Costco Wholesale Corporation Audit Risk Assessment and Procedures

VerifiedAdded on 2022/09/10

|15

|3460

|21

Report

AI Summary

This report is a memorandum prepared for Deloitte Consulting LLP, focusing on the audit risk assessment for Costco Wholesale Corporation. It provides an overview of Costco's background, including its founding, market position, and operational structure, highlighting its membership-based hypermarket model and its significant presence in the retail industry. The report details the company's reliance on technology and the associated inherent risks, particularly concerning revenue recognition and related products. It analyzes inherent risks such as the collectability of receivables, sales returns, and the impact of technology and consumer spending. The document also addresses control risk, detection risk, and outlines substantive analytical procedures, including risk management strategies and the importance of internal controls. Furthermore, the report recommends strategies to mitigate risks related to consumer spending, reputational concerns, intense competition, supply chain failures, and fraud. The report emphasizes the role of auditors in evaluating procedures and policies, and in advising management to achieve retail chain objectives. The assessment includes an evaluation of accounting policies, industry trends, and the company's risk factors, offering insights into the financial performance and operational challenges faced by Costco.

Running head: AUDIT & ASSURANCE

Operation Management

Name:

Institution:

Date:

Operation Management

Name:

Institution:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE

MEMORANDUM

to: Johnathan Liljegren, Auditor, Deloitte consulting llp

from: Jun Liu, Accountant, Costco Wholesale Corporation Audit Engagement

subject: Costco WholeSale Corporation audit risk

date: December 15, 2019

Dear Mr. Liljergren,

At your request sir, I have compiled all the necessary and required information for the

company’s estimation of its audit risk. The company’s name is COACH Inc. the

memorandum shows an overview of the company’s background information and the

conclusion about the application of proper inherent risks, detection risks and control risks.

Costco Wholesale Corporation Overview and Background

Costco Wholesale Corporation, simply known as Costco was founded in Seattle Washington

in 1983. The company has subsidiaries and store located in 785 stores in major cities in the

United States of America and other countries. As of 2015, Costco was the second largest

retailer in America and across the entire globe only behind Walmart. In 2019, Costco was

ranked at position 14 on the Fortune 500 rankings as one of the largest corporation in the US

by revenue consideration. By 2019, Costco had 546 stores in the U.S, 100 stores in Canada,

MEMORANDUM

to: Johnathan Liljegren, Auditor, Deloitte consulting llp

from: Jun Liu, Accountant, Costco Wholesale Corporation Audit Engagement

subject: Costco WholeSale Corporation audit risk

date: December 15, 2019

Dear Mr. Liljergren,

At your request sir, I have compiled all the necessary and required information for the

company’s estimation of its audit risk. The company’s name is COACH Inc. the

memorandum shows an overview of the company’s background information and the

conclusion about the application of proper inherent risks, detection risks and control risks.

Costco Wholesale Corporation Overview and Background

Costco Wholesale Corporation, simply known as Costco was founded in Seattle Washington

in 1983. The company has subsidiaries and store located in 785 stores in major cities in the

United States of America and other countries. As of 2015, Costco was the second largest

retailer in America and across the entire globe only behind Walmart. In 2019, Costco was

ranked at position 14 on the Fortune 500 rankings as one of the largest corporation in the US

by revenue consideration. By 2019, Costco had 546 stores in the U.S, 100 stores in Canada,

AUDIT & ASSURANCE

39 stores in Mexico, 29 in the U.K, 26 store in Japan and the rest distributed all over

countries in Asia and Europe (Byrnes et al, 2019),. It is a member’s only hypermarket that

offer high quality products at low costs. It sells its own brand and other brands and its profit

strategy is through membership fees, high sales, high product turnover, low profitability and

large purchases. (Costco Wholesale Corporation 10-K).

Industry, Competitors and Operation

Costco Wholesale Corporations operates in the retail and wholesale industry. It is a

large membership. it is a large membership only hypermarket which offers a wide range of

products from groceries, clothing, alcoholic and non-alcoholic beverages, bakeries,

electronics, pharmaceutical products and many more. By 2019, the company operated 785

stores across the world with an average area of 146, 000 square feet. The warehouses are in

operation every single day of the week. Its marketing strategy is to provide high quality

products at low cost all across its customers and its members. Its competitors include the

largest retail store in the world Walmart, Amazon, Kroger and Target. Costco ancillary

business also provides its members with food courts, gas stations, eyewear and pharmacies.

(Costco Wholesale Corporation Capital IQ).

Management / Auditors conclusion on internal controls

The company’s management and audit committees determined that internal controls

are effective. The audit committee subsequently recommended to the Board of Director’s that

the 2012 audited financial statements be included in the annual report. Our firm expressed an

unqualified opinion with respect to the company’s internal controls and all consolidated

financial statements for 2012.

39 stores in Mexico, 29 in the U.K, 26 store in Japan and the rest distributed all over

countries in Asia and Europe (Byrnes et al, 2019),. It is a member’s only hypermarket that

offer high quality products at low costs. It sells its own brand and other brands and its profit

strategy is through membership fees, high sales, high product turnover, low profitability and

large purchases. (Costco Wholesale Corporation 10-K).

Industry, Competitors and Operation

Costco Wholesale Corporations operates in the retail and wholesale industry. It is a

large membership. it is a large membership only hypermarket which offers a wide range of

products from groceries, clothing, alcoholic and non-alcoholic beverages, bakeries,

electronics, pharmaceutical products and many more. By 2019, the company operated 785

stores across the world with an average area of 146, 000 square feet. The warehouses are in

operation every single day of the week. Its marketing strategy is to provide high quality

products at low cost all across its customers and its members. Its competitors include the

largest retail store in the world Walmart, Amazon, Kroger and Target. Costco ancillary

business also provides its members with food courts, gas stations, eyewear and pharmacies.

(Costco Wholesale Corporation Capital IQ).

Management / Auditors conclusion on internal controls

The company’s management and audit committees determined that internal controls

are effective. The audit committee subsequently recommended to the Board of Director’s that

the 2012 audited financial statements be included in the annual report. Our firm expressed an

unqualified opinion with respect to the company’s internal controls and all consolidated

financial statements for 2012.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE

Technology Concerns

Costco is heavily dependent on technology. As noted in the 2017 10-K, the company

needs to implement new technologies to remain competitive and mitigate business risk . The

business risk associated with technology includes Costco’s ability to sustain its market share

in the industry and continue to grow. The company must implement new technologies to

maintain its differentiation from other manufacturers and, according to the 2012 10-K, to

achieve financial targets. A firm’s dependence on technology increases inherent risk for

audits (Farooq, & De Villiers, 2017).

Costco is a large, complex organization operating in a dynamic industry. As such,

reliance on technology creates risk for material misstatements. For example, when personnel

are not adequately trained on new information systems, inherent risk increases. Substantial

and timely training is required to minimize human error when entering transactions in

systems that provide data to the financial statements. Additionally, control risk fluctuates

until management and auditors evaluate the operating effectiveness of new information

systems.

Accounting policy and assertions to be evaluated

The significant accounting policy evaluated in this memo is revenue recognition and

Related Products Revenue Recognition. Revenue is recognized by Costco when products are

delivered to dealers or distributors and ownership is transferred. The primary assertion is

existence. Other relevant assertions include occurrence, accuracy, completeness and cut-off.

In this respect, transactions are tested to determine they took place, accounts receivables

exist, sales and accounts receivables are recorded at the proper amount, and all sales

transactions are recorded at the correct amount and in the proper period (Kanjanapradit,

Benos, & Angelidis, 2017)..

Technology Concerns

Costco is heavily dependent on technology. As noted in the 2017 10-K, the company

needs to implement new technologies to remain competitive and mitigate business risk . The

business risk associated with technology includes Costco’s ability to sustain its market share

in the industry and continue to grow. The company must implement new technologies to

maintain its differentiation from other manufacturers and, according to the 2012 10-K, to

achieve financial targets. A firm’s dependence on technology increases inherent risk for

audits (Farooq, & De Villiers, 2017).

Costco is a large, complex organization operating in a dynamic industry. As such,

reliance on technology creates risk for material misstatements. For example, when personnel

are not adequately trained on new information systems, inherent risk increases. Substantial

and timely training is required to minimize human error when entering transactions in

systems that provide data to the financial statements. Additionally, control risk fluctuates

until management and auditors evaluate the operating effectiveness of new information

systems.

Accounting policy and assertions to be evaluated

The significant accounting policy evaluated in this memo is revenue recognition and

Related Products Revenue Recognition. Revenue is recognized by Costco when products are

delivered to dealers or distributors and ownership is transferred. The primary assertion is

existence. Other relevant assertions include occurrence, accuracy, completeness and cut-off.

In this respect, transactions are tested to determine they took place, accounts receivables

exist, sales and accounts receivables are recorded at the proper amount, and all sales

transactions are recorded at the correct amount and in the proper period (Kanjanapradit,

Benos, & Angelidis, 2017)..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE

Inherent Risks

Costco Wholesalers generates revenue through two primary activities: sales and

financing. One area of inherent risk is the collectability of accounts receivables and finance

receivables. It is critical to understand the distinction between the two activities when

performing test of details on accounts receivables. The detection risk for accounts receivables

needs to be low in order to determine if any finance receivables are mistakenly classified as

accounts receivables. This is important because this plan is designed to test sales and related

products revenue, not finance revenue.

Sales returns also affect inherent risk. In the case of Costco we must review the

dealers’ terms and identify if any right to return unsold products exist. For example, dealers

may be able to return 2012 unsold models when 2017 models become available for sale. This

could explain any seasonal increases in returns which otherwise appear abnormal.

Inherent risk and the assessment

The expansion of Costco Wholesale Corporation operating under the international and

local trademarks increases the potential of business risks which forces the retail companies in

this industries to come up with policies and actions to curb this risks. This is the inherent

risks involved in the retail industry. The role of the internal auditor further has become more

important in evaluating the effectiveness of procedures and policies and informing the board

and the senior management to assist in achieving the objectives of the retail chain. Proper

management of inherent risks and business risks at Costco boosts its competitiveness. The

management team should view management of risk in making decisions concerning

sustainability and company investments. Accordingly, the review of the risks addresses the

sufficiency and insufficiency of internal controls and how to improve their effectiveness.

The inherent risks in the retail industry include;

Inherent Risks

Costco Wholesalers generates revenue through two primary activities: sales and

financing. One area of inherent risk is the collectability of accounts receivables and finance

receivables. It is critical to understand the distinction between the two activities when

performing test of details on accounts receivables. The detection risk for accounts receivables

needs to be low in order to determine if any finance receivables are mistakenly classified as

accounts receivables. This is important because this plan is designed to test sales and related

products revenue, not finance revenue.

Sales returns also affect inherent risk. In the case of Costco we must review the

dealers’ terms and identify if any right to return unsold products exist. For example, dealers

may be able to return 2012 unsold models when 2017 models become available for sale. This

could explain any seasonal increases in returns which otherwise appear abnormal.

Inherent risk and the assessment

The expansion of Costco Wholesale Corporation operating under the international and

local trademarks increases the potential of business risks which forces the retail companies in

this industries to come up with policies and actions to curb this risks. This is the inherent

risks involved in the retail industry. The role of the internal auditor further has become more

important in evaluating the effectiveness of procedures and policies and informing the board

and the senior management to assist in achieving the objectives of the retail chain. Proper

management of inherent risks and business risks at Costco boosts its competitiveness. The

management team should view management of risk in making decisions concerning

sustainability and company investments. Accordingly, the review of the risks addresses the

sufficiency and insufficiency of internal controls and how to improve their effectiveness.

The inherent risks in the retail industry include;

AUDIT & ASSURANCE

1. A decline in consumer spending- one of the greatest dangers facing the retail stores

include a declining purchasing power from the consumers.

The role of the auditor is to ensure that;

a. The company takes proper procedures to consider and monitor the impact of the

changes in indicators affecting spending such as ; unemployment, government

spending and many others.

b. Monitor confidence levels of the consumer index so as to measure the market

conditions of consumers and their behaviors.

c. Proper strategy implementation on consumer spending should be adopted.

d. They help to monitor the daily sales and the consequences of the decrease in sales.

2. Reputational Risk

Due to the direct contact of customers and the retail chain, the worst risks is when the

customers stop buying from a store like Costco and view them from a negative light. Further,

inherent risk increases due to the advancement of social media and the internet. A

shortcoming in consumer satisfaction will negatively impact the reputation of the store hence

affecting their revenues.

Recommendation

a. The recommendations in this is to ensure that the store takes periodic consumer

satisfaction surveys to predict the needs and expectations of the consumer.

b. Management systems to ensure that complaints from customers are dealt with

c. Provide appropriate training to the employees.

d. The company should ensure that it draws proper policies in dealing with social media to

act swiftly on negative customer feedback and tainting of their image and brand.

1. A decline in consumer spending- one of the greatest dangers facing the retail stores

include a declining purchasing power from the consumers.

The role of the auditor is to ensure that;

a. The company takes proper procedures to consider and monitor the impact of the

changes in indicators affecting spending such as ; unemployment, government

spending and many others.

b. Monitor confidence levels of the consumer index so as to measure the market

conditions of consumers and their behaviors.

c. Proper strategy implementation on consumer spending should be adopted.

d. They help to monitor the daily sales and the consequences of the decrease in sales.

2. Reputational Risk

Due to the direct contact of customers and the retail chain, the worst risks is when the

customers stop buying from a store like Costco and view them from a negative light. Further,

inherent risk increases due to the advancement of social media and the internet. A

shortcoming in consumer satisfaction will negatively impact the reputation of the store hence

affecting their revenues.

Recommendation

a. The recommendations in this is to ensure that the store takes periodic consumer

satisfaction surveys to predict the needs and expectations of the consumer.

b. Management systems to ensure that complaints from customers are dealt with

c. Provide appropriate training to the employees.

d. The company should ensure that it draws proper policies in dealing with social media to

act swiftly on negative customer feedback and tainting of their image and brand.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE

e. Ensure that there is a good consumer –employee relationship and quality interaction.

3. Intense competition

Retail stores and supermarkets have intense competition due to barriers to the entry. Increase

in competition may hinder the growth of the retail company. Competition makes sure that

retail stores like Walmart and Costco influence consumers purchasing decisions through price

reduction (Marques, Santos, & Santos, 2016)..

Recommendations

1. it will be recommended that the company periodically monitors the product prices in

the market with that of the competitors

2. increase customer satisfaction through products like loyalty cards and other customer

friendly concepts

3. adoption of an elaborate product pricing strategy by understanding the behaviors of

the consumer and their purchasing decisions

4. Planning for strategic sales increase by taking advantages of events such as Christmas

holidays, back to school and sports events.

Supply Chain Failure

The lack if goods to display in the supermarket stores is a hindrance to the daily operations of

the store due to failure of the supply chain.

Recommendations

1. The auditor recommends that the outlets may qualify more than one supplier to avoid

depending on one supplier

2. Use of proper sales forecasts

e. Ensure that there is a good consumer –employee relationship and quality interaction.

3. Intense competition

Retail stores and supermarkets have intense competition due to barriers to the entry. Increase

in competition may hinder the growth of the retail company. Competition makes sure that

retail stores like Walmart and Costco influence consumers purchasing decisions through price

reduction (Marques, Santos, & Santos, 2016)..

Recommendations

1. it will be recommended that the company periodically monitors the product prices in

the market with that of the competitors

2. increase customer satisfaction through products like loyalty cards and other customer

friendly concepts

3. adoption of an elaborate product pricing strategy by understanding the behaviors of

the consumer and their purchasing decisions

4. Planning for strategic sales increase by taking advantages of events such as Christmas

holidays, back to school and sports events.

Supply Chain Failure

The lack if goods to display in the supermarket stores is a hindrance to the daily operations of

the store due to failure of the supply chain.

Recommendations

1. The auditor recommends that the outlets may qualify more than one supplier to avoid

depending on one supplier

2. Use of proper sales forecasts

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE

3. Adopt a proper stock management policy

4. Periodically control stock and maintain a reasonable inventory level. This will ensure

that there is a smooth operation in the retail store without facing any shortage in the

shelves.

5. Adopt automated systems in the store management systems to review the level of

stock available and increase its sales.

Fraud and theft and poor storage is also another inherent risk faced by the retail store

Detection risks and Substantive Analytical Procedures

Risk and money management strategy

The retail industry risk management strategy is the main document that describes the

risk management system in the Retail industry, and defines the basic principles in accordance

with which the Retail industry forms a system for managing risks and the adequacy of its own

funds (capital). The objectives of risk management and capital adequacy are to ensure and

maintain an acceptable level of risk, to provide capital to cover significant risks, and to

comply with the requirements of the state bodies of the American regulating the Retail

industry's activities.

To ensure stability and efficiency of work, the Retail industry has a risk management

system that allows you to efficiently and timely identify, evaluate and limit the risks taken by

the Retail industry, control their volume, structure and identify the main factors affecting the

degree of risk, minimize the consequences if risks occur. The Retail industry has created a

Risk Management Service, which ensures coordination and centralization of management of

all retail industry risks, independent of the activities of other divisions of the Retail industry

that carry out retail industry operations and other transactions that carry retail industry risks.

The risk management service is directly subordinate to the President of the Retail industry

3. Adopt a proper stock management policy

4. Periodically control stock and maintain a reasonable inventory level. This will ensure

that there is a smooth operation in the retail store without facing any shortage in the

shelves.

5. Adopt automated systems in the store management systems to review the level of

stock available and increase its sales.

Fraud and theft and poor storage is also another inherent risk faced by the retail store

Detection risks and Substantive Analytical Procedures

Risk and money management strategy

The retail industry risk management strategy is the main document that describes the

risk management system in the Retail industry, and defines the basic principles in accordance

with which the Retail industry forms a system for managing risks and the adequacy of its own

funds (capital). The objectives of risk management and capital adequacy are to ensure and

maintain an acceptable level of risk, to provide capital to cover significant risks, and to

comply with the requirements of the state bodies of the American regulating the Retail

industry's activities.

To ensure stability and efficiency of work, the Retail industry has a risk management

system that allows you to efficiently and timely identify, evaluate and limit the risks taken by

the Retail industry, control their volume, structure and identify the main factors affecting the

degree of risk, minimize the consequences if risks occur. The Retail industry has created a

Risk Management Service, which ensures coordination and centralization of management of

all retail industry risks, independent of the activities of other divisions of the Retail industry

that carry out retail industry operations and other transactions that carry retail industry risks.

The risk management service is directly subordinate to the President of the Retail industry

AUDIT & ASSURANCE

and has the right to report directly to the Retail industry's Board of Directors on problems

related to retail industry risk management (Knechel, & Salterio, 2016). .

The Retail industry identifies the following types of risks as significant: credit, market

(stock, currency, interest), operational, liquidity loss risk. The Retail industry is also exposed

to regulatory risk, the risk of loss of business reputation, legal, strategic and country risks,

and the risk of legalization (laundering) of proceeds from crime.

In the risk management process, the Board of Directors and the Management Board,

as well as the collegial bodies of the Retail industry (the Credit Committee, the Assets and

Liabilities Management Committee, the Problem Assets Management Committee) and the

Risk Management Service, managers and employees of structural Retail industry divisions.

The Internal Control Service and the Financial Monitoring Service have a number of control

functions in the risk management system.The risk management procedures inherent in the

Retail industry’s activities include identification, analysis, quantitative and qualitative

assessment, proposals to limit and minimize losses, and subsequent control and monitoring of

risk-bearing operations (Simnett, Carson, & Vanstraelen, 2016). Based on the results of the

assessment and monitoring of the level of accepted risks, the management bodies, specialized

bodies of the Retail industry and interested divisions of the Retail industry receive the

relevant management reports necessary for making decisions.

Assessment of Control Risk, Analytical Procedures, and recommended Substantive

Analytical Procedures, and Substantive Test.

In the common sense, the testing process is a sequential system of interrelated tasks

for monitoring the status of something. The question of the need for tests has long been

decided by practice: “Yes, we need it, but in its place, if they solve a certain range of

problems. It should be noted that the massive use of tests in practice occurred simultaneously

and has the right to report directly to the Retail industry's Board of Directors on problems

related to retail industry risk management (Knechel, & Salterio, 2016). .

The Retail industry identifies the following types of risks as significant: credit, market

(stock, currency, interest), operational, liquidity loss risk. The Retail industry is also exposed

to regulatory risk, the risk of loss of business reputation, legal, strategic and country risks,

and the risk of legalization (laundering) of proceeds from crime.

In the risk management process, the Board of Directors and the Management Board,

as well as the collegial bodies of the Retail industry (the Credit Committee, the Assets and

Liabilities Management Committee, the Problem Assets Management Committee) and the

Risk Management Service, managers and employees of structural Retail industry divisions.

The Internal Control Service and the Financial Monitoring Service have a number of control

functions in the risk management system.The risk management procedures inherent in the

Retail industry’s activities include identification, analysis, quantitative and qualitative

assessment, proposals to limit and minimize losses, and subsequent control and monitoring of

risk-bearing operations (Simnett, Carson, & Vanstraelen, 2016). Based on the results of the

assessment and monitoring of the level of accepted risks, the management bodies, specialized

bodies of the Retail industry and interested divisions of the Retail industry receive the

relevant management reports necessary for making decisions.

Assessment of Control Risk, Analytical Procedures, and recommended Substantive

Analytical Procedures, and Substantive Test.

In the common sense, the testing process is a sequential system of interrelated tasks

for monitoring the status of something. The question of the need for tests has long been

decided by practice: “Yes, we need it, but in its place, if they solve a certain range of

problems. It should be noted that the massive use of tests in practice occurred simultaneously

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT & ASSURANCE

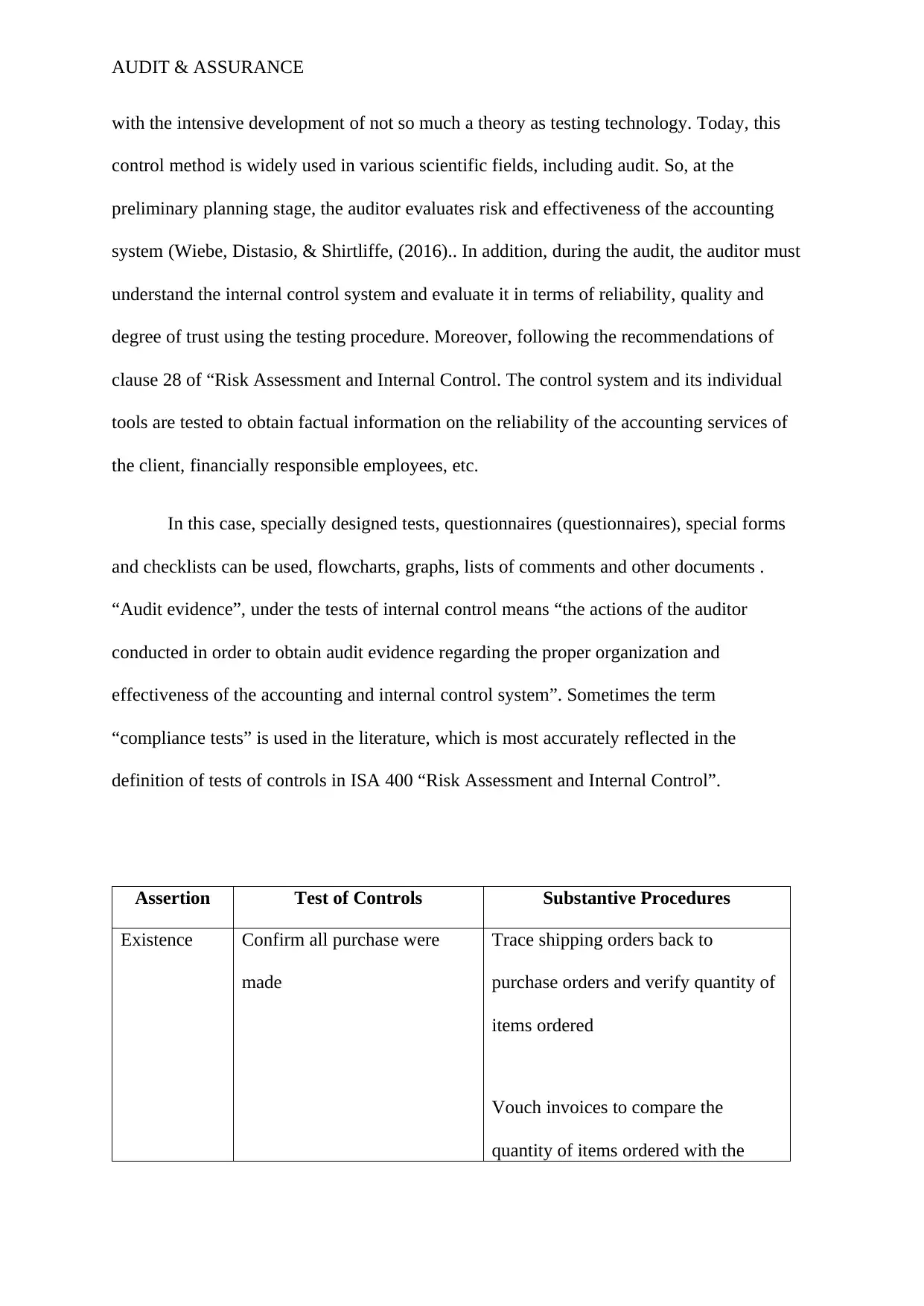

with the intensive development of not so much a theory as testing technology. Today, this

control method is widely used in various scientific fields, including audit. So, at the

preliminary planning stage, the auditor evaluates risk and effectiveness of the accounting

system (Wiebe, Distasio, & Shirtliffe, (2016).. In addition, during the audit, the auditor must

understand the internal control system and evaluate it in terms of reliability, quality and

degree of trust using the testing procedure. Moreover, following the recommendations of

clause 28 of “Risk Assessment and Internal Control. The control system and its individual

tools are tested to obtain factual information on the reliability of the accounting services of

the client, financially responsible employees, etc.

In this case, specially designed tests, questionnaires (questionnaires), special forms

and checklists can be used, flowcharts, graphs, lists of comments and other documents .

“Audit evidence”, under the tests of internal control means “the actions of the auditor

conducted in order to obtain audit evidence regarding the proper organization and

effectiveness of the accounting and internal control system”. Sometimes the term

“compliance tests” is used in the literature, which is most accurately reflected in the

definition of tests of controls in ISA 400 “Risk Assessment and Internal Control”.

Assertion Test of Controls Substantive Procedures

Existence Confirm all purchase were

made

Trace shipping orders back to

purchase orders and verify quantity of

items ordered

Vouch invoices to compare the

quantity of items ordered with the

with the intensive development of not so much a theory as testing technology. Today, this

control method is widely used in various scientific fields, including audit. So, at the

preliminary planning stage, the auditor evaluates risk and effectiveness of the accounting

system (Wiebe, Distasio, & Shirtliffe, (2016).. In addition, during the audit, the auditor must

understand the internal control system and evaluate it in terms of reliability, quality and

degree of trust using the testing procedure. Moreover, following the recommendations of

clause 28 of “Risk Assessment and Internal Control. The control system and its individual

tools are tested to obtain factual information on the reliability of the accounting services of

the client, financially responsible employees, etc.

In this case, specially designed tests, questionnaires (questionnaires), special forms

and checklists can be used, flowcharts, graphs, lists of comments and other documents .

“Audit evidence”, under the tests of internal control means “the actions of the auditor

conducted in order to obtain audit evidence regarding the proper organization and

effectiveness of the accounting and internal control system”. Sometimes the term

“compliance tests” is used in the literature, which is most accurately reflected in the

definition of tests of controls in ISA 400 “Risk Assessment and Internal Control”.

Assertion Test of Controls Substantive Procedures

Existence Confirm all purchase were

made

Trace shipping orders back to

purchase orders and verify quantity of

items ordered

Vouch invoices to compare the

quantity of items ordered with the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

AUDIT & ASSURANCE

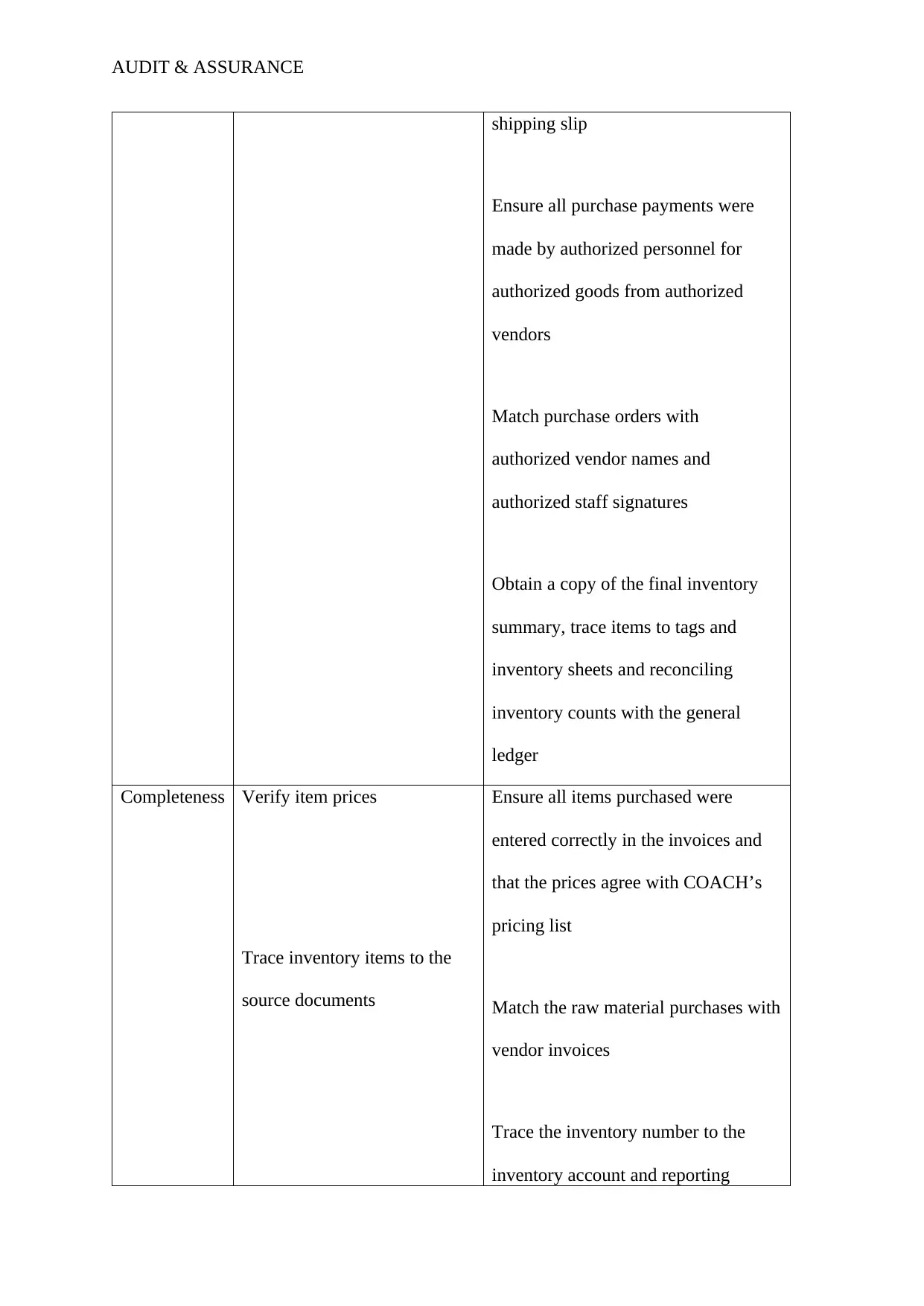

shipping slip

Ensure all purchase payments were

made by authorized personnel for

authorized goods from authorized

vendors

Match purchase orders with

authorized vendor names and

authorized staff signatures

Obtain a copy of the final inventory

summary, trace items to tags and

inventory sheets and reconciling

inventory counts with the general

ledger

Completeness Verify item prices

Trace inventory items to the

source documents

Ensure all items purchased were

entered correctly in the invoices and

that the prices agree with COACH’s

pricing list

Match the raw material purchases with

vendor invoices

Trace the inventory number to the

inventory account and reporting

shipping slip

Ensure all purchase payments were

made by authorized personnel for

authorized goods from authorized

vendors

Match purchase orders with

authorized vendor names and

authorized staff signatures

Obtain a copy of the final inventory

summary, trace items to tags and

inventory sheets and reconciling

inventory counts with the general

ledger

Completeness Verify item prices

Trace inventory items to the

source documents

Ensure all items purchased were

entered correctly in the invoices and

that the prices agree with COACH’s

pricing list

Match the raw material purchases with

vendor invoices

Trace the inventory number to the

inventory account and reporting

AUDIT & ASSURANCE

system

Occurrence

Confirm customer’s method of

payment

Confirm the updating of

inventory receiving floor

sheet, segregation of duties,

and the update of perpetual

records

Match method of payment to

COACH’s retail industry statement to

verify the date of payment, transaction

number, and amount

Ensure floor sheets and recording of

inventory is completed by a different

staff member and ensure that a

voucher package is created after goods

are delivered to the warehouse.

Rights and

obligations

Inquiry of possible

consignment of inventory

Inspection of shipping and

receiving reports from

domestic and international

warehouses

Obtain direct confirmation from the

warehouse custodian in regard to

quantity, price of products, and

condition of inventory held at their

location

Examine shipping and receiving

reports from domestic and

international warehouses to verify that

the goods are being received on the

estimated date, traced to the

appropriate source journal, and

determined that proper cut off was

system

Occurrence

Confirm customer’s method of

payment

Confirm the updating of

inventory receiving floor

sheet, segregation of duties,

and the update of perpetual

records

Match method of payment to

COACH’s retail industry statement to

verify the date of payment, transaction

number, and amount

Ensure floor sheets and recording of

inventory is completed by a different

staff member and ensure that a

voucher package is created after goods

are delivered to the warehouse.

Rights and

obligations

Inquiry of possible

consignment of inventory

Inspection of shipping and

receiving reports from

domestic and international

warehouses

Obtain direct confirmation from the

warehouse custodian in regard to

quantity, price of products, and

condition of inventory held at their

location

Examine shipping and receiving

reports from domestic and

international warehouses to verify that

the goods are being received on the

estimated date, traced to the

appropriate source journal, and

determined that proper cut off was

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.