Audit Risk Analysis of API: Internal Controls, Ratios, and Procedures

VerifiedAdded on 2023/03/20

|12

|4263

|52

Report

AI Summary

This report, prepared as a memorandum to Wayne Wiadrowski, analyzes the audit risks associated with Always Precise Instruments Pty Limited (API). It examines various financial ratios, including current ratio, return on equity, return on total assets, gross margin, marketing expenses, sales expenses, times interest earned, days in inventory, days in accounts receivable, and debt-to-equity ratio, comparing them to industry benchmarks and identifying potential misstatements. The report details audit procedures to address these risks, such as testing account balances, verifying capital, analyzing sales figures, and assessing inventory and debt management. Furthermore, it highlights internal control weaknesses related to the company's reliance on its system for purchase orders and inventory management, emphasizing the associated risks and recommending mitigation strategies. The analysis aims to provide a comprehensive understanding of API's financial health and guide the auditor in forming an informed opinion on the company's financial statements.

Running head: Auditing and Assurance

Auditing and Assurance

Name of the Student

Name of the University

Author Note

Auditing and Assurance

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Auditing and Assurance

Memorandum

To: Wayne Wiadrowski

From: Audit Manager

Date: 8th May, 2019

Subject: Analysis of the audit risk in the ratio and internal control of API.

Purpose of the Memo

The first responsibility of the auditor is to check whether the financial statement are showing

true and fair view or not. It is their duty to know to check all the details of the company and

also to give proper opinion of the company financial statements and to check whether there is

any fraud is going in the company or not. In the given case it can be seen that auditor of

Always Precise Instruments Pty Limited is performing the audit and using the financial ratio

as a base to judge the potential risks in the business and what are the audit process which can

be taken by them in the same. It also include the internal control weakness of the company

and also the sampling size which is been used by the auditor in regards with the audit process.

The different aspects of the company are been shown in the coming table which are listed

below:

Audit Risk and their Audit Procedures

Ratio Analysis Audit Risk Audit Procedure

Current

Ratio

The current ratio has

been increase as in

current year is 1.64

which is a very good

sign that the company

is able to make their

liquidity position

better in compare to

previous year

(Chambers and Odar

2015). It is because of

High amount in

current asset or low

value of current

liability

As the company current

ratio is been less than the

industry benchmark so it

can be because

misstatement in the

balance of the asset and

liability so the company

must have alter their

value so it can show a

decrease or increase in

the current ratio De

(Simone, Ege &

Stomberg 2014).

The procedure which

the auditor should carry

it should apply test of

control as it should

verify the account

balance of both current

asset and liabilities so

that it can know where

there is material

misstatements in the

company (DeFond &

Zhang 2014).

Quick

Ratio

As per the data given

this clearly show that

the company have

increase in the quick

ratio as in 2018 it is

0.91 which is good in

There can material

misstatement in the quick

ratio as it help the

company to get more

number of investors by

seeing the quick ratio

As the auditor should

perform test of control

method as it should

verify the changes

properly in regards with

quick asset and current

Auditing and Assurance

Memorandum

To: Wayne Wiadrowski

From: Audit Manager

Date: 8th May, 2019

Subject: Analysis of the audit risk in the ratio and internal control of API.

Purpose of the Memo

The first responsibility of the auditor is to check whether the financial statement are showing

true and fair view or not. It is their duty to know to check all the details of the company and

also to give proper opinion of the company financial statements and to check whether there is

any fraud is going in the company or not. In the given case it can be seen that auditor of

Always Precise Instruments Pty Limited is performing the audit and using the financial ratio

as a base to judge the potential risks in the business and what are the audit process which can

be taken by them in the same. It also include the internal control weakness of the company

and also the sampling size which is been used by the auditor in regards with the audit process.

The different aspects of the company are been shown in the coming table which are listed

below:

Audit Risk and their Audit Procedures

Ratio Analysis Audit Risk Audit Procedure

Current

Ratio

The current ratio has

been increase as in

current year is 1.64

which is a very good

sign that the company

is able to make their

liquidity position

better in compare to

previous year

(Chambers and Odar

2015). It is because of

High amount in

current asset or low

value of current

liability

As the company current

ratio is been less than the

industry benchmark so it

can be because

misstatement in the

balance of the asset and

liability so the company

must have alter their

value so it can show a

decrease or increase in

the current ratio De

(Simone, Ege &

Stomberg 2014).

The procedure which

the auditor should carry

it should apply test of

control as it should

verify the account

balance of both current

asset and liabilities so

that it can know where

there is material

misstatements in the

company (DeFond &

Zhang 2014).

Quick

Ratio

As per the data given

this clearly show that

the company have

increase in the quick

ratio as in 2018 it is

0.91 which is good in

There can material

misstatement in the quick

ratio as it help the

company to get more

number of investors by

seeing the quick ratio

As the auditor should

perform test of control

method as it should

verify the changes

properly in regards with

quick asset and current

2

Auditing and Assurance

compare to 2017 0.87

so it show company

has increase its cash

asset more so this is a

good symbol as they

can easily able to pay

their short term

liability easily and

effectively (Donelson,

Ege & McInnis 2016).

increase so the company

may have done alter the

value to show a good

ratio to the financial user

of the company

(Furnham & Gunter

2015).

liability so that it can

know the reason of the

increase in the current

ratio.

Return on

Equity

The return on equity

has been decreased in

the current year as in

2018 it is 14.7 but in

2017 it was 16.6 so it

show that the

company have

increase the capital

and due to these the

ratio have been

decrease in the current

year

As the ratio is also

decrease in compare to

the benchmark of the

industry so this signify

that there is a risk of

material misstatements as

showing low amount

return on equity help

them to reduce the profit

as it can be because they

have increase in the

capital so this ratio got

decrease in the current

year (Gay & Simnett

2012).

The auditor should do

the verification of the

capital and the rate

which is been used by

the company as it will

help them know how

the company is able to

increase the capital in

the company and the

reason behind of the

increase in the equity

capital (Gerakos &

Syverson 2015).

Return on

Total

Assets

The given data shows

that the company has

decrease in the return

on total asset as in

2018 it was 12.5 but

in 2017 it was 14.9 so

this show the

company is unable to

do the proper

utilization of the asset

and as a result it is

having a decrease in

the ratio.

As it is seen that the

company ratio is also

below the industry

benchmark so it is a risk

and as the management is

not able to do the fuller

utilization of the asset

and so it is the reason

that the ratio has been

decreased in the

company an directly

affect the earning of the

company (Griffiths

2016).

The auditor should do

in-depth analysis of the

company accounts and

the transaction related

to the asset so that it can

able to know the real

reason why the

company is unable to do

fuller utilization of the

assets (Hall 2015).

Gross

Margin

As per the data given

it can be clearly seen

there is a huge

decrease in the ratio in

the current year as in

2018 it is 6.5 but in

2017 it is 10.3 so this

There can be material

misstatement in the

company as the company

must have stated wrong

amount of sale so that it

can decrease the gross

profit of the company

Auditor should carry

test of control under this

situation as the sale

should be tested by the

auditor and also should

check the market

demand so that it can

Auditing and Assurance

compare to 2017 0.87

so it show company

has increase its cash

asset more so this is a

good symbol as they

can easily able to pay

their short term

liability easily and

effectively (Donelson,

Ege & McInnis 2016).

increase so the company

may have done alter the

value to show a good

ratio to the financial user

of the company

(Furnham & Gunter

2015).

liability so that it can

know the reason of the

increase in the current

ratio.

Return on

Equity

The return on equity

has been decreased in

the current year as in

2018 it is 14.7 but in

2017 it was 16.6 so it

show that the

company have

increase the capital

and due to these the

ratio have been

decrease in the current

year

As the ratio is also

decrease in compare to

the benchmark of the

industry so this signify

that there is a risk of

material misstatements as

showing low amount

return on equity help

them to reduce the profit

as it can be because they

have increase in the

capital so this ratio got

decrease in the current

year (Gay & Simnett

2012).

The auditor should do

the verification of the

capital and the rate

which is been used by

the company as it will

help them know how

the company is able to

increase the capital in

the company and the

reason behind of the

increase in the equity

capital (Gerakos &

Syverson 2015).

Return on

Total

Assets

The given data shows

that the company has

decrease in the return

on total asset as in

2018 it was 12.5 but

in 2017 it was 14.9 so

this show the

company is unable to

do the proper

utilization of the asset

and as a result it is

having a decrease in

the ratio.

As it is seen that the

company ratio is also

below the industry

benchmark so it is a risk

and as the management is

not able to do the fuller

utilization of the asset

and so it is the reason

that the ratio has been

decreased in the

company an directly

affect the earning of the

company (Griffiths

2016).

The auditor should do

in-depth analysis of the

company accounts and

the transaction related

to the asset so that it can

able to know the real

reason why the

company is unable to do

fuller utilization of the

assets (Hall 2015).

Gross

Margin

As per the data given

it can be clearly seen

there is a huge

decrease in the ratio in

the current year as in

2018 it is 6.5 but in

2017 it is 10.3 so this

There can be material

misstatement in the

company as the company

must have stated wrong

amount of sale so that it

can decrease the gross

profit of the company

Auditor should carry

test of control under this

situation as the sale

should be tested by the

auditor and also should

check the market

demand so that it can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Auditing and Assurance

show that the

company is unable to

get proper sale in the

current year and as a

result the ratio got

decrease. It is because

of low amount of sale

or high cost expenses.

and able to save amount

of tax from it

(He ,Zeadally & Wu

2018)

assume about the sale

amount which is there

in the financial

statement and can

conclude whether they

are any material

misstatement or not

Marketing

Expenses

There is high increase

in the marketing

expense of the

company as in 2018 it

is 4.4% but in 2017 it

is 3.8% so this is

increase and it will

directly affect the net

profit of the company.

As there is high amount

of marketing expenses is

there this signify that the

company must done

some material

misstatement in the

expenses it must have

overstated the expenses

as it is also increased in

compare to industry

benchmark so this show

company is able to get

high amount of the

expenses which not a

good sign in regards with

the net profit of the

company (King 2014).

The auditor should

carry test of control

methods as there is an

increase in the expenses

so the auditor should

verify the invoice and

also should check

whether the expenses

are done in some other

cases are not been

included in this

expenses.

Sales

Expenses

As per the data it is

clear that there is a

decrease in the ratio as

in 2018 it is 3.4% and

in 2017 it is 3.6% so

this the good sign that

the company is able to

control the expenses

and as a result it will

able to increase the

overall profit of the

company.

As the company expense

is even low compare to

the industry benchmark

so there can be a risk of

material misstatement in

the account and the

company may have

decrease the value of the

expenses so that it can

able to show an increase

in gross profit and can

misstated it to the

financial user of the

company (Knechel &

Salterio 2016).

Auditor should use test

of details method in this

scenario as it should

check the details of the

invoice of the sale so

that it can conclude

about the fairness of the

expenses and can check

the reason of material

misstatement.

Times

Interest

Earned

The data show that the

company have got a

decrease in the ratio as

in 2018 it is 3.6 but in

2017 it was 4.6 so this

show that the

As per the given scenario

it can be say that there is

material misstatement in

the ratio and as it help

the company to decrease

their borrowing cost and

Auditor should perform

different process in this

case as it should able to

check all the borrowing

details so that it can

know what are the

Auditing and Assurance

show that the

company is unable to

get proper sale in the

current year and as a

result the ratio got

decrease. It is because

of low amount of sale

or high cost expenses.

and able to save amount

of tax from it

(He ,Zeadally & Wu

2018)

assume about the sale

amount which is there

in the financial

statement and can

conclude whether they

are any material

misstatement or not

Marketing

Expenses

There is high increase

in the marketing

expense of the

company as in 2018 it

is 4.4% but in 2017 it

is 3.8% so this is

increase and it will

directly affect the net

profit of the company.

As there is high amount

of marketing expenses is

there this signify that the

company must done

some material

misstatement in the

expenses it must have

overstated the expenses

as it is also increased in

compare to industry

benchmark so this show

company is able to get

high amount of the

expenses which not a

good sign in regards with

the net profit of the

company (King 2014).

The auditor should

carry test of control

methods as there is an

increase in the expenses

so the auditor should

verify the invoice and

also should check

whether the expenses

are done in some other

cases are not been

included in this

expenses.

Sales

Expenses

As per the data it is

clear that there is a

decrease in the ratio as

in 2018 it is 3.4% and

in 2017 it is 3.6% so

this the good sign that

the company is able to

control the expenses

and as a result it will

able to increase the

overall profit of the

company.

As the company expense

is even low compare to

the industry benchmark

so there can be a risk of

material misstatement in

the account and the

company may have

decrease the value of the

expenses so that it can

able to show an increase

in gross profit and can

misstated it to the

financial user of the

company (Knechel &

Salterio 2016).

Auditor should use test

of details method in this

scenario as it should

check the details of the

invoice of the sale so

that it can conclude

about the fairness of the

expenses and can check

the reason of material

misstatement.

Times

Interest

Earned

The data show that the

company have got a

decrease in the ratio as

in 2018 it is 3.6 but in

2017 it was 4.6 so this

show that the

As per the given scenario

it can be say that there is

material misstatement in

the ratio and as it help

the company to decrease

their borrowing cost and

Auditor should perform

different process in this

case as it should able to

check all the borrowing

details so that it can

know what are the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Auditing and Assurance

company is unable to

get sufficient earning

and as a result of it the

company is unable to

make proper

repayment of the

borrowing done by

them.

also it directly affect the

earning capacity of the

company (Kumar &

Sharma 2015).

amount which is going

to be pay by the

company and the reason

why they are unable to

pay the required amount

in the current year.

Days in

Inventory

There is increase in

the day in the current

year as in 2018 it is

34.9 and in 2017 it is

32.9 so it is company

is increasing its

inventory stock so this

signify that the

company is able to

make the inventory

perform very well in

the business.

There can be material

misstatements in the

inventory as the company

may have increase the

cost of the inventory so

that it can able the gross

profit of the company (Li

et al., 2016).

Auditor should carry

test of control method

in this case as it will

help them to know what

are the reason of

increase in the

inventory and how the

company y manage to

such increase and it also

help them to know the

reason for material

misstatement in the

company.

Days in

Accounts

Receivable

There is an increase in

the account receivable

of the company which

indicate that the

company is giving

more time to the

debtors to pay back

the money as it help

them to increase the

sale by changing the

payment tenure of the

company.

There is misstatement in

the accounts as the

company may have

increase the sale but they

may have overstated the

account balance and as a

result the company have

done material

misstatement in the

financial statement of the

company (Lin et al.,

2014).

Auditor should check

test of control methods

as it should as it should

check the internal

control weakness of the

company as this will

help them to get an

overview of the

inventory system and

also it will help them to

know the reason of

material misstatements

in the accounts.

Debt to

Equity

Ratio

There is an increase in

the debt ratio of the

company so this

signify that the

company have got an

increase in the debt

and so as a result this

ratio has been

increased.

As it have got some

misstatements in the debt

so it can be risk in the

audit process so the

company may have over-

valued the long term

liability so that it can

show an increase in the

debt ratio of the company

and can able to influence

financial user to invest in

Auditor should access

the debt of the company

and should check all the

details regarding the

dent so that it can know

the reason of the

increase in the debt

amount also it help

them to know the

material misstatement

in the company.

Auditing and Assurance

company is unable to

get sufficient earning

and as a result of it the

company is unable to

make proper

repayment of the

borrowing done by

them.

also it directly affect the

earning capacity of the

company (Kumar &

Sharma 2015).

amount which is going

to be pay by the

company and the reason

why they are unable to

pay the required amount

in the current year.

Days in

Inventory

There is increase in

the day in the current

year as in 2018 it is

34.9 and in 2017 it is

32.9 so it is company

is increasing its

inventory stock so this

signify that the

company is able to

make the inventory

perform very well in

the business.

There can be material

misstatements in the

inventory as the company

may have increase the

cost of the inventory so

that it can able the gross

profit of the company (Li

et al., 2016).

Auditor should carry

test of control method

in this case as it will

help them to know what

are the reason of

increase in the

inventory and how the

company y manage to

such increase and it also

help them to know the

reason for material

misstatement in the

company.

Days in

Accounts

Receivable

There is an increase in

the account receivable

of the company which

indicate that the

company is giving

more time to the

debtors to pay back

the money as it help

them to increase the

sale by changing the

payment tenure of the

company.

There is misstatement in

the accounts as the

company may have

increase the sale but they

may have overstated the

account balance and as a

result the company have

done material

misstatement in the

financial statement of the

company (Lin et al.,

2014).

Auditor should check

test of control methods

as it should as it should

check the internal

control weakness of the

company as this will

help them to get an

overview of the

inventory system and

also it will help them to

know the reason of

material misstatements

in the accounts.

Debt to

Equity

Ratio

There is an increase in

the debt ratio of the

company so this

signify that the

company have got an

increase in the debt

and so as a result this

ratio has been

increased.

As it have got some

misstatements in the debt

so it can be risk in the

audit process so the

company may have over-

valued the long term

liability so that it can

show an increase in the

debt ratio of the company

and can able to influence

financial user to invest in

Auditor should access

the debt of the company

and should check all the

details regarding the

dent so that it can know

the reason of the

increase in the debt

amount also it help

them to know the

material misstatement

in the company.

5

Auditing and Assurance

the company (Newton et

al., 2015)

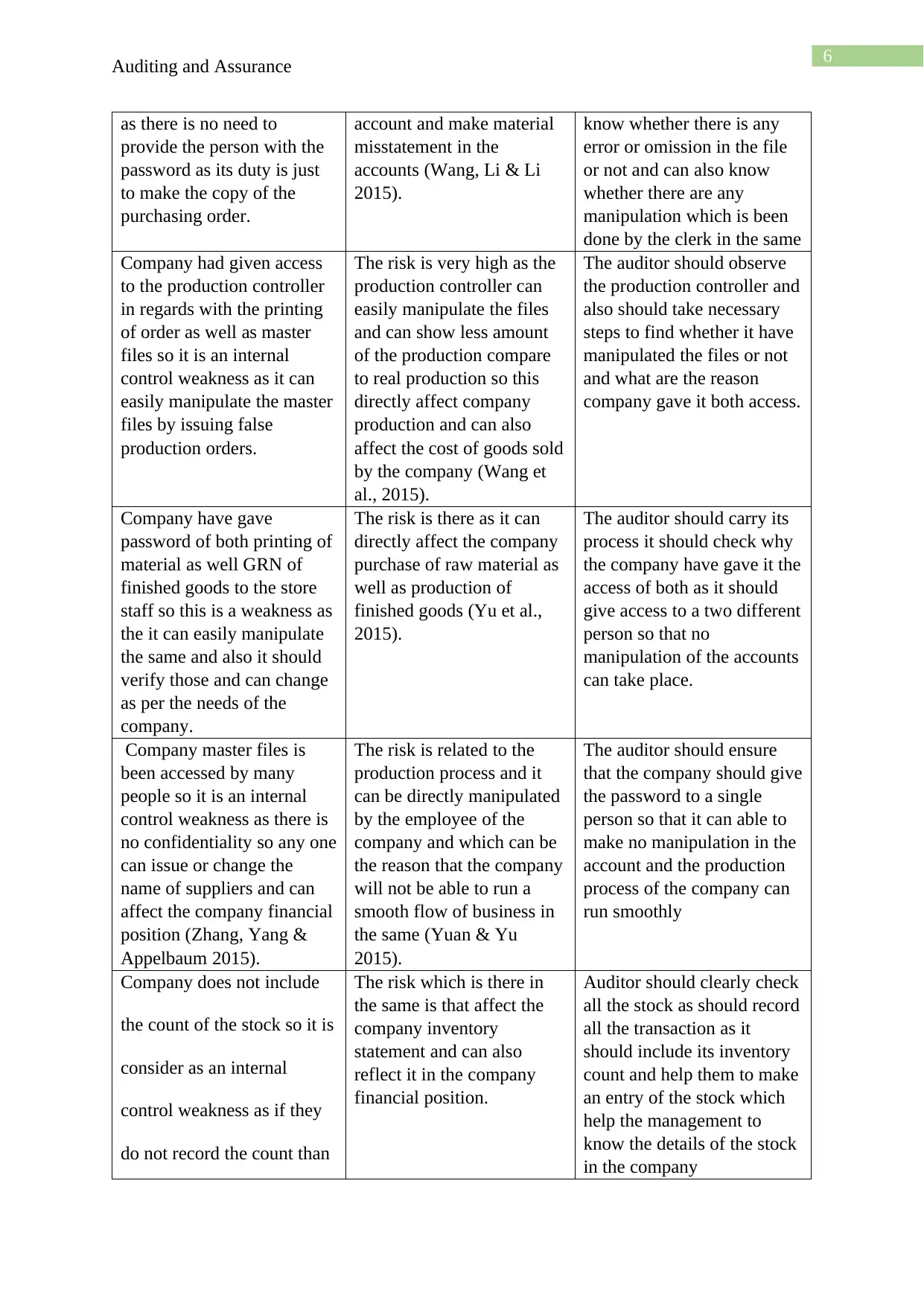

Inventory Internal Control Weakness and Risk associated with them

Internal Control Weakness Audit Risk Audit Procedure

The company is solely

depend upon the system in

regards with the generation

of the purchase order so is it

is a weakness, if there is any

problem in the system than it

will directly affect the

company and may dispute

may occur in the same

(Reeves, Culverwell &

Wittman 2017).

The audit risk in the given

case is that as the system

does not work properly so it

may happen the over or

under purchase order may

be generated and that can

affect the requirement of the

company and as a result it

will have to incur loss in

related to the same.

Testing of the internal

control should be the audit

process. As it should verify

the system properly so that it

can able to get them a good

amount of reason to trust the

system and also it should

able to make the error and

omission which happen due

to the internal control

weakness.

The company is totally

depend upon the system in

regards with the generation

of the purchase order so it is

consider as an weakness as

if the system is not working

properly than it can affect

the purchasing order of the

company (Sandvig et al,.

2014).

Audit risk in the present

case is that it can severely

affect the production

process as a result of it the

company may have to suffer

losses as it they are unable

to get details of the

production order so they not

able to do proper purchase

and as a result it will impact

on the business of the

company.

The risk associated in the

case is control risk so the

auditor should test the

system of the company and

also it should take necessary

steps so that the efficiency of

the system so that it can

know the amount of the error

which the company system

can make.

The system of company

automatically select the

suppliers as per the latest

update so it is consider as a

weakness as if the system

got some problem and

selected wrong supplier so it

will affect the company as

they may to pay high

amount of goods which they

could have got in low price.

This can directly affect the

relation of the raw material

and finished goods as if

they unable to get required

amount of the raw material

they will not able to make

any finished goods and it

will make a loss in the

business (Wang, Li & Li

2014).

The risk is associated with

the situation is control risk

and the auditor should able

to do substantive procedure

so that it can check the

system periodically and also

keep a record of its

efficiency so that it will

directly affect the company

and can know the reason of

material misstatements in the

account.

Company had given the

password of its master file to

the clerk so it is consider as

an internal control weakness

As it is not its responsibility

still it have given the

password so that it can

easily manipulate the

Auditor should carry test of

control method as it should

check all the details in the

master file so that it can

Auditing and Assurance

the company (Newton et

al., 2015)

Inventory Internal Control Weakness and Risk associated with them

Internal Control Weakness Audit Risk Audit Procedure

The company is solely

depend upon the system in

regards with the generation

of the purchase order so is it

is a weakness, if there is any

problem in the system than it

will directly affect the

company and may dispute

may occur in the same

(Reeves, Culverwell &

Wittman 2017).

The audit risk in the given

case is that as the system

does not work properly so it

may happen the over or

under purchase order may

be generated and that can

affect the requirement of the

company and as a result it

will have to incur loss in

related to the same.

Testing of the internal

control should be the audit

process. As it should verify

the system properly so that it

can able to get them a good

amount of reason to trust the

system and also it should

able to make the error and

omission which happen due

to the internal control

weakness.

The company is totally

depend upon the system in

regards with the generation

of the purchase order so it is

consider as an weakness as

if the system is not working

properly than it can affect

the purchasing order of the

company (Sandvig et al,.

2014).

Audit risk in the present

case is that it can severely

affect the production

process as a result of it the

company may have to suffer

losses as it they are unable

to get details of the

production order so they not

able to do proper purchase

and as a result it will impact

on the business of the

company.

The risk associated in the

case is control risk so the

auditor should test the

system of the company and

also it should take necessary

steps so that the efficiency of

the system so that it can

know the amount of the error

which the company system

can make.

The system of company

automatically select the

suppliers as per the latest

update so it is consider as a

weakness as if the system

got some problem and

selected wrong supplier so it

will affect the company as

they may to pay high

amount of goods which they

could have got in low price.

This can directly affect the

relation of the raw material

and finished goods as if

they unable to get required

amount of the raw material

they will not able to make

any finished goods and it

will make a loss in the

business (Wang, Li & Li

2014).

The risk is associated with

the situation is control risk

and the auditor should able

to do substantive procedure

so that it can check the

system periodically and also

keep a record of its

efficiency so that it will

directly affect the company

and can know the reason of

material misstatements in the

account.

Company had given the

password of its master file to

the clerk so it is consider as

an internal control weakness

As it is not its responsibility

still it have given the

password so that it can

easily manipulate the

Auditor should carry test of

control method as it should

check all the details in the

master file so that it can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Auditing and Assurance

as there is no need to

provide the person with the

password as its duty is just

to make the copy of the

purchasing order.

account and make material

misstatement in the

accounts (Wang, Li & Li

2015).

know whether there is any

error or omission in the file

or not and can also know

whether there are any

manipulation which is been

done by the clerk in the same

Company had given access

to the production controller

in regards with the printing

of order as well as master

files so it is an internal

control weakness as it can

easily manipulate the master

files by issuing false

production orders.

The risk is very high as the

production controller can

easily manipulate the files

and can show less amount

of the production compare

to real production so this

directly affect company

production and can also

affect the cost of goods sold

by the company (Wang et

al., 2015).

The auditor should observe

the production controller and

also should take necessary

steps to find whether it have

manipulated the files or not

and what are the reason

company gave it both access.

Company have gave

password of both printing of

material as well GRN of

finished goods to the store

staff so this is a weakness as

the it can easily manipulate

the same and also it should

verify those and can change

as per the needs of the

company.

The risk is there as it can

directly affect the company

purchase of raw material as

well as production of

finished goods (Yu et al.,

2015).

The auditor should carry its

process it should check why

the company have gave it the

access of both as it should

give access to a two different

person so that no

manipulation of the accounts

can take place.

Company master files is

been accessed by many

people so it is an internal

control weakness as there is

no confidentiality so any one

can issue or change the

name of suppliers and can

affect the company financial

position (Zhang, Yang &

Appelbaum 2015).

The risk is related to the

production process and it

can be directly manipulated

by the employee of the

company and which can be

the reason that the company

will not be able to run a

smooth flow of business in

the same (Yuan & Yu

2015).

The auditor should ensure

that the company should give

the password to a single

person so that it can able to

make no manipulation in the

account and the production

process of the company can

run smoothly

Company does not include

the count of the stock so it is

consider as an internal

control weakness as if they

do not record the count than

The risk which is there in

the same is that affect the

company inventory

statement and can also

reflect it in the company

financial position.

Auditor should clearly check

all the stock as should record

all the transaction as it

should include its inventory

count and help them to make

an entry of the stock which

help the management to

know the details of the stock

in the company

Auditing and Assurance

as there is no need to

provide the person with the

password as its duty is just

to make the copy of the

purchasing order.

account and make material

misstatement in the

accounts (Wang, Li & Li

2015).

know whether there is any

error or omission in the file

or not and can also know

whether there are any

manipulation which is been

done by the clerk in the same

Company had given access

to the production controller

in regards with the printing

of order as well as master

files so it is an internal

control weakness as it can

easily manipulate the master

files by issuing false

production orders.

The risk is very high as the

production controller can

easily manipulate the files

and can show less amount

of the production compare

to real production so this

directly affect company

production and can also

affect the cost of goods sold

by the company (Wang et

al., 2015).

The auditor should observe

the production controller and

also should take necessary

steps to find whether it have

manipulated the files or not

and what are the reason

company gave it both access.

Company have gave

password of both printing of

material as well GRN of

finished goods to the store

staff so this is a weakness as

the it can easily manipulate

the same and also it should

verify those and can change

as per the needs of the

company.

The risk is there as it can

directly affect the company

purchase of raw material as

well as production of

finished goods (Yu et al.,

2015).

The auditor should carry its

process it should check why

the company have gave it the

access of both as it should

give access to a two different

person so that no

manipulation of the accounts

can take place.

Company master files is

been accessed by many

people so it is an internal

control weakness as there is

no confidentiality so any one

can issue or change the

name of suppliers and can

affect the company financial

position (Zhang, Yang &

Appelbaum 2015).

The risk is related to the

production process and it

can be directly manipulated

by the employee of the

company and which can be

the reason that the company

will not be able to run a

smooth flow of business in

the same (Yuan & Yu

2015).

The auditor should ensure

that the company should give

the password to a single

person so that it can able to

make no manipulation in the

account and the production

process of the company can

run smoothly

Company does not include

the count of the stock so it is

consider as an internal

control weakness as if they

do not record the count than

The risk which is there in

the same is that affect the

company inventory

statement and can also

reflect it in the company

financial position.

Auditor should clearly check

all the stock as should record

all the transaction as it

should include its inventory

count and help them to make

an entry of the stock which

help the management to

know the details of the stock

in the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Auditing and Assurance

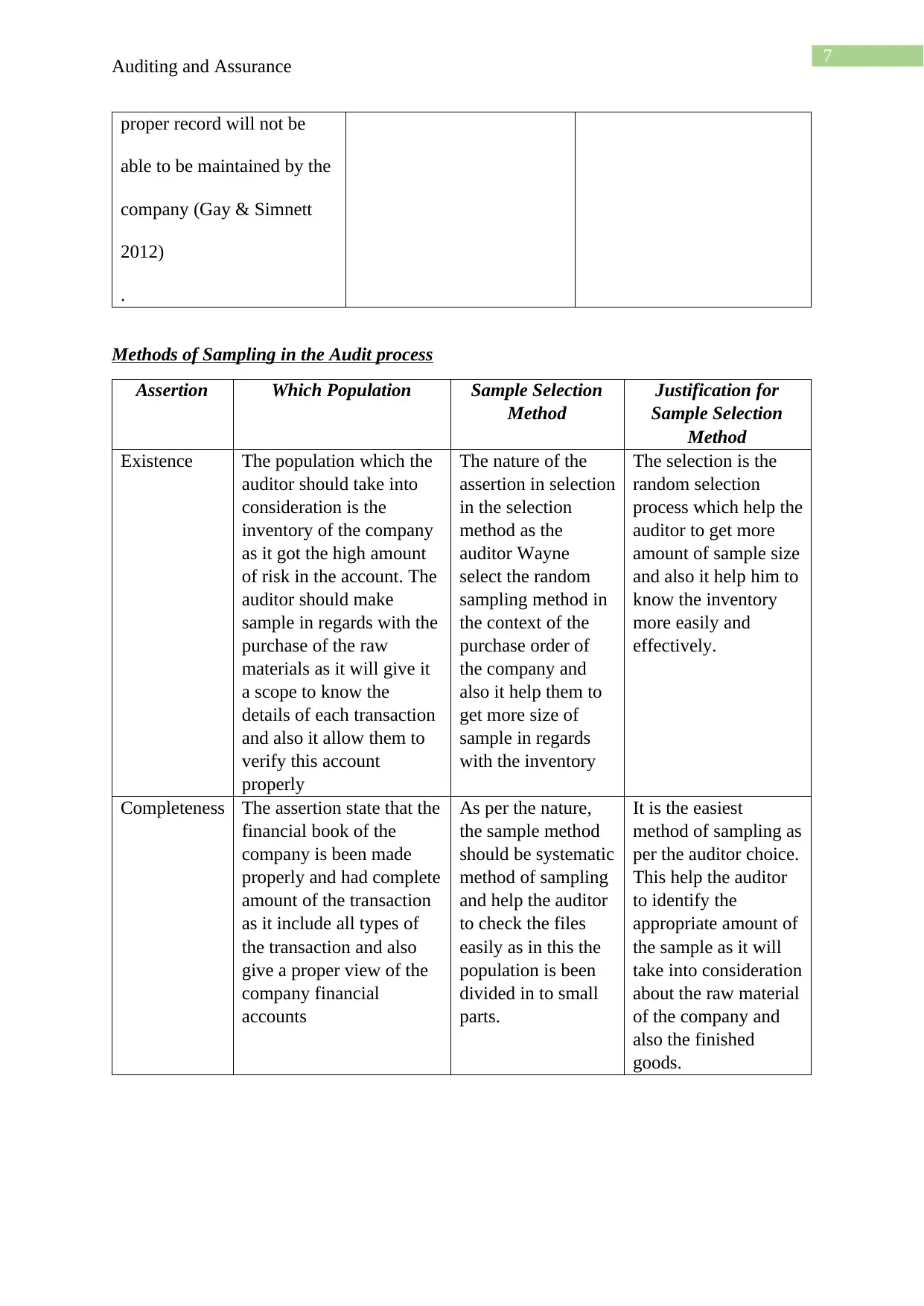

proper record will not be

able to be maintained by the

company (Gay & Simnett

2012)

.

Methods of Sampling in the Audit process

Assertion Which Population Sample Selection

Method

Justification for

Sample Selection

Method

Existence The population which the

auditor should take into

consideration is the

inventory of the company

as it got the high amount

of risk in the account. The

auditor should make

sample in regards with the

purchase of the raw

materials as it will give it

a scope to know the

details of each transaction

and also it allow them to

verify this account

properly

The nature of the

assertion in selection

in the selection

method as the

auditor Wayne

select the random

sampling method in

the context of the

purchase order of

the company and

also it help them to

get more size of

sample in regards

with the inventory

The selection is the

random selection

process which help the

auditor to get more

amount of sample size

and also it help him to

know the inventory

more easily and

effectively.

Completeness The assertion state that the

financial book of the

company is been made

properly and had complete

amount of the transaction

as it include all types of

the transaction and also

give a proper view of the

company financial

accounts

As per the nature,

the sample method

should be systematic

method of sampling

and help the auditor

to check the files

easily as in this the

population is been

divided in to small

parts.

It is the easiest

method of sampling as

per the auditor choice.

This help the auditor

to identify the

appropriate amount of

the sample as it will

take into consideration

about the raw material

of the company and

also the finished

goods.

Auditing and Assurance

proper record will not be

able to be maintained by the

company (Gay & Simnett

2012)

.

Methods of Sampling in the Audit process

Assertion Which Population Sample Selection

Method

Justification for

Sample Selection

Method

Existence The population which the

auditor should take into

consideration is the

inventory of the company

as it got the high amount

of risk in the account. The

auditor should make

sample in regards with the

purchase of the raw

materials as it will give it

a scope to know the

details of each transaction

and also it allow them to

verify this account

properly

The nature of the

assertion in selection

in the selection

method as the

auditor Wayne

select the random

sampling method in

the context of the

purchase order of

the company and

also it help them to

get more size of

sample in regards

with the inventory

The selection is the

random selection

process which help the

auditor to get more

amount of sample size

and also it help him to

know the inventory

more easily and

effectively.

Completeness The assertion state that the

financial book of the

company is been made

properly and had complete

amount of the transaction

as it include all types of

the transaction and also

give a proper view of the

company financial

accounts

As per the nature,

the sample method

should be systematic

method of sampling

and help the auditor

to check the files

easily as in this the

population is been

divided in to small

parts.

It is the easiest

method of sampling as

per the auditor choice.

This help the auditor

to identify the

appropriate amount of

the sample as it will

take into consideration

about the raw material

of the company and

also the finished

goods.

8

Auditing and Assurance

Reference

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), 45-69.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Gay, G., & Simnett, R. (2012). Auditing and assurance services in Australia. McGraw-Hill

Education Australia.

Gerakos, J., & Syverson, C. (2015). Competition in the audit market: Policy implications. Journal of

Accounting Research, 53(4), 725-775.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

He, D., Zeadally, S., & Wu, L. (2018). Certificateless public auditing scheme for cloud-

assisted wireless body area networks. IEEE Systems Journal, 12(1), 64-73.

King, N. (2014). U.S. Patent No. 8,712,813. Washington, DC: U.S. Patent and Trademark

Office.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Auditing and Assurance

Reference

Chambers, A.D. and Odar, M., 2015. A new vision for internal audit. Managerial Auditing

Journal, 30(1), pp.34-55.

De Simone, L., Ege, M. S., & Stomberg, B. (2014). Internal control quality: The role of

auditor-provided tax services. The Accounting Review, 90(4), 1469-1496.

DeFond, M., & Zhang, J. (2014). A review of archival auditing research. Journal of

Accounting and Economics, 58(2-3), 275-326.

Donelson, D. C., Ege, M. S., & McInnis, J. M. (2016). Internal control weaknesses and

financial reporting fraud. Auditing: A Journal of Practice & Theory, 36(3), 45-69.

Furnham, A., & Gunter, B. (2015). Corporate Assessment (Routledge Revivals): Auditing a

Company's Personality. Routledge.

Gay, G., & Simnett, R. (2012). Auditing and assurance services in Australia. McGraw-Hill

Education Australia.

Gerakos, J., & Syverson, C. (2015). Competition in the audit market: Policy implications. Journal of

Accounting Research, 53(4), 725-775.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Hall, J. A. (2015). Information technology auditing. Cengage Learning.

He, D., Zeadally, S., & Wu, L. (2018). Certificateless public auditing scheme for cloud-

assisted wireless body area networks. IEEE Systems Journal, 12(1), 64-73.

King, N. (2014). U.S. Patent No. 8,712,813. Washington, DC: U.S. Patent and Trademark

Office.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Auditing and Assurance

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Li, J., Li, J., Xie, D., & Cai, Z. (2016). Secure auditing and deduplicating data in cloud. IEEE

Transactions on Computers, 65(8), 2386-2396.

Lin, Y. C., Wang, Y. C., Chiou, J. R., & Huang, H. W. (2014). CEO characteristics and

internal control quality. Corporate Governance: An International Review, 22(1), 24-

42.

Newton, N. J., Persellin, J. S., Wang, D., & Wilkins, M. S. (2015). Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), 603-623.

Reeves, A., Culverwell, J., & Wittman, A. (2017). U.S. Patent No. 9,734,139. Washington,

DC: U.S. Patent and Trademark Office.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Wang, B., Li, B., & Li, H. (2014). Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), 43-56.

Wang, B., Li, B., & Li, H. (2015). Panda: Public auditing for shared data with efficient user

revocation in the cloud. IEEE Transactions on services computing, 8(1), 92-106.

Wang, J., Chen, X., Huang, X., You, I., & Xiang, Y. (2015). Verifiable auditing for

outsourced database in cloud computing. IEEE transactions on computers, 64(11),

3293-3303.

Yu, J., Ren, K., Wang, C., & Varadharajan, V. (2015). Enabling cloud storage auditing with

key-exposure resistance. IEEE Transactions on Information forensics and

security, 10(6), 1167-1179.

Auditing and Assurance

Kumar, R., & Sharma, V. (2015). Auditing: Principles and practice. PHI Learning Pvt. Ltd..

Li, J., Li, J., Xie, D., & Cai, Z. (2016). Secure auditing and deduplicating data in cloud. IEEE

Transactions on Computers, 65(8), 2386-2396.

Lin, Y. C., Wang, Y. C., Chiou, J. R., & Huang, H. W. (2014). CEO characteristics and

internal control quality. Corporate Governance: An International Review, 22(1), 24-

42.

Newton, N. J., Persellin, J. S., Wang, D., & Wilkins, M. S. (2015). Internal control opinion

shopping and audit market competition. The Accounting Review, 91(2), 603-623.

Reeves, A., Culverwell, J., & Wittman, A. (2017). U.S. Patent No. 9,734,139. Washington,

DC: U.S. Patent and Trademark Office.

Sandvig, C., Hamilton, K., Karahalios, K., & Langbort, C. (2014). Auditing algorithms:

Research methods for detecting discrimination on internet platforms. Data and

discrimination: converting critical concerns into productive inquiry, 22.

Wang, B., Li, B., & Li, H. (2014). Oruta: Privacy-preserving public auditing for shared data

in the cloud. IEEE transactions on cloud computing, 2(1), 43-56.

Wang, B., Li, B., & Li, H. (2015). Panda: Public auditing for shared data with efficient user

revocation in the cloud. IEEE Transactions on services computing, 8(1), 92-106.

Wang, J., Chen, X., Huang, X., You, I., & Xiang, Y. (2015). Verifiable auditing for

outsourced database in cloud computing. IEEE transactions on computers, 64(11),

3293-3303.

Yu, J., Ren, K., Wang, C., & Varadharajan, V. (2015). Enabling cloud storage auditing with

key-exposure resistance. IEEE Transactions on Information forensics and

security, 10(6), 1167-1179.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Auditing and Assurance

Yuan, J., & Yu, S. (2015). Public integrity auditing for dynamic data sharing with multiuser

modification. IEEE Transactions on Information Forensics and Security, 10(8), 1717-

1726.

Zhang, J., Yang, X., & Appelbaum, D. (2015). Toward effective Big Data analysis in

continuous auditing. Accounting Horizons, 29(2), 469-476.

Auditing and Assurance

Yuan, J., & Yu, S. (2015). Public integrity auditing for dynamic data sharing with multiuser

modification. IEEE Transactions on Information Forensics and Security, 10(8), 1717-

1726.

Zhang, J., Yang, X., & Appelbaum, D. (2015). Toward effective Big Data analysis in

continuous auditing. Accounting Horizons, 29(2), 469-476.

11

Auditing and Assurance

Auditing and Assurance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.