CQUniversity: ACCT20075 Auditing and Ethical Practices Report

VerifiedAdded on 2023/06/07

|17

|3392

|281

Report

AI Summary

This report provides a comprehensive analysis of auditing and ethical practices, focusing on the application of these principles to a specific company's financial statements. The report begins by defining materiality and its significance in the audit process, followed by an assessment of the firm's cash and cash equivalents, receivables, and assets. It calculates and analyzes financial ratios, including profitability, liquidity, and stability ratios, to evaluate the company's financial performance and position. Additionally, the report scrutinizes the statement of cash flow and reviews the audit report, providing an overall assessment of the company's financial health and the auditor's opinion. The report covers important aspects of the audit process, including the analysis of financial statements, application of materiality, and evaluation of financial ratios.

Running head: AUDITING AND ETHICAL PRACTICES

Auditing and Ethical Practices

Name of the Student:

Name of the University:

Authors Note:

Auditing and Ethical Practices

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHICAL PRACTICES

Table of Contents

Solution to Part 1........................................................................................................................2

Materiality..............................................................................................................................2

Enumeration of materiality....................................................................................................2

Materiality in audit.................................................................................................................3

Assessment of firm’s Cash and cash equivalents –................................................................3

Assessment of firm’s Receivables –......................................................................................3

Assessment of firm’s Assets –...............................................................................................3

Quantitative approximation of materiality of the firm Charter Hall Group...........................4

Analysis of Firm’s Draft notes together with disclosures......................................................4

Solution to Part 2:.......................................................................................................................6

Important financial ratios.......................................................................................................6

Profitability ratio-...................................................................................................................7

Liquidity ratio of the firm Charter Hall Group......................................................................8

Solution to part 3........................................................................................................................9

Analysis of the statement of stream of flow of cash..............................................................9

Going concern risk.................................................................................................................9

Audit report..........................................................................................................................10

References................................................................................................................................10

Table of Contents

Solution to Part 1........................................................................................................................2

Materiality..............................................................................................................................2

Enumeration of materiality....................................................................................................2

Materiality in audit.................................................................................................................3

Assessment of firm’s Cash and cash equivalents –................................................................3

Assessment of firm’s Receivables –......................................................................................3

Assessment of firm’s Assets –...............................................................................................3

Quantitative approximation of materiality of the firm Charter Hall Group...........................4

Analysis of Firm’s Draft notes together with disclosures......................................................4

Solution to Part 2:.......................................................................................................................6

Important financial ratios.......................................................................................................6

Profitability ratio-...................................................................................................................7

Liquidity ratio of the firm Charter Hall Group......................................................................8

Solution to part 3........................................................................................................................9

Analysis of the statement of stream of flow of cash..............................................................9

Going concern risk.................................................................................................................9

Audit report..........................................................................................................................10

References................................................................................................................................10

2AUDITING AND ETHICAL PRACTICES

Solution to Part 1

Materiality

Materiality can be considered to be one of most important notions for auditors.

Particularly, misstatements that entail omissions can be considered to be material when in

collectively or separately they can exert influence decisions of users of financial statements

(Knechel & Salterio, 2016). In itself, materiality in audit comprises of both qualitative as well

as quantitative facets. As such, materiality in the process of performing as well as planning

the audit lays stress on the below mentioned factors–

opinion on the subject of materiality are mainly based on varied situations and

circumstances that comprise of characteristics along with size of misstatements

Misstatements can be regarded to be material in case if it can exert impact on

decisions of users concerning the financial assertion (Junior, Best & Cotter 2014).

Opinions designed are based on common requirements of users as a group

Enumeration of materiality

According to qualitative research approach, materiality is approximated to be 5% of

firm’s net earnings before tax for the particular year under deliberation. Nevertheless, the

materiality is a subject of specialized professional opinions. As a result, in case if the firm’s

net earnings is observed to be volatile then there are other scales and points of references that

might be taken into account, such as firm’s revenue or else gross profit (Simnett, Carson &

Vanstraelen, 2016). Nevertheless, for majority of the profit earning firms, the most fitting

benchmark is the firm’s net income before tax. Profit gained before tax for the year ended

30th June 2017 of Charter Hall Group is registered to be $ 281 million. Thus, misstatement

Solution to Part 1

Materiality

Materiality can be considered to be one of most important notions for auditors.

Particularly, misstatements that entail omissions can be considered to be material when in

collectively or separately they can exert influence decisions of users of financial statements

(Knechel & Salterio, 2016). In itself, materiality in audit comprises of both qualitative as well

as quantitative facets. As such, materiality in the process of performing as well as planning

the audit lays stress on the below mentioned factors–

opinion on the subject of materiality are mainly based on varied situations and

circumstances that comprise of characteristics along with size of misstatements

Misstatements can be regarded to be material in case if it can exert impact on

decisions of users concerning the financial assertion (Junior, Best & Cotter 2014).

Opinions designed are based on common requirements of users as a group

Enumeration of materiality

According to qualitative research approach, materiality is approximated to be 5% of

firm’s net earnings before tax for the particular year under deliberation. Nevertheless, the

materiality is a subject of specialized professional opinions. As a result, in case if the firm’s

net earnings is observed to be volatile then there are other scales and points of references that

might be taken into account, such as firm’s revenue or else gross profit (Simnett, Carson &

Vanstraelen, 2016). Nevertheless, for majority of the profit earning firms, the most fitting

benchmark is the firm’s net income before tax. Profit gained before tax for the year ended

30th June 2017 of Charter Hall Group is registered to be $ 281 million. Thus, misstatement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHICAL PRACTICES

can be regarded to be material in case if the same amounts to be ($ 281 *5%) = $ 14.05

million or else over and above that.

Materiality in audit

Assessment of firm’s Cash and cash equivalents –

Cash as well as cash equivalent can be considered to be material in its nature. Seeing

that cash is for all time exposed to misappropriation, thievery and misuse, firm’s total cash

can be assessed and the balance can be matched with the statement of bank. Moreover, the

assessor can test out all the transaction of cash associated receipts, coupons, vouchers and

approval to assure that there are no misstatements (Jelinek, 2015). Analysis of the annual

report of the firm Charter Hall Group helps in identifying the fact that the cash and cash

equivalents of the firm has increased from $145 million in 2016 to $174 million in 2017. In

this case, the receipts of the payments in cash and statements of banks can be examined

appropriately.

Assessment of firm’s Receivables –

Receivables can be considered to be a material item as receivables are those items that

turn into bad debts when remain due for a long period of time. Thus, in a bid to verify the

status of firm’s receivables, the assessor has the need to undertake debtor’s aging analysis

and present queries concerning the ones that are due for over and above the period of credit

allowance (Taylor‐Alexander, 2017). In this case, receivables registered to be $65 million

during 2017 can be said to be material in terms of size.

Assessment of firm’s Assets –

Audit procedures such as classification testing can be undertaken to examine whether

purchase records for different fixed assets were appropriately categorised within the correct

account for fixed assets. The total assets of the firm are observed to have increased from

can be regarded to be material in case if the same amounts to be ($ 281 *5%) = $ 14.05

million or else over and above that.

Materiality in audit

Assessment of firm’s Cash and cash equivalents –

Cash as well as cash equivalent can be considered to be material in its nature. Seeing

that cash is for all time exposed to misappropriation, thievery and misuse, firm’s total cash

can be assessed and the balance can be matched with the statement of bank. Moreover, the

assessor can test out all the transaction of cash associated receipts, coupons, vouchers and

approval to assure that there are no misstatements (Jelinek, 2015). Analysis of the annual

report of the firm Charter Hall Group helps in identifying the fact that the cash and cash

equivalents of the firm has increased from $145 million in 2016 to $174 million in 2017. In

this case, the receipts of the payments in cash and statements of banks can be examined

appropriately.

Assessment of firm’s Receivables –

Receivables can be considered to be a material item as receivables are those items that

turn into bad debts when remain due for a long period of time. Thus, in a bid to verify the

status of firm’s receivables, the assessor has the need to undertake debtor’s aging analysis

and present queries concerning the ones that are due for over and above the period of credit

allowance (Taylor‐Alexander, 2017). In this case, receivables registered to be $65 million

during 2017 can be said to be material in terms of size.

Assessment of firm’s Assets –

Audit procedures such as classification testing can be undertaken to examine whether

purchase records for different fixed assets were appropriately categorised within the correct

account for fixed assets. The total assets of the firm are observed to have increased from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHICAL PRACTICES

$1421 million in 2016 to $1873 million in 2017. Real estate properties of the firm have also

increased from $15 million in 2016 to $19 million in the year 2017. The basic audit that can

be carried out in this regard is the investigation and thereby establishment of the fact that the

asset of the firm subsists.

Quantitative approximation of materiality of the firm Charter Hall Group

A wide range of approximately 50% to roughly 75% of planning materiality can be

regarded as acceptable misstatement for Charter Hall Group as level of risk concerning

financial statement is sensible. Again, the tolerable misstatement is founded to ascertain low

level for particular items that are separately important under specific financial items, for

example, firm’s cash, accounts receivables as well as inventories (Helin, & Babri, 2015).

Analysis of Firm’s Draft notes together with disclosures

Different items from the firm’s disclosure that are significant for the process of audit

are hereby discussed in detail below: –

Asset Impairment – For the purpose of undertaking audit on asset impairment, the assessor

might consider verifying all the supposition utilized for enumerating the value that is in use

and assessing the fair value that is reduced by the specific cost of selling. However, for the

purpose of auditing of impairment of asset, the carrying amount of specific assets can be

verified with asset register and other related documents (Moroney, 2015). Essentially, the

auditor of the firm might also consider testing out and checking depreciation techniques

together with market value of assets of the firm matched with firm’s assets to ensure that the

appropriate process has been implemented.

Contingent liabilities – this is the credible requirement of the firm that may perhaps add to

the firm’s payables founded on diverse forthcoming contingent event. However, if the firm’s

contingent liability becomes material otherwise if whole amount cannot be anticipated, the

$1421 million in 2016 to $1873 million in 2017. Real estate properties of the firm have also

increased from $15 million in 2016 to $19 million in the year 2017. The basic audit that can

be carried out in this regard is the investigation and thereby establishment of the fact that the

asset of the firm subsists.

Quantitative approximation of materiality of the firm Charter Hall Group

A wide range of approximately 50% to roughly 75% of planning materiality can be

regarded as acceptable misstatement for Charter Hall Group as level of risk concerning

financial statement is sensible. Again, the tolerable misstatement is founded to ascertain low

level for particular items that are separately important under specific financial items, for

example, firm’s cash, accounts receivables as well as inventories (Helin, & Babri, 2015).

Analysis of Firm’s Draft notes together with disclosures

Different items from the firm’s disclosure that are significant for the process of audit

are hereby discussed in detail below: –

Asset Impairment – For the purpose of undertaking audit on asset impairment, the assessor

might consider verifying all the supposition utilized for enumerating the value that is in use

and assessing the fair value that is reduced by the specific cost of selling. However, for the

purpose of auditing of impairment of asset, the carrying amount of specific assets can be

verified with asset register and other related documents (Moroney, 2015). Essentially, the

auditor of the firm might also consider testing out and checking depreciation techniques

together with market value of assets of the firm matched with firm’s assets to ensure that the

appropriate process has been implemented.

Contingent liabilities – this is the credible requirement of the firm that may perhaps add to

the firm’s payables founded on diverse forthcoming contingent event. However, if the firm’s

contingent liability becomes material otherwise if whole amount cannot be anticipated, the

5AUDITING AND ETHICAL PRACTICES

evaluator shall estimate probability and likelihood of happening of events. Fundamentally,

likelihood can be probable, sensibly possible otherwise remote. In a bid to review likelihood,

the assessor can apply specialised professional opinion (Gaynor et al., 2015). Nevertheless,

for plausible class of contingent liabilities the assessor can apply unique accounting

treatment. Additionally, the liability can be presented in the notes segment of the disclosure

section.

evaluator shall estimate probability and likelihood of happening of events. Fundamentally,

likelihood can be probable, sensibly possible otherwise remote. In a bid to review likelihood,

the assessor can apply specialised professional opinion (Gaynor et al., 2015). Nevertheless,

for plausible class of contingent liabilities the assessor can apply unique accounting

treatment. Additionally, the liability can be presented in the notes segment of the disclosure

section.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHICAL PRACTICES

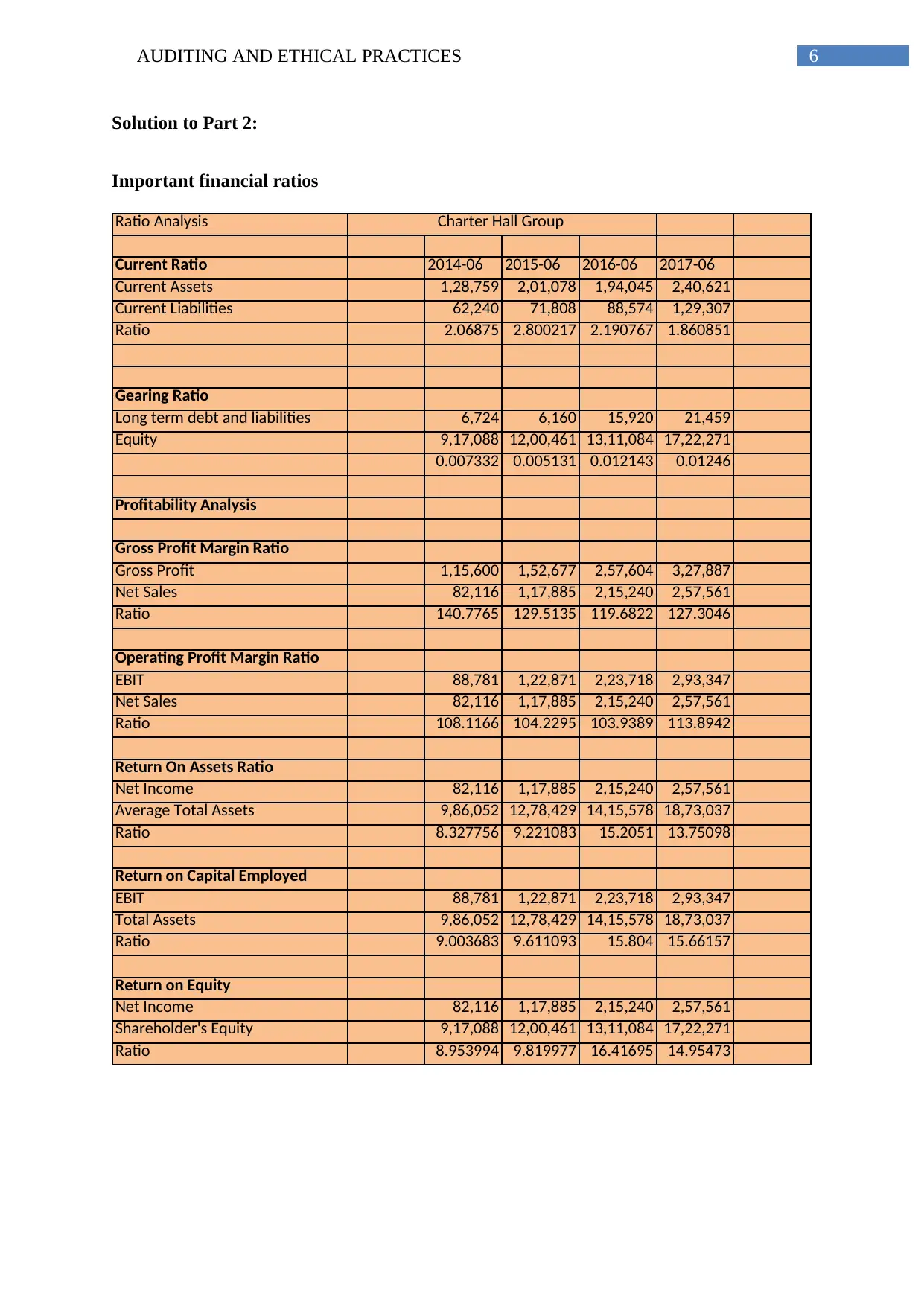

Solution to Part 2:

Important financial ratios

Ratio Analysis

Current Ratio 2014-06 2015-06 2016-06 2017-06

Current Assets 1,28,759 2,01,078 1,94,045 2,40,621

Current Liabilities 62,240 71,808 88,574 1,29,307

Ratio 2.06875 2.800217 2.190767 1.860851

Gearing Ratio

Long term debt and liabilities 6,724 6,160 15,920 21,459

Equity 9,17,088 12,00,461 13,11,084 17,22,271

0.007332 0.005131 0.012143 0.01246

Profitability Analysis

Gross Profit Margin Ratio

Gross Profit 1,15,600 1,52,677 2,57,604 3,27,887

Net Sales 82,116 1,17,885 2,15,240 2,57,561

Ratio 140.7765 129.5135 119.6822 127.3046

Operating Profit Margin Ratio

EBIT 88,781 1,22,871 2,23,718 2,93,347

Net Sales 82,116 1,17,885 2,15,240 2,57,561

Ratio 108.1166 104.2295 103.9389 113.8942

Return On Assets Ratio

Net Income 82,116 1,17,885 2,15,240 2,57,561

Average Total Assets 9,86,052 12,78,429 14,15,578 18,73,037

Ratio 8.327756 9.221083 15.2051 13.75098

Return on Capital Employed

EBIT 88,781 1,22,871 2,23,718 2,93,347

Total Assets 9,86,052 12,78,429 14,15,578 18,73,037

Ratio 9.003683 9.611093 15.804 15.66157

Return on Equity

Net Income 82,116 1,17,885 2,15,240 2,57,561

Shareholder's Equity 9,17,088 12,00,461 13,11,084 17,22,271

Ratio 8.953994 9.819977 16.41695 14.95473

Charter Hall Group

Solution to Part 2:

Important financial ratios

Ratio Analysis

Current Ratio 2014-06 2015-06 2016-06 2017-06

Current Assets 1,28,759 2,01,078 1,94,045 2,40,621

Current Liabilities 62,240 71,808 88,574 1,29,307

Ratio 2.06875 2.800217 2.190767 1.860851

Gearing Ratio

Long term debt and liabilities 6,724 6,160 15,920 21,459

Equity 9,17,088 12,00,461 13,11,084 17,22,271

0.007332 0.005131 0.012143 0.01246

Profitability Analysis

Gross Profit Margin Ratio

Gross Profit 1,15,600 1,52,677 2,57,604 3,27,887

Net Sales 82,116 1,17,885 2,15,240 2,57,561

Ratio 140.7765 129.5135 119.6822 127.3046

Operating Profit Margin Ratio

EBIT 88,781 1,22,871 2,23,718 2,93,347

Net Sales 82,116 1,17,885 2,15,240 2,57,561

Ratio 108.1166 104.2295 103.9389 113.8942

Return On Assets Ratio

Net Income 82,116 1,17,885 2,15,240 2,57,561

Average Total Assets 9,86,052 12,78,429 14,15,578 18,73,037

Ratio 8.327756 9.221083 15.2051 13.75098

Return on Capital Employed

EBIT 88,781 1,22,871 2,23,718 2,93,347

Total Assets 9,86,052 12,78,429 14,15,578 18,73,037

Ratio 9.003683 9.611093 15.804 15.66157

Return on Equity

Net Income 82,116 1,17,885 2,15,240 2,57,561

Shareholder's Equity 9,17,088 12,00,461 13,11,084 17,22,271

Ratio 8.953994 9.819977 16.41695 14.95473

Charter Hall Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHICAL PRACTICES

Profitability ratio-

Profitability ratios are primarily utilized to evaluate the company’s potency to acquire

profit in comparison to expenses of the firm. Essentially, net profit margin of the Charter Hall

Group reflects the profit retained with the firm after making disbursement for different

operational, financial as well as taxation expends of the firm. However, based on analysis of

key ratio it can be hereby stated that the operating profit ratio of the firm has increased from

103.93 % in 2016 to 113.89% in 2017 reflecting an upward moving trajectory and a desirable

financial situation. Again, gross profit margin shows a fluctuating trend throughout the period

2014-2017. This ratio initially dipped during the period 2015 in comparison to the year 2014.

Thereafter, it further declined in the year 2016. However, later on during the period 2017, this

ratio improved considerably, reflecting a favourable financial condition (SURYANTO,

2017). Again, return on firm’s asset represents profitability of the firm in comparison its

assets (Davies & Aston, 2017). Essentially, it reflects the level of efficiency of firm’s

management in utilizing its assets for generation of earnings.

There are different types of assertion that may possibly be associated to profitability

ratio is level of accurateness. It might be that different items of expends as well as incomes

might not have been properly registered in full amounts. Therefore, audit process for this

assertion shall be to test out that firm’s records for expends and earnings (Louwers et al.,

2015). This is mainly to examine whether accurate amount has been registered and to ensure

that there is no overstatement or understatement.

Stability ratio of the firm Charter Hall Group – The important financial ratio on stability

analyses the overall debt amount that can be supported by the business entity. Essentially, this

ratio is also implemented to determine financial leverage of the firm Charter Hall Group.

Again, Debt equity ratio enumerates overall proportion of firm’s assets that are funded by

Profitability ratio-

Profitability ratios are primarily utilized to evaluate the company’s potency to acquire

profit in comparison to expenses of the firm. Essentially, net profit margin of the Charter Hall

Group reflects the profit retained with the firm after making disbursement for different

operational, financial as well as taxation expends of the firm. However, based on analysis of

key ratio it can be hereby stated that the operating profit ratio of the firm has increased from

103.93 % in 2016 to 113.89% in 2017 reflecting an upward moving trajectory and a desirable

financial situation. Again, gross profit margin shows a fluctuating trend throughout the period

2014-2017. This ratio initially dipped during the period 2015 in comparison to the year 2014.

Thereafter, it further declined in the year 2016. However, later on during the period 2017, this

ratio improved considerably, reflecting a favourable financial condition (SURYANTO,

2017). Again, return on firm’s asset represents profitability of the firm in comparison its

assets (Davies & Aston, 2017). Essentially, it reflects the level of efficiency of firm’s

management in utilizing its assets for generation of earnings.

There are different types of assertion that may possibly be associated to profitability

ratio is level of accurateness. It might be that different items of expends as well as incomes

might not have been properly registered in full amounts. Therefore, audit process for this

assertion shall be to test out that firm’s records for expends and earnings (Louwers et al.,

2015). This is mainly to examine whether accurate amount has been registered and to ensure

that there is no overstatement or understatement.

Stability ratio of the firm Charter Hall Group – The important financial ratio on stability

analyses the overall debt amount that can be supported by the business entity. Essentially, this

ratio is also implemented to determine financial leverage of the firm Charter Hall Group.

Again, Debt equity ratio enumerates overall proportion of firm’s assets that are funded by

8AUDITING AND ETHICAL PRACTICES

means of borrowings. In particular, it can be seen that on an average roughly 34% to around

38% of firm’s assets are funded by using borrowed funds (Ferrell & Fraedrich, 2015).Again,

debt equity ratio also enumerates the overall debt and equity proportion of the firm to fund

assets. In this case, it can be recognized that equity proportion of the firm has considerably

increased during the period so as the debt. Also, the debt to equity ratio has also increased

although insignificantly during the period 2017 in comparison to the year ago period.

Varied categories of assertion that might perhaps be associated to the ratio on stability

is essentially accuracy. It might be the fact that different debt items, assets along with equities

of the firm might not be properly registered in the financial assertions of the firm. Therefore,

in that case, audit procedures might possibly involve the processs of verification of all the

associated documents on purchase of assets, data on borrowings, examination of register for

sales and catalog share issue (Carson, Fargher & Zhang, 2016).

Liquidity ratio of the firm Charter Hall Group – liquidity ratios are primarily utilized for

the purpose of measuring overall liquidity condition of the firm. The current ratio is

calculated for testing out whether the firm’s current assets of Charter Hall Group are adequate

enough to repay their current obligations. Based on the enumerated financial ratio it can be

said that current ratio has decreased 2.06 in 2014 to 1.86 in 2017. Thus, the liquidity

condition of the firm can be said to have deteriorated throughout the specified period.

A kind of assertion that may perhaps be attached to stability ratio is essentially

accuracy in addition to classification. In this case, it might be the fact that different current

assets as well as current liabilities items might perhaps not have been registered in full

amounts (Cohen & Simnett, 2014). Also, it might however so happen that firm’s current

assets as well as liabilities might not have been appropriately categorised. This means that

non-current assets/liabilities might have been categorised and identified as current. In this

means of borrowings. In particular, it can be seen that on an average roughly 34% to around

38% of firm’s assets are funded by using borrowed funds (Ferrell & Fraedrich, 2015).Again,

debt equity ratio also enumerates the overall debt and equity proportion of the firm to fund

assets. In this case, it can be recognized that equity proportion of the firm has considerably

increased during the period so as the debt. Also, the debt to equity ratio has also increased

although insignificantly during the period 2017 in comparison to the year ago period.

Varied categories of assertion that might perhaps be associated to the ratio on stability

is essentially accuracy. It might be the fact that different debt items, assets along with equities

of the firm might not be properly registered in the financial assertions of the firm. Therefore,

in that case, audit procedures might possibly involve the processs of verification of all the

associated documents on purchase of assets, data on borrowings, examination of register for

sales and catalog share issue (Carson, Fargher & Zhang, 2016).

Liquidity ratio of the firm Charter Hall Group – liquidity ratios are primarily utilized for

the purpose of measuring overall liquidity condition of the firm. The current ratio is

calculated for testing out whether the firm’s current assets of Charter Hall Group are adequate

enough to repay their current obligations. Based on the enumerated financial ratio it can be

said that current ratio has decreased 2.06 in 2014 to 1.86 in 2017. Thus, the liquidity

condition of the firm can be said to have deteriorated throughout the specified period.

A kind of assertion that may perhaps be attached to stability ratio is essentially

accuracy in addition to classification. In this case, it might be the fact that different current

assets as well as current liabilities items might perhaps not have been registered in full

amounts (Cohen & Simnett, 2014). Also, it might however so happen that firm’s current

assets as well as liabilities might not have been appropriately categorised. This means that

non-current assets/liabilities might have been categorised and identified as current. In this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHICAL PRACTICES

case, audit processes for this specific assertion would involve examination and verification of

different pertinent documents and register for firm’s current assets as well as current

liabilities.

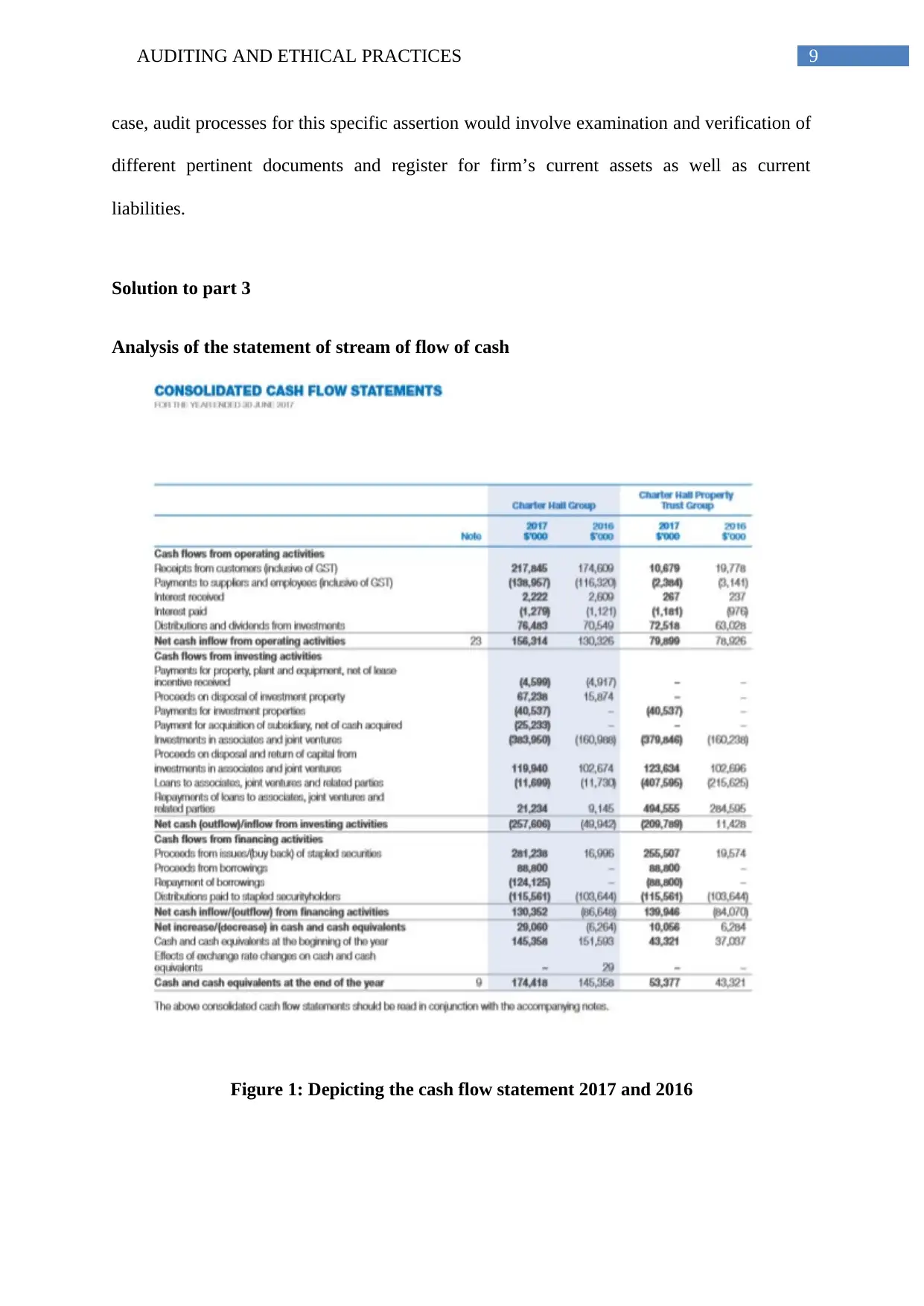

Solution to part 3

Analysis of the statement of stream of flow of cash

Figure 1: Depicting the cash flow statement 2017 and 2016

case, audit processes for this specific assertion would involve examination and verification of

different pertinent documents and register for firm’s current assets as well as current

liabilities.

Solution to part 3

Analysis of the statement of stream of flow of cash

Figure 1: Depicting the cash flow statement 2017 and 2016

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHICAL PRACTICES

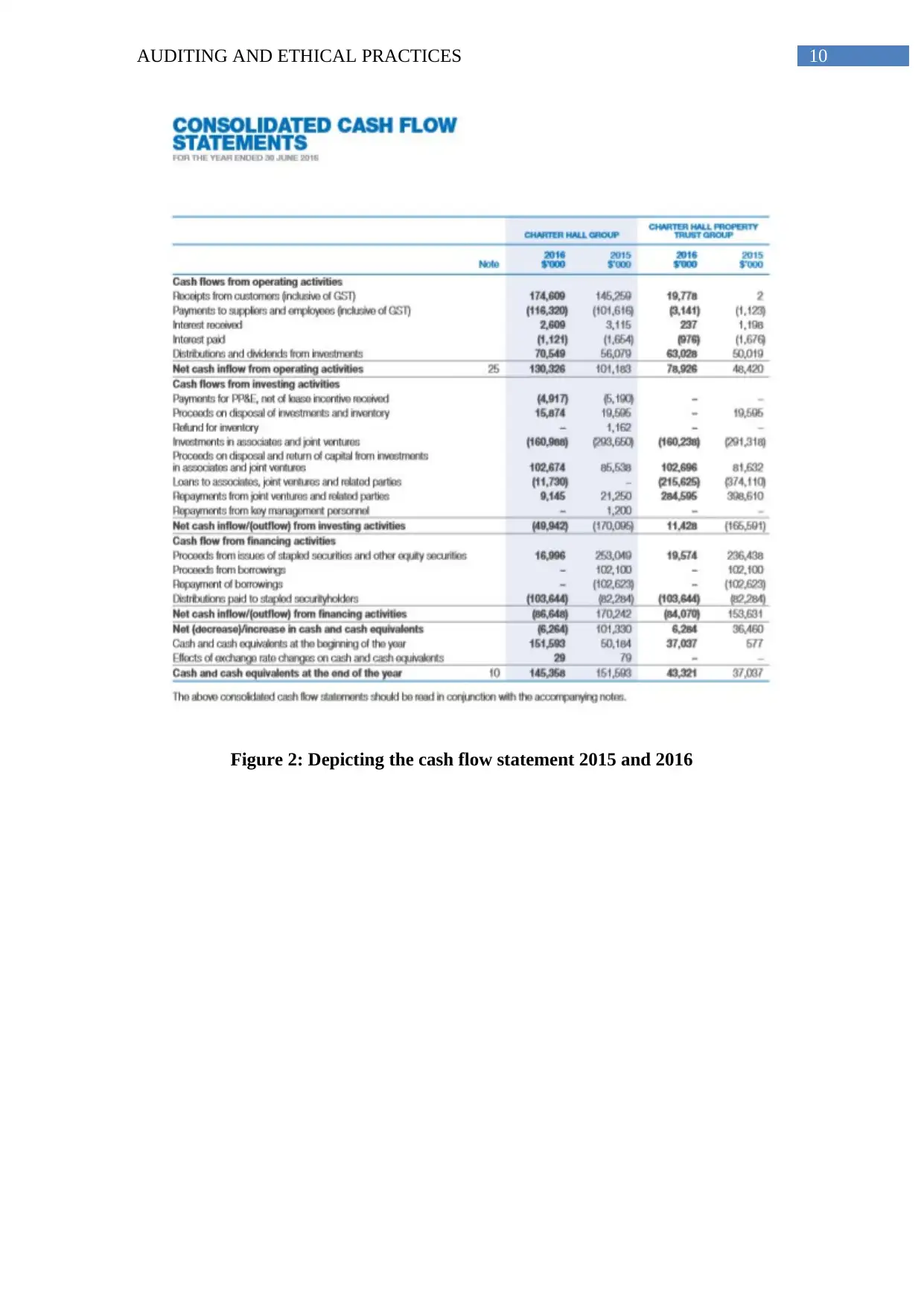

Figure 2: Depicting the cash flow statement 2015 and 2016

Figure 2: Depicting the cash flow statement 2015 and 2016

11AUDITING AND ETHICAL PRACTICES

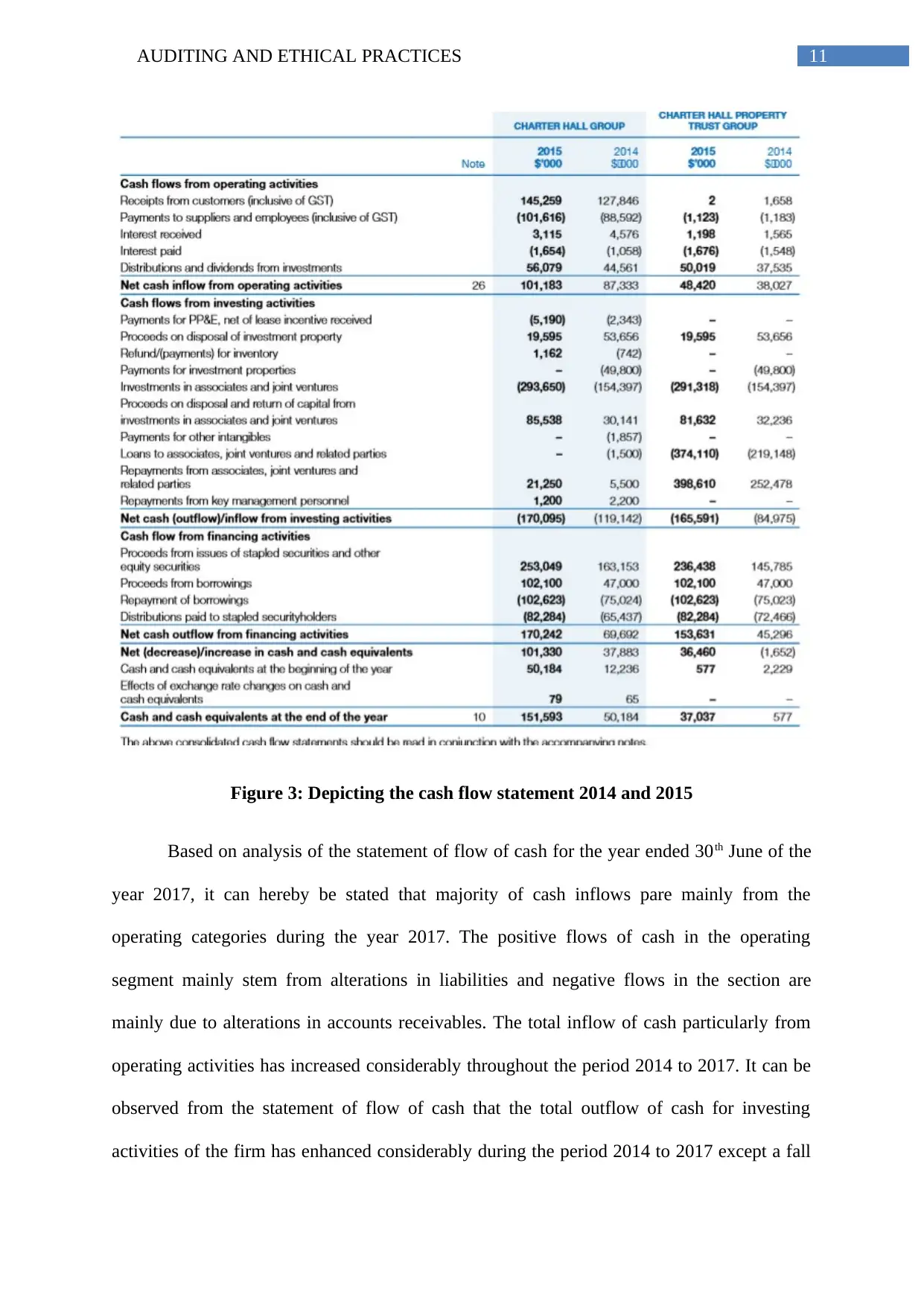

Figure 3: Depicting the cash flow statement 2014 and 2015

Based on analysis of the statement of flow of cash for the year ended 30th June of the

year 2017, it can hereby be stated that majority of cash inflows pare mainly from the

operating categories during the year 2017. The positive flows of cash in the operating

segment mainly stem from alterations in liabilities and negative flows in the section are

mainly due to alterations in accounts receivables. The total inflow of cash particularly from

operating activities has increased considerably throughout the period 2014 to 2017. It can be

observed from the statement of flow of cash that the total outflow of cash for investing

activities of the firm has enhanced considerably during the period 2014 to 2017 except a fall

Figure 3: Depicting the cash flow statement 2014 and 2015

Based on analysis of the statement of flow of cash for the year ended 30th June of the

year 2017, it can hereby be stated that majority of cash inflows pare mainly from the

operating categories during the year 2017. The positive flows of cash in the operating

segment mainly stem from alterations in liabilities and negative flows in the section are

mainly due to alterations in accounts receivables. The total inflow of cash particularly from

operating activities has increased considerably throughout the period 2014 to 2017. It can be

observed from the statement of flow of cash that the total outflow of cash for investing

activities of the firm has enhanced considerably during the period 2014 to 2017 except a fall

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.