Auditing of Always Precise Instruments (API): Risk Analysis

VerifiedAdded on 2022/12/30

|15

|3868

|48

Report

AI Summary

This report, prepared for the audit manager of Always Precise Instruments Pty Limited (API), analyzes the audit risks associated with the company's financial statements. The report examines various financial ratios, including current ratio, quick ratio, return on equity, return on total assets, gross margin, marketing expenses, admin expenses, times interest earned, days in inventory, days in accounts receivable, and debt to equity ratio, identifying potential misstatements and their impact on the financial position of the business. For each ratio, the report outlines the audit procedures, such as test of details and test of controls, that the auditor should undertake to mitigate the identified risks. The report also addresses weaknesses in inventory internal control, detailing associated audit risks and recommended audit procedures to improve the system. The report emphasizes the importance of accurate financial representation and the auditor's role in ensuring the validity and fairness of the financial statements.

Running head: AUDITING

Auditing

Name of the Student:

Name of the University:

Author’s Note

Auditing

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

AUDITING

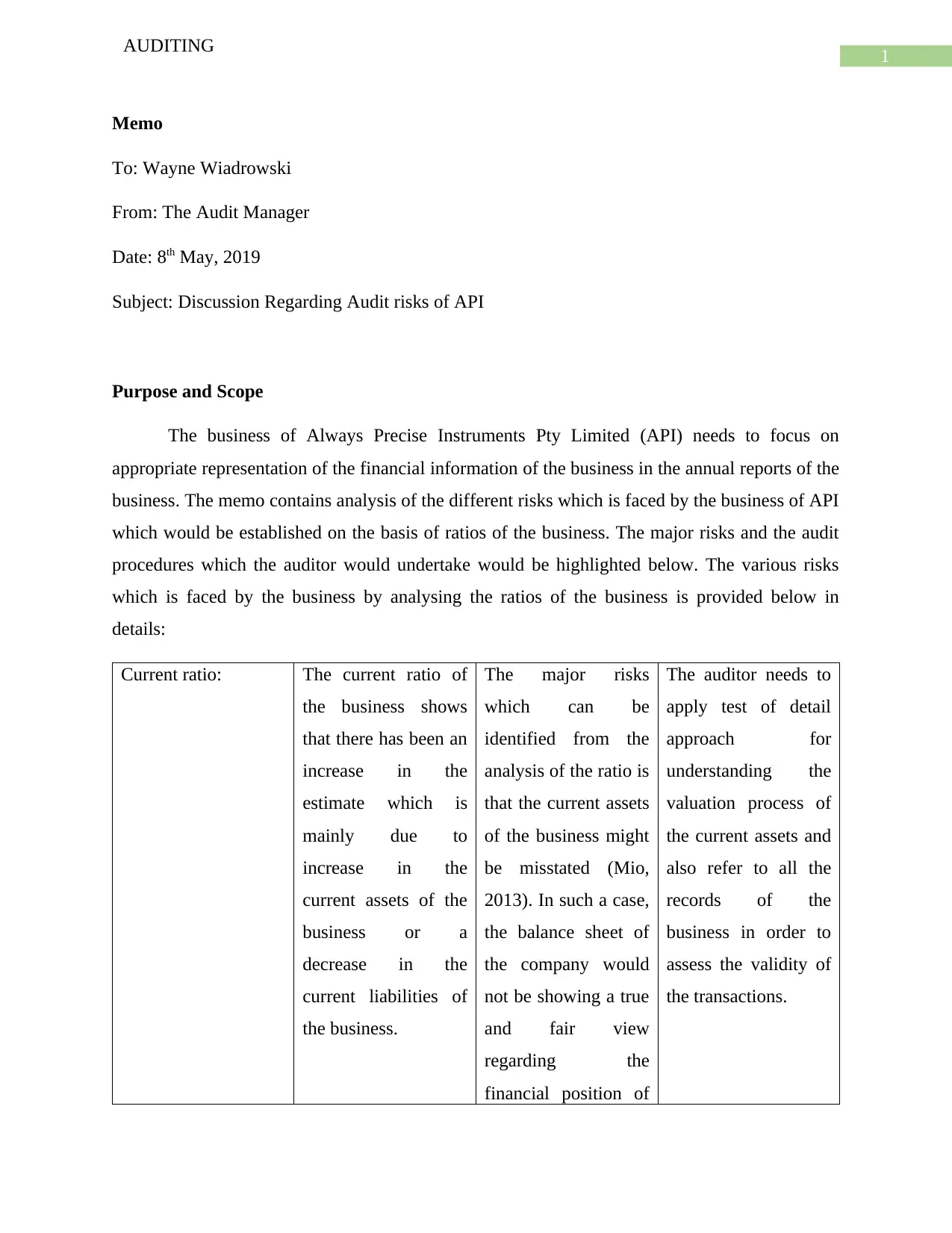

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The business of Always Precise Instruments Pty Limited (API) needs to focus on

appropriate representation of the financial information of the business in the annual reports of the

business. The memo contains analysis of the different risks which is faced by the business of API

which would be established on the basis of ratios of the business. The major risks and the audit

procedures which the auditor would undertake would be highlighted below. The various risks

which is faced by the business by analysing the ratios of the business is provided below in

details:

Current ratio: The current ratio of

the business shows

that there has been an

increase in the

estimate which is

mainly due to

increase in the

current assets of the

business or a

decrease in the

current liabilities of

the business.

The major risks

which can be

identified from the

analysis of the ratio is

that the current assets

of the business might

be misstated (Mio,

2013). In such a case,

the balance sheet of

the company would

not be showing a true

and fair view

regarding the

financial position of

The auditor needs to

apply test of detail

approach for

understanding the

valuation process of

the current assets and

also refer to all the

records of the

business in order to

assess the validity of

the transactions.

AUDITING

Memo

To: Wayne Wiadrowski

From: The Audit Manager

Date: 8th May, 2019

Subject: Discussion Regarding Audit risks of API

Purpose and Scope

The business of Always Precise Instruments Pty Limited (API) needs to focus on

appropriate representation of the financial information of the business in the annual reports of the

business. The memo contains analysis of the different risks which is faced by the business of API

which would be established on the basis of ratios of the business. The major risks and the audit

procedures which the auditor would undertake would be highlighted below. The various risks

which is faced by the business by analysing the ratios of the business is provided below in

details:

Current ratio: The current ratio of

the business shows

that there has been an

increase in the

estimate which is

mainly due to

increase in the

current assets of the

business or a

decrease in the

current liabilities of

the business.

The major risks

which can be

identified from the

analysis of the ratio is

that the current assets

of the business might

be misstated (Mio,

2013). In such a case,

the balance sheet of

the company would

not be showing a true

and fair view

regarding the

financial position of

The auditor needs to

apply test of detail

approach for

understanding the

valuation process of

the current assets and

also refer to all the

records of the

business in order to

assess the validity of

the transactions.

2

AUDITING

the business.

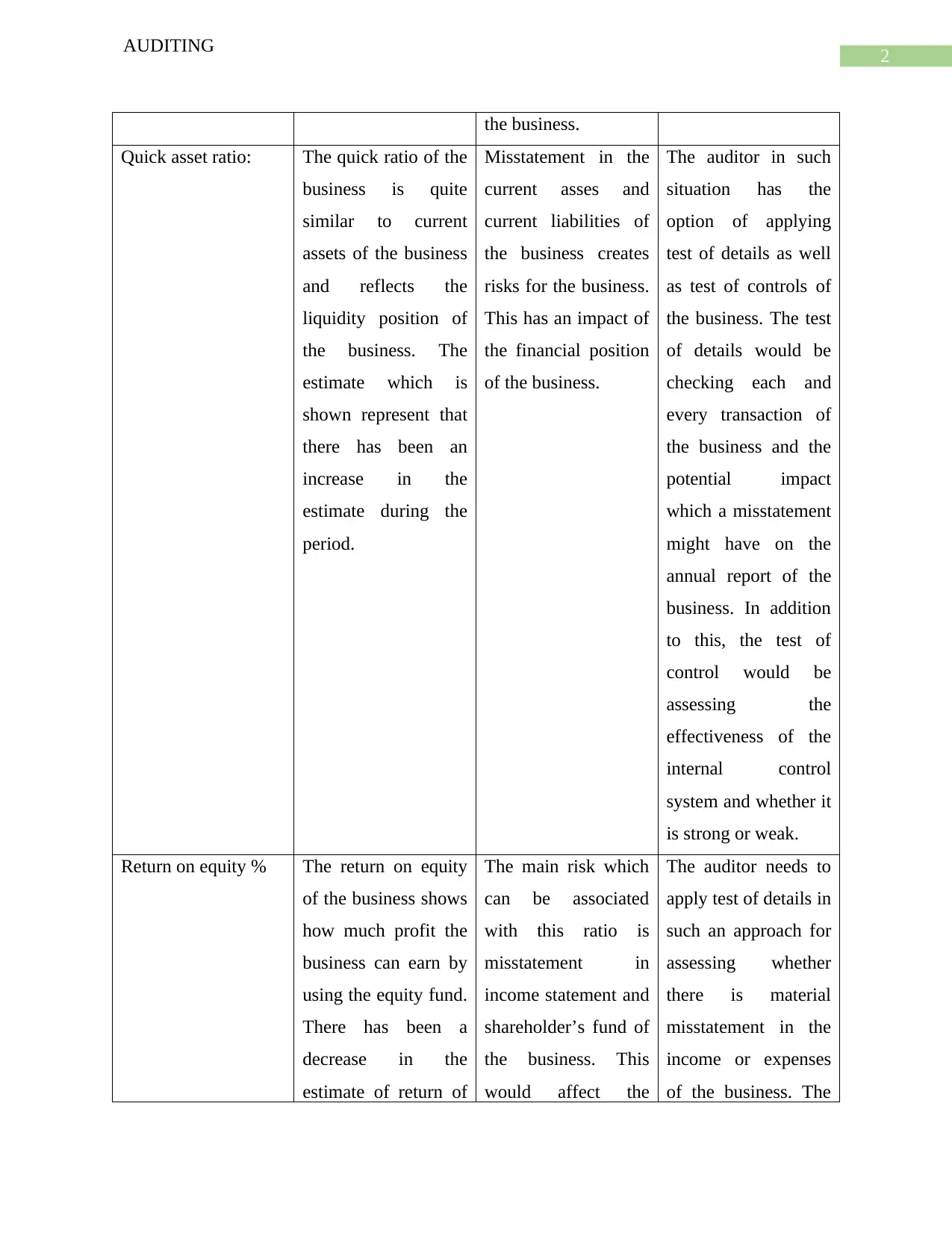

Quick asset ratio: The quick ratio of the

business is quite

similar to current

assets of the business

and reflects the

liquidity position of

the business. The

estimate which is

shown represent that

there has been an

increase in the

estimate during the

period.

Misstatement in the

current asses and

current liabilities of

the business creates

risks for the business.

This has an impact of

the financial position

of the business.

The auditor in such

situation has the

option of applying

test of details as well

as test of controls of

the business. The test

of details would be

checking each and

every transaction of

the business and the

potential impact

which a misstatement

might have on the

annual report of the

business. In addition

to this, the test of

control would be

assessing the

effectiveness of the

internal control

system and whether it

is strong or weak.

Return on equity % The return on equity

of the business shows

how much profit the

business can earn by

using the equity fund.

There has been a

decrease in the

estimate of return of

The main risk which

can be associated

with this ratio is

misstatement in

income statement and

shareholder’s fund of

the business. This

would affect the

The auditor needs to

apply test of details in

such an approach for

assessing whether

there is material

misstatement in the

income or expenses

of the business. The

AUDITING

the business.

Quick asset ratio: The quick ratio of the

business is quite

similar to current

assets of the business

and reflects the

liquidity position of

the business. The

estimate which is

shown represent that

there has been an

increase in the

estimate during the

period.

Misstatement in the

current asses and

current liabilities of

the business creates

risks for the business.

This has an impact of

the financial position

of the business.

The auditor in such

situation has the

option of applying

test of details as well

as test of controls of

the business. The test

of details would be

checking each and

every transaction of

the business and the

potential impact

which a misstatement

might have on the

annual report of the

business. In addition

to this, the test of

control would be

assessing the

effectiveness of the

internal control

system and whether it

is strong or weak.

Return on equity % The return on equity

of the business shows

how much profit the

business can earn by

using the equity fund.

There has been a

decrease in the

estimate of return of

The main risk which

can be associated

with this ratio is

misstatement in

income statement and

shareholder’s fund of

the business. This

would affect the

The auditor needs to

apply test of details in

such an approach for

assessing whether

there is material

misstatement in the

income or expenses

of the business. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

AUDITING

equity which suggest

that either the profits

of the business have

declined or the equity

of the business is

overvalued slightly.

accuracy of the

income statement and

also affect the

financial position of

the business as a

whole.

auditor can also apply

couching practices in

the business so as to

ascertain that the

income and expenses

figures are accurate.

Return on total assets

%

The return on total

asset represent the

profit which is

generated by using

the assets. This is

considered to be one

of the financial

indicators of the

business. There is a

decrease in the ratio

which might be due

to fall in profits of the

business or

overvaluation of the

assets of the business.

The main risks in

such case is related to

misstatement in

income and expenses

account and there

might also be an

overvaluation of the

assets of the business.

The misstatement in

profits would affect

the entire financial

statements thereby

affecting genuineness

of the ratio

The test which the

auditor of the

business can apply in

such a case is test of

details for analysing

the items of income

or expenses of the

business. In addition

to this, the auditor of

the business also

needs to apply

verification practices

in the business so that

the assets of the

business are properly

recorded and

appropriately valued.

The auditor can also

use the opinion of an

expert for valuing the

assets of the business.

Gross margin % The gross profit

margin is a very

important estimate

which reveals the

The risk which is

created with such a

ratio is the risk of

misstatement in the

The auditor needs to

apply both test of

control and test of

details which would

AUDITING

equity which suggest

that either the profits

of the business have

declined or the equity

of the business is

overvalued slightly.

accuracy of the

income statement and

also affect the

financial position of

the business as a

whole.

auditor can also apply

couching practices in

the business so as to

ascertain that the

income and expenses

figures are accurate.

Return on total assets

%

The return on total

asset represent the

profit which is

generated by using

the assets. This is

considered to be one

of the financial

indicators of the

business. There is a

decrease in the ratio

which might be due

to fall in profits of the

business or

overvaluation of the

assets of the business.

The main risks in

such case is related to

misstatement in

income and expenses

account and there

might also be an

overvaluation of the

assets of the business.

The misstatement in

profits would affect

the entire financial

statements thereby

affecting genuineness

of the ratio

The test which the

auditor of the

business can apply in

such a case is test of

details for analysing

the items of income

or expenses of the

business. In addition

to this, the auditor of

the business also

needs to apply

verification practices

in the business so that

the assets of the

business are properly

recorded and

appropriately valued.

The auditor can also

use the opinion of an

expert for valuing the

assets of the business.

Gross margin % The gross profit

margin is a very

important estimate

which reveals the

The risk which is

created with such a

ratio is the risk of

misstatement in the

The auditor needs to

apply both test of

control and test of

details which would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

AUDITING

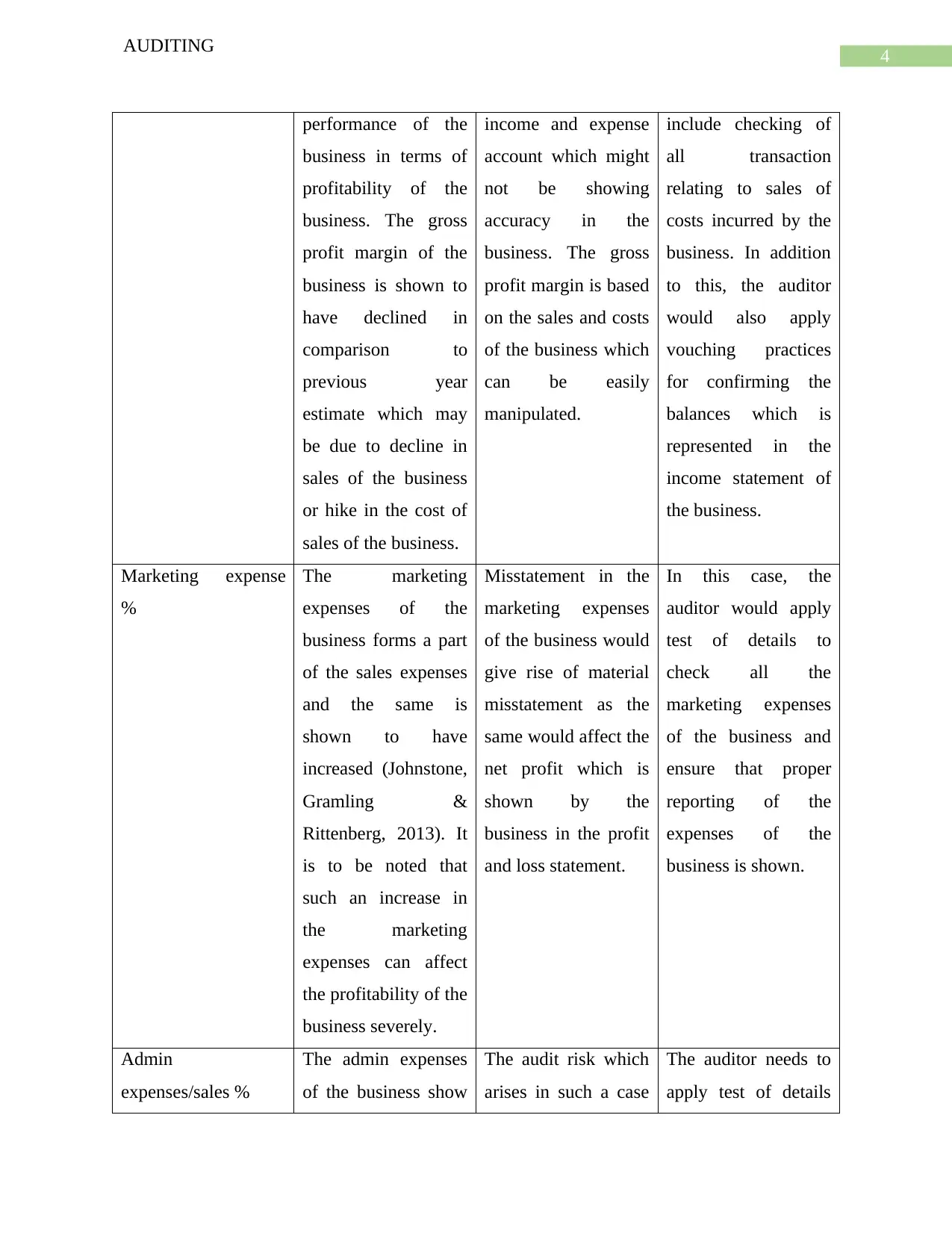

performance of the

business in terms of

profitability of the

business. The gross

profit margin of the

business is shown to

have declined in

comparison to

previous year

estimate which may

be due to decline in

sales of the business

or hike in the cost of

sales of the business.

income and expense

account which might

not be showing

accuracy in the

business. The gross

profit margin is based

on the sales and costs

of the business which

can be easily

manipulated.

include checking of

all transaction

relating to sales of

costs incurred by the

business. In addition

to this, the auditor

would also apply

vouching practices

for confirming the

balances which is

represented in the

income statement of

the business.

Marketing expense

%

The marketing

expenses of the

business forms a part

of the sales expenses

and the same is

shown to have

increased (Johnstone,

Gramling &

Rittenberg, 2013). It

is to be noted that

such an increase in

the marketing

expenses can affect

the profitability of the

business severely.

Misstatement in the

marketing expenses

of the business would

give rise of material

misstatement as the

same would affect the

net profit which is

shown by the

business in the profit

and loss statement.

In this case, the

auditor would apply

test of details to

check all the

marketing expenses

of the business and

ensure that proper

reporting of the

expenses of the

business is shown.

Admin

expenses/sales %

The admin expenses

of the business show

The audit risk which

arises in such a case

The auditor needs to

apply test of details

AUDITING

performance of the

business in terms of

profitability of the

business. The gross

profit margin of the

business is shown to

have declined in

comparison to

previous year

estimate which may

be due to decline in

sales of the business

or hike in the cost of

sales of the business.

income and expense

account which might

not be showing

accuracy in the

business. The gross

profit margin is based

on the sales and costs

of the business which

can be easily

manipulated.

include checking of

all transaction

relating to sales of

costs incurred by the

business. In addition

to this, the auditor

would also apply

vouching practices

for confirming the

balances which is

represented in the

income statement of

the business.

Marketing expense

%

The marketing

expenses of the

business forms a part

of the sales expenses

and the same is

shown to have

increased (Johnstone,

Gramling &

Rittenberg, 2013). It

is to be noted that

such an increase in

the marketing

expenses can affect

the profitability of the

business severely.

Misstatement in the

marketing expenses

of the business would

give rise of material

misstatement as the

same would affect the

net profit which is

shown by the

business in the profit

and loss statement.

In this case, the

auditor would apply

test of details to

check all the

marketing expenses

of the business and

ensure that proper

reporting of the

expenses of the

business is shown.

Admin

expenses/sales %

The admin expenses

of the business show

The audit risk which

arises in such a case

The auditor needs to

apply test of details

5

AUDITING

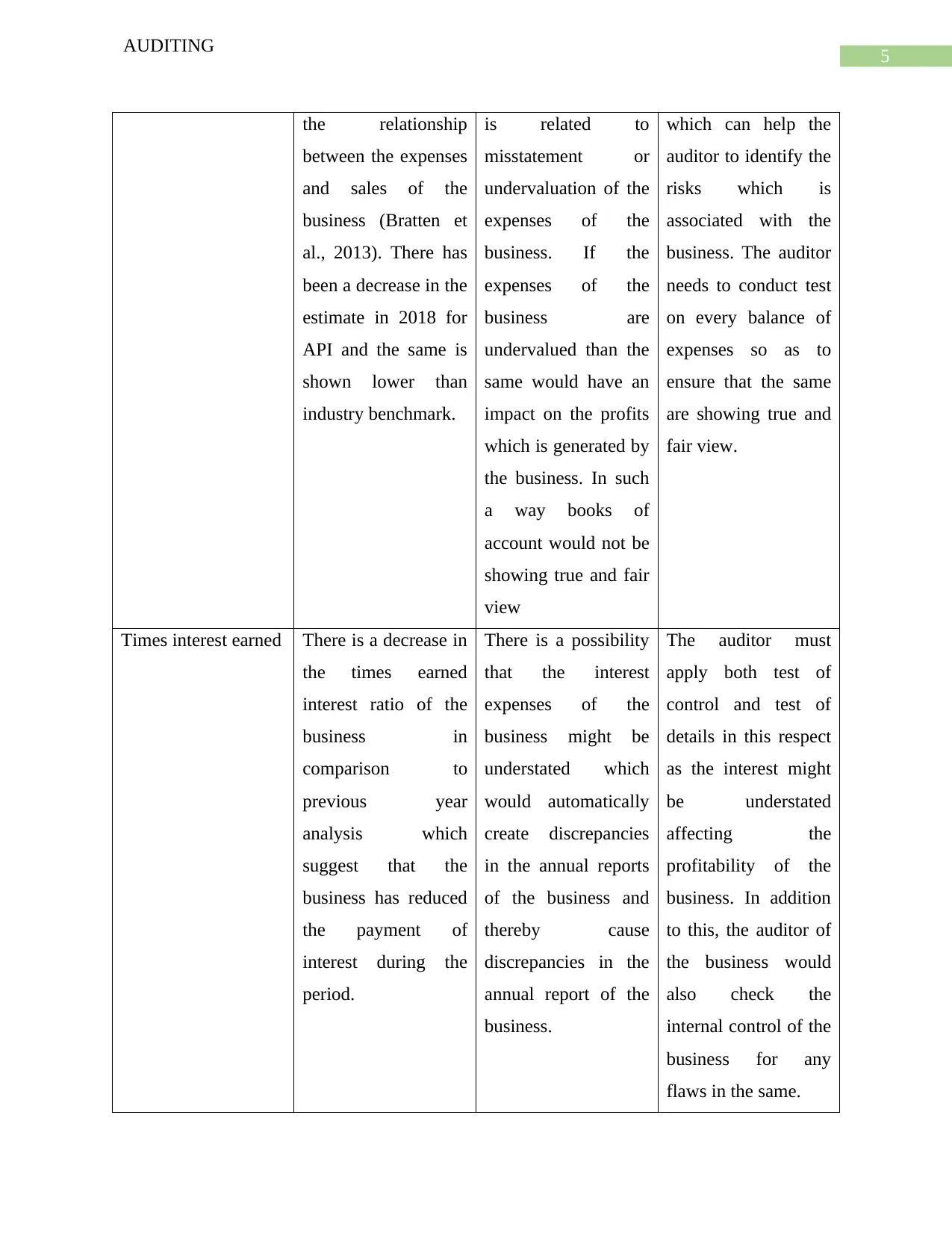

the relationship

between the expenses

and sales of the

business (Bratten et

al., 2013). There has

been a decrease in the

estimate in 2018 for

API and the same is

shown lower than

industry benchmark.

is related to

misstatement or

undervaluation of the

expenses of the

business. If the

expenses of the

business are

undervalued than the

same would have an

impact on the profits

which is generated by

the business. In such

a way books of

account would not be

showing true and fair

view

which can help the

auditor to identify the

risks which is

associated with the

business. The auditor

needs to conduct test

on every balance of

expenses so as to

ensure that the same

are showing true and

fair view.

Times interest earned There is a decrease in

the times earned

interest ratio of the

business in

comparison to

previous year

analysis which

suggest that the

business has reduced

the payment of

interest during the

period.

There is a possibility

that the interest

expenses of the

business might be

understated which

would automatically

create discrepancies

in the annual reports

of the business and

thereby cause

discrepancies in the

annual report of the

business.

The auditor must

apply both test of

control and test of

details in this respect

as the interest might

be understated

affecting the

profitability of the

business. In addition

to this, the auditor of

the business would

also check the

internal control of the

business for any

flaws in the same.

AUDITING

the relationship

between the expenses

and sales of the

business (Bratten et

al., 2013). There has

been a decrease in the

estimate in 2018 for

API and the same is

shown lower than

industry benchmark.

is related to

misstatement or

undervaluation of the

expenses of the

business. If the

expenses of the

business are

undervalued than the

same would have an

impact on the profits

which is generated by

the business. In such

a way books of

account would not be

showing true and fair

view

which can help the

auditor to identify the

risks which is

associated with the

business. The auditor

needs to conduct test

on every balance of

expenses so as to

ensure that the same

are showing true and

fair view.

Times interest earned There is a decrease in

the times earned

interest ratio of the

business in

comparison to

previous year

analysis which

suggest that the

business has reduced

the payment of

interest during the

period.

There is a possibility

that the interest

expenses of the

business might be

understated which

would automatically

create discrepancies

in the annual reports

of the business and

thereby cause

discrepancies in the

annual report of the

business.

The auditor must

apply both test of

control and test of

details in this respect

as the interest might

be understated

affecting the

profitability of the

business. In addition

to this, the auditor of

the business would

also check the

internal control of the

business for any

flaws in the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

AUDITING

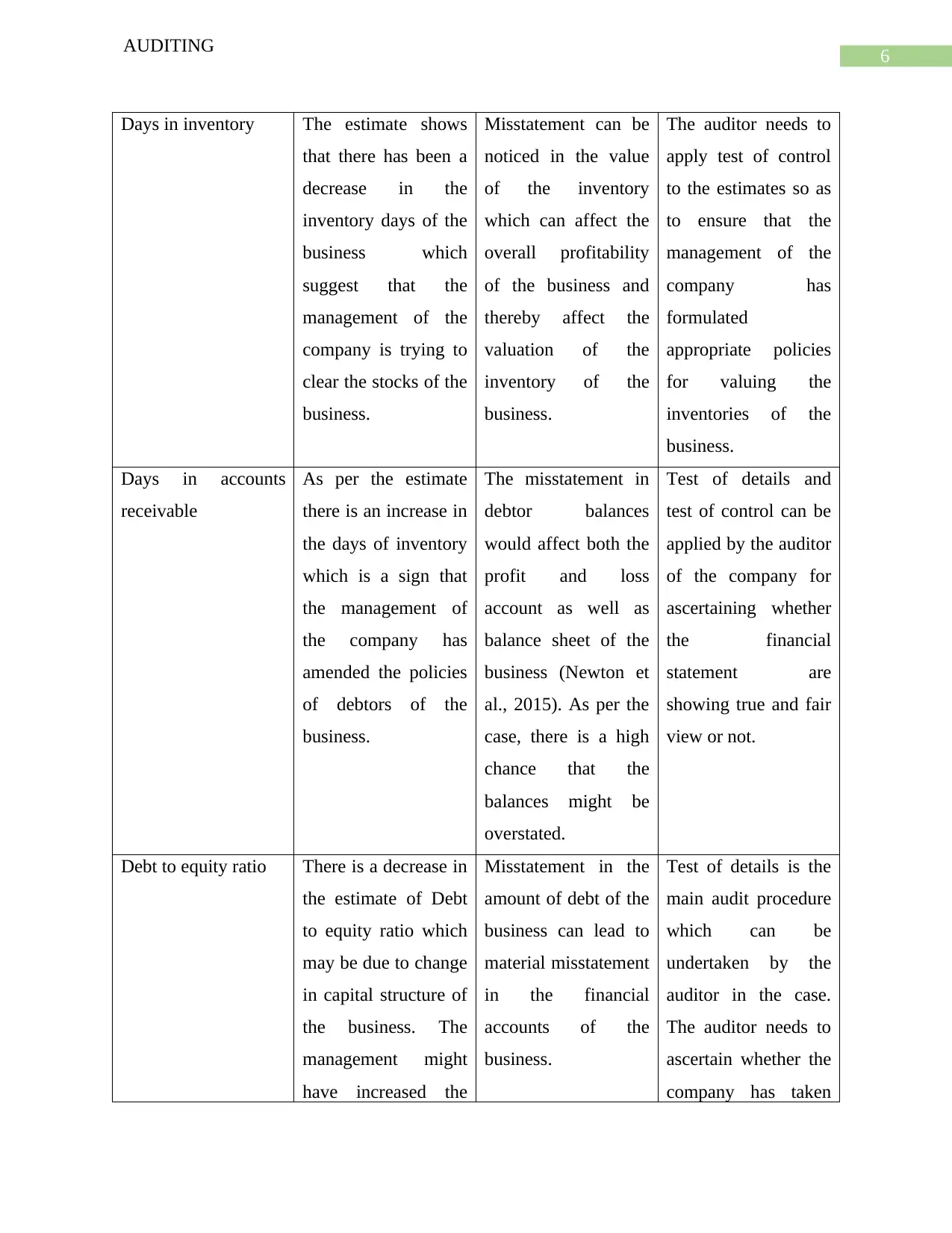

Days in inventory The estimate shows

that there has been a

decrease in the

inventory days of the

business which

suggest that the

management of the

company is trying to

clear the stocks of the

business.

Misstatement can be

noticed in the value

of the inventory

which can affect the

overall profitability

of the business and

thereby affect the

valuation of the

inventory of the

business.

The auditor needs to

apply test of control

to the estimates so as

to ensure that the

management of the

company has

formulated

appropriate policies

for valuing the

inventories of the

business.

Days in accounts

receivable

As per the estimate

there is an increase in

the days of inventory

which is a sign that

the management of

the company has

amended the policies

of debtors of the

business.

The misstatement in

debtor balances

would affect both the

profit and loss

account as well as

balance sheet of the

business (Newton et

al., 2015). As per the

case, there is a high

chance that the

balances might be

overstated.

Test of details and

test of control can be

applied by the auditor

of the company for

ascertaining whether

the financial

statement are

showing true and fair

view or not.

Debt to equity ratio There is a decrease in

the estimate of Debt

to equity ratio which

may be due to change

in capital structure of

the business. The

management might

have increased the

Misstatement in the

amount of debt of the

business can lead to

material misstatement

in the financial

accounts of the

business.

Test of details is the

main audit procedure

which can be

undertaken by the

auditor in the case.

The auditor needs to

ascertain whether the

company has taken

AUDITING

Days in inventory The estimate shows

that there has been a

decrease in the

inventory days of the

business which

suggest that the

management of the

company is trying to

clear the stocks of the

business.

Misstatement can be

noticed in the value

of the inventory

which can affect the

overall profitability

of the business and

thereby affect the

valuation of the

inventory of the

business.

The auditor needs to

apply test of control

to the estimates so as

to ensure that the

management of the

company has

formulated

appropriate policies

for valuing the

inventories of the

business.

Days in accounts

receivable

As per the estimate

there is an increase in

the days of inventory

which is a sign that

the management of

the company has

amended the policies

of debtors of the

business.

The misstatement in

debtor balances

would affect both the

profit and loss

account as well as

balance sheet of the

business (Newton et

al., 2015). As per the

case, there is a high

chance that the

balances might be

overstated.

Test of details and

test of control can be

applied by the auditor

of the company for

ascertaining whether

the financial

statement are

showing true and fair

view or not.

Debt to equity ratio There is a decrease in

the estimate of Debt

to equity ratio which

may be due to change

in capital structure of

the business. The

management might

have increased the

Misstatement in the

amount of debt of the

business can lead to

material misstatement

in the financial

accounts of the

business.

Test of details is the

main audit procedure

which can be

undertaken by the

auditor in the case.

The auditor needs to

ascertain whether the

company has taken

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

AUDITING

proportion of debt

capital in the capital

mix of the business.

additional debts

during the year or

not.

Weaknesses in Inventory Internal Control, Audit Risk and Procedures

Internal Control Weakness Audit Risk Audit Procedure

The weakness in the system

which has been identified in

the process is that the stock

of raw materials of the

computers has been lowered

to about 70 percent where it

was the responsibility of the

department to generate the

purchase orders. This kind

of errors will lead to dispute

in the purchase orders.

The audit risk which is

associated here is that it

creates major implication on

the purchase orders.

Improper adjustments in the

purchase orders of the can

lead to loss for the API.

The significant audit

procedures must be acquired

in this case to further test the

internal control system and

the risk associated with it.

Testing must be conducted

on an interval basis through

the computerised system

which will further reduce the

chances of fraud and error in

the system (Chang et al.,

2019).

Another major weakness in

the system which is

identified in such a situation

is that the inventory internal

control system of API is

further dependent on the

orders which is computer

generated. Hence, in such

circumstances the disputes

in the computer can hamper

the overall production

This kind of weakness

further crease audit risk with

the potential impact on the

system. There will be high

chance of failure regarding

the placements of the raw

material or the finished

products of the firm. The

date of the production might

show error in the system can

automatically hamper the

It is hence needed to reduce

the risk by ensuring that the

internal control management

of the company enhances the

computerised system by

removing the glitches

associated in the same.

Regular upgrading in the

system is needed to make

sure that the system remains

error free. This will further

AUDITING

proportion of debt

capital in the capital

mix of the business.

additional debts

during the year or

not.

Weaknesses in Inventory Internal Control, Audit Risk and Procedures

Internal Control Weakness Audit Risk Audit Procedure

The weakness in the system

which has been identified in

the process is that the stock

of raw materials of the

computers has been lowered

to about 70 percent where it

was the responsibility of the

department to generate the

purchase orders. This kind

of errors will lead to dispute

in the purchase orders.

The audit risk which is

associated here is that it

creates major implication on

the purchase orders.

Improper adjustments in the

purchase orders of the can

lead to loss for the API.

The significant audit

procedures must be acquired

in this case to further test the

internal control system and

the risk associated with it.

Testing must be conducted

on an interval basis through

the computerised system

which will further reduce the

chances of fraud and error in

the system (Chang et al.,

2019).

Another major weakness in

the system which is

identified in such a situation

is that the inventory internal

control system of API is

further dependent on the

orders which is computer

generated. Hence, in such

circumstances the disputes

in the computer can hamper

the overall production

This kind of weakness

further crease audit risk with

the potential impact on the

system. There will be high

chance of failure regarding

the placements of the raw

material or the finished

products of the firm. The

date of the production might

show error in the system can

automatically hamper the

It is hence needed to reduce

the risk by ensuring that the

internal control management

of the company enhances the

computerised system by

removing the glitches

associated in the same.

Regular upgrading in the

system is needed to make

sure that the system remains

error free. This will further

8

AUDITING

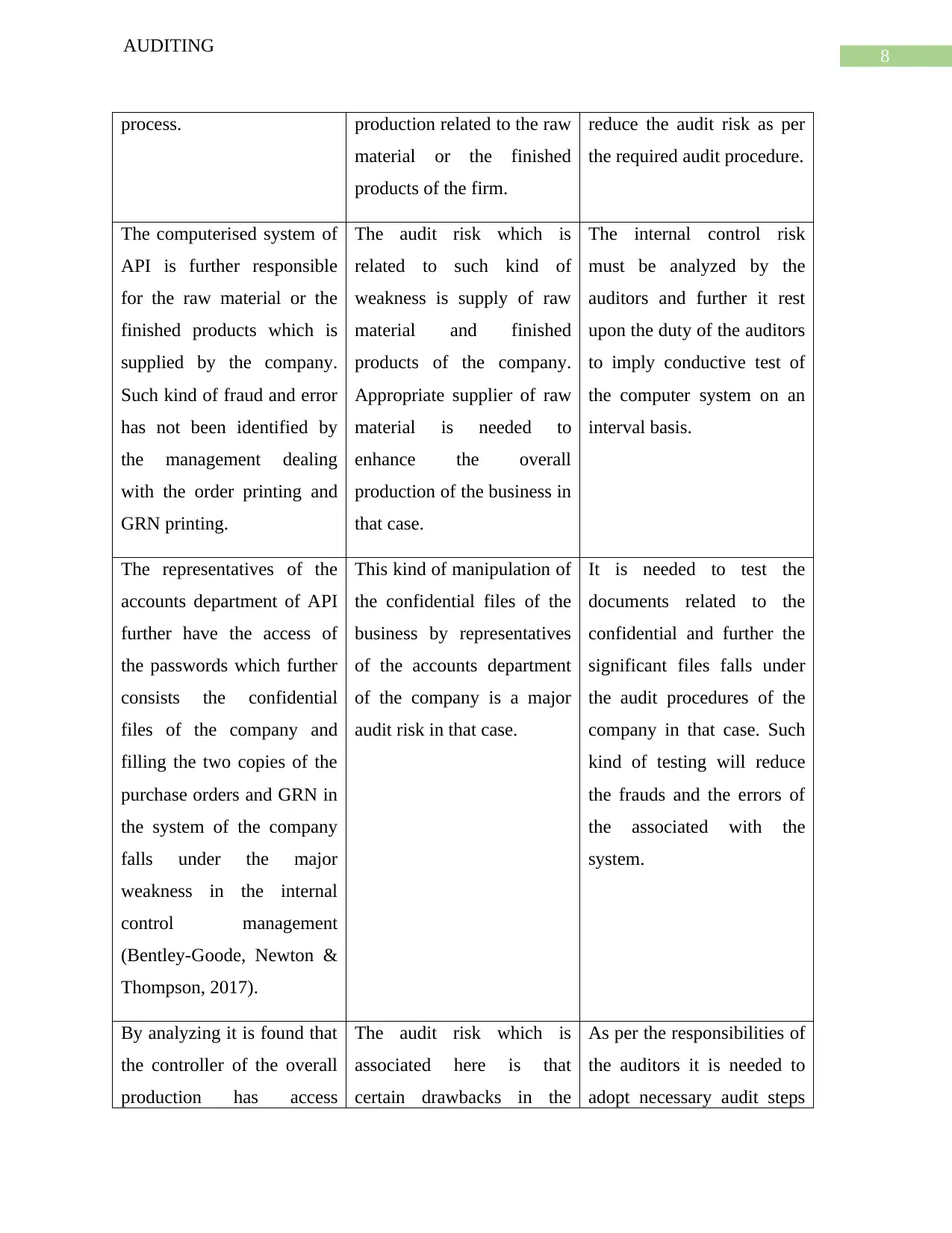

process. production related to the raw

material or the finished

products of the firm.

reduce the audit risk as per

the required audit procedure.

The computerised system of

API is further responsible

for the raw material or the

finished products which is

supplied by the company.

Such kind of fraud and error

has not been identified by

the management dealing

with the order printing and

GRN printing.

The audit risk which is

related to such kind of

weakness is supply of raw

material and finished

products of the company.

Appropriate supplier of raw

material is needed to

enhance the overall

production of the business in

that case.

The internal control risk

must be analyzed by the

auditors and further it rest

upon the duty of the auditors

to imply conductive test of

the computer system on an

interval basis.

The representatives of the

accounts department of API

further have the access of

the passwords which further

consists the confidential

files of the company and

filling the two copies of the

purchase orders and GRN in

the system of the company

falls under the major

weakness in the internal

control management

(Bentley-Goode, Newton &

Thompson, 2017).

This kind of manipulation of

the confidential files of the

business by representatives

of the accounts department

of the company is a major

audit risk in that case.

It is needed to test the

documents related to the

confidential and further the

significant files falls under

the audit procedures of the

company in that case. Such

kind of testing will reduce

the frauds and the errors of

the associated with the

system.

By analyzing it is found that

the controller of the overall

production has access

The audit risk which is

associated here is that

certain drawbacks in the

As per the responsibilities of

the auditors it is needed to

adopt necessary audit steps

AUDITING

process. production related to the raw

material or the finished

products of the firm.

reduce the audit risk as per

the required audit procedure.

The computerised system of

API is further responsible

for the raw material or the

finished products which is

supplied by the company.

Such kind of fraud and error

has not been identified by

the management dealing

with the order printing and

GRN printing.

The audit risk which is

related to such kind of

weakness is supply of raw

material and finished

products of the company.

Appropriate supplier of raw

material is needed to

enhance the overall

production of the business in

that case.

The internal control risk

must be analyzed by the

auditors and further it rest

upon the duty of the auditors

to imply conductive test of

the computer system on an

interval basis.

The representatives of the

accounts department of API

further have the access of

the passwords which further

consists the confidential

files of the company and

filling the two copies of the

purchase orders and GRN in

the system of the company

falls under the major

weakness in the internal

control management

(Bentley-Goode, Newton &

Thompson, 2017).

This kind of manipulation of

the confidential files of the

business by representatives

of the accounts department

of the company is a major

audit risk in that case.

It is needed to test the

documents related to the

confidential and further the

significant files falls under

the audit procedures of the

company in that case. Such

kind of testing will reduce

the frauds and the errors of

the associated with the

system.

By analyzing it is found that

the controller of the overall

production has access

The audit risk which is

associated here is that

certain drawbacks in the

As per the responsibilities of

the auditors it is needed to

adopt necessary audit steps

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

AUDITING

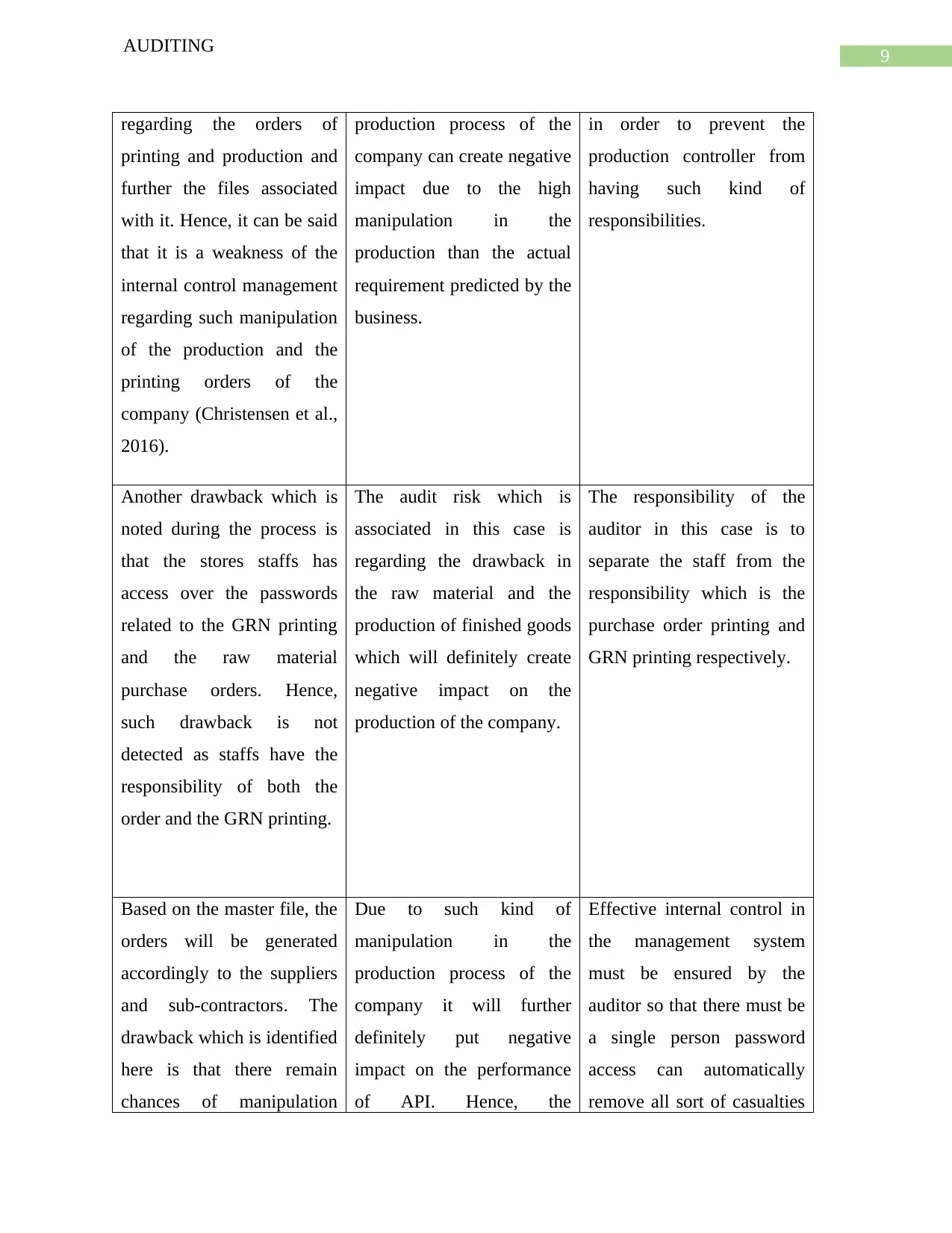

regarding the orders of

printing and production and

further the files associated

with it. Hence, it can be said

that it is a weakness of the

internal control management

regarding such manipulation

of the production and the

printing orders of the

company (Christensen et al.,

2016).

production process of the

company can create negative

impact due to the high

manipulation in the

production than the actual

requirement predicted by the

business.

in order to prevent the

production controller from

having such kind of

responsibilities.

Another drawback which is

noted during the process is

that the stores staffs has

access over the passwords

related to the GRN printing

and the raw material

purchase orders. Hence,

such drawback is not

detected as staffs have the

responsibility of both the

order and the GRN printing.

The audit risk which is

associated in this case is

regarding the drawback in

the raw material and the

production of finished goods

which will definitely create

negative impact on the

production of the company.

The responsibility of the

auditor in this case is to

separate the staff from the

responsibility which is the

purchase order printing and

GRN printing respectively.

Based on the master file, the

orders will be generated

accordingly to the suppliers

and sub-contractors. The

drawback which is identified

here is that there remain

chances of manipulation

Due to such kind of

manipulation in the

production process of the

company it will further

definitely put negative

impact on the performance

of API. Hence, the

Effective internal control in

the management system

must be ensured by the

auditor so that there must be

a single person password

access can automatically

remove all sort of casualties

AUDITING

regarding the orders of

printing and production and

further the files associated

with it. Hence, it can be said

that it is a weakness of the

internal control management

regarding such manipulation

of the production and the

printing orders of the

company (Christensen et al.,

2016).

production process of the

company can create negative

impact due to the high

manipulation in the

production than the actual

requirement predicted by the

business.

in order to prevent the

production controller from

having such kind of

responsibilities.

Another drawback which is

noted during the process is

that the stores staffs has

access over the passwords

related to the GRN printing

and the raw material

purchase orders. Hence,

such drawback is not

detected as staffs have the

responsibility of both the

order and the GRN printing.

The audit risk which is

associated in this case is

regarding the drawback in

the raw material and the

production of finished goods

which will definitely create

negative impact on the

production of the company.

The responsibility of the

auditor in this case is to

separate the staff from the

responsibility which is the

purchase order printing and

GRN printing respectively.

Based on the master file, the

orders will be generated

accordingly to the suppliers

and sub-contractors. The

drawback which is identified

here is that there remain

chances of manipulation

Due to such kind of

manipulation in the

production process of the

company it will further

definitely put negative

impact on the performance

of API. Hence, the

Effective internal control in

the management system

must be ensured by the

auditor so that there must be

a single person password

access can automatically

remove all sort of casualties

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

AUDITING

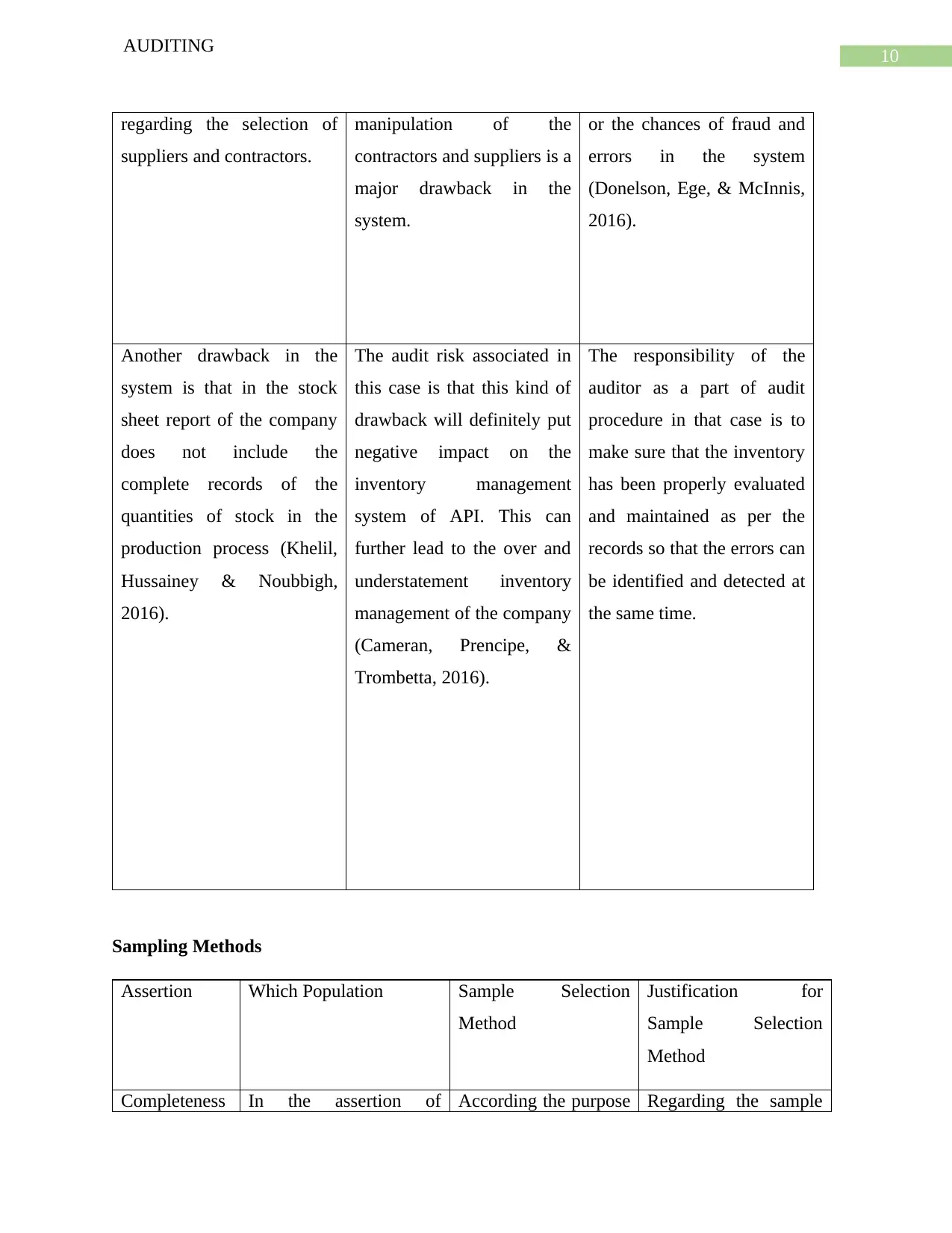

regarding the selection of

suppliers and contractors.

manipulation of the

contractors and suppliers is a

major drawback in the

system.

or the chances of fraud and

errors in the system

(Donelson, Ege, & McInnis,

2016).

Another drawback in the

system is that in the stock

sheet report of the company

does not include the

complete records of the

quantities of stock in the

production process (Khelil,

Hussainey & Noubbigh,

2016).

The audit risk associated in

this case is that this kind of

drawback will definitely put

negative impact on the

inventory management

system of API. This can

further lead to the over and

understatement inventory

management of the company

(Cameran, Prencipe, &

Trombetta, 2016).

The responsibility of the

auditor as a part of audit

procedure in that case is to

make sure that the inventory

has been properly evaluated

and maintained as per the

records so that the errors can

be identified and detected at

the same time.

Sampling Methods

Assertion Which Population Sample Selection

Method

Justification for

Sample Selection

Method

Completeness In the assertion of According the purpose Regarding the sample

AUDITING

regarding the selection of

suppliers and contractors.

manipulation of the

contractors and suppliers is a

major drawback in the

system.

or the chances of fraud and

errors in the system

(Donelson, Ege, & McInnis,

2016).

Another drawback in the

system is that in the stock

sheet report of the company

does not include the

complete records of the

quantities of stock in the

production process (Khelil,

Hussainey & Noubbigh,

2016).

The audit risk associated in

this case is that this kind of

drawback will definitely put

negative impact on the

inventory management

system of API. This can

further lead to the over and

understatement inventory

management of the company

(Cameran, Prencipe, &

Trombetta, 2016).

The responsibility of the

auditor as a part of audit

procedure in that case is to

make sure that the inventory

has been properly evaluated

and maintained as per the

records so that the errors can

be identified and detected at

the same time.

Sampling Methods

Assertion Which Population Sample Selection

Method

Justification for

Sample Selection

Method

Completeness In the assertion of According the purpose Regarding the sample

11

AUDITING

completeness there must

be the record of all the

financial transaction in

the financial statement of

the company. This

particular assertion is

related to the

understatement of the

inventories of the

company. In such a

situation it is the duty of

Wayne to collect the

required information’s

regarding the purchase of

raw material and the

finished products

(Knechel 2016).

of assertions, the

required sample

selection process of

the company must be

in a systematic way.

This further requires

identifying the

uniformity in the

physical units from the

evaluation of the

entire system (William

Jr, Glover & Prawitt,

2016).

selection method, it is

the most suitable

method which must be

undertaken by the

auditor. In this method

it can further be

ascertained by Wayne

is that there must be

implication of the even

system for sampling

the entire population of

the selected samples in

such circumstances.

On behalf o f the

company, Wayne will

further be able to

regulate the sampling

of raw material

purchased and finished

goods produced in

such a positive way.

Hence in such

circumstances, the

detection of frauds and

errors in the inventory

account of API

increases which is

positive point as per

the business

perspective. This kind

of sampling methods

AUDITING

completeness there must

be the record of all the

financial transaction in

the financial statement of

the company. This

particular assertion is

related to the

understatement of the

inventories of the

company. In such a

situation it is the duty of

Wayne to collect the

required information’s

regarding the purchase of

raw material and the

finished products

(Knechel 2016).

of assertions, the

required sample

selection process of

the company must be

in a systematic way.

This further requires

identifying the

uniformity in the

physical units from the

evaluation of the

entire system (William

Jr, Glover & Prawitt,

2016).

selection method, it is

the most suitable

method which must be

undertaken by the

auditor. In this method

it can further be

ascertained by Wayne

is that there must be

implication of the even

system for sampling

the entire population of

the selected samples in

such circumstances.

On behalf o f the

company, Wayne will

further be able to

regulate the sampling

of raw material

purchased and finished

goods produced in

such a positive way.

Hence in such

circumstances, the

detection of frauds and

errors in the inventory

account of API

increases which is

positive point as per

the business

perspective. This kind

of sampling methods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.