ACCG925 - Individual Assignment: Audit Report Changes & Impact

VerifiedAdded on 2020/02/23

|10

|1354

|264

Report

AI Summary

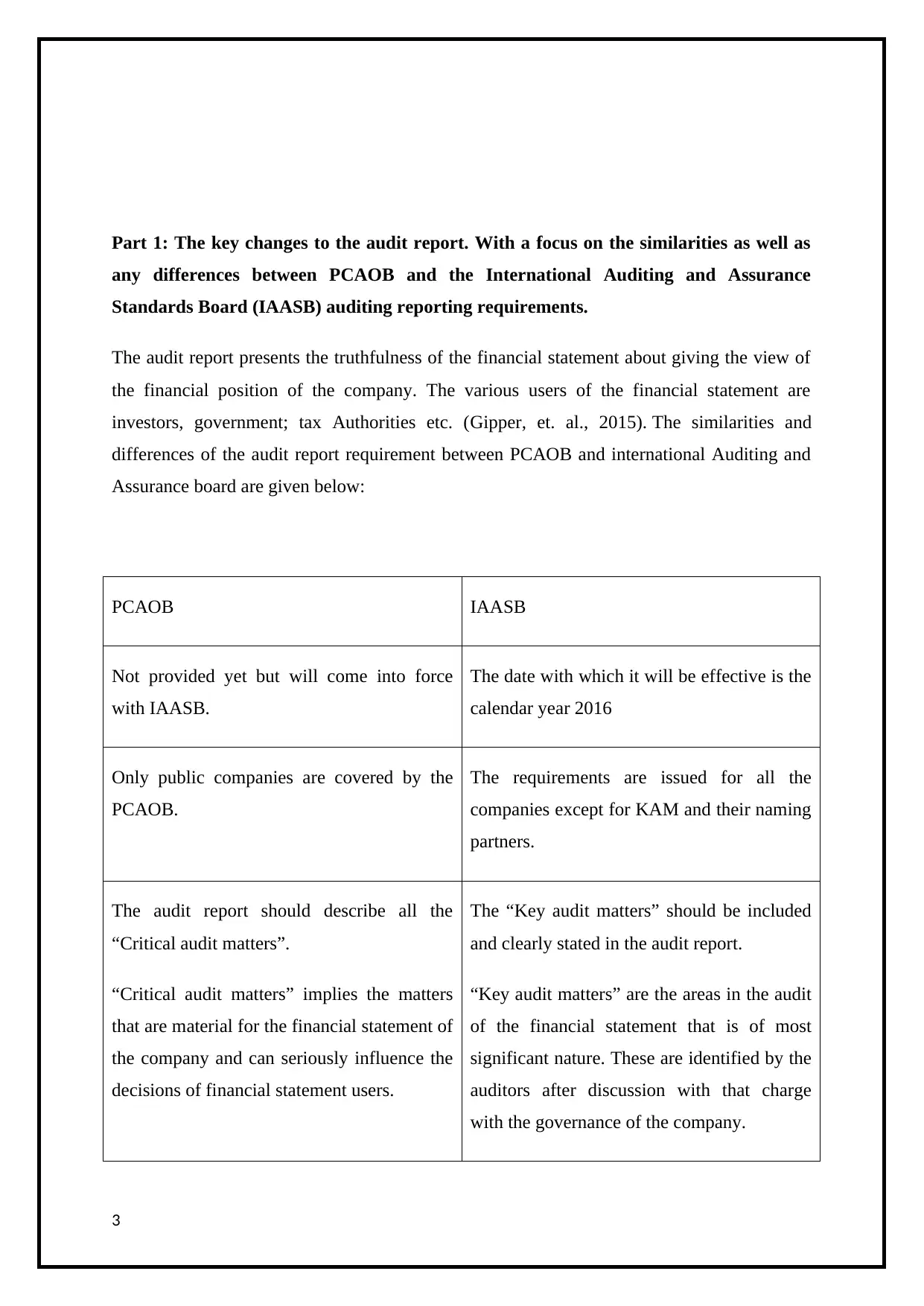

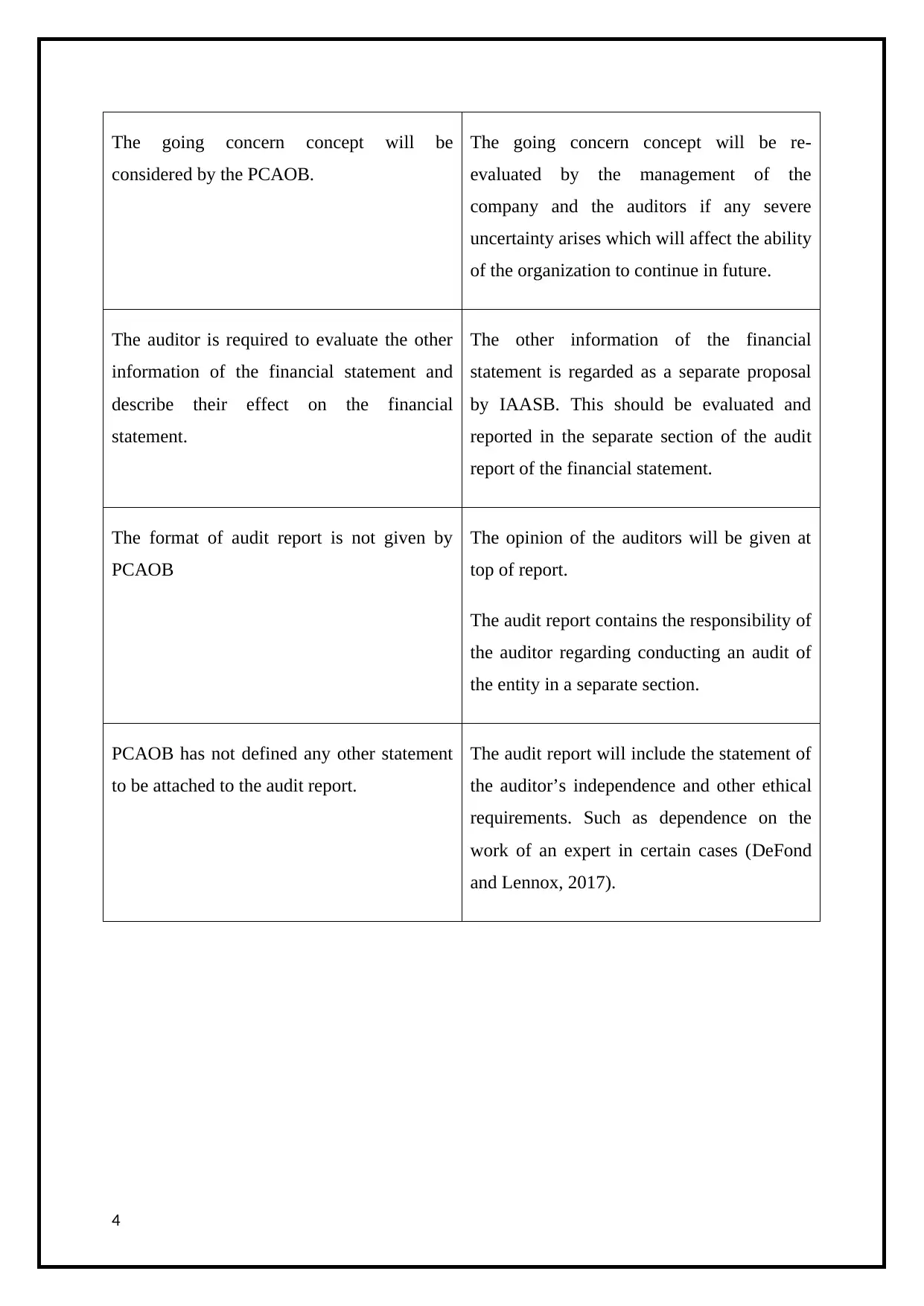

This report analyzes the key changes in audit reporting, focusing on the similarities and differences between the requirements of the Public Company Accounting Oversight Board (PCAOB) and the International Auditing and Assurance Standards Board (IAASB). It examines the introduction of Key Audit Matters (KAM) and Critical Audit Matters, the treatment of going concern concepts, and the presentation of other financial information. The report explains the motivations behind these changes, aiming to increase transparency, and critiques their potential to achieve their objectives. Finally, it outlines the likely impact of these changes on audit practice, emphasizing the need for auditors to provide clearer, more informative reports that are easily understood by various stakeholders, including investors and the general public. The report references relevant literature to support its analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.