ACC 707 Auditing: Risk Assessment, Procedures, and ASA 701

VerifiedAdded on 2023/04/23

|12

|3330

|196

Report

AI Summary

This report provides an analysis of auditing and assurance services, focusing on risk assessment and audit procedures for Advanced Computer Solutions Limited's inventory and Green Machine Limited's property, plant, and equipment (PPE). It identifies key assertions at risk, such as valuation and completeness for inventory, and inaccurate accounting of expenditure and improper accounting estimates for PPE. Substantive audit procedures are outlined for each assertion, including physical verification, sales return verification, and purchase/sale bill verification. The report also discusses the requirements of ASA 701 regarding communicating key audit matters in the auditor's report, including necessary disclosures related to inventory valuation and supply agreements below cost price. The analysis considers factors like increased sales returns, inventory turnover rates, and accounting estimates, emphasizing the importance of proper valuation, recording, and measurement in financial statements. The report concludes with recommendations for auditors to address identified risks and ensure compliance with auditing standards.

1

AUDITING AND ASSURANCE SERVICES

Student Name: Student ID:

1/18/2019

AUDITING AND ASSURANCE SERVICES

Student Name: Student ID:

1/18/2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SYNOPSIS

Contents

EXECUTIVE SUMMARY................................................................................................................................ 3

INTRODUCTION............................................................................................................................................. 4

QUESTION 1 – ADVANCED COMPUTER SOLUTIONS LIMITED................................................................................5

TWO KEY ASSERTIONS AT RISK................................................................................................................................5

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION.....................................................................................6

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES..............................................................................7

QUESTION 2– GREEN MACHINE LIMITED............................................................................................................. 8

TWO KEY ASSERTIONS AT RISK................................................................................................................................8

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION.....................................................................................9

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES............................................................................10

CONCLUSION AND RECOMMENDATION............................................................................................................ 11

REFERENCES...................................................................................................................................................... 11

2

Contents

EXECUTIVE SUMMARY................................................................................................................................ 3

INTRODUCTION............................................................................................................................................. 4

QUESTION 1 – ADVANCED COMPUTER SOLUTIONS LIMITED................................................................................5

TWO KEY ASSERTIONS AT RISK................................................................................................................................5

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION.....................................................................................6

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES..............................................................................7

QUESTION 2– GREEN MACHINE LIMITED............................................................................................................. 8

TWO KEY ASSERTIONS AT RISK................................................................................................................................8

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION.....................................................................................9

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES............................................................................10

CONCLUSION AND RECOMMENDATION............................................................................................................ 11

REFERENCES...................................................................................................................................................... 11

2

EXECUTIVE SUMMARY

In the effective and efficient function of the working of any organization, the function of the

accounts and finance plays a very important. It is because of the fact that all other function

cannot perform in the better spirit unless the finance function works effectively and efficiently.

Through this report, the function of the auditing and the assurance has been discussed in detail.

The report has been majorly presented with two important objectives. One of the objectives is to

ascertain the process adopted by the company in relation to the inventory and the property plant

and equipment. The second objective of this report is to understand how the same have affected

the matters which are required to be reported by the auditor of the company. With these two

main aims, the report has been presented with appropriate sections and headings and the data for

the preparation of this report has been obtained from the reliable primary as well as secondary

sources.

3

In the effective and efficient function of the working of any organization, the function of the

accounts and finance plays a very important. It is because of the fact that all other function

cannot perform in the better spirit unless the finance function works effectively and efficiently.

Through this report, the function of the auditing and the assurance has been discussed in detail.

The report has been majorly presented with two important objectives. One of the objectives is to

ascertain the process adopted by the company in relation to the inventory and the property plant

and equipment. The second objective of this report is to understand how the same have affected

the matters which are required to be reported by the auditor of the company. With these two

main aims, the report has been presented with appropriate sections and headings and the data for

the preparation of this report has been obtained from the reliable primary as well as secondary

sources.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The financial crisis that has occurred across the world with the immediate collapse of the

Lehman Brothers and HIH Insurance has led the wave of awareness and requirement of change

which in turn have led the development and the adoption of the new auditing standard. The

change has occurred in the auditing function because of the major reason that the auditor plays a

fiduciary role between the auditee and the regulatory authorities. If the auditor hides anything

from the authorities and the stakeholders than the uses of the stakeholders will decline and will

lead to taking of wrong decisions by them. Through this report, the importance of the audit

function has been detailed with reference to the new auditing standard having number 701

namely communicating the key audit matters in the auditor’s report. The report has been divided

into two main headings. One is related to the analysis of the inventory of the Advanced

Computer solutions Limited and the second is related to the analysis of the property plant and

equipment of Green machine Limited. In both of the cases, the key risk assertions have been

analysed and the audit procedures which shall be adopted in response to that key risk assertions

have been detailed. Then the importance of the new auditing standard in both the cases have

been discussed whether the same is required to be reported as the key audit matter in the

auditor’s report. If it is required to be reported then what type of disclosure is required to be

made and how it is to be made have been discussed. The report has then ended up with the

necessary conclusion and recommendation.

4

The financial crisis that has occurred across the world with the immediate collapse of the

Lehman Brothers and HIH Insurance has led the wave of awareness and requirement of change

which in turn have led the development and the adoption of the new auditing standard. The

change has occurred in the auditing function because of the major reason that the auditor plays a

fiduciary role between the auditee and the regulatory authorities. If the auditor hides anything

from the authorities and the stakeholders than the uses of the stakeholders will decline and will

lead to taking of wrong decisions by them. Through this report, the importance of the audit

function has been detailed with reference to the new auditing standard having number 701

namely communicating the key audit matters in the auditor’s report. The report has been divided

into two main headings. One is related to the analysis of the inventory of the Advanced

Computer solutions Limited and the second is related to the analysis of the property plant and

equipment of Green machine Limited. In both of the cases, the key risk assertions have been

analysed and the audit procedures which shall be adopted in response to that key risk assertions

have been detailed. Then the importance of the new auditing standard in both the cases have

been discussed whether the same is required to be reported as the key audit matter in the

auditor’s report. If it is required to be reported then what type of disclosure is required to be

made and how it is to be made have been discussed. The report has then ended up with the

necessary conclusion and recommendation.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 1 – ADVANCED COMPUTER SOLUTIONS LIMITED

In this question, the inventory of the company for the year ending 30th of June 2018 has been

analysed with the information available from the company.

TWO KEY ASSERTIONS AT RISK

Following key assertions at risk have been analysed:

1. Valuation – The first assertion at risk which have been analysed is the valuation. It has

been identified from the below mentioned information:

S. No. Particulars 2018 2017

1 Average Inventory 3.8 times 5.4 times

2 Closing Inventory 26 percent of Sales 18 percent of Sales

From the above table it is inferred that the closing inventory in terms of the percentage has been

increased from the 18% of sales in the year of 2017 to the 26% of sales in the year of 2018.

Despite of this increase, the average inventory has been decreased from 5.4 times in the year of

2017 to 3.8 times in the year of 2018. It has been very clearly mentioned that the average

inventory has been based on the closing inventory. On the one hand the percentage of inventory

in terms of sales has been increased and on the other hand the average inventory has been

decreased. It is depicted that some sort of the misstatement is there in the value of the inventory

which has been stated in the balance sheet as on 30th of June 2018. Thus, it clearly shows that the

valuation of the inventory which has been done is not correct. If it would have been correct than

the percentage of the inventory and the average inventory times would have been higher.

Along with this information, more information is available regarding the inventory is that

company has been experiencing the high level of sales return due to the problem in the software

that the company has launched in this year. If the sales return are at the highest then the closing

inventory would have been higher in terms of the percentage of the sales as well as the average

inventory. But it is not the case as per the information provided by the company.

5

In this question, the inventory of the company for the year ending 30th of June 2018 has been

analysed with the information available from the company.

TWO KEY ASSERTIONS AT RISK

Following key assertions at risk have been analysed:

1. Valuation – The first assertion at risk which have been analysed is the valuation. It has

been identified from the below mentioned information:

S. No. Particulars 2018 2017

1 Average Inventory 3.8 times 5.4 times

2 Closing Inventory 26 percent of Sales 18 percent of Sales

From the above table it is inferred that the closing inventory in terms of the percentage has been

increased from the 18% of sales in the year of 2017 to the 26% of sales in the year of 2018.

Despite of this increase, the average inventory has been decreased from 5.4 times in the year of

2017 to 3.8 times in the year of 2018. It has been very clearly mentioned that the average

inventory has been based on the closing inventory. On the one hand the percentage of inventory

in terms of sales has been increased and on the other hand the average inventory has been

decreased. It is depicted that some sort of the misstatement is there in the value of the inventory

which has been stated in the balance sheet as on 30th of June 2018. Thus, it clearly shows that the

valuation of the inventory which has been done is not correct. If it would have been correct than

the percentage of the inventory and the average inventory times would have been higher.

Along with this information, more information is available regarding the inventory is that

company has been experiencing the high level of sales return due to the problem in the software

that the company has launched in this year. If the sales return are at the highest then the closing

inventory would have been higher in terms of the percentage of the sales as well as the average

inventory. But it is not the case as per the information provided by the company.

5

From the above discussion it can be clearly interpreted that the valuation of the inventory has not

been done in the correct and fair manner and has undervalued the inventory which otherwise

should be higher.

2. Completeness of Accounting of Inventory – The completeness has been asserted because

of the reason that the value at which the inventory has been reported and presented in the

financial statements does not reflect the true picture of the information that has been

made available by the company. From the facts that have been decided and interpreted

from the assertion of the valuation, it is explicit that the come doubts can be raised on the

accounting of the inventory as to whether it has been completed in all the respects or not

before providing the financial statements of the company to the auditor for the auditing

purpose. It has been further evidenced by the following further information available with

the company:

- Company has moved its inventory from one warehouse to six different warehouse and

- Company has entered into supply of the products to the government department with

the various products.

- Company’s sale returns are high due to technical problem in software.

It depicts that the inventory is high and the company has not accounted all the

transactions relating to the inventory in accounting books (Bajada and Trayler, 2010).

Secondly, company is having the problem in the software and have high sale returns and

still the company has been involved in the supplying the various products to the

department. Thus, the assertion of the completeness is also presented in the inventory.

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION

Auditor is required to perform the audit by following the defined audit procedures. In case of

each of the assertion, the auditor is required to perform the following audit procedures:

Valuation – For the assertion of the valuation, following are the audit procedures:

- Physical verification of inventory with Cut Off Procedures – The auditor shall specify

the cutoff date on which either the staff of the company or the auditor will start the

6

been done in the correct and fair manner and has undervalued the inventory which otherwise

should be higher.

2. Completeness of Accounting of Inventory – The completeness has been asserted because

of the reason that the value at which the inventory has been reported and presented in the

financial statements does not reflect the true picture of the information that has been

made available by the company. From the facts that have been decided and interpreted

from the assertion of the valuation, it is explicit that the come doubts can be raised on the

accounting of the inventory as to whether it has been completed in all the respects or not

before providing the financial statements of the company to the auditor for the auditing

purpose. It has been further evidenced by the following further information available with

the company:

- Company has moved its inventory from one warehouse to six different warehouse and

- Company has entered into supply of the products to the government department with

the various products.

- Company’s sale returns are high due to technical problem in software.

It depicts that the inventory is high and the company has not accounted all the

transactions relating to the inventory in accounting books (Bajada and Trayler, 2010).

Secondly, company is having the problem in the software and have high sale returns and

still the company has been involved in the supplying the various products to the

department. Thus, the assertion of the completeness is also presented in the inventory.

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION

Auditor is required to perform the audit by following the defined audit procedures. In case of

each of the assertion, the auditor is required to perform the following audit procedures:

Valuation – For the assertion of the valuation, following are the audit procedures:

- Physical verification of inventory with Cut Off Procedures – The auditor shall specify

the cutoff date on which either the staff of the company or the auditor will start the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

verification of the stock in the physical terms. By adopting these procedures on the

regular basis, the company and the auditor will have the knowledge that the inventory

in quantitative terms as shown in the books of accounts tallies with the inventory

lying at the premises of the company including the designated warehouses.

- Verification of the Sales Return – As during the period, it has been noticed that the

company has encountered the sales return at the highest due to the problem in the

software, it is necessary to verify each of the transaction and as to check whether the

same have been properly accounted for in the books of accounts.

Completeness - For the assertion of the valuation, following are the audit procedures:

- Verification of Purchase and Sale Bills – The auditor is required to verify each of the

purchase and sale bills so as to check whether the same have been accounted for in

the books of account or not in an accurate manner. The verification also includes the

rate of the items at which they have been purchased and sold.

- External Confirmation – Confirmation from the debtors and creditors shall be

obtained as to check whether all the entries have been accounted or not. Confirmation

is most importantly required for the parties from whom the goods sold have been

returned.

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES

As per the new auditing standard 701, the key audit matters are the matters which have the

significant impact on the presentation of the financial statements of the company. These matters

are totally on the part of the professional judgment of the auditor issuing the audit report (AASB,

2015). The auditor’s report these matters to the persons who are assigned and charged with the

governance of the company. Auditor is required to undertake the following considerations:

Areas which have the risks in significant terms and involved the judgment of the auditor

(Thomson, 2017).

Areas where the appropriate audit evidence is not provided to the auditors or the auditor

is unable to collect the audit evidence (Masytoh O, 2010).

7

regular basis, the company and the auditor will have the knowledge that the inventory

in quantitative terms as shown in the books of accounts tallies with the inventory

lying at the premises of the company including the designated warehouses.

- Verification of the Sales Return – As during the period, it has been noticed that the

company has encountered the sales return at the highest due to the problem in the

software, it is necessary to verify each of the transaction and as to check whether the

same have been properly accounted for in the books of accounts.

Completeness - For the assertion of the valuation, following are the audit procedures:

- Verification of Purchase and Sale Bills – The auditor is required to verify each of the

purchase and sale bills so as to check whether the same have been accounted for in

the books of account or not in an accurate manner. The verification also includes the

rate of the items at which they have been purchased and sold.

- External Confirmation – Confirmation from the debtors and creditors shall be

obtained as to check whether all the entries have been accounted or not. Confirmation

is most importantly required for the parties from whom the goods sold have been

returned.

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES

As per the new auditing standard 701, the key audit matters are the matters which have the

significant impact on the presentation of the financial statements of the company. These matters

are totally on the part of the professional judgment of the auditor issuing the audit report (AASB,

2015). The auditor’s report these matters to the persons who are assigned and charged with the

governance of the company. Auditor is required to undertake the following considerations:

Areas which have the risks in significant terms and involved the judgment of the auditor

(Thomson, 2017).

Areas where the appropriate audit evidence is not provided to the auditors or the auditor

is unable to collect the audit evidence (Masytoh O, 2010).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The appropriate effect of the substantial transactions on such audit.

Inventory being an important part of the current assets as stated in the financial statements of the

company, its proper valuation, recording and measurement is of the utmost importance.

Following are the key audit matters which shall be reported by the auditor of the company and its

necessary disclosures are:

- First key audit matter is the situation where the company has agreed to supply the

goods at the price equal to the 10% below the cost price. It is significant because it

will be providing the losses to the company and still the company has agreed for the

same. The auditor shall disclose complexity which is involved and the chances for

going into liquidation (Cordos and Fülöpa, 2015).

- Second key audit matter is that the inventory has been wrongly valuated because of

the reason that the inventory in percentage terms has been decreased which otherwise

would have been increased due to sale return. Thus, the complexities of the

circumstances and the estimates used for inventory valuation led the disclosure as the

key audit matter.

QUESTION 2– GREEN MACHINE LIMITED

In this question, the property plant and equipment of the company for the year ending 30th of

June 2018 has been analysed with the information available from the company.

TWO KEY ASSERTIONS AT RISK

Following key assertions at risk have been analysed:

Inaccurate Accounting of Expenditure – The first assertion at risk which has been analyzed is

inaccurate accounting of expenditure or amount spent by the company in relation to its Property,

Plant & Equipment. The repairs and other running expenditure of the machineries are treated as

part of cost rather than considering the same in Income statement of the company. On the other

hand, major purchase of parts and accessories of machinery is treated as normal running and

maintenance expenditure and debited in Income statement rather than treating the same as Cost

of Plant and Machinery as per AASB 116 (McKee, 2015) . It shows the accounting personnel

are not performing their jobs in appropriate manner and they have lack of knowledge in context

8

Inventory being an important part of the current assets as stated in the financial statements of the

company, its proper valuation, recording and measurement is of the utmost importance.

Following are the key audit matters which shall be reported by the auditor of the company and its

necessary disclosures are:

- First key audit matter is the situation where the company has agreed to supply the

goods at the price equal to the 10% below the cost price. It is significant because it

will be providing the losses to the company and still the company has agreed for the

same. The auditor shall disclose complexity which is involved and the chances for

going into liquidation (Cordos and Fülöpa, 2015).

- Second key audit matter is that the inventory has been wrongly valuated because of

the reason that the inventory in percentage terms has been decreased which otherwise

would have been increased due to sale return. Thus, the complexities of the

circumstances and the estimates used for inventory valuation led the disclosure as the

key audit matter.

QUESTION 2– GREEN MACHINE LIMITED

In this question, the property plant and equipment of the company for the year ending 30th of

June 2018 has been analysed with the information available from the company.

TWO KEY ASSERTIONS AT RISK

Following key assertions at risk have been analysed:

Inaccurate Accounting of Expenditure – The first assertion at risk which has been analyzed is

inaccurate accounting of expenditure or amount spent by the company in relation to its Property,

Plant & Equipment. The repairs and other running expenditure of the machineries are treated as

part of cost rather than considering the same in Income statement of the company. On the other

hand, major purchase of parts and accessories of machinery is treated as normal running and

maintenance expenditure and debited in Income statement rather than treating the same as Cost

of Plant and Machinery as per AASB 116 (McKee, 2015) . It shows the accounting personnel

are not performing their jobs in appropriate manner and they have lack of knowledge in context

8

of identifying the nature of expenditure. The impact of this assertions leads to wrong profitability

and wrong valuation of Property, Plant and Equipment which is the major backbone for

valuation of business.

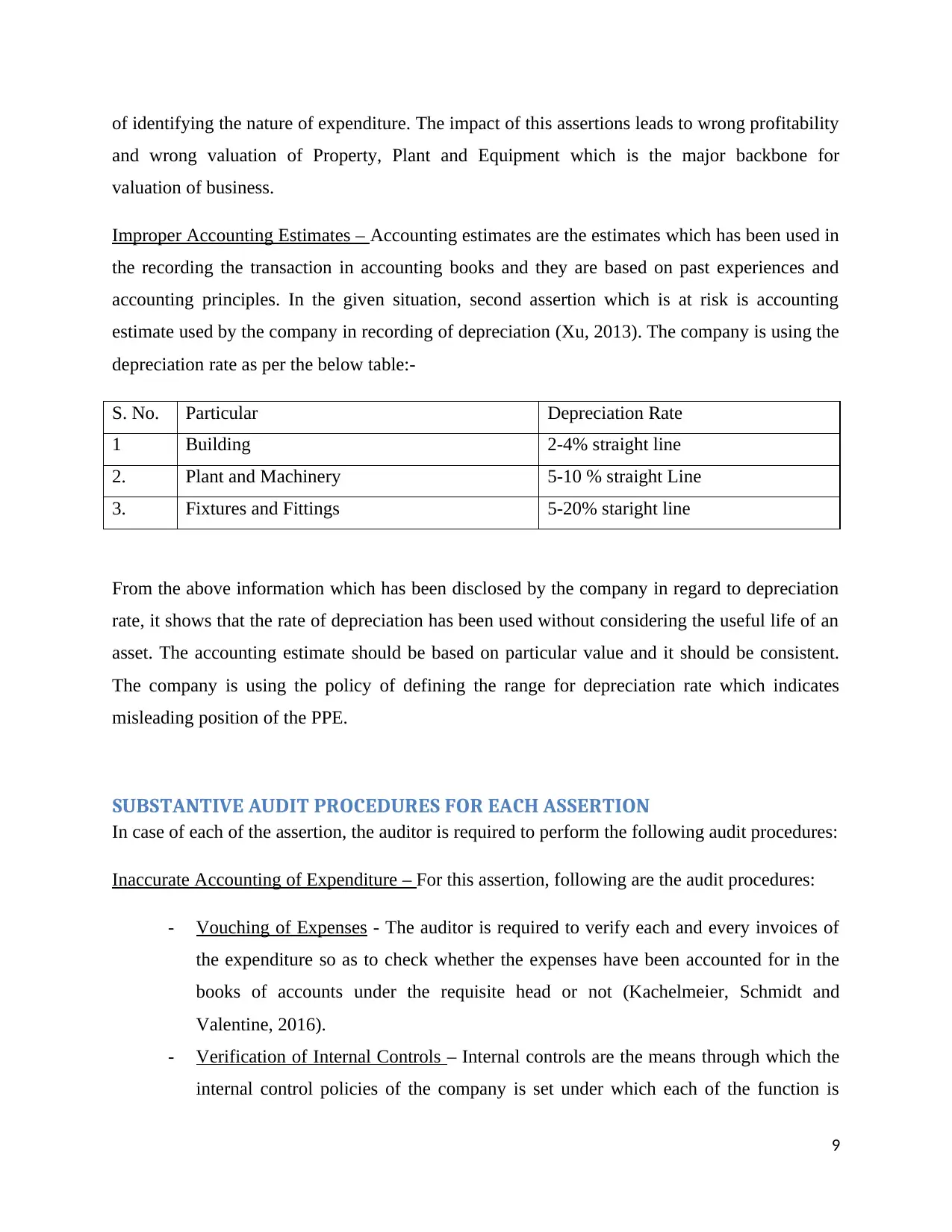

Improper Accounting Estimates – Accounting estimates are the estimates which has been used in

the recording the transaction in accounting books and they are based on past experiences and

accounting principles. In the given situation, second assertion which is at risk is accounting

estimate used by the company in recording of depreciation (Xu, 2013). The company is using the

depreciation rate as per the below table:-

S. No. Particular Depreciation Rate

1 Building 2-4% straight line

2. Plant and Machinery 5-10 % straight Line

3. Fixtures and Fittings 5-20% staright line

From the above information which has been disclosed by the company in regard to depreciation

rate, it shows that the rate of depreciation has been used without considering the useful life of an

asset. The accounting estimate should be based on particular value and it should be consistent.

The company is using the policy of defining the range for depreciation rate which indicates

misleading position of the PPE.

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION

In case of each of the assertion, the auditor is required to perform the following audit procedures:

Inaccurate Accounting of Expenditure – For this assertion, following are the audit procedures:

- Vouching of Expenses - The auditor is required to verify each and every invoices of

the expenditure so as to check whether the expenses have been accounted for in the

books of accounts under the requisite head or not (Kachelmeier, Schmidt and

Valentine, 2016).

- Verification of Internal Controls – Internal controls are the means through which the

internal control policies of the company is set under which each of the function is

9

and wrong valuation of Property, Plant and Equipment which is the major backbone for

valuation of business.

Improper Accounting Estimates – Accounting estimates are the estimates which has been used in

the recording the transaction in accounting books and they are based on past experiences and

accounting principles. In the given situation, second assertion which is at risk is accounting

estimate used by the company in recording of depreciation (Xu, 2013). The company is using the

depreciation rate as per the below table:-

S. No. Particular Depreciation Rate

1 Building 2-4% straight line

2. Plant and Machinery 5-10 % straight Line

3. Fixtures and Fittings 5-20% staright line

From the above information which has been disclosed by the company in regard to depreciation

rate, it shows that the rate of depreciation has been used without considering the useful life of an

asset. The accounting estimate should be based on particular value and it should be consistent.

The company is using the policy of defining the range for depreciation rate which indicates

misleading position of the PPE.

SUBSTANTIVE AUDIT PROCEDURES FOR EACH ASSERTION

In case of each of the assertion, the auditor is required to perform the following audit procedures:

Inaccurate Accounting of Expenditure – For this assertion, following are the audit procedures:

- Vouching of Expenses - The auditor is required to verify each and every invoices of

the expenditure so as to check whether the expenses have been accounted for in the

books of accounts under the requisite head or not (Kachelmeier, Schmidt and

Valentine, 2016).

- Verification of Internal Controls – Internal controls are the means through which the

internal control policies of the company is set under which each of the function is

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

required to be performed under the defined guidelines. The auditor is required to

check whether the company has the internal controls system in place or not with

regard to the approval of each of the accounting entry under the proper heads.

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES

The new auditing standards require the key audit matters to be communicated with the persons

who are charged with the governance of the company. Following key audit matters have been

identified and the same shall be reported in the independent auditor report of the company.

- The first key audit matter which has been observed is the accounting of the

expenditure with the improper bifurcation between the revenue and capital

expenditure. It has affected the results of the financial statements of the company

majorly the statement of the profit and loss account. By misleading the stakeholders

of the company through the financial statements which are materially misstated, the

decision taken by them will be wrong and thus it has the necessary complexities and

requires the professional judgment and has the major impact on the audit and thus has

been classified as the key audit matter.

- The second key audit matter is regarding the rates of the depreciation which have

been used by the management of the company for the different classes of assets

irrespective of the fact that some assets have less useful life and some assets have

more and thus some are required to be depreciated at the highest rates and some to be

depreciated at the lower rates respectively. But the company has calculated the

depreciation at the rates which are very low for some of the assets like building and

plant and machinery despite of the fact that these assets have less useful life (Xu,

2011). Through this the statement of the profit and loss will not give the true picture

of the profit for the year and also the balance sheet will not give the true picture of the

net worth of the company including the realizable value of the asset. By having such

complexity and the major impact on the audit, it has been classified as the key audit

matter.

10

check whether the company has the internal controls system in place or not with

regard to the approval of each of the accounting entry under the proper heads.

REQUIREMENT OF ASA 701 AND ITS NECESSARY DISCLOSURES

The new auditing standards require the key audit matters to be communicated with the persons

who are charged with the governance of the company. Following key audit matters have been

identified and the same shall be reported in the independent auditor report of the company.

- The first key audit matter which has been observed is the accounting of the

expenditure with the improper bifurcation between the revenue and capital

expenditure. It has affected the results of the financial statements of the company

majorly the statement of the profit and loss account. By misleading the stakeholders

of the company through the financial statements which are materially misstated, the

decision taken by them will be wrong and thus it has the necessary complexities and

requires the professional judgment and has the major impact on the audit and thus has

been classified as the key audit matter.

- The second key audit matter is regarding the rates of the depreciation which have

been used by the management of the company for the different classes of assets

irrespective of the fact that some assets have less useful life and some assets have

more and thus some are required to be depreciated at the highest rates and some to be

depreciated at the lower rates respectively. But the company has calculated the

depreciation at the rates which are very low for some of the assets like building and

plant and machinery despite of the fact that these assets have less useful life (Xu,

2011). Through this the statement of the profit and loss will not give the true picture

of the profit for the year and also the balance sheet will not give the true picture of the

net worth of the company including the realizable value of the asset. By having such

complexity and the major impact on the audit, it has been classified as the key audit

matter.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION AND RECOMMENDATION

The report issued by the auditor plays significant role in the financial industry as all the

stakeholders of the respective company on the basis of this report take decisions in response to

the company. The decision may be related to the investment in equity or financing of loans by

the financial institutions or taking up an employment in the company and etc. With the

emergence and the applicability of the new auditing standard, the importance of the auditor’s

report has been further increased and the same has been welcomed by the stakeholders including

the government authorities. Through this report, the basic and important content of the balance

sheet have been analysed. One is inventory and the other one is property plant and equipment.

The key risk assertions have been properly identified and the respective audit procedures have

been detailed with proper references. In order to conclude the report, the concepts have been

exhibited and the importance of auditing function has been properly laid down.

The recommendation from the findings of the report is that the audit shall be conducted in a

much defined manner and the key matters shall be reported so as to enable the users and the

stakeholders to make the effective and efficient decision.

REFERENCES

AASB, (2015), “ASA 701, Communicating Key Audit Matters in the Independents Auditors

report”, available on http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf

accessed at 18/01/2019.

Bajada, C. and Trayler, R., (2010). “How Australia Survived the Global Financial Crisis. The

Financial and Economic Crises: An International Perspective”, Edward Elgar: Cheltenham, UK

and Northampton, USA, pp.139-154.

Cordos, G.S. and Fülöpa, M.T., (2015), “Understanding audit reporting changes: introduction of

Key Audit Matters.” Accounting and Management Information Systems, 14(1), p.128.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K.,(2016). “The disclaimer effect of disclosing

critical audit matters in the auditor’s report.”, Accounting Journal, Vol 5, pp 22-26

11

The report issued by the auditor plays significant role in the financial industry as all the

stakeholders of the respective company on the basis of this report take decisions in response to

the company. The decision may be related to the investment in equity or financing of loans by

the financial institutions or taking up an employment in the company and etc. With the

emergence and the applicability of the new auditing standard, the importance of the auditor’s

report has been further increased and the same has been welcomed by the stakeholders including

the government authorities. Through this report, the basic and important content of the balance

sheet have been analysed. One is inventory and the other one is property plant and equipment.

The key risk assertions have been properly identified and the respective audit procedures have

been detailed with proper references. In order to conclude the report, the concepts have been

exhibited and the importance of auditing function has been properly laid down.

The recommendation from the findings of the report is that the audit shall be conducted in a

much defined manner and the key matters shall be reported so as to enable the users and the

stakeholders to make the effective and efficient decision.

REFERENCES

AASB, (2015), “ASA 701, Communicating Key Audit Matters in the Independents Auditors

report”, available on http://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf

accessed at 18/01/2019.

Bajada, C. and Trayler, R., (2010). “How Australia Survived the Global Financial Crisis. The

Financial and Economic Crises: An International Perspective”, Edward Elgar: Cheltenham, UK

and Northampton, USA, pp.139-154.

Cordos, G.S. and Fülöpa, M.T., (2015), “Understanding audit reporting changes: introduction of

Key Audit Matters.” Accounting and Management Information Systems, 14(1), p.128.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K.,(2016). “The disclaimer effect of disclosing

critical audit matters in the auditor’s report.”, Accounting Journal, Vol 5, pp 22-26

11

Masytoh O, (2010), “The analysis of determinants of Going Concern Audit Report”, Journal of

Modern Accounting and Auditing, Vol 6(4), pp 27-36.

McKee, D., (2015). “New external audit report standards are game changing.: Governance

Directions, 67(4), p.222.

Thomson, J., (2017), “Five lessons from the Spectacular fall of Eddy Grooves”, available at

http://www.smartcompany.com.au/finance/five-lessons-from-the-spectacular-fall-of-eddy-

grroves.html accessed on 18/01/2019.

Xu, Y., (2011). “Audit reports in Australia during the global financial crisis”. Australian

Accounting Review, 21(1), pp.22-31

Xu, Y., (2013). “Responses by Australian auditors to the global financial crisis.” Accounting &

Finance, 53(1), pp.301-338.

..

12

Modern Accounting and Auditing, Vol 6(4), pp 27-36.

McKee, D., (2015). “New external audit report standards are game changing.: Governance

Directions, 67(4), p.222.

Thomson, J., (2017), “Five lessons from the Spectacular fall of Eddy Grooves”, available at

http://www.smartcompany.com.au/finance/five-lessons-from-the-spectacular-fall-of-eddy-

grroves.html accessed on 18/01/2019.

Xu, Y., (2011). “Audit reports in Australia during the global financial crisis”. Australian

Accounting Review, 21(1), pp.22-31

Xu, Y., (2013). “Responses by Australian auditors to the global financial crisis.” Accounting &

Finance, 53(1), pp.301-338.

..

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.