Audit, Assurance, and Compliance Report for DIPL: Risk Factors

VerifiedAdded on 2020/03/04

|11

|2250

|29

Report

AI Summary

This report provides a detailed analysis of audit, assurance, and compliance aspects related to the financial performance of DIPL. It begins by applying analytical procedures to DIPL's financial information for the years 2013-2015, focusing on ratio analysis (profit margin, solvency ratio, and current ratio) and how these results impact audit scheduling decisions. The report then identifies two inherent risk factors arising from the nature of DIPL's trade process, emphasizing the risk of material misstatement in the financial report. Furthermore, it pinpoints two key fraud risk factors associated with misstatements due to fraudulent financial coverage and clarifies how these recognized risk factors influence the conduct of the audit. The analysis incorporates various perspectives from financial accounting, risk management, and auditing literature to provide a comprehensive understanding of DIPL's financial position and the associated audit considerations.

Running head: AUDIT, ASSURANCE AND COMPLIANCE

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Audit, Assurance and Compliance

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2AUDIT, ASSURANCE AND COMPLIANCE

Table of Contents

Question 1........................................................................................................................................3

Applying analytical procedures to the financial information for DIPL for the last three years......3

Clarify how the results can manipulate scheduling decisions for the audit for the year ending 30th

June 2015.........................................................................................................................................4

Question 2........................................................................................................................................5

Identifying two inherent risk factors that arise from the nature of DIPL trade process..................5

Risk that affect the risk of material misstatement in the financial report........................................6

Question 3........................................................................................................................................7

Part A...............................................................................................................................................7

Identify two key fraud risk factors relating to misstatements that arise from fraudulent financial

coverage to which DIPL may be susceptible...................................................................................7

Part B...............................................................................................................................................8

Clarify how the risk factors recognized that influence the conduct of the audit.............................8

Reference List..................................................................................................................................9

Table of Contents

Question 1........................................................................................................................................3

Applying analytical procedures to the financial information for DIPL for the last three years......3

Clarify how the results can manipulate scheduling decisions for the audit for the year ending 30th

June 2015.........................................................................................................................................4

Question 2........................................................................................................................................5

Identifying two inherent risk factors that arise from the nature of DIPL trade process..................5

Risk that affect the risk of material misstatement in the financial report........................................6

Question 3........................................................................................................................................7

Part A...............................................................................................................................................7

Identify two key fraud risk factors relating to misstatements that arise from fraudulent financial

coverage to which DIPL may be susceptible...................................................................................7

Part B...............................................................................................................................................8

Clarify how the risk factors recognized that influence the conduct of the audit.............................8

Reference List..................................................................................................................................9

3AUDIT, ASSURANCE AND COMPLIANCE

Question 1

Applying analytical procedures to the financial information for DIPL for the last three

years

In this given question, it properly explains about analytical process that is present in the

financial report for company such as DIPL. The financial report of company helps in developing

a plan for audit activities (William, Glover and Prawitt 2016). The audit plan is used as a specific

guideline that should be followed while undertaking the audit function. It is important for the

assessor to check over costs of audit at reasonable level as well as assisting in reducing

misunderstanding with the customers. Analytical approach should be used to the financial

declarations for the firm DIPL that means to the process of dissemination of the information that

are accessed from financial declaration of the business enterprise. The given process needs to be

evaluated by utilizing a variety of mechanisms. On using the analytical approach, it is important

to analyze financial declarations where various accountants and financial analysts collect

information that helps in arriving at final decision-making activities (Becker, Stead and Stead

2016).

Analytical approach of common sizing mainly aims at evaluating the financial

declarations to a common specific point. It further help in making the comparison with the

financial statements for given period of time. It is the responsibility of the assessor to look at

different line of items that are already mentioned in the financial report and check the reporting

types (Soh and Martinov-Bennie 2015). For instance, it is all about how items are registered like

net assets as well as net liabilities that goes along with owner equity as shown in the financial

reporting and examining the digression on comparing to normal activities. Furthermore,

Question 1

Applying analytical procedures to the financial information for DIPL for the last three

years

In this given question, it properly explains about analytical process that is present in the

financial report for company such as DIPL. The financial report of company helps in developing

a plan for audit activities (William, Glover and Prawitt 2016). The audit plan is used as a specific

guideline that should be followed while undertaking the audit function. It is important for the

assessor to check over costs of audit at reasonable level as well as assisting in reducing

misunderstanding with the customers. Analytical approach should be used to the financial

declarations for the firm DIPL that means to the process of dissemination of the information that

are accessed from financial declaration of the business enterprise. The given process needs to be

evaluated by utilizing a variety of mechanisms. On using the analytical approach, it is important

to analyze financial declarations where various accountants and financial analysts collect

information that helps in arriving at final decision-making activities (Becker, Stead and Stead

2016).

Analytical approach of common sizing mainly aims at evaluating the financial

declarations to a common specific point. It further help in making the comparison with the

financial statements for given period of time. It is the responsibility of the assessor to look at

different line of items that are already mentioned in the financial report and check the reporting

types (Soh and Martinov-Bennie 2015). For instance, it is all about how items are registered like

net assets as well as net liabilities that goes along with owner equity as shown in the financial

reporting and examining the digression on comparing to normal activities. Furthermore,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4AUDIT, ASSURANCE AND COMPLIANCE

benchmarking is one of the analytical procedures that are present at the time of analyzing plan of

audit. In addition, variation of actual financial declaration from the benchmark aims at

identifying deviation and cause for any of detected variance for determining actual problem.

Therefore, ratio analysis is one of the important tools that is used for essential analytical

approach for comparing financial declarations and assessing the plan of audit activities.

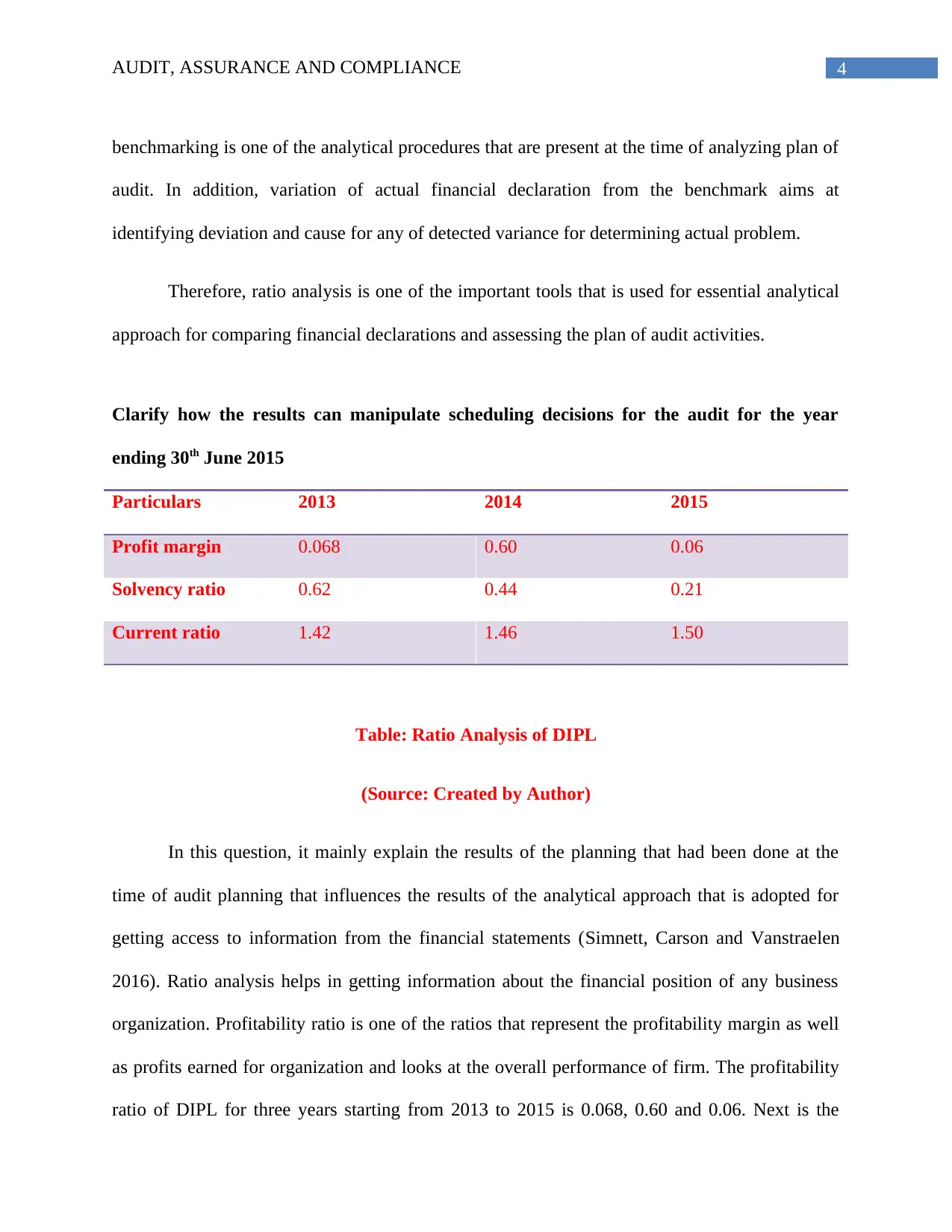

Clarify how the results can manipulate scheduling decisions for the audit for the year

ending 30th June 2015

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Table: Ratio Analysis of DIPL

(Source: Created by Author)

In this question, it mainly explain the results of the planning that had been done at the

time of audit planning that influences the results of the analytical approach that is adopted for

getting access to information from the financial statements (Simnett, Carson and Vanstraelen

2016). Ratio analysis helps in getting information about the financial position of any business

organization. Profitability ratio is one of the ratios that represent the profitability margin as well

as profits earned for organization and looks at the overall performance of firm. The profitability

ratio of DIPL for three years starting from 2013 to 2015 is 0.068, 0.60 and 0.06. Next is the

benchmarking is one of the analytical procedures that are present at the time of analyzing plan of

audit. In addition, variation of actual financial declaration from the benchmark aims at

identifying deviation and cause for any of detected variance for determining actual problem.

Therefore, ratio analysis is one of the important tools that is used for essential analytical

approach for comparing financial declarations and assessing the plan of audit activities.

Clarify how the results can manipulate scheduling decisions for the audit for the year

ending 30th June 2015

Particulars 2013 2014 2015

Profit margin 0.068 0.60 0.06

Solvency ratio 0.62 0.44 0.21

Current ratio 1.42 1.46 1.50

Table: Ratio Analysis of DIPL

(Source: Created by Author)

In this question, it mainly explain the results of the planning that had been done at the

time of audit planning that influences the results of the analytical approach that is adopted for

getting access to information from the financial statements (Simnett, Carson and Vanstraelen

2016). Ratio analysis helps in getting information about the financial position of any business

organization. Profitability ratio is one of the ratios that represent the profitability margin as well

as profits earned for organization and looks at the overall performance of firm. The profitability

ratio of DIPL for three years starting from 2013 to 2015 is 0.068, 0.60 and 0.06. Next is the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5AUDIT, ASSURANCE AND COMPLIANCE

current ratio that helps in assessing the liquidity position of DIPL for three consecutive years and

arrives at 1.42 (2013), 1.46 (2014) and 1.5 (2015). The ideal current ratio is 2:1.

Solvency ratio is calculated for DIPL for three consecutive years and it arrives at 0.62

(2013), 0.44 (2014) and 0.21 (2015). Comparing the results of ratio for three consecutive years

help in getting access to overall cash flow that remains adequate for meeting both short-term as

well as long-term liabilities for DIPL

It is the responsibility of the assessor to understand the relative position of the firm for

three consecutive years as well as analyzing the factors that leads to undesirable or unfavorable

condition of business enterprise (Marques, Santos and Santos 2016).

Question 2

Identifying two inherent risk factors that arise from the nature of DIPL trade process

In this particular question, it is required to identify two inherent risks that are faced by

DIPL in their business operations (Louwers et al. 2015). The material misstated figures are

present in the financial declarations of business and this is one of the significant factors at the

time of conducting audit as well as attracts serious concern. It is important to identify the

financial declarations as mentioned in the financial statements that get accustomed to various

types of systematic and unsystematic risks. These statements portray true and fair view of

financial statement of business that can be either financial or non-financial. It is important for the

assessor for evaluating different types of risks (Becker, Stead and Stead 2016).

current ratio that helps in assessing the liquidity position of DIPL for three consecutive years and

arrives at 1.42 (2013), 1.46 (2014) and 1.5 (2015). The ideal current ratio is 2:1.

Solvency ratio is calculated for DIPL for three consecutive years and it arrives at 0.62

(2013), 0.44 (2014) and 0.21 (2015). Comparing the results of ratio for three consecutive years

help in getting access to overall cash flow that remains adequate for meeting both short-term as

well as long-term liabilities for DIPL

It is the responsibility of the assessor to understand the relative position of the firm for

three consecutive years as well as analyzing the factors that leads to undesirable or unfavorable

condition of business enterprise (Marques, Santos and Santos 2016).

Question 2

Identifying two inherent risk factors that arise from the nature of DIPL trade process

In this particular question, it is required to identify two inherent risks that are faced by

DIPL in their business operations (Louwers et al. 2015). The material misstated figures are

present in the financial declarations of business and this is one of the significant factors at the

time of conducting audit as well as attracts serious concern. It is important to identify the

financial declarations as mentioned in the financial statements that get accustomed to various

types of systematic and unsystematic risks. These statements portray true and fair view of

financial statement of business that can be either financial or non-financial. It is important for the

assessor for evaluating different types of risks (Becker, Stead and Stead 2016).

6AUDIT, ASSURANCE AND COMPLIANCE

Inherent risk is one of the risks that leads to significant errors that result from activities,

operations as well as environment and nature of accounts. There are various types of risk that

have significant impact on the financial statements. These types of risk relates to identifying the

risk that cannot be predicted by the bookkeepers after correlating to omission as diverse errors

(Kend, Houghton and Jubb 2014).

From the case study, it is noted that the accounts had omitted numerous transactions that

was overlooked by DIPL management. There had been ineffective planning of sales as well as

marketing activities that lead to inconsistencies. It is noted that analysis of financial declarations

of DIPL favors the level of profits that is generated from revenue. Management can face the

failure that needs adjustment in the functionalities as well as identification of requirements that is

essential for maintaining the desirable profits. The business faced failure and they need to

identify macro as well as micro economic factors in terms of social, political and others. DIPL

had poor sales figures that can be seen in the inherent level of risk and leads to risk at the time of

analyzing the financial declarations (Becker, Stead and Stead 2016).

There are different factors that lead to inherent risk into various sectors. Business

enterprise can have material misstatement because of falsification of different items as well as

external factors that concerns environment (Junior, Best and Cotter 2014).

Risk that affect the risk of material misstatement in the financial report

There is various identified risk that need to be taken into consideration as susceptibility

for given assertion in association with material misstatement. Some of the risk is as follows:

Inherent risk is one of the risks that leads to significant errors that result from activities,

operations as well as environment and nature of accounts. There are various types of risk that

have significant impact on the financial statements. These types of risk relates to identifying the

risk that cannot be predicted by the bookkeepers after correlating to omission as diverse errors

(Kend, Houghton and Jubb 2014).

From the case study, it is noted that the accounts had omitted numerous transactions that

was overlooked by DIPL management. There had been ineffective planning of sales as well as

marketing activities that lead to inconsistencies. It is noted that analysis of financial declarations

of DIPL favors the level of profits that is generated from revenue. Management can face the

failure that needs adjustment in the functionalities as well as identification of requirements that is

essential for maintaining the desirable profits. The business faced failure and they need to

identify macro as well as micro economic factors in terms of social, political and others. DIPL

had poor sales figures that can be seen in the inherent level of risk and leads to risk at the time of

analyzing the financial declarations (Becker, Stead and Stead 2016).

There are different factors that lead to inherent risk into various sectors. Business

enterprise can have material misstatement because of falsification of different items as well as

external factors that concerns environment (Junior, Best and Cotter 2014).

Risk that affect the risk of material misstatement in the financial report

There is various identified risk that need to be taken into consideration as susceptibility

for given assertion in association with material misstatement. Some of the risk is as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7AUDIT, ASSURANCE AND COMPLIANCE

One of the identified inherent risks is excessive pressure on employees as well as

management. It is noted that excessive workload on members of the staff members of

business that leads to poor bookkeeping (Eilifsen et al. 2013). It gives rise to certain

attributes for encountering cash flow issues as well as poor operating outcomes that goes

along with poor liquidity.

One of the identified inherent risks is risk of errors or misinterpreted errors. Error or

misrepresentation hampers intricacy as well as reliability.

One of the identified inherent risks is unusual pressure on management. It may take

happen that management get incentives for their work and it is misstated in the pecuniary

declarations.

One of the identified inherent risks is integrity of the entire management. DIPL

management lack requisite integrity and expects to remain prepared for the loss of

reputation in the overall business community.

One of the identified inherent risks is nature of entity business. The business operations at

DIPL lead to growth to major economic along with competitive circumstances. In

addition, there are various factors that lead to overall inherent risk of business entity that

analyze audit planning structure in the most appropriate way (Arens et al. 2016).

One of the identified inherent risks is excessive pressure on employees as well as

management. It is noted that excessive workload on members of the staff members of

business that leads to poor bookkeeping (Eilifsen et al. 2013). It gives rise to certain

attributes for encountering cash flow issues as well as poor operating outcomes that goes

along with poor liquidity.

One of the identified inherent risks is risk of errors or misinterpreted errors. Error or

misrepresentation hampers intricacy as well as reliability.

One of the identified inherent risks is unusual pressure on management. It may take

happen that management get incentives for their work and it is misstated in the pecuniary

declarations.

One of the identified inherent risks is integrity of the entire management. DIPL

management lack requisite integrity and expects to remain prepared for the loss of

reputation in the overall business community.

One of the identified inherent risks is nature of entity business. The business operations at

DIPL lead to growth to major economic along with competitive circumstances. In

addition, there are various factors that lead to overall inherent risk of business entity that

analyze audit planning structure in the most appropriate way (Arens et al. 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8AUDIT, ASSURANCE AND COMPLIANCE

Question 3

Part A

Identify two key fraud risk factors relating to misstatements that arise from fraudulent

financial coverage to which DIPL may be susceptible

An operating business entity may face substantial loss because of their assets that result

from fraudulent activities. In addition, fraud in business takes place when workers are not

satisfied and that leads to excessive workloads. Furthermore, business enterprise face high fraud

risks because of the management as well as pressure from investors who reports related financial

outcomes for achieving specific target (Cohen and Simnett 2014).

In this case study on DIPL, the company in real faces risk that take place from the nature

how they operate and instigate the workers for engaging in fraudulent activities because of high

level of dissatisfaction. It is because of the novel accounting system that had given rise to

excessive workload as well as work pressure on the workers. DIPL faces fraudulent activities

that give rise to excessive pressure on employees at the time of carrying out the installation

process of IT system (Arens et al. 2015).

Part B

Clarify how the risk factors recognized that influence the conduct of the audit

It is the responsibility of the auditor to identify the risk that is associated with the

implementation of novel IT accounting system for monitoring the activities at various levels. It is

Question 3

Part A

Identify two key fraud risk factors relating to misstatements that arise from fraudulent

financial coverage to which DIPL may be susceptible

An operating business entity may face substantial loss because of their assets that result

from fraudulent activities. In addition, fraud in business takes place when workers are not

satisfied and that leads to excessive workloads. Furthermore, business enterprise face high fraud

risks because of the management as well as pressure from investors who reports related financial

outcomes for achieving specific target (Cohen and Simnett 2014).

In this case study on DIPL, the company in real faces risk that take place from the nature

how they operate and instigate the workers for engaging in fraudulent activities because of high

level of dissatisfaction. It is because of the novel accounting system that had given rise to

excessive workload as well as work pressure on the workers. DIPL faces fraudulent activities

that give rise to excessive pressure on employees at the time of carrying out the installation

process of IT system (Arens et al. 2015).

Part B

Clarify how the risk factors recognized that influence the conduct of the audit

It is the responsibility of the auditor to identify the risk that is associated with the

implementation of novel IT accounting system for monitoring the activities at various levels. It is

9AUDIT, ASSURANCE AND COMPLIANCE

because of high cost of paper than its average costs, it leads to the process of valuation of raw

materials as adopted by DIPL (Becker, Stead and Stead 2016). The auditors are responsible for

carrying out ways for evaluating financial statements as well as monitoring various mechanisms

for specific period. Therefore it helps in detecting the risks that are properly mentioned in the

financial statements of any business enterprise.

because of high cost of paper than its average costs, it leads to the process of valuation of raw

materials as adopted by DIPL (Becker, Stead and Stead 2016). The auditors are responsible for

carrying out ways for evaluating financial statements as well as monitoring various mechanisms

for specific period. Therefore it helps in detecting the risks that are properly mentioned in the

financial statements of any business enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10AUDIT, ASSURANCE AND COMPLIANCE

Reference List

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Arens, A.A., Elder, R.J., Beasley, M.S. and Jones, J., 2015. Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Becker, L.L., Stead, J.G. and Stead, W.E., 2016. Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), p.29.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

Reference List

Arens, A.A., Elder, R.J., Beasley, M.S. and Hogan, C.E., 2016. Auditing and assurance services.

Pearson.

Arens, A.A., Elder, R.J., Beasley, M.S. and Jones, J., 2015. Auditing: The Art and Science of

Assurance Engagements. Pearson Canada.

Becker, L.L., Stead, J.G. and Stead, W.E., 2016. Sustainability Assurance: A Strategic

Opportunity for CPA Firms. Management Accounting Quarterly, 17(3), p.29.

Cohen, J.R. and Simnett, R., 2014. CSR and assurance services: A research agenda. Auditing: A

Journal of Practice & Theory, 34(1), pp.59-74.

Eilifsen, A., Messier, W.F., Glover, S.M. and Prawitt, D.F., 2013. Auditing and assurance

services. McGraw-Hill.

Junior, R.M., Best, P.J. and Cotter, J., 2014. Sustainability reporting and assurance: A historical

analysis on a world-wide phenomenon. Journal of Business Ethics, 120(1), pp.1-11.

Kend, M., Houghton, K.A. and Jubb, C., 2014. Competition issues in the market for audit and

assurance services: are the concerns justified?. Australian Accounting Review, 24(4), pp.313-

320.

Louwers, T.J., Ramsay, R.J., Sinason, D.H., Strawser, J.R. and Thibodeau, J.C., 2015. Auditing

& assurance services. McGraw-Hill Education.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11AUDIT, ASSURANCE AND COMPLIANCE

Marques, R.P., Santos, H. and Santos, C., 2016. Evaluating Information Systems with

Continuous Assurance Services. International Journal of Information Systems in the Service

Sector (IJISSS), 8(3), pp.1-15.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A Journal of

Practice & Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Marques, R.P., Santos, H. and Santos, C., 2016. Evaluating Information Systems with

Continuous Assurance Services. International Journal of Information Systems in the Service

Sector (IJISSS), 8(3), pp.1-15.

Simnett, R., Carson, E. and Vanstraelen, A., 2016. International Archival Auditing and

Assurance Research: Trends, Methodological Issues, and Opportunities. Auditing: A Journal of

Practice & Theory, 35(3), pp.1-32.

Soh, D.S. and Martinov-Bennie, N., 2015. Internal auditors’ perceptions of their role in

environmental, social and governance assurance and consulting. Managerial Auditing

Journal, 30(1), pp.80-111.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.