Auditing, Assurance, and Compliance Report: Case Study Analysis

VerifiedAdded on 2020/03/02

|9

|2114

|76

Report

AI Summary

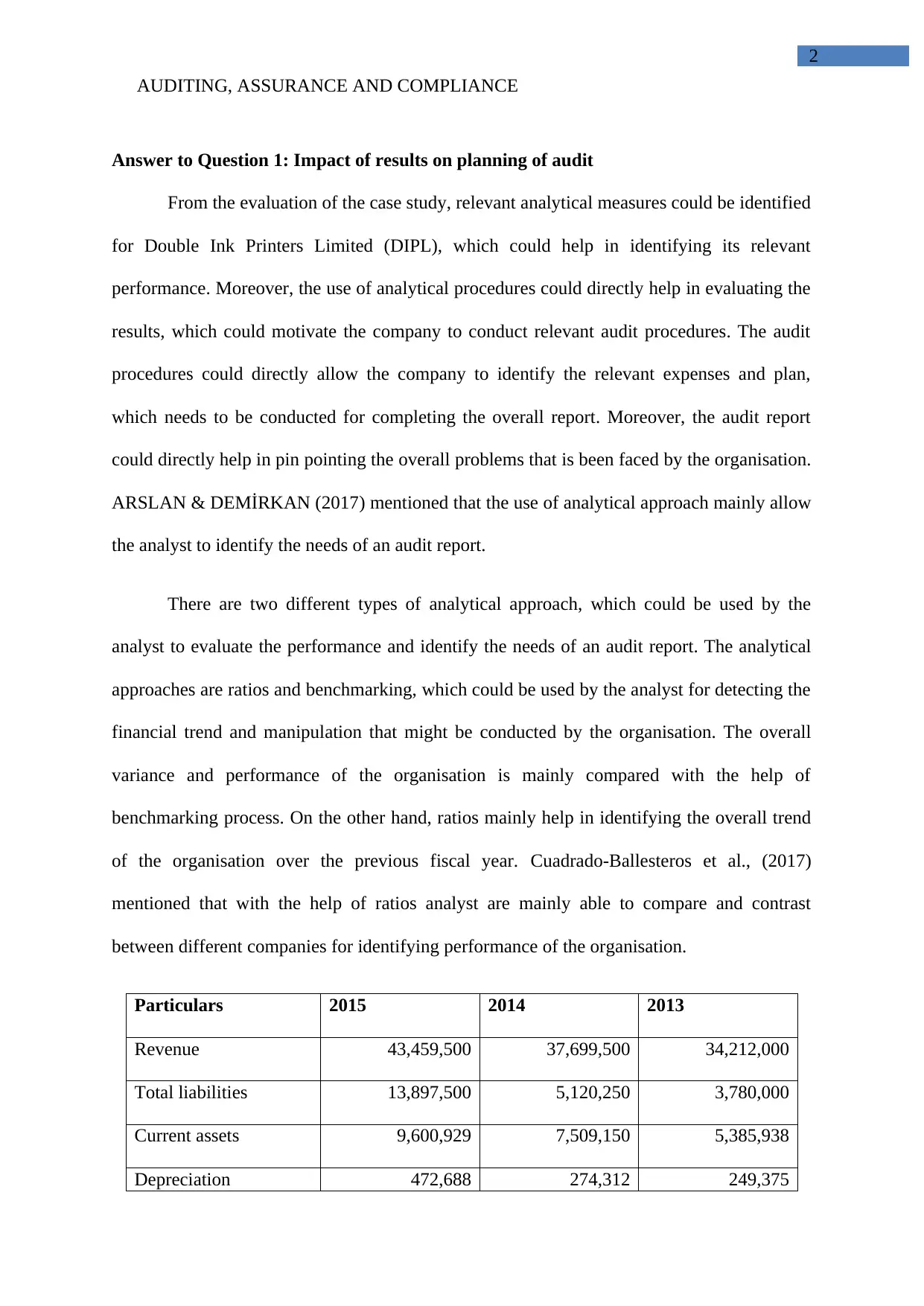

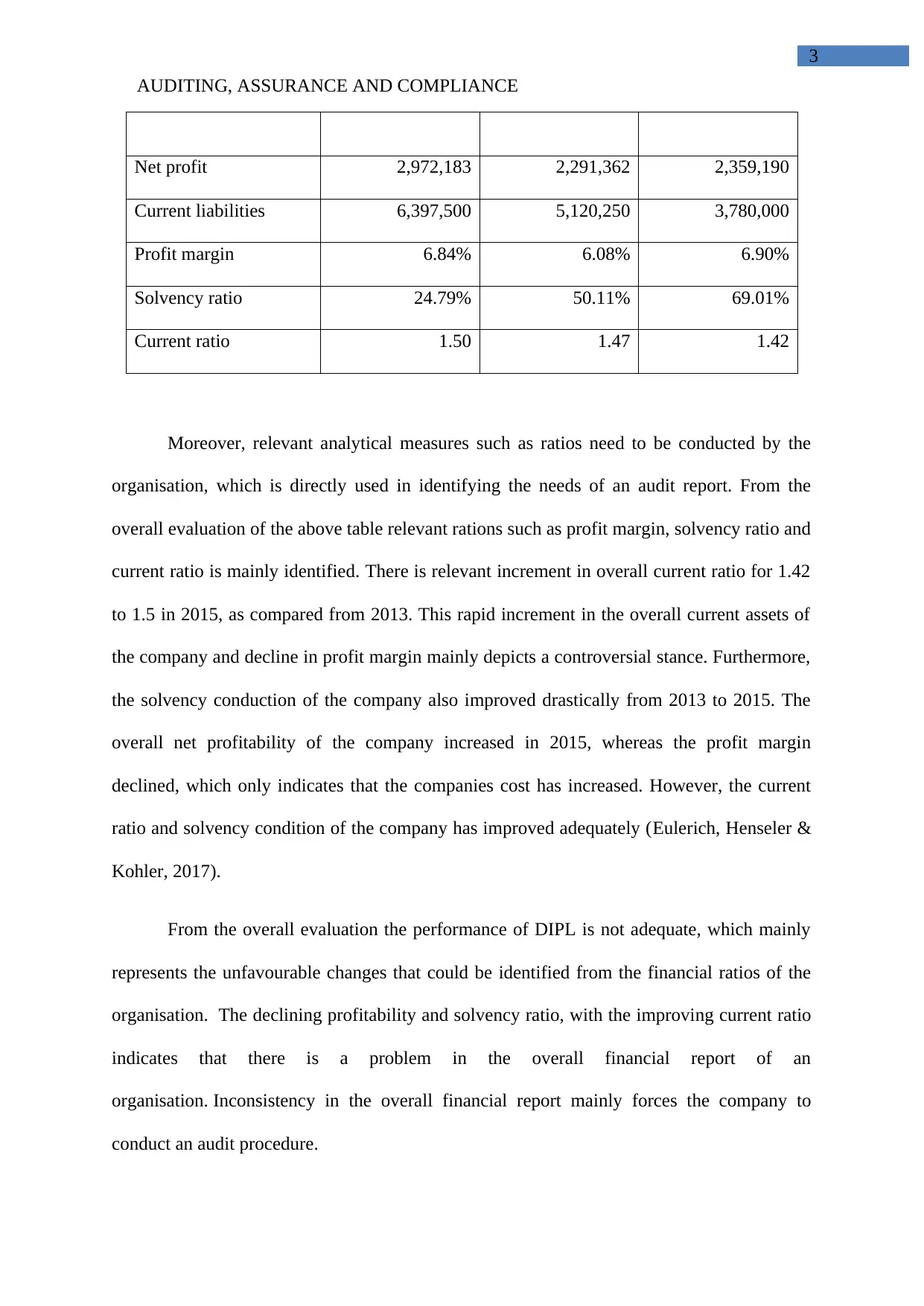

This report provides a comprehensive analysis of auditing, assurance, and compliance, focusing on a case study of Double Ink Printers Limited (DIPL). The report begins with an assessment of how financial results impact audit planning, utilizing financial ratios such as profit margin, solvency, and current ratios to evaluate DIPL's performance from 2013 to 2015. It identifies declining profitability and solvency ratios as indicators of potential financial issues. The report then explains the concept of risk and its impact on material misstatements, highlighting inheritance risks stemming from inexperienced employees, an inadequate workforce, and the implementation of a new accounting system. Two key fraud risks are identified: manipulation in financial report preparation to secure loans and increased fraudulent activities within the workforce. Finally, the report explores the impact of these risk factors on audit procedures, emphasizing the need for enhanced monitoring systems and accurate material valuation. The analysis underscores the importance of robust audit procedures to mitigate financial risks and ensure compliance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.