Auditing of Arena Reit: Risk Assessment and Audit Procedures

VerifiedAdded on 2023/06/07

|22

|4271

|66

Report

AI Summary

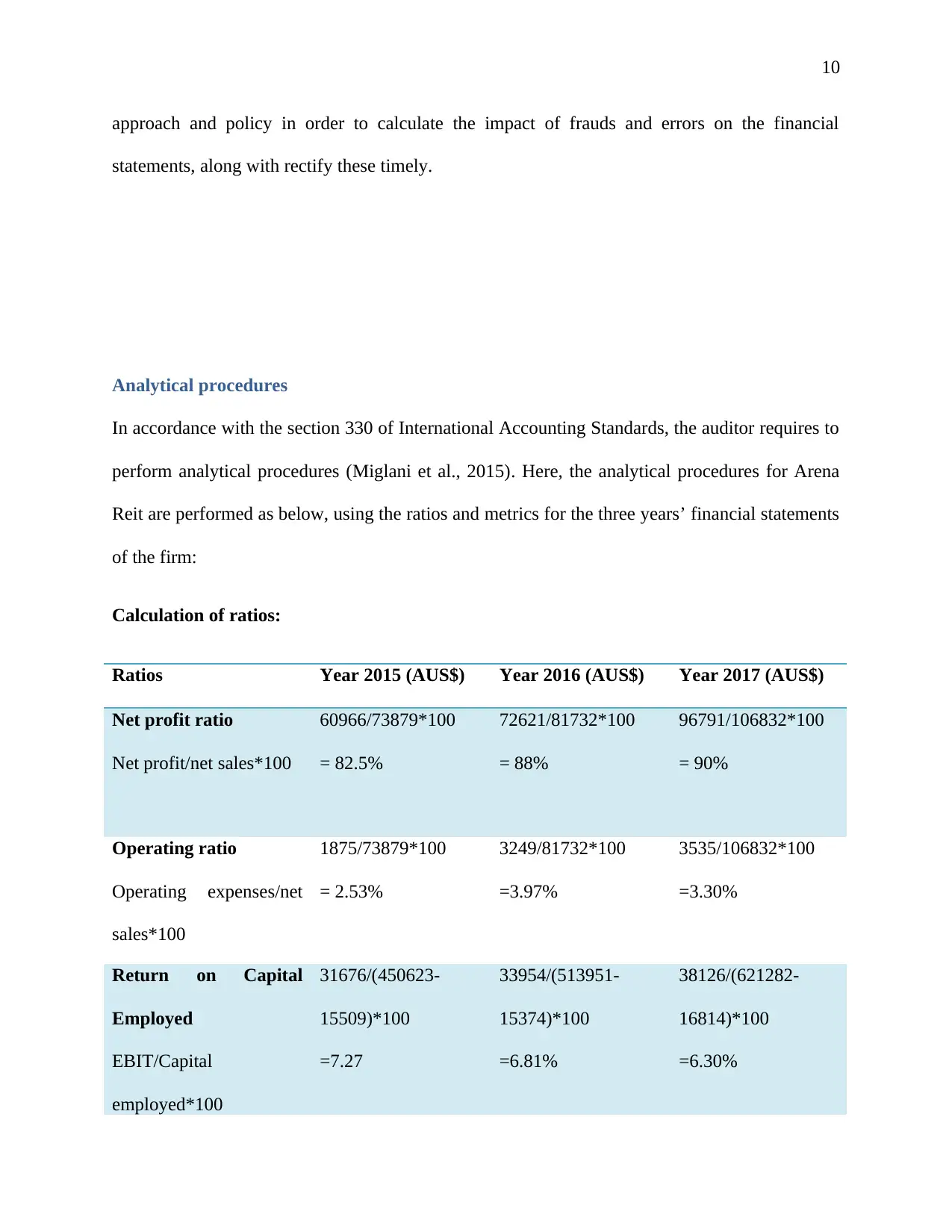

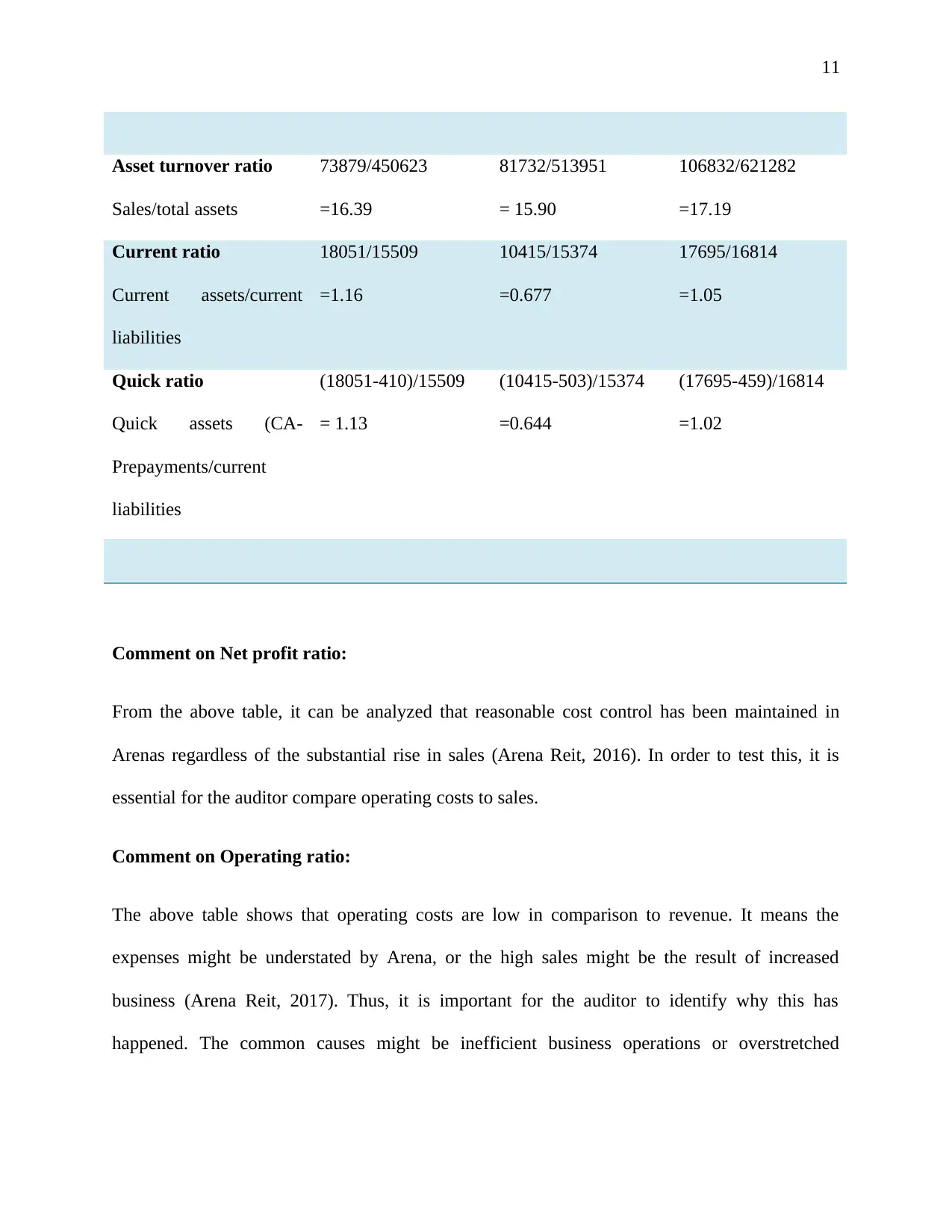

This report presents an audit of Arena Reit, a real estate company in Australia. It begins with an executive summary and introduction, followed by an analysis of key business risks, categorized into development, financial policy, operational, location, and appearance risks. The report then applies the audit risk model to assess inherent, control, and detection risks, determining a detection risk of 0.10. Analytical procedures are performed using financial ratios over three years, including net profit, operating, capital employed, asset turnover, current, and quick ratios, with commentary on each. The report details audit work steps using a substantive approach and includes a sampling plan. The conclusion summarizes the findings, highlighting Arena Reit's compliance with relevant guidelines and areas for improvement. Key business risks include operational, external, and regulatory factors, and the audit emphasizes the importance of understanding these risks for effective financial statement analysis. The report uses the International Accounting Standard (ISA) 315 guidelines to evaluate risk and includes calculations to determine detection risk. The report is a comprehensive audit of Arena Reit.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.