay its current

AUDIT

Review of Draft and disclosure

The company should able to carry many assumptions in the company business so this

the auditor should able to analysis the company information and see whether all the

requirement which are there are meant by the auditor or not (Goh, Krishnan & Li 2013). It

should analysis each aspects of company disclosure so that this will help the company to gain

more amount of advantage in company financial statement. Auditor is not able to find proper

disclosure than it should record the same in the company annual report and should also base

its opinion upon the company financial statement.

Section 2

Analytical Procedure in Company

Auditor have to analysis the company financial statement properly so that it can able

to give proper opinion upon the company financial statement. It should carry financial

analysis in company as the auditor is able to know the company performance with the help of

financial ratio of the company. The financial ratio help the company to know about the

different aspects and also show how the company is carrying its activities in the business.

Liquidity Ratio

This ratio show about the company liquidity position in the business as it take into

consideration how the company is able to pay short term liability with the help of liquidity

asset. It show the proper liquidity position of company financial statement as if company is

having good liquidity position so this signify that the company is able to carry its operation

more easily and effectively in business (Griffiths 2016). The ratio is divided into three parts

as current ratio, quick ratio and cash ratio.

Current Ratio – This ratio show about the company paying capabilities in regards of its

current liability with current asset. This ratio show how the company is able to pay its current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDIT

liability with the help of current asset. The more high ratio, the more company is having

liquidity in the business.

The above calculation shows that the company is having an increase in current ratio so this

signify that the company is having proper amount of liquidity in their financial statement. As

the ideal current ratio is 2 but the company is having 3.78 which is very good so this signify

that the company is able to meet all the asset and requirement of the current liability in the

company financial statement.

Quick Ratio – This ratio shows that company ability to pays its current liability with regards

of quick asset. As the company consider only the cash asset which can easily be converted

into cash so this does not include the inventory part in the business (Jacoby and Levy 2016.

The company having good quick ratio signify that there is high amount cash liquidity in the

business.

The above calculation show about the quick ratio as per the company quick ratio, the

company is having an increase in the ratio so this signify that the company is having more

amount of cash asset in the business which will help them to pay their debt easily and

effectively in the business.

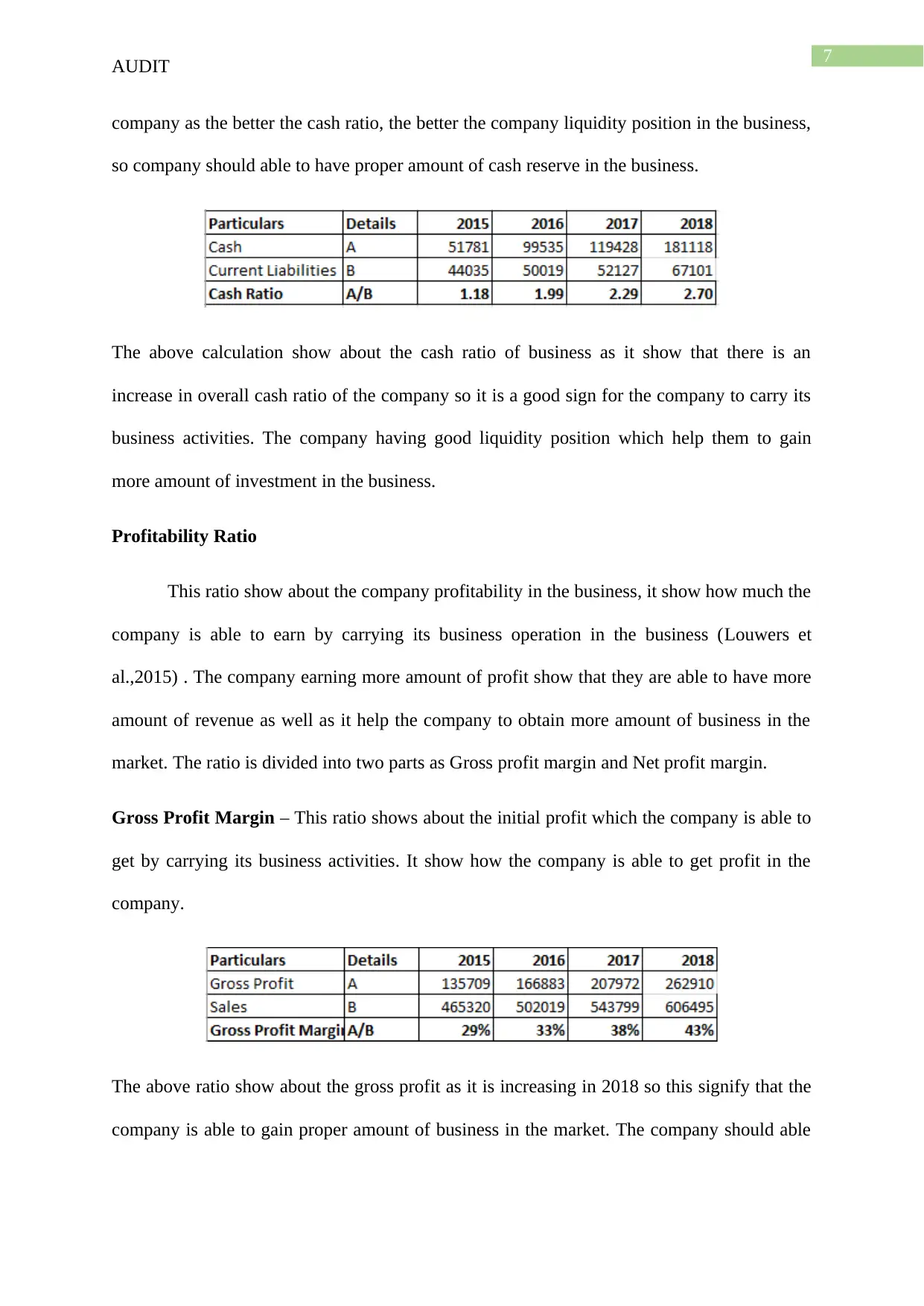

Cash Ratio – This ratio show about the company payment of short term liability in regards of

cash of the company (Knechel & Salterio 2016). This show the real liquidity position of the

AUDIT

liability with the help of current asset. The more high ratio, the more company is having

liquidity in the business.

The above calculation shows that the company is having an increase in current ratio so this

signify that the company is having proper amount of liquidity in their financial statement. As

the ideal current ratio is 2 but the company is having 3.78 which is very good so this signify

that the company is able to meet all the asset and requirement of the current liability in the

company financial statement.

Quick Ratio – This ratio shows that company ability to pays its current liability with regards

of quick asset. As the company consider only the cash asset which can easily be converted

into cash so this does not include the inventory part in the business (Jacoby and Levy 2016.

The company having good quick ratio signify that there is high amount cash liquidity in the

business.

The above calculation show about the quick ratio as per the company quick ratio, the

company is having an increase in the ratio so this signify that the company is having more

amount of cash asset in the business which will help them to pay their debt easily and

effectively in the business.

Cash Ratio – This ratio show about the company payment of short term liability in regards of

cash of the company (Knechel & Salterio 2016). This show the real liquidity position of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDIT

company as the better the cash ratio, the better the company liquidity position in the business,

so company should able to have proper amount of cash reserve in the business.

The above calculation show about the cash ratio of business as it show that there is an

increase in overall cash ratio of the company so it is a good sign for the company to carry its

business activities. The company having good liquidity position which help them to gain

more amount of investment in the business.

Profitability Ratio

This ratio show about the company profitability in the business, it show how much the

company is able to earn by carrying its business operation in the business (Louwers et

al.,2015) . The company earning more amount of profit show that they are able to have more

amount of revenue as well as it help the company to obtain more amount of business in the

market. The ratio is divided into two parts as Gross profit margin and Net profit margin.

Gross Profit Margin – This ratio shows about the initial profit which the company is able to

get by carrying its business activities. It show how the company is able to get profit in the

company.

The above ratio show about the gross profit as it is increasing in 2018 so this signify that the

company is able to gain proper amount of business in the market. The company should able

AUDIT

company as the better the cash ratio, the better the company liquidity position in the business,

so company should able to have proper amount of cash reserve in the business.

The above calculation show about the cash ratio of business as it show that there is an

increase in overall cash ratio of the company so it is a good sign for the company to carry its

business activities. The company having good liquidity position which help them to gain

more amount of investment in the business.

Profitability Ratio

This ratio show about the company profitability in the business, it show how much the

company is able to earn by carrying its business operation in the business (Louwers et

al.,2015) . The company earning more amount of profit show that they are able to have more

amount of revenue as well as it help the company to obtain more amount of business in the

market. The ratio is divided into two parts as Gross profit margin and Net profit margin.

Gross Profit Margin – This ratio shows about the initial profit which the company is able to

get by carrying its business activities. It show how the company is able to get profit in the

company.

The above ratio show about the gross profit as it is increasing in 2018 so this signify that the

company is able to gain proper amount of business in the market. The company should able

8

AUDIT

to have proper business so this will help them to gain more amount of investment in the

company business.

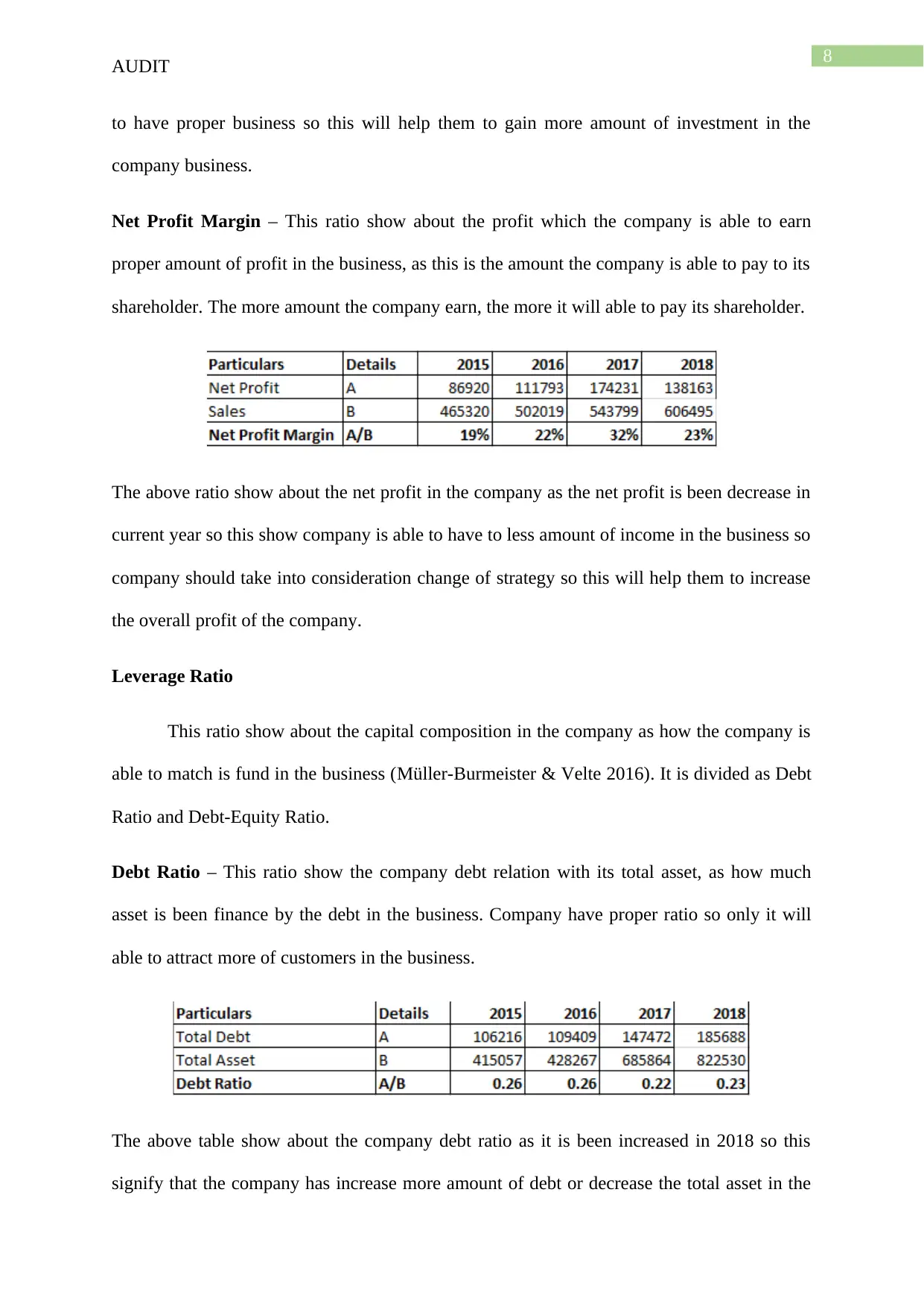

Net Profit Margin – This ratio show about the profit which the company is able to earn

proper amount of profit in the business, as this is the amount the company is able to pay to its

shareholder. The more amount the company earn, the more it will able to pay its shareholder.

The above ratio show about the net profit in the company as the net profit is been decrease in

current year so this show company is able to have to less amount of income in the business so

company should take into consideration change of strategy so this will help them to increase

the overall profit of the company.

Leverage Ratio

This ratio show about the capital composition in the company as how the company is

able to match is fund in the business (Müller-Burmeister & Velte 2016). It is divided as Debt

Ratio and Debt-Equity Ratio.

Debt Ratio – This ratio show the company debt relation with its total asset, as how much

asset is been finance by the debt in the business. Company have proper ratio so only it will

able to attract more of customers in the business.

The above table show about the company debt ratio as it is been increased in 2018 so this

signify that the company has increase more amount of debt or decrease the total asset in the

AUDIT

to have proper business so this will help them to gain more amount of investment in the

company business.

Net Profit Margin – This ratio show about the profit which the company is able to earn

proper amount of profit in the business, as this is the amount the company is able to pay to its

shareholder. The more amount the company earn, the more it will able to pay its shareholder.

The above ratio show about the net profit in the company as the net profit is been decrease in

current year so this show company is able to have to less amount of income in the business so

company should take into consideration change of strategy so this will help them to increase

the overall profit of the company.

Leverage Ratio

This ratio show about the capital composition in the company as how the company is

able to match is fund in the business (Müller-Burmeister & Velte 2016). It is divided as Debt

Ratio and Debt-Equity Ratio.

Debt Ratio – This ratio show the company debt relation with its total asset, as how much

asset is been finance by the debt in the business. Company have proper ratio so only it will

able to attract more of customers in the business.

The above table show about the company debt ratio as it is been increased in 2018 so this

signify that the company has increase more amount of debt or decrease the total asset in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDIT

business. Company should able to manage properly the debt and asset composition in the

business.

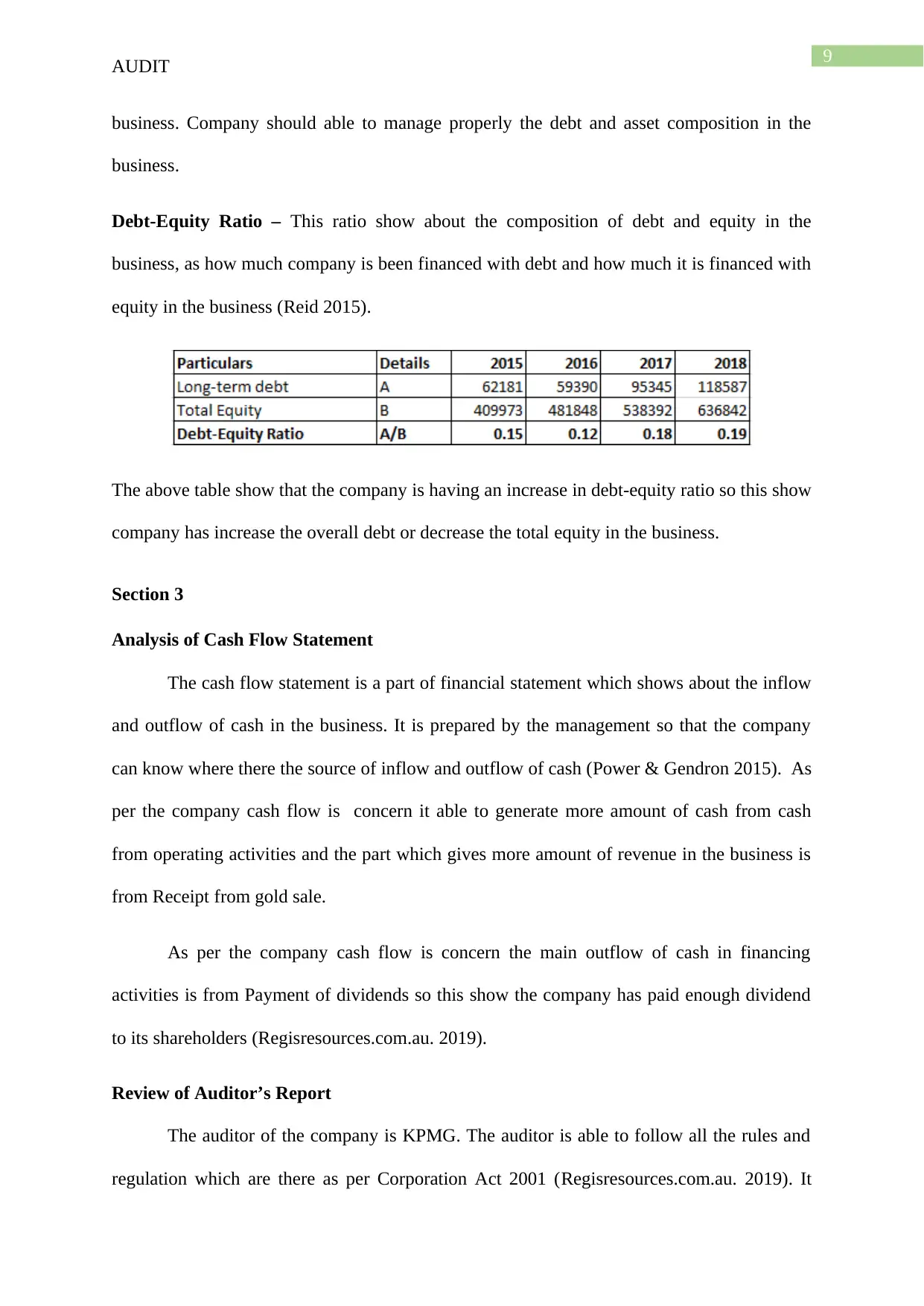

Debt-Equity Ratio – This ratio show about the composition of debt and equity in the

business, as how much company is been financed with debt and how much it is financed with

equity in the business (Reid 2015).

The above table show that the company is having an increase in debt-equity ratio so this show

company has increase the overall debt or decrease the total equity in the business.

Section 3

Analysis of Cash Flow Statement

The cash flow statement is a part of financial statement which shows about the inflow

and outflow of cash in the business. It is prepared by the management so that the company

can know where there the source of inflow and outflow of cash (Power & Gendron 2015). As

per the company cash flow is concern it able to generate more amount of cash from cash

from operating activities and the part which gives more amount of revenue in the business is

from Receipt from gold sale.

As per the company cash flow is concern the main outflow of cash in financing

activities is from Payment of dividends so this show the company has paid enough dividend

to its shareholders (Regisresources.com.au. 2019).

Review of Auditor’s Report

The auditor of the company is KPMG. The auditor is able to follow all the rules and

regulation which are there as per Corporation Act 2001 (Regisresources.com.au. 2019). It

AUDIT

business. Company should able to manage properly the debt and asset composition in the

business.

Debt-Equity Ratio – This ratio show about the composition of debt and equity in the

business, as how much company is been financed with debt and how much it is financed with

equity in the business (Reid 2015).

The above table show that the company is having an increase in debt-equity ratio so this show

company has increase the overall debt or decrease the total equity in the business.

Section 3

Analysis of Cash Flow Statement

The cash flow statement is a part of financial statement which shows about the inflow

and outflow of cash in the business. It is prepared by the management so that the company

can know where there the source of inflow and outflow of cash (Power & Gendron 2015). As

per the company cash flow is concern it able to generate more amount of cash from cash

from operating activities and the part which gives more amount of revenue in the business is

from Receipt from gold sale.

As per the company cash flow is concern the main outflow of cash in financing

activities is from Payment of dividends so this show the company has paid enough dividend

to its shareholders (Regisresources.com.au. 2019).

Review of Auditor’s Report

The auditor of the company is KPMG. The auditor is able to follow all the rules and

regulation which are there as per Corporation Act 2001 (Regisresources.com.au. 2019). It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDIT

show that the company is able to follow all the required rules and show that the company is

having true and fair or not. It able have no material misstatement in company financial

statement.

Auditor is able to give key audit matter in the company annual report. This are the

matter which the auditor able to give in auditor report so that the user can know the risk

which are associated in the company financial activities.

Conclusion

The report concludes about the auditing process in the company as how the company

is able to carry its financial information to the user. The report show about the auditing

process in then business as how the auditor is able to carry different process in the business.

The first part of the report show about the materiality and scope of audit in the business as

how the auditor is able to ascertain the materiality in the company business. It also show

about the analytical procedure which the auditor have to follow in regards of company

financial statement in the business. It show about the financial ratio and show how the

company is able to have proper financial performance in the business. Lastly the report show

about the analysis of company cash flow statement and auditor report of the company.

AUDIT

show that the company is able to follow all the required rules and show that the company is

having true and fair or not. It able have no material misstatement in company financial

statement.

Auditor is able to give key audit matter in the company annual report. This are the

matter which the auditor able to give in auditor report so that the user can know the risk

which are associated in the company financial activities.

Conclusion

The report concludes about the auditing process in the company as how the company

is able to carry its financial information to the user. The report show about the auditing

process in then business as how the auditor is able to carry different process in the business.

The first part of the report show about the materiality and scope of audit in the business as

how the auditor is able to ascertain the materiality in the company business. It also show

about the analytical procedure which the auditor have to follow in regards of company

financial statement in the business. It show about the financial ratio and show how the

company is able to have proper financial performance in the business. Lastly the report show

about the analysis of company cash flow statement and auditor report of the company.

11

AUDIT

Reference

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

AUDIT

Reference

Coppage, R., & Shastri, T. (2014). Effectively Applying Professional Skepticism to Improve

Audit Quality. The CPA Journal, 84(8), 24.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Elder, R. J., Akresh, A. D., Glover, S. M., Higgs, J. L., & Liljegren, J. (2013). Audit sampling

research: A synthesis and implications for future research. Auditing: A Journal of

Practice & Theory, 32(sp1), 99-129.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Goh, B. W., Krishnan, J., & Li, D. (2013). Auditor reporting under Section 404: The

association between the internal control and going concern audit

opinions. Contemporary Accounting Research, 30(3), 970-995.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Jacoby, J. and Levy, H.B., 2016. The materiality mystery. The CPA Journal, 86(7), p.14.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Louwers, T. J., Ramsay, R. J., Sinason, D. H., Strawser, J. R., & Thibodeau, J. C.

(2015). Auditing & assurance services. McGraw-Hill Education.

Müller-Burmeister, C., & Velte, P. (2016). Increased materiality judgments in financial

accounting and external audit: a critical comparison between German and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.