Comprehensive Audit Report: Select Harvests Limited Financial Analysis

VerifiedAdded on 2023/01/11

|13

|2320

|29

Report

AI Summary

This report provides a comprehensive audit analysis of Select Harvests Limited. It begins by determining the appropriate level of materiality for the 2019 audit, discussing the nature of materiality, its significance in financial statement audits, and the considerations for its determination, including a quantitative estimate. The report then reviews various draft notes and disclosures, highlighting significant aspects like contingencies and outlining necessary audit procedures. Furthermore, the report analyzes audit assertions, including account balances, classes of transactions, and presentation and disclosure, using ratio analysis to identify potential misstatements and related audit procedures. Finally, the report reviews the cash flow statement, analyzing cash inflows and outflows from operating, investing, and financing activities, and assessing the company's going concern risk, concluding with an overview of the company's financial position and compliance with accounting standards.

AUDIT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

Nature of materiality...............................................................................................................3

Section 2...........................................................................................................................................4

Audit assertion for HARVESTS LIMITED...........................................................................4

Section 3.........................................................................................................................................11

Review of cash flow statement.............................................................................................11

CONCLUSION..............................................................................................................................12

REEFRENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

Nature of materiality...............................................................................................................3

Section 2...........................................................................................................................................4

Audit assertion for HARVESTS LIMITED...........................................................................4

Section 3.........................................................................................................................................11

Review of cash flow statement.............................................................................................11

CONCLUSION..............................................................................................................................12

REEFRENCES..............................................................................................................................13

INTRODUCTION

Audit consists of the review or examination by an inspector of different records followed by a

practical warehouse check and make certain the recorded method of reporting purchases is used

by all agencies (Krishnan, 2015). It is required to ensure the correctness of the organization's

financial statements. The aim of audit is to review and validate the records with an impartial

body and insure that the accounting reports are handled in a correct way, and there is no

misstatement or theft.

In this level of materiality to be used for the audit, preliminary analytical review on the

information provided about company. In addition, review the statement of cash flows is also

discussed to identify the primary cash receipts and cash payments during the year.

Section 1

Nature of materiality

The principle of materiality is important for the audit. Auditors implement this in the

preparation process to perform an audit to determine the impact of reported audit failures and of

erroneous errors in the financial report, if any. Although the content of the audit may first be

decided at the layout level, auditors will be mindful of adjustments during the auditor of any

results of the audit which might involve re-evaluation of the original assessments.

Used materiality level in year 2018 by Select harvest limited- In year 2018, this company has

applied overall group materiality of 1.95 million. It indicates that 5% of group’s three year

average of profit before tax, excluding the three months. As well as they applied threshold,

together with qualitative way to find out the scope of audit (Starr, 2016).

Materiality level for year 2019 which can be used by Select harvest limited in their financial

statements:

There are three types of audit materiality which have different nature and feature. It

depends on companies that which method they can apply in their financial statements. Herein,

below description of audit materiality is mentioned that can be used by above mentioned

company:

Overall materiality- The overall value is referred to as the level that reflects the important point

in the firm's statements and will affect the decision-making by the consumers of the company's

financial reports as a whole as determined by the auditor nominated.

Audit consists of the review or examination by an inspector of different records followed by a

practical warehouse check and make certain the recorded method of reporting purchases is used

by all agencies (Krishnan, 2015). It is required to ensure the correctness of the organization's

financial statements. The aim of audit is to review and validate the records with an impartial

body and insure that the accounting reports are handled in a correct way, and there is no

misstatement or theft.

In this level of materiality to be used for the audit, preliminary analytical review on the

information provided about company. In addition, review the statement of cash flows is also

discussed to identify the primary cash receipts and cash payments during the year.

Section 1

Nature of materiality

The principle of materiality is important for the audit. Auditors implement this in the

preparation process to perform an audit to determine the impact of reported audit failures and of

erroneous errors in the financial report, if any. Although the content of the audit may first be

decided at the layout level, auditors will be mindful of adjustments during the auditor of any

results of the audit which might involve re-evaluation of the original assessments.

Used materiality level in year 2018 by Select harvest limited- In year 2018, this company has

applied overall group materiality of 1.95 million. It indicates that 5% of group’s three year

average of profit before tax, excluding the three months. As well as they applied threshold,

together with qualitative way to find out the scope of audit (Starr, 2016).

Materiality level for year 2019 which can be used by Select harvest limited in their financial

statements:

There are three types of audit materiality which have different nature and feature. It

depends on companies that which method they can apply in their financial statements. Herein,

below description of audit materiality is mentioned that can be used by above mentioned

company:

Overall materiality- The overall value is referred to as the level that reflects the important point

in the firm's statements and will affect the decision-making by the consumers of the company's

financial reports as a whole as determined by the auditor nominated.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overall performance materiality- The overall level of performance is the amount of materiality

measured by the auditor of the organization and could be smaller than the complete standard of

materiality. This degree of materiality is limited to that of the total level of materiality such that

the probability of many forms of slight mistakes or insignificant omissions, which the auditor

was not able to detect, is taken into consideration if calculated in full and thereby reduces the

chance of aggregates reaching the total materiality standard.

Specific materiality- Specific materialism relates to the degree of materiality to define the

potential irregularities in account balances that that impact users' economic decisions of business

financial statements in the case of particular fields inside the organization, for some types of

transactions.

From above mentioned three materiality, Select harvest limited should apply Overall materiality.

This is so because it is suitable for financial statements. As well as they have been applied this

method in last year too. It can be helpful for them making better assessment of their financial

position.

(Jamkhaneh and Gildeh, 2012)

Section 2

Audit assertion for HARVESTS LIMITED

Audit assertion is essential elements of audit process. Auditors use various audit assertions

in order to test policies, guidelines, financial reports, internal and external reports, statements of

finance of business organization. Many organizations consider it as presentation, measurement

of monetary information .It will provide basis for audit procedure. Audit procedure is the tools

which are used by auditors in order to identify quality of monetary and financial data provided

by their clients. Methods uses in audit procedure is totally depends on audit assertions of the

organization. Many business enterprises thought that preparation of financial statement, and

managing accounting are the responsibility of auditors, but an auditor or farm of audit only work

accuracy and for long their efficiency when management department of organization provides

them reliable and accurate information and proof of record. Auditor’s uses various assertions to

identifying risk of misstatement of material and theses are also used to formulate audit

procedure. Audit assertion is divided into 3 categories they ate related with the GAAP. It

includes account balance, classes of transactions presentation and disclosure of financial

measured by the auditor of the organization and could be smaller than the complete standard of

materiality. This degree of materiality is limited to that of the total level of materiality such that

the probability of many forms of slight mistakes or insignificant omissions, which the auditor

was not able to detect, is taken into consideration if calculated in full and thereby reduces the

chance of aggregates reaching the total materiality standard.

Specific materiality- Specific materialism relates to the degree of materiality to define the

potential irregularities in account balances that that impact users' economic decisions of business

financial statements in the case of particular fields inside the organization, for some types of

transactions.

From above mentioned three materiality, Select harvest limited should apply Overall materiality.

This is so because it is suitable for financial statements. As well as they have been applied this

method in last year too. It can be helpful for them making better assessment of their financial

position.

(Jamkhaneh and Gildeh, 2012)

Section 2

Audit assertion for HARVESTS LIMITED

Audit assertion is essential elements of audit process. Auditors use various audit assertions

in order to test policies, guidelines, financial reports, internal and external reports, statements of

finance of business organization. Many organizations consider it as presentation, measurement

of monetary information .It will provide basis for audit procedure. Audit procedure is the tools

which are used by auditors in order to identify quality of monetary and financial data provided

by their clients. Methods uses in audit procedure is totally depends on audit assertions of the

organization. Many business enterprises thought that preparation of financial statement, and

managing accounting are the responsibility of auditors, but an auditor or farm of audit only work

accuracy and for long their efficiency when management department of organization provides

them reliable and accurate information and proof of record. Auditor’s uses various assertions to

identifying risk of misstatement of material and theses are also used to formulate audit

procedure. Audit assertion is divided into 3 categories they ate related with the GAAP. It

includes account balance, classes of transactions presentation and disclosure of financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement. Auditors use assertion for measurement of accountancy of financial statement and on

the basis of theses they find out risk material area and they provides their suggestions and

identify the causes of differences arises between various factors of organization.

Ratio Analysis

Gross Profit Ratio

Particular Formula 2016 2017 2018 2019

Gross Profit

Ratio

Revenue –

Cost of goods

sold /

Revenue*

100

19.80 13.12 22.91 22.91

Net Profit Ratio

Particular Formula 2016 2017 2018 2019

Net

Profit

Ratio

Net Profit

/Net Sales

*100

11.82 3.85 9.86 9.86

Fixed assets turnover

Particular Formula 2016 2017 2018 2019

Fixed

assets

turnover

Net Sales /

Average

fixed assets

1.22 0.92 0.72 .72

Inventory turnover

Particular Formula 2016 2017 2018 2019

Inventory

turnover

Cost of

goods sold/

1.86 2.17 1.62 1.62

the basis of theses they find out risk material area and they provides their suggestions and

identify the causes of differences arises between various factors of organization.

Ratio Analysis

Gross Profit Ratio

Particular Formula 2016 2017 2018 2019

Gross Profit

Ratio

Revenue –

Cost of goods

sold /

Revenue*

100

19.80 13.12 22.91 22.91

Net Profit Ratio

Particular Formula 2016 2017 2018 2019

Net

Profit

Ratio

Net Profit

/Net Sales

*100

11.82 3.85 9.86 9.86

Fixed assets turnover

Particular Formula 2016 2017 2018 2019

Fixed

assets

turnover

Net Sales /

Average

fixed assets

1.22 0.92 0.72 .72

Inventory turnover

Particular Formula 2016 2017 2018 2019

Inventory

turnover

Cost of

goods sold/

1.86 2.17 1.62 1.62

Average

inventories

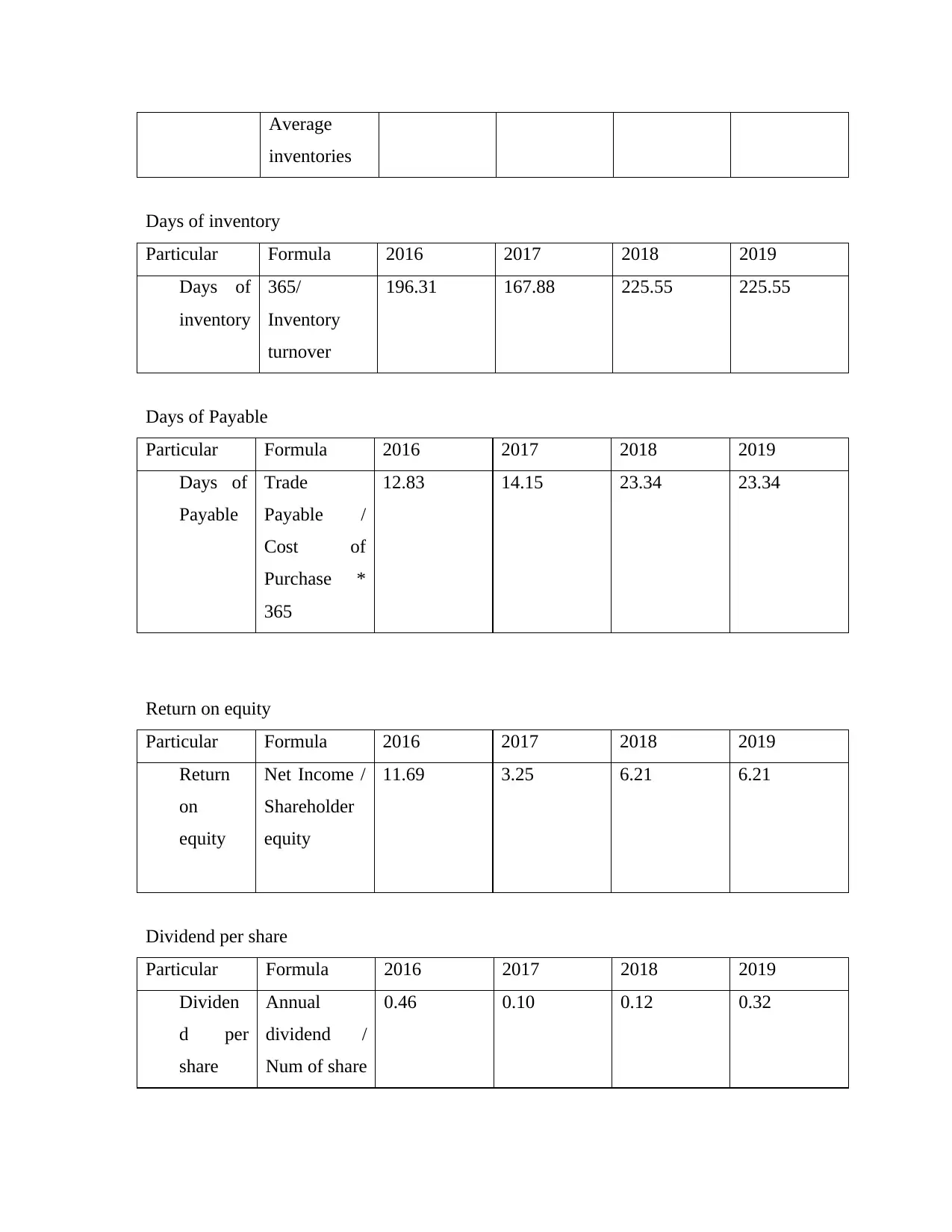

Days of inventory

Particular Formula 2016 2017 2018 2019

Days of

inventory

365/

Inventory

turnover

196.31 167.88 225.55 225.55

Days of Payable

Particular Formula 2016 2017 2018 2019

Days of

Payable

Trade

Payable /

Cost of

Purchase *

365

12.83 14.15 23.34 23.34

Return on equity

Particular Formula 2016 2017 2018 2019

Return

on

equity

Net Income /

Shareholder

equity

11.69 3.25 6.21 6.21

Dividend per share

Particular Formula 2016 2017 2018 2019

Dividen

d per

share

Annual

dividend /

Num of share

0.46 0.10 0.12 0.32

inventories

Days of inventory

Particular Formula 2016 2017 2018 2019

Days of

inventory

365/

Inventory

turnover

196.31 167.88 225.55 225.55

Days of Payable

Particular Formula 2016 2017 2018 2019

Days of

Payable

Trade

Payable /

Cost of

Purchase *

365

12.83 14.15 23.34 23.34

Return on equity

Particular Formula 2016 2017 2018 2019

Return

on

equity

Net Income /

Shareholder

equity

11.69 3.25 6.21 6.21

Dividend per share

Particular Formula 2016 2017 2018 2019

Dividen

d per

share

Annual

dividend /

Num of share

0.46 0.10 0.12 0.32

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

From all these ratio analysis it has been identified that as compare to other years in 2017 the

balance of accounts and difference among all ratio is different from another years, thus

auditors take investigation and identify causes of their changes and high differences. They

use 3 types of assertion:

Account balance: It included balance of accounts at they’re ended

Classes of transaction: Auditors take income statement transaction as basis of their assertion

calculation (Wen, Hao and Bu, 2015).

Presentation and discourse: It included how various accounts are presented in financial

statements.

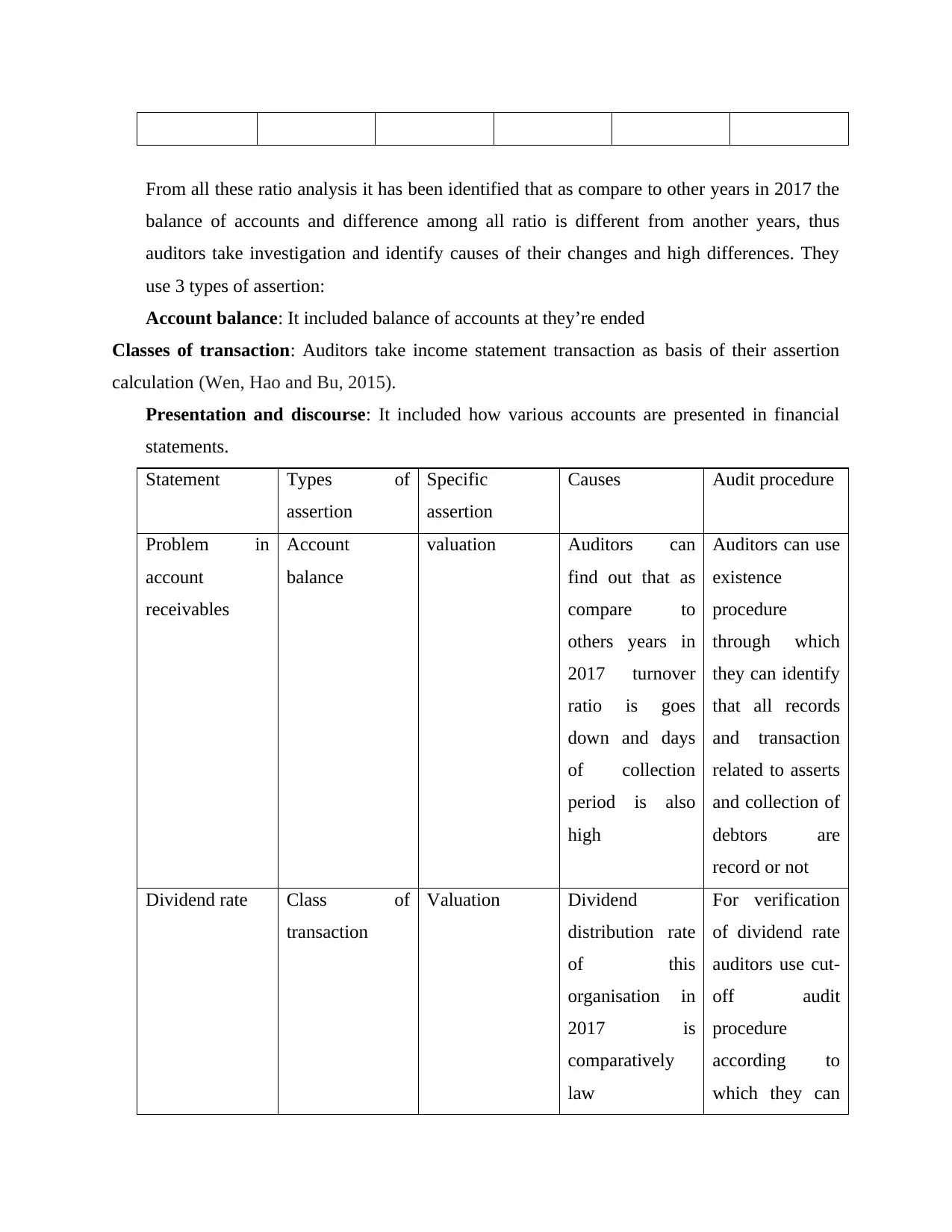

Statement Types of

assertion

Specific

assertion

Causes Audit procedure

Problem in

account

receivables

Account

balance

valuation Auditors can

find out that as

compare to

others years in

2017 turnover

ratio is goes

down and days

of collection

period is also

high

Auditors can use

existence

procedure

through which

they can identify

that all records

and transaction

related to asserts

and collection of

debtors are

record or not

Dividend rate Class of

transaction

Valuation Dividend

distribution rate

of this

organisation in

2017 is

comparatively

law

For verification

of dividend rate

auditors use cut-

off audit

procedure

according to

which they can

balance of accounts and difference among all ratio is different from another years, thus

auditors take investigation and identify causes of their changes and high differences. They

use 3 types of assertion:

Account balance: It included balance of accounts at they’re ended

Classes of transaction: Auditors take income statement transaction as basis of their assertion

calculation (Wen, Hao and Bu, 2015).

Presentation and discourse: It included how various accounts are presented in financial

statements.

Statement Types of

assertion

Specific

assertion

Causes Audit procedure

Problem in

account

receivables

Account

balance

valuation Auditors can

find out that as

compare to

others years in

2017 turnover

ratio is goes

down and days

of collection

period is also

high

Auditors can use

existence

procedure

through which

they can identify

that all records

and transaction

related to asserts

and collection of

debtors are

record or not

Dividend rate Class of

transaction

Valuation Dividend

distribution rate

of this

organisation in

2017 is

comparatively

law

For verification

of dividend rate

auditors use cut-

off audit

procedure

according to

which they can

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

find out and

check that all the

calculation and

earning save in

reserve are

calculation on

specific period

of time or not

Stock valuation

problem

Account

balance

Existence Due to lack of

inventory

management

system the turn

over ration is

comparatively

low

Completeness

testing audit

procedure has

been used for

verification of

stock that id any

transactions, or

recording o

stock martial has

been missing

during recording

proceed u on

not., for this

they check all

the invoices, of

purchaser.

Sales ratio Account

balance

Occurrence Auditors find

out the cases

which is the

reason of low

ratio of saes and

margin

For valuation of

correct margin

ratio they use

valuation audit

procedure in

order to check

all the

check that all the

calculation and

earning save in

reserve are

calculation on

specific period

of time or not

Stock valuation

problem

Account

balance

Existence Due to lack of

inventory

management

system the turn

over ration is

comparatively

low

Completeness

testing audit

procedure has

been used for

verification of

stock that id any

transactions, or

recording o

stock martial has

been missing

during recording

proceed u on

not., for this

they check all

the invoices, of

purchaser.

Sales ratio Account

balance

Occurrence Auditors find

out the cases

which is the

reason of low

ratio of saes and

margin

For valuation of

correct margin

ratio they use

valuation audit

procedure in

order to check

all the

transaction is

correctly record

as proof

(Jamkhaneh and

Gildeh, 2012).

This will use to

analysis the

effectively of

managing

department.

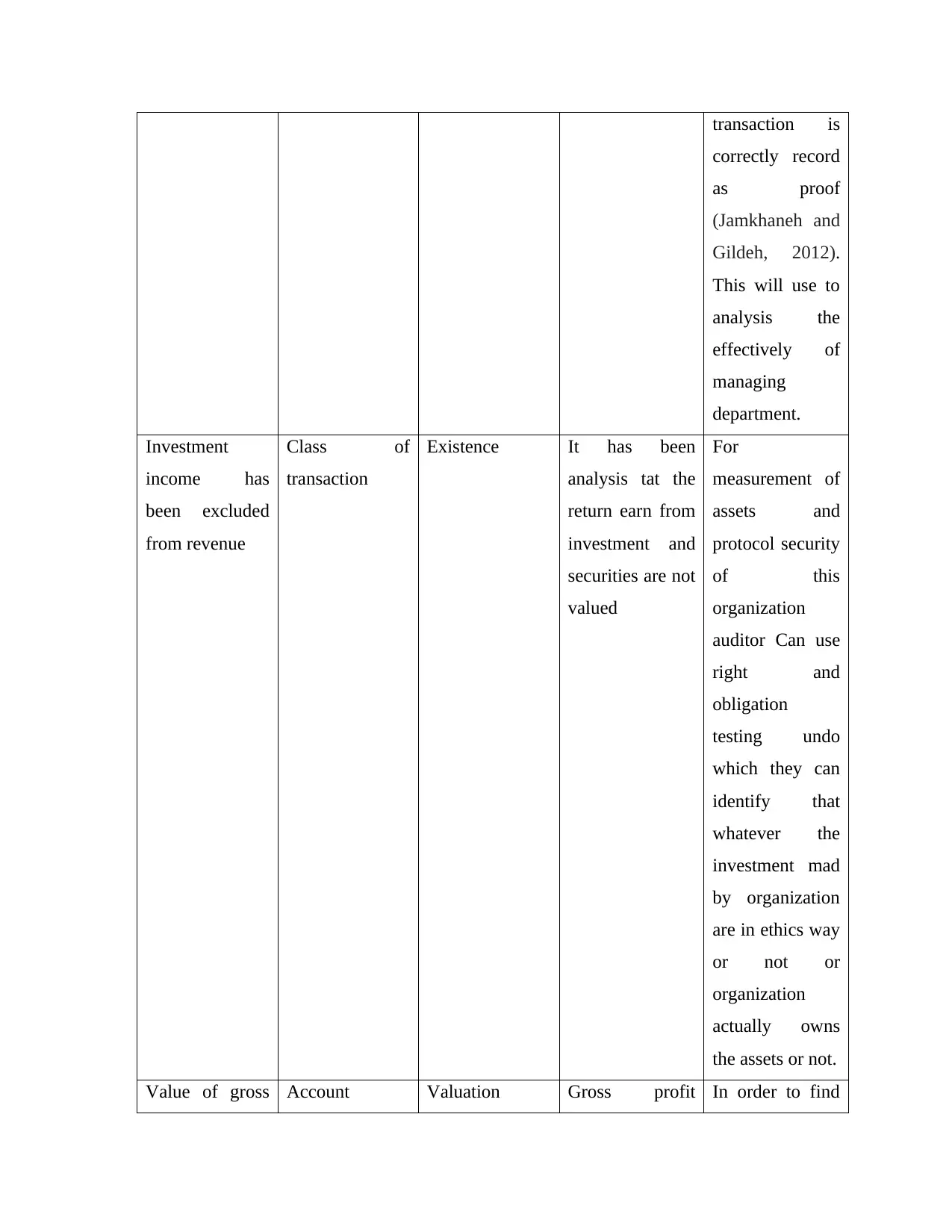

Investment

income has

been excluded

from revenue

Class of

transaction

Existence It has been

analysis tat the

return earn from

investment and

securities are not

valued

For

measurement of

assets and

protocol security

of this

organization

auditor Can use

right and

obligation

testing undo

which they can

identify that

whatever the

investment mad

by organization

are in ethics way

or not or

organization

actually owns

the assets or not.

Value of gross Account Valuation Gross profit In order to find

correctly record

as proof

(Jamkhaneh and

Gildeh, 2012).

This will use to

analysis the

effectively of

managing

department.

Investment

income has

been excluded

from revenue

Class of

transaction

Existence It has been

analysis tat the

return earn from

investment and

securities are not

valued

For

measurement of

assets and

protocol security

of this

organization

auditor Can use

right and

obligation

testing undo

which they can

identify that

whatever the

investment mad

by organization

are in ethics way

or not or

organization

actually owns

the assets or not.

Value of gross Account Valuation Gross profit In order to find

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

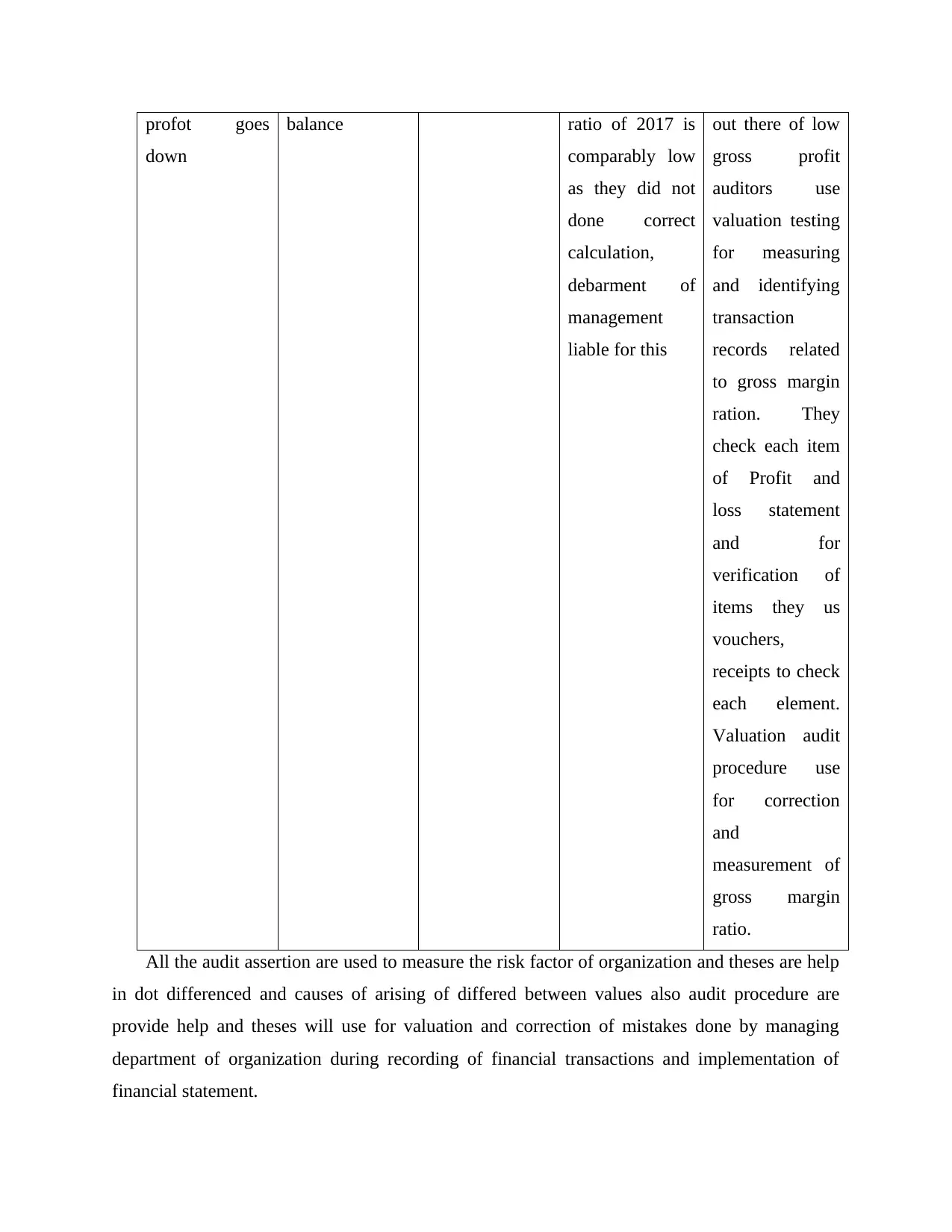

profot goes

down

balance ratio of 2017 is

comparably low

as they did not

done correct

calculation,

debarment of

management

liable for this

out there of low

gross profit

auditors use

valuation testing

for measuring

and identifying

transaction

records related

to gross margin

ration. They

check each item

of Profit and

loss statement

and for

verification of

items they us

vouchers,

receipts to check

each element.

Valuation audit

procedure use

for correction

and

measurement of

gross margin

ratio.

All the audit assertion are used to measure the risk factor of organization and theses are help

in dot differenced and causes of arising of differed between values also audit procedure are

provide help and theses will use for valuation and correction of mistakes done by managing

department of organization during recording of financial transactions and implementation of

financial statement.

down

balance ratio of 2017 is

comparably low

as they did not

done correct

calculation,

debarment of

management

liable for this

out there of low

gross profit

auditors use

valuation testing

for measuring

and identifying

transaction

records related

to gross margin

ration. They

check each item

of Profit and

loss statement

and for

verification of

items they us

vouchers,

receipts to check

each element.

Valuation audit

procedure use

for correction

and

measurement of

gross margin

ratio.

All the audit assertion are used to measure the risk factor of organization and theses are help

in dot differenced and causes of arising of differed between values also audit procedure are

provide help and theses will use for valuation and correction of mistakes done by managing

department of organization during recording of financial transactions and implementation of

financial statement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 3

Review of cash flow statement

The cash flow analysis demonstrates how a Harvest conducts business or where it gathers its

funds from (cash flows). Cash flows are shown in the cash balance report comprises all cash

flows obtained by a firm from its current operations and capital funding accounts and all cash

flows generated within the period for operating expenses and acquisitions (Cordeiro, Rodrigues

and de Castro, 2012). From the 2018-19 annual report of Harvest Limited it has been determined

that the highest money or cash inflow is from receipts from customer as in in 2018 it was ($,000)

77289 which really gets an immersive hike as ($,000) 310,929 in 2019. The net cash inflows

form the operating activities at the end of the year was 80337 which shows that Harvest Ltd have

enough operation that support in making higher results and recover the cost involved in

managing these operations. It was also determined that proceeds from the borrowing shows the

second most profitable cash inflows during the year 2019 which is 282,667as it was 39,100 in

year 2018. From the annual report, it is clearly identified that the cash outflows from the

financing activities was such as a hectic for company that it affect the overall profit during the

year. The repayment of borrowing was one of the most unprofitable activities or it can be stated

that maximum amount of cash outflow was happen form there. As in year 2018 it was (40,200)

which increase up to (313, 067) in year 2019 which reduces the net profit of company by a vast

margin. The non-cash financing activities for harvest Ltd was repayment of loan, repayment of

financial lease, dividend on ordinary share and reinvestment plan. Similarly the other non-cash

investing activities are payment of water right, payment of property, plant and equipment, tree

development costs. Through entire analysis of statement the going concern risk of Harvest ltd

was credit risk is the probability of loss arising from the non-repayment or breach of a loan by a

borrower. The prospect of an investor not being issued a mortgage and interest historically

means that cash balances can interrupt and payment costs rise. The credit risk can be offset by

over-cash flows. From the auditor’s report, it has been identified that the company is controlled

entity as per the corporation act 2001 which mainly includes Select Harvest Ltd give fair view of

all the financial position and is complying business as per the Australian accounting standard.

Review of cash flow statement

The cash flow analysis demonstrates how a Harvest conducts business or where it gathers its

funds from (cash flows). Cash flows are shown in the cash balance report comprises all cash

flows obtained by a firm from its current operations and capital funding accounts and all cash

flows generated within the period for operating expenses and acquisitions (Cordeiro, Rodrigues

and de Castro, 2012). From the 2018-19 annual report of Harvest Limited it has been determined

that the highest money or cash inflow is from receipts from customer as in in 2018 it was ($,000)

77289 which really gets an immersive hike as ($,000) 310,929 in 2019. The net cash inflows

form the operating activities at the end of the year was 80337 which shows that Harvest Ltd have

enough operation that support in making higher results and recover the cost involved in

managing these operations. It was also determined that proceeds from the borrowing shows the

second most profitable cash inflows during the year 2019 which is 282,667as it was 39,100 in

year 2018. From the annual report, it is clearly identified that the cash outflows from the

financing activities was such as a hectic for company that it affect the overall profit during the

year. The repayment of borrowing was one of the most unprofitable activities or it can be stated

that maximum amount of cash outflow was happen form there. As in year 2018 it was (40,200)

which increase up to (313, 067) in year 2019 which reduces the net profit of company by a vast

margin. The non-cash financing activities for harvest Ltd was repayment of loan, repayment of

financial lease, dividend on ordinary share and reinvestment plan. Similarly the other non-cash

investing activities are payment of water right, payment of property, plant and equipment, tree

development costs. Through entire analysis of statement the going concern risk of Harvest ltd

was credit risk is the probability of loss arising from the non-repayment or breach of a loan by a

borrower. The prospect of an investor not being issued a mortgage and interest historically

means that cash balances can interrupt and payment costs rise. The credit risk can be offset by

over-cash flows. From the auditor’s report, it has been identified that the company is controlled

entity as per the corporation act 2001 which mainly includes Select Harvest Ltd give fair view of

all the financial position and is complying business as per the Australian accounting standard.

CONCLUSION

In the end of the report, it has been concluded that the word audit obviously applies to an

analysis of the financial statements. An audit is an impartial analysis and assessment of an

organization's financial reports to insure that the annual reports provide a reasonable and correct

reflection of the activities that they appear to reflect. Internal accountants are paid by the

corporation or agency with which they undertake an audit and the subsequent audit report is

presented immediately to the managers and the boards of directors.

In the end of the report, it has been concluded that the word audit obviously applies to an

analysis of the financial statements. An audit is an impartial analysis and assessment of an

organization's financial reports to insure that the annual reports provide a reasonable and correct

reflection of the activities that they appear to reflect. Internal accountants are paid by the

corporation or agency with which they undertake an audit and the subsequent audit report is

presented immediately to the managers and the boards of directors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.