Audit, Assurance and Compliance Report: Case Study Analysis, DIPL

VerifiedAdded on 2020/03/01

|9

|2101

|392

Report

AI Summary

This report analyzes the audit, assurance, and compliance aspects of a case study. It begins by identifying relevant audit plans based on the evaluation of the case study of DIPL, and how results could influence audit procedures. The report then depicts different risks and their impact on material misstatements, including inheritance risk arising from issues like employee pressure and ineffective management. The report also mentions key fraud risks, such as employee manipulation and financial report manipulation. Finally, it outlines how these identified fraud risks could lead to specific audit procedures. The analysis includes financial ratio evaluations and their implications for the company's performance, as well as a discussion of potential corrective measures. The report uses various academic sources to support its findings, including studies on audit procedures and risk assessment.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

1

Table of Contents

Answer to Question 1: Mentioning how results could influence audit procedures...................2

Answer to Question 2: Depicting different risk and its impact on material misstatement........4

Answer to Question 3a: Mentioning two key fraud risk............................................................5

Answer to Question 3b: Mentioning how identified fraud risk could lead to audit...................7

Reference:..................................................................................................................................8

1

Table of Contents

Answer to Question 1: Mentioning how results could influence audit procedures...................2

Answer to Question 2: Depicting different risk and its impact on material misstatement........4

Answer to Question 3a: Mentioning two key fraud risk............................................................5

Answer to Question 3b: Mentioning how identified fraud risk could lead to audit...................7

Reference:..................................................................................................................................8

AUDIT, ASSURANCE AND COMPLIANCE

2

Answer to Question 1: Mentioning how results could influence audit procedures

From the evaluation of the case study of DIPL relevant audit plans could be

identified, which might be used in evaluating the financial information of the company. The

relevant analytical approach could be used in identifying the overall financial trend, which

might be used in identifying the overall needs for an audit operation. Baylis et al. (2017)

stated that with the help of audit procedures organisation are able to identify the minimum

expenses needed for completing the audit procedure. Furthermore, relevant analytical

approach can be used in identifying the overall financial trend of DIPL. The overall use of

common sized analytical approach could directly allow the analyst to use the approach for

analysing the overall financial reports declared by the organisation.

The use of relevant analytical approach such as ratios and benchmarking could be

identified as the viable approach for analysing performance of DIPL. In addition, the use of

benchmarking could directly help in identifying the overall financial stability of the

organisation. The use of benchmarking could directly allow the analyst to evaluate the overall

financial performance of the organisation, where relevant problems in operations could be

identified. Moreover, relevant ratios could also be used in the analytical approach, where it

might directly compare returns of the company with its previous fiscal year. Duncan and

Whittington (2014) mentioned that ratios mainly allow the organisation to identify the

relevant trend in the overall financial report, which could help in detecting the overall

progress and decline in the financial stability of an organisation. Therefore, ratios are mainly

used as the overall analytical approach for evaluating the performance of the DIPL in the

three fiscal years.

Particulars 2013 2014 2015

Net profit 2,359,190 2,291,362 2,972,183

2

Answer to Question 1: Mentioning how results could influence audit procedures

From the evaluation of the case study of DIPL relevant audit plans could be

identified, which might be used in evaluating the financial information of the company. The

relevant analytical approach could be used in identifying the overall financial trend, which

might be used in identifying the overall needs for an audit operation. Baylis et al. (2017)

stated that with the help of audit procedures organisation are able to identify the minimum

expenses needed for completing the audit procedure. Furthermore, relevant analytical

approach can be used in identifying the overall financial trend of DIPL. The overall use of

common sized analytical approach could directly allow the analyst to use the approach for

analysing the overall financial reports declared by the organisation.

The use of relevant analytical approach such as ratios and benchmarking could be

identified as the viable approach for analysing performance of DIPL. In addition, the use of

benchmarking could directly help in identifying the overall financial stability of the

organisation. The use of benchmarking could directly allow the analyst to evaluate the overall

financial performance of the organisation, where relevant problems in operations could be

identified. Moreover, relevant ratios could also be used in the analytical approach, where it

might directly compare returns of the company with its previous fiscal year. Duncan and

Whittington (2014) mentioned that ratios mainly allow the organisation to identify the

relevant trend in the overall financial report, which could help in detecting the overall

progress and decline in the financial stability of an organisation. Therefore, ratios are mainly

used as the overall analytical approach for evaluating the performance of the DIPL in the

three fiscal years.

Particulars 2013 2014 2015

Net profit 2,359,190 2,291,362 2,972,183

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE

3

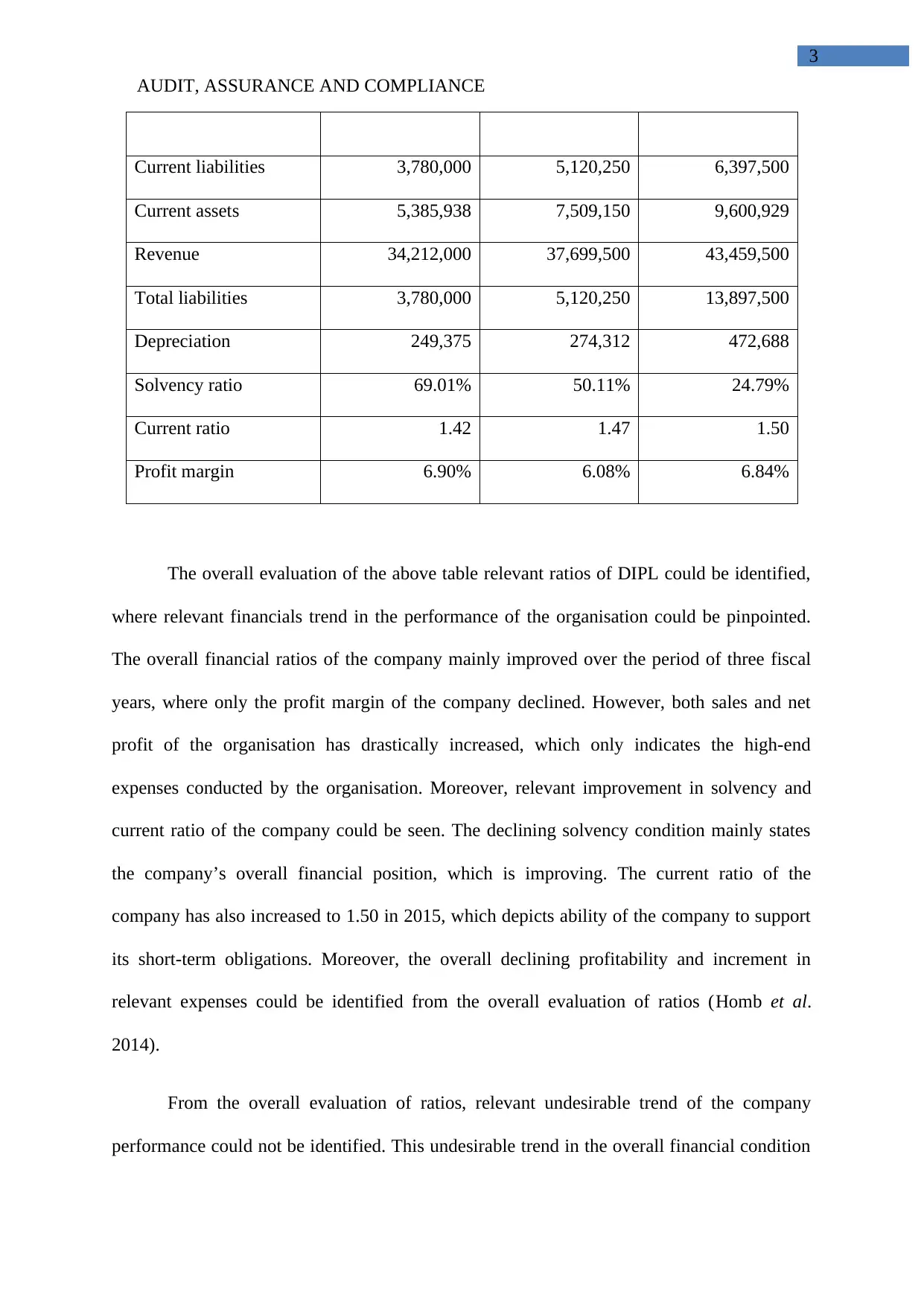

Current liabilities 3,780,000 5,120,250 6,397,500

Current assets 5,385,938 7,509,150 9,600,929

Revenue 34,212,000 37,699,500 43,459,500

Total liabilities 3,780,000 5,120,250 13,897,500

Depreciation 249,375 274,312 472,688

Solvency ratio 69.01% 50.11% 24.79%

Current ratio 1.42 1.47 1.50

Profit margin 6.90% 6.08% 6.84%

The overall evaluation of the above table relevant ratios of DIPL could be identified,

where relevant financials trend in the performance of the organisation could be pinpointed.

The overall financial ratios of the company mainly improved over the period of three fiscal

years, where only the profit margin of the company declined. However, both sales and net

profit of the organisation has drastically increased, which only indicates the high-end

expenses conducted by the organisation. Moreover, relevant improvement in solvency and

current ratio of the company could be seen. The declining solvency condition mainly states

the company’s overall financial position, which is improving. The current ratio of the

company has also increased to 1.50 in 2015, which depicts ability of the company to support

its short-term obligations. Moreover, the overall declining profitability and increment in

relevant expenses could be identified from the overall evaluation of ratios (Homb et al.

2014).

From the overall evaluation of ratios, relevant undesirable trend of the company

performance could not be identified. This undesirable trend in the overall financial condition

3

Current liabilities 3,780,000 5,120,250 6,397,500

Current assets 5,385,938 7,509,150 9,600,929

Revenue 34,212,000 37,699,500 43,459,500

Total liabilities 3,780,000 5,120,250 13,897,500

Depreciation 249,375 274,312 472,688

Solvency ratio 69.01% 50.11% 24.79%

Current ratio 1.42 1.47 1.50

Profit margin 6.90% 6.08% 6.84%

The overall evaluation of the above table relevant ratios of DIPL could be identified,

where relevant financials trend in the performance of the organisation could be pinpointed.

The overall financial ratios of the company mainly improved over the period of three fiscal

years, where only the profit margin of the company declined. However, both sales and net

profit of the organisation has drastically increased, which only indicates the high-end

expenses conducted by the organisation. Moreover, relevant improvement in solvency and

current ratio of the company could be seen. The declining solvency condition mainly states

the company’s overall financial position, which is improving. The current ratio of the

company has also increased to 1.50 in 2015, which depicts ability of the company to support

its short-term obligations. Moreover, the overall declining profitability and increment in

relevant expenses could be identified from the overall evaluation of ratios (Homb et al.

2014).

From the overall evaluation of ratios, relevant undesirable trend of the company

performance could not be identified. This undesirable trend in the overall financial condition

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

4

of DIPL is mainly identified from the evaluation of ratios. The ratio evaluation mainly helps

in identifying the overall position where the company’s operations are desirable or not could

be identified. Therefore, adequate corrective measures need to be conducted by the

management of DIPL for identifying the current financial position of the company. This

mainly helps in identifying the needs for relevant audit procedures needed by the organisation

(Hut-Mossel et al. 2017).

Answer to Question 2: Depicting different risk and its impact on material misstatement

The evaluation of the overall case study of DIPL mainly helps in pin pointing the

relevant risk, which is directly increasing the chance of material misstatement. The two

different type of material misstatement risk could be identified, which could directly increase

the inheritance risk of DIPL. The first risk of inheritance can be portrayed from the omission

in the record keeping where the employee of the organisation did not conduct relevant

transactions. The management mainly needed a new system, which increased pressure on the

employees to covert the transaction and relevant use the system at short durations. This

increased pressure on the employees could directly increase the overall misstatement risk,

which could directly increase organisations inherence risk. There are relevant problem, which

could be identified from the overall evaluation of the case study. The current employee that is

maintained by the company is not relevant for the finance department, which is increasing the

overall misstatements in the organisation (Schmidt, Wood and Grabski 2016).

Moreover, the company has also failed achieve the targeted profits, where the

management is mainly responsible. The management was not putting all the relevant input in

the business for supporting the activities and achieving the targeted goals. The lack of

integrity and motivation level in management was relevantly low, which is directly affecting

the overall performance of the organisation. In addition, the relevant complexities could be

4

of DIPL is mainly identified from the evaluation of ratios. The ratio evaluation mainly helps

in identifying the overall position where the company’s operations are desirable or not could

be identified. Therefore, adequate corrective measures need to be conducted by the

management of DIPL for identifying the current financial position of the company. This

mainly helps in identifying the needs for relevant audit procedures needed by the organisation

(Hut-Mossel et al. 2017).

Answer to Question 2: Depicting different risk and its impact on material misstatement

The evaluation of the overall case study of DIPL mainly helps in pin pointing the

relevant risk, which is directly increasing the chance of material misstatement. The two

different type of material misstatement risk could be identified, which could directly increase

the inheritance risk of DIPL. The first risk of inheritance can be portrayed from the omission

in the record keeping where the employee of the organisation did not conduct relevant

transactions. The management mainly needed a new system, which increased pressure on the

employees to covert the transaction and relevant use the system at short durations. This

increased pressure on the employees could directly increase the overall misstatement risk,

which could directly increase organisations inherence risk. There are relevant problem, which

could be identified from the overall evaluation of the case study. The current employee that is

maintained by the company is not relevant for the finance department, which is increasing the

overall misstatements in the organisation (Schmidt, Wood and Grabski 2016).

Moreover, the company has also failed achieve the targeted profits, where the

management is mainly responsible. The management was not putting all the relevant input in

the business for supporting the activities and achieving the targeted goals. The lack of

integrity and motivation level in management was relevantly low, which is directly affecting

the overall performance of the organisation. In addition, the relevant complexities could be

AUDIT, ASSURANCE AND COMPLIANCE

5

identified from selection process that was used by the management in promoting a new CEO.

This ineffective process of the management could directly affect the overall inheritance risk

of the organisation, which could in turn hamper relevant problems faced by the company.

Furthermore, there is relevantly low employees, which is been employed by the organisation

in changing the overall accounting system. This could directly increase the overall

manipulations and material misstatements, which in turn could increase the inheritance risk

of the organisation. Shafii, Abidin and Salleh (2015) mentioned that the overall increment in

the inheritance risk could increase the implementation of audit report for identify the overall

financial condition of the company.

Therefore, from the evaluation it could be understood that there is excessive

workloads on the employees, as new accounting system is been imposed by the organisation.

This excessive pressure has mainly increased the chance of material misstatement and

omission of relevant transaction in the financial report. Moreover, there are relevant issues in

the poor booking system, which could directly affect the overall financial report of the

organisation. Thus, the organisation is mainly portrayed high-end incentives to its

management, which raise the unethical concern that might increase material misstatement

affecting its financial report.

Answer to Question 3a: Mentioning two key fraud risk

There are relevant different types of risk, which could hamper operation of the

company and increase its material misstatement. The overall risk such as fraudulent activities

risk and financial misstatement risk are mainly identified from the overall case study. The

explanations of the overall risks are mainly depicted as follows.

Fraudulent

activities of the

The overall fraudulent activities are mainly detected from the

employees of DIPL, where the workforce of the organisation is mainly

5

identified from selection process that was used by the management in promoting a new CEO.

This ineffective process of the management could directly affect the overall inheritance risk

of the organisation, which could in turn hamper relevant problems faced by the company.

Furthermore, there is relevantly low employees, which is been employed by the organisation

in changing the overall accounting system. This could directly increase the overall

manipulations and material misstatements, which in turn could increase the inheritance risk

of the organisation. Shafii, Abidin and Salleh (2015) mentioned that the overall increment in

the inheritance risk could increase the implementation of audit report for identify the overall

financial condition of the company.

Therefore, from the evaluation it could be understood that there is excessive

workloads on the employees, as new accounting system is been imposed by the organisation.

This excessive pressure has mainly increased the chance of material misstatement and

omission of relevant transaction in the financial report. Moreover, there are relevant issues in

the poor booking system, which could directly affect the overall financial report of the

organisation. Thus, the organisation is mainly portrayed high-end incentives to its

management, which raise the unethical concern that might increase material misstatement

affecting its financial report.

Answer to Question 3a: Mentioning two key fraud risk

There are relevant different types of risk, which could hamper operation of the

company and increase its material misstatement. The overall risk such as fraudulent activities

risk and financial misstatement risk are mainly identified from the overall case study. The

explanations of the overall risks are mainly depicted as follows.

Fraudulent

activities of the

The overall fraudulent activities are mainly detected from the

employees of DIPL, where the workforce of the organisation is mainly

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT, ASSURANCE AND COMPLIANCE

6

employees manipulating relevant transactions. Management mainly forced the

employees to use the new counting machine, which increased relevant

pressure. Thus, it is determined that overall manipulations conducted

with employee for directly increases the material misstatement in the

financial report of the organization. Fraudulent activities used by the

employees in completing the change in accounting software would it

increase the material misstatement and increase the inheritance risk.

Furthermore, there was relevantly minimum workforce present in the

organization, with relevant low experience and efficiency. This mainly

increase the chance of material misstatement, employees will not be

able to adequately record all the transactions conducted by the

organization (Thaweejinda and Senivongse 2014).

Manipulation in the

financial report

The second fraud can be detected from the overall manipulations

conducted in the financial report. The organisation need a loan of 7.5

million from BDO Finance, which has a relevant measures that needs

to be maintained by the organisation for the continuing the loan. DIPL

mainly needs a current ratio of 1.5 and debt to equity ratio less than 1.

Therefore it could be estimated that the management could manipulate

the overall values in the financial report to comply with the loan

requirements, as it needs the loan to continue with its business

operation. This could mainly increase the overall material

misstatement, where relevant inheritance risk increases (Schmidt,

Wood and Grabski 2016).

6

employees manipulating relevant transactions. Management mainly forced the

employees to use the new counting machine, which increased relevant

pressure. Thus, it is determined that overall manipulations conducted

with employee for directly increases the material misstatement in the

financial report of the organization. Fraudulent activities used by the

employees in completing the change in accounting software would it

increase the material misstatement and increase the inheritance risk.

Furthermore, there was relevantly minimum workforce present in the

organization, with relevant low experience and efficiency. This mainly

increase the chance of material misstatement, employees will not be

able to adequately record all the transactions conducted by the

organization (Thaweejinda and Senivongse 2014).

Manipulation in the

financial report

The second fraud can be detected from the overall manipulations

conducted in the financial report. The organisation need a loan of 7.5

million from BDO Finance, which has a relevant measures that needs

to be maintained by the organisation for the continuing the loan. DIPL

mainly needs a current ratio of 1.5 and debt to equity ratio less than 1.

Therefore it could be estimated that the management could manipulate

the overall values in the financial report to comply with the loan

requirements, as it needs the loan to continue with its business

operation. This could mainly increase the overall material

misstatement, where relevant inheritance risk increases (Schmidt,

Wood and Grabski 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT, ASSURANCE AND COMPLIANCE

7

Answer to Question 3b: Mentioning how identified fraud risk could lead to audit

The overall case study mainly helps in identifying the overall risk that is affecting the

overall financial report of the organisation. There are relevant frailer activities, which could

be conducted but the employee, when implementing the new accounting system. The pressure

inputted by the management could have led to the overall manipulation of the financial

report. Therefore, the organisation could use adequate monitoring system, which could

adequately reduce the overall fraudulent activities in DIPL. Moreover, the valuation of raw

materials is relevantly valued at wrong cost, where the average costing is used, while the use

of normal costing needs to be conducted. This could directly help in reducing the overall

manipulations in the financial report. Thus, the use of overall audit procedures could directly

help in identifying the overall problems that is hindering operations of the organisation

(Winer et al. 2015).

7

Answer to Question 3b: Mentioning how identified fraud risk could lead to audit

The overall case study mainly helps in identifying the overall risk that is affecting the

overall financial report of the organisation. There are relevant frailer activities, which could

be conducted but the employee, when implementing the new accounting system. The pressure

inputted by the management could have led to the overall manipulation of the financial

report. Therefore, the organisation could use adequate monitoring system, which could

adequately reduce the overall fraudulent activities in DIPL. Moreover, the valuation of raw

materials is relevantly valued at wrong cost, where the average costing is used, while the use

of normal costing needs to be conducted. This could directly help in reducing the overall

manipulations in the financial report. Thus, the use of overall audit procedures could directly

help in identifying the overall problems that is hindering operations of the organisation

(Winer et al. 2015).

AUDIT, ASSURANCE AND COMPLIANCE

8

Reference:

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention:

An examination of differences in chiropractic record-keeping compliance. Journal of

Chiropractic Education, 28(2), pp.123-129.

Hut-Mossel, L., Welker, G., Ahaus, K. and Gans, R., 2017. Understanding how and why

audits work: protocol for a realist review of audit programmes to improve hospital care. BMJ

open, 7(6), p.e015121.

Schmidt, P.J., Wood, J.T. and Grabski, S.V., 2016. Business in the Cloud: Research

Questions on Governance, Audit, and Assurance. Journal of Information Systems, 30(3),

pp.173-189.

Shafii, Z., Abidin, A.Z. and Salleh, S., 2015. Integrated internal-external Shariah audit

model: A proposal towards the enhancement of Shariah assurance practices in Islamic

financial institutions (No. 1436-7).

Thaweejinda, J. and Senivongse, T., 2014, May. Semantic search for cloud providers with

security conformance to Cloud Controls Matrix. In Computer Science and Software

Engineering (JCSSE), 2014 11th International Joint Conference on (pp. 286-291). IEEE.

8

Reference:

Baylis, R.M., Burnap, P., Clatworthy, M.A., Gad, M.A. and Pong, C.K., 2017. Private

lenders’ demand for audit. Journal of Accounting and Economics.

Duncan, B. and Whittington, M., 2014, September. Compliance with standards, assurance

and audit: Does this equal security?. In Proceedings of the 7th International Conference on

Security of Information and Networks (p. 77). ACM.

Homb, N.M., Sheybani, S., Derby, D. and Wood, K., 2014. Audit and feedback intervention:

An examination of differences in chiropractic record-keeping compliance. Journal of

Chiropractic Education, 28(2), pp.123-129.

Hut-Mossel, L., Welker, G., Ahaus, K. and Gans, R., 2017. Understanding how and why

audits work: protocol for a realist review of audit programmes to improve hospital care. BMJ

open, 7(6), p.e015121.

Schmidt, P.J., Wood, J.T. and Grabski, S.V., 2016. Business in the Cloud: Research

Questions on Governance, Audit, and Assurance. Journal of Information Systems, 30(3),

pp.173-189.

Shafii, Z., Abidin, A.Z. and Salleh, S., 2015. Integrated internal-external Shariah audit

model: A proposal towards the enhancement of Shariah assurance practices in Islamic

financial institutions (No. 1436-7).

Thaweejinda, J. and Senivongse, T., 2014, May. Semantic search for cloud providers with

security conformance to Cloud Controls Matrix. In Computer Science and Software

Engineering (JCSSE), 2014 11th International Joint Conference on (pp. 286-291). IEEE.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.