Auditing Theory & Practice: Analysis of ASA 315 and Auditor Liability

VerifiedAdded on 2023/06/08

|15

|3260

|249

Report

AI Summary

This report evaluates the case of Miller Yates Howarth (MYH), focusing on auditor responsibilities under ASA 315 concerning client governance, ethical issues using the American Accounting Association Decision Model, and the impact of auditor inclusion and statutory caps on liability. It identifies issues such as unclear top management responsibility, ineffective executive committees, and ethical violations by employees. Recommendations include improved governance processes, stronger internal controls, and ethical training. The report concludes that addressing these issues can mitigate audit risk and enhance the integrity of financial reporting. Desklib provides access to similar solved assignments and past papers for students.

Running head: AUDITING THEORY AND PRACTICE

Auditing Theory and Practice

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing Theory and Practice

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING THEORY AND PRACTICE

Executive Summary:

The report has identified various aspects related to ASA 315, American Accounting

Association Model and liability of the auditors. The unclear responsibility from the top

management of CAB, ineffective executive committee and others have been identified as the

significant issues in accordance with ASA 315 for which appropriate recommendations have

been provided to overcome the situation. In the second situation, it has been assessed that John

has not attended his office by giving a fake reason, which has violated the ethical principle

mentioned under the American Accounting Association Model. This mandates the need for

David Little, the senior employee of the organisation, to inform the same to the other team

members for maintaining ethical integrity. Finally, it has been evaluated that the inclusion of

auditors as well as statutory cap would help in minimising the liability of the auditors.

Executive Summary:

The report has identified various aspects related to ASA 315, American Accounting

Association Model and liability of the auditors. The unclear responsibility from the top

management of CAB, ineffective executive committee and others have been identified as the

significant issues in accordance with ASA 315 for which appropriate recommendations have

been provided to overcome the situation. In the second situation, it has been assessed that John

has not attended his office by giving a fake reason, which has violated the ethical principle

mentioned under the American Accounting Association Model. This mandates the need for

David Little, the senior employee of the organisation, to inform the same to the other team

members for maintaining ethical integrity. Finally, it has been evaluated that the inclusion of

auditors as well as statutory cap would help in minimising the liability of the auditors.

2AUDITING THEORY AND PRACTICE

Table of Contents

Introduction:....................................................................................................................................3

Answer to Question 1:.....................................................................................................................3

Answer to Question 2:.....................................................................................................................8

Answer to Question 3:...................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

Table of Contents

Introduction:....................................................................................................................................3

Answer to Question 1:.....................................................................................................................3

Answer to Question 2:.....................................................................................................................8

Answer to Question 3:...................................................................................................................10

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING THEORY AND PRACTICE

Introduction:

The current report aims to evaluate the case information of Miller Yates Howarth

(MYH), which is an accounting organisation having branches in New South Wales and

Queensland. The first segment of the report would focus on summarising the responsibility of the

auditor for reviewing the governance of the audit client by taking into consideration the standard

called ASA 315. The second segment would highlight the ethical issues by using the American

Accounting Association Decision Model in relation to the provided auditing work. Finally, the

report would shed light on explanation of the role that inclusion of auditors and statutory cap on

the liability of the auditors have on the drawbacks on the liabilities of the auditors.

Answer to Question 1:

When the audit functions of the organisations are conducted, it is necessary for the

auditors to govern various client-related aspects. In this context, the standard that contains

special attention is “ASA 315 Understanding the Entity and Its Environment and Assessing the

Risks of Material Misstatement”. This includes all accountabilities of the auditors in order to

review the client governance.

In accordance with ASA 315, the auditors are obliged to gain fair overview of the

industries of their clients, regulatory authorities in relation to the clients, framework for financial

reporting as well as other external factors (Auasb.gov.au, 2018). Along with this, the auditors are

liable to collect information about the operations, ownership structure, governance structure,

financial sources of the clients. Furthermore, they need to accumulate information for gaining an

Introduction:

The current report aims to evaluate the case information of Miller Yates Howarth

(MYH), which is an accounting organisation having branches in New South Wales and

Queensland. The first segment of the report would focus on summarising the responsibility of the

auditor for reviewing the governance of the audit client by taking into consideration the standard

called ASA 315. The second segment would highlight the ethical issues by using the American

Accounting Association Decision Model in relation to the provided auditing work. Finally, the

report would shed light on explanation of the role that inclusion of auditors and statutory cap on

the liability of the auditors have on the drawbacks on the liabilities of the auditors.

Answer to Question 1:

When the audit functions of the organisations are conducted, it is necessary for the

auditors to govern various client-related aspects. In this context, the standard that contains

special attention is “ASA 315 Understanding the Entity and Its Environment and Assessing the

Risks of Material Misstatement”. This includes all accountabilities of the auditors in order to

review the client governance.

In accordance with ASA 315, the auditors are obliged to gain fair overview of the

industries of their clients, regulatory authorities in relation to the clients, framework for financial

reporting as well as other external factors (Auasb.gov.au, 2018). Along with this, the auditors are

liable to collect information about the operations, ownership structure, governance structure,

financial sources of the clients. Furthermore, they need to accumulate information for gaining an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING THEORY AND PRACTICE

insight of the application and selection of accounting estimates, causes for change and

understanding the suitability for the selected organisations (Wang & Fargher, 2017).

More precisely, the auditors need to be obliged to understand the enforced internal client

control, since the auditors are required to judge whether the internal control is relevant for the

audit risk. At the time to obtain fair overview of internal control, the auditors should take into

account internal control design. Besides, ASA 315 mandates the need for the auditors to gain a

thorough insight regarding the different components of the control environment related to the

audit clients (Contessotto & Moroney, 2014). Hence, all individuals need to be analysed having

roles in the governance process of the organisation and it is a part of the auditors’ responsibility.

Such analysis would assist the auditors in gaining an understanding of the fact whether a culture

of honesty coupled with ethical behaviour exists in the business organisations.

ASA 315 states that it is the duty of the auditors to gain insight regarding the fact whether

the clients possess the needed processes in order to identify the financial reporting risks

(Bagshaw & Selwood, 2014). These risks need to be estimated and they are to be evaluated,

which is a significant duty of the auditors. After conducting such evaluation, they formulate the

necessary strategies for auditing. According to ASA 315, the auditors are responsible to gain

overview of the internal information system of their audit clients and the importance of such

system with financing reporting system of the clients. Henceforth, it is clearly understood that it

is the responsibility of the auditors to review the crucial aspects associated with client

governance for complying with ASA 315.

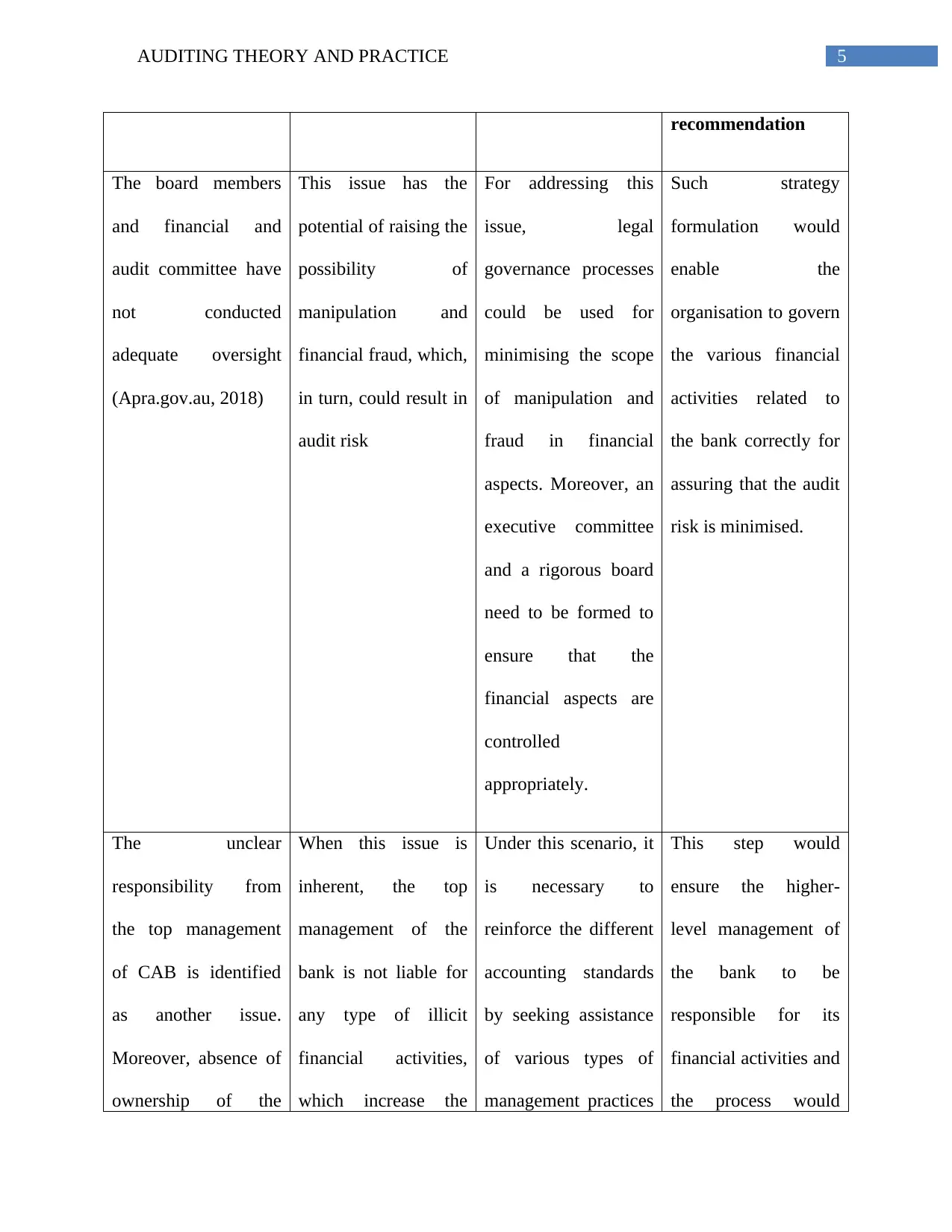

Issue Impact on raising

audit risk

Recommendations Reduction in audit

risk because of the

insight of the application and selection of accounting estimates, causes for change and

understanding the suitability for the selected organisations (Wang & Fargher, 2017).

More precisely, the auditors need to be obliged to understand the enforced internal client

control, since the auditors are required to judge whether the internal control is relevant for the

audit risk. At the time to obtain fair overview of internal control, the auditors should take into

account internal control design. Besides, ASA 315 mandates the need for the auditors to gain a

thorough insight regarding the different components of the control environment related to the

audit clients (Contessotto & Moroney, 2014). Hence, all individuals need to be analysed having

roles in the governance process of the organisation and it is a part of the auditors’ responsibility.

Such analysis would assist the auditors in gaining an understanding of the fact whether a culture

of honesty coupled with ethical behaviour exists in the business organisations.

ASA 315 states that it is the duty of the auditors to gain insight regarding the fact whether

the clients possess the needed processes in order to identify the financial reporting risks

(Bagshaw & Selwood, 2014). These risks need to be estimated and they are to be evaluated,

which is a significant duty of the auditors. After conducting such evaluation, they formulate the

necessary strategies for auditing. According to ASA 315, the auditors are responsible to gain

overview of the internal information system of their audit clients and the importance of such

system with financing reporting system of the clients. Henceforth, it is clearly understood that it

is the responsibility of the auditors to review the crucial aspects associated with client

governance for complying with ASA 315.

Issue Impact on raising

audit risk

Recommendations Reduction in audit

risk because of the

5AUDITING THEORY AND PRACTICE

recommendation

The board members

and financial and

audit committee have

not conducted

adequate oversight

(Apra.gov.au, 2018)

This issue has the

potential of raising the

possibility of

manipulation and

financial fraud, which,

in turn, could result in

audit risk

For addressing this

issue, legal

governance processes

could be used for

minimising the scope

of manipulation and

fraud in financial

aspects. Moreover, an

executive committee

and a rigorous board

need to be formed to

ensure that the

financial aspects are

controlled

appropriately.

Such strategy

formulation would

enable the

organisation to govern

the various financial

activities related to

the bank correctly for

assuring that the audit

risk is minimised.

The unclear

responsibility from

the top management

of CAB is identified

as another issue.

Moreover, absence of

ownership of the

When this issue is

inherent, the top

management of the

bank is not liable for

any type of illicit

financial activities,

which increase the

Under this scenario, it

is necessary to

reinforce the different

accounting standards

by seeking assistance

of various types of

management practices

This step would

ensure the higher-

level management of

the bank to be

responsible for its

financial activities and

the process would

recommendation

The board members

and financial and

audit committee have

not conducted

adequate oversight

(Apra.gov.au, 2018)

This issue has the

potential of raising the

possibility of

manipulation and

financial fraud, which,

in turn, could result in

audit risk

For addressing this

issue, legal

governance processes

could be used for

minimising the scope

of manipulation and

fraud in financial

aspects. Moreover, an

executive committee

and a rigorous board

need to be formed to

ensure that the

financial aspects are

controlled

appropriately.

Such strategy

formulation would

enable the

organisation to govern

the various financial

activities related to

the bank correctly for

assuring that the audit

risk is minimised.

The unclear

responsibility from

the top management

of CAB is identified

as another issue.

Moreover, absence of

ownership of the

When this issue is

inherent, the top

management of the

bank is not liable for

any type of illicit

financial activities,

which increase the

Under this scenario, it

is necessary to

reinforce the different

accounting standards

by seeking assistance

of various types of

management practices

This step would

ensure the higher-

level management of

the bank to be

responsible for its

financial activities and

the process would

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING THEORY AND PRACTICE

significant risks could

arise from the end of

the executive

committee.

audit risk. (Louwers et al.,

2015).

contribute to fall in

the audit risk of the

bank.

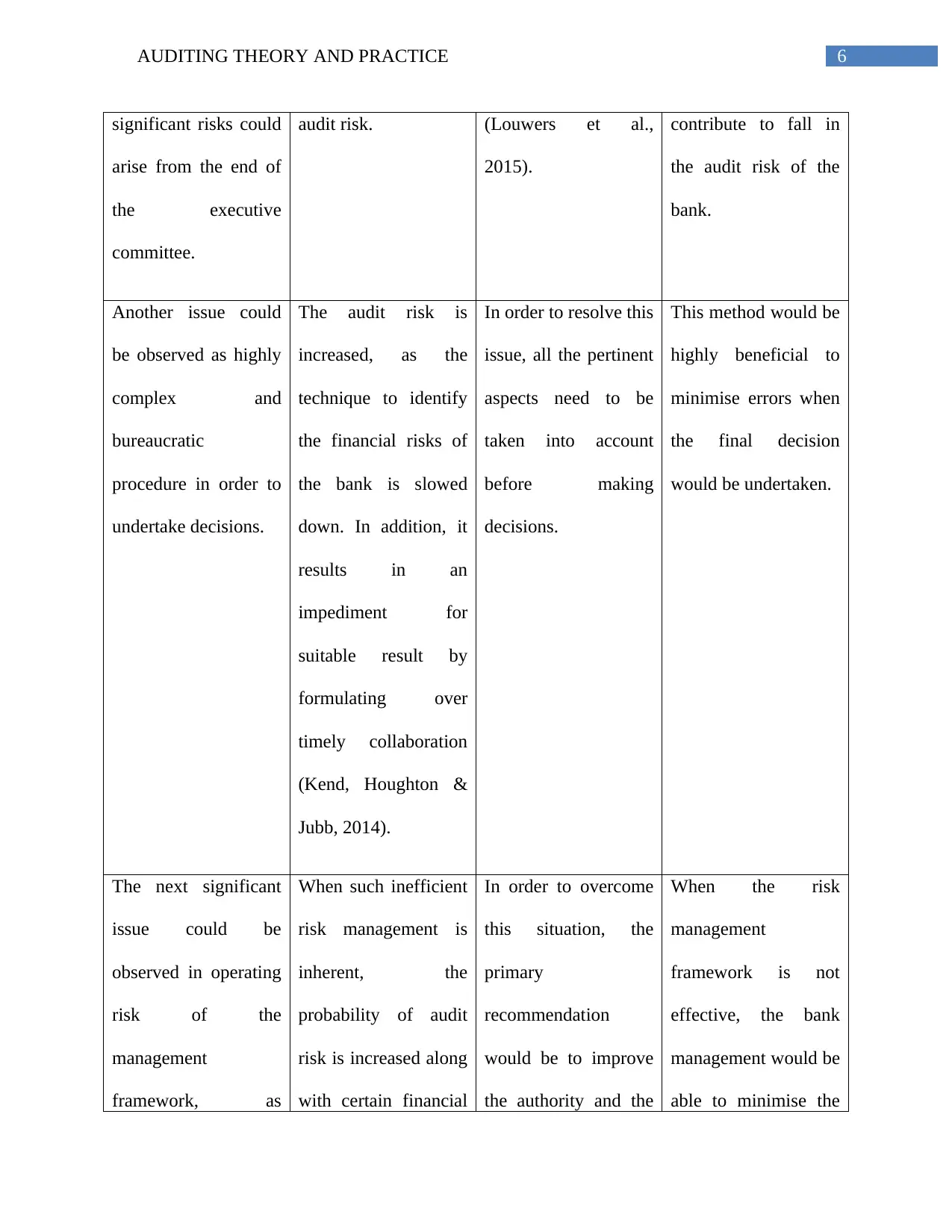

Another issue could

be observed as highly

complex and

bureaucratic

procedure in order to

undertake decisions.

The audit risk is

increased, as the

technique to identify

the financial risks of

the bank is slowed

down. In addition, it

results in an

impediment for

suitable result by

formulating over

timely collaboration

(Kend, Houghton &

Jubb, 2014).

In order to resolve this

issue, all the pertinent

aspects need to be

taken into account

before making

decisions.

This method would be

highly beneficial to

minimise errors when

the final decision

would be undertaken.

The next significant

issue could be

observed in operating

risk of the

management

framework, as

When such inefficient

risk management is

inherent, the

probability of audit

risk is increased along

with certain financial

In order to overcome

this situation, the

primary

recommendation

would be to improve

the authority and the

When the risk

management

framework is not

effective, the bank

management would be

able to minimise the

significant risks could

arise from the end of

the executive

committee.

audit risk. (Louwers et al.,

2015).

contribute to fall in

the audit risk of the

bank.

Another issue could

be observed as highly

complex and

bureaucratic

procedure in order to

undertake decisions.

The audit risk is

increased, as the

technique to identify

the financial risks of

the bank is slowed

down. In addition, it

results in an

impediment for

suitable result by

formulating over

timely collaboration

(Kend, Houghton &

Jubb, 2014).

In order to resolve this

issue, all the pertinent

aspects need to be

taken into account

before making

decisions.

This method would be

highly beneficial to

minimise errors when

the final decision

would be undertaken.

The next significant

issue could be

observed in operating

risk of the

management

framework, as

When such inefficient

risk management is

inherent, the

probability of audit

risk is increased along

with certain financial

In order to overcome

this situation, the

primary

recommendation

would be to improve

the authority and the

When the risk

management

framework is not

effective, the bank

management would be

able to minimise the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING THEORY AND PRACTICE

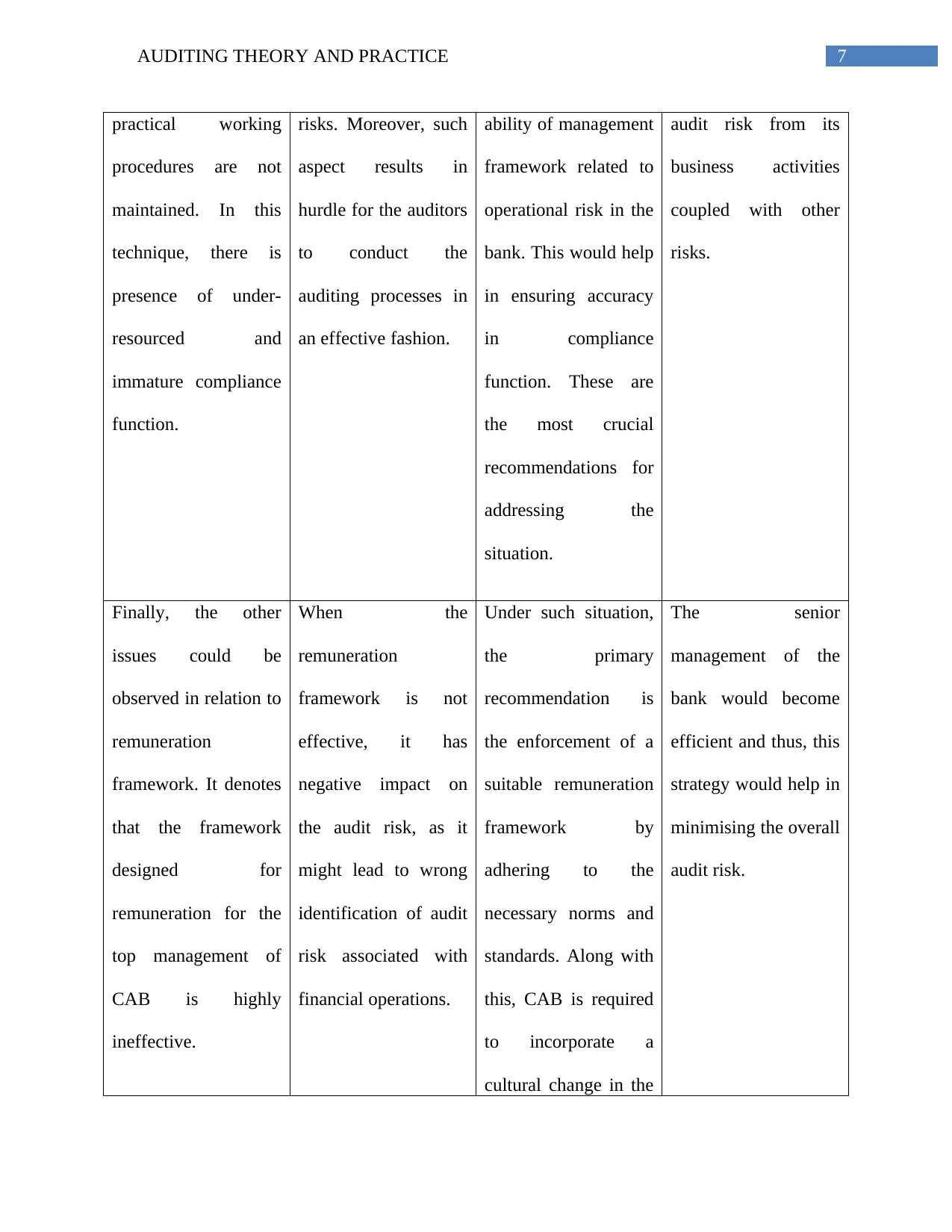

practical working

procedures are not

maintained. In this

technique, there is

presence of under-

resourced and

immature compliance

function.

risks. Moreover, such

aspect results in

hurdle for the auditors

to conduct the

auditing processes in

an effective fashion.

ability of management

framework related to

operational risk in the

bank. This would help

in ensuring accuracy

in compliance

function. These are

the most crucial

recommendations for

addressing the

situation.

audit risk from its

business activities

coupled with other

risks.

Finally, the other

issues could be

observed in relation to

remuneration

framework. It denotes

that the framework

designed for

remuneration for the

top management of

CAB is highly

ineffective.

When the

remuneration

framework is not

effective, it has

negative impact on

the audit risk, as it

might lead to wrong

identification of audit

risk associated with

financial operations.

Under such situation,

the primary

recommendation is

the enforcement of a

suitable remuneration

framework by

adhering to the

necessary norms and

standards. Along with

this, CAB is required

to incorporate a

cultural change in the

The senior

management of the

bank would become

efficient and thus, this

strategy would help in

minimising the overall

audit risk.

practical working

procedures are not

maintained. In this

technique, there is

presence of under-

resourced and

immature compliance

function.

risks. Moreover, such

aspect results in

hurdle for the auditors

to conduct the

auditing processes in

an effective fashion.

ability of management

framework related to

operational risk in the

bank. This would help

in ensuring accuracy

in compliance

function. These are

the most crucial

recommendations for

addressing the

situation.

audit risk from its

business activities

coupled with other

risks.

Finally, the other

issues could be

observed in relation to

remuneration

framework. It denotes

that the framework

designed for

remuneration for the

top management of

CAB is highly

ineffective.

When the

remuneration

framework is not

effective, it has

negative impact on

the audit risk, as it

might lead to wrong

identification of audit

risk associated with

financial operations.

Under such situation,

the primary

recommendation is

the enforcement of a

suitable remuneration

framework by

adhering to the

necessary norms and

standards. Along with

this, CAB is required

to incorporate a

cultural change in the

The senior

management of the

bank would become

efficient and thus, this

strategy would help in

minimising the overall

audit risk.

8AUDITING THEORY AND PRACTICE

organisation in order

to identify risks

effectively and the

remedial procedures.

Answer to Question 2:

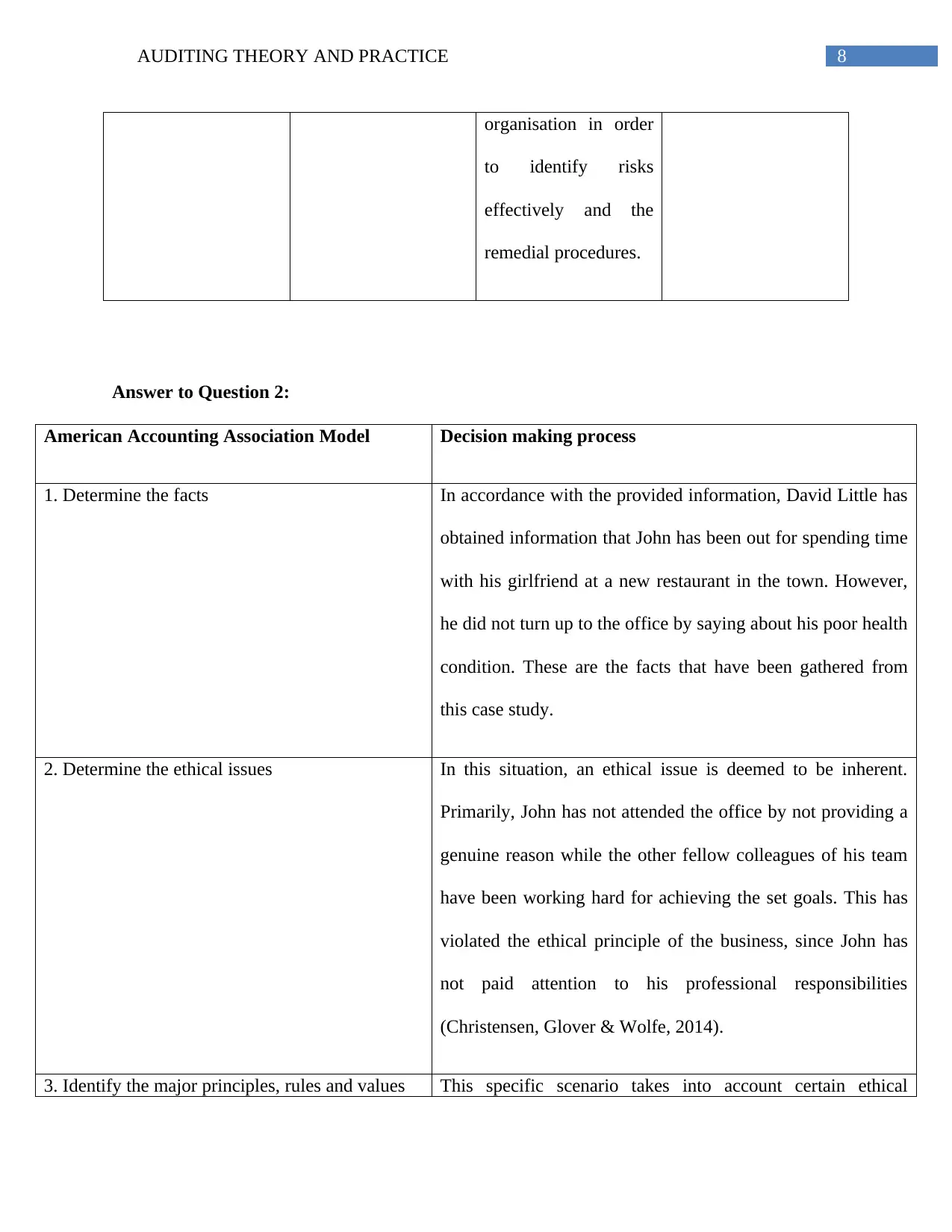

American Accounting Association Model Decision making process

1. Determine the facts In accordance with the provided information, David Little has

obtained information that John has been out for spending time

with his girlfriend at a new restaurant in the town. However,

he did not turn up to the office by saying about his poor health

condition. These are the facts that have been gathered from

this case study.

2. Determine the ethical issues In this situation, an ethical issue is deemed to be inherent.

Primarily, John has not attended the office by not providing a

genuine reason while the other fellow colleagues of his team

have been working hard for achieving the set goals. This has

violated the ethical principle of the business, since John has

not paid attention to his professional responsibilities

(Christensen, Glover & Wolfe, 2014).

3. Identify the major principles, rules and values This specific scenario takes into account certain ethical

organisation in order

to identify risks

effectively and the

remedial procedures.

Answer to Question 2:

American Accounting Association Model Decision making process

1. Determine the facts In accordance with the provided information, David Little has

obtained information that John has been out for spending time

with his girlfriend at a new restaurant in the town. However,

he did not turn up to the office by saying about his poor health

condition. These are the facts that have been gathered from

this case study.

2. Determine the ethical issues In this situation, an ethical issue is deemed to be inherent.

Primarily, John has not attended the office by not providing a

genuine reason while the other fellow colleagues of his team

have been working hard for achieving the set goals. This has

violated the ethical principle of the business, since John has

not paid attention to his professional responsibilities

(Christensen, Glover & Wolfe, 2014).

3. Identify the major principles, rules and values This specific scenario takes into account certain ethical

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING THEORY AND PRACTICE

values, principles and rules. It is noteworthy to mention that

the auditors need to be responsible for maintaining the

integrity associated with the profession by maintaining

honesty and straightforwardness (Earley et al., 2016). Along

with this, the professionals would not compromise their

responsibilities and duties in any type of circumstances.

Moreover, they need to adhere to the pertinent regulations and

laws so that any type of unprofessional acts could be avoided

(Apesb.org.au, 2018).

4. Specify the alternatives In this scenario, two courses of action are deemed to be

inherent. In accordance with the initial course of action, David

Little needs to coordinate with his other members regarding

the illegitimate action of John for assuring that the other

members receive more appreciation than John. The second

course of action states that David would not disclose any

actions of John and thus, he would allow John to receive the

same credit for the job despite of restricted efforts.

5. Compare values and alternatives It could be found that the initial course of action fully ensures

adherence to all the values, principles and norms related to

auditing profession. David is required to share such action

with his other team members, since John has not acted in

professional, honest and integrated manner in his auditing

profession (Collier, 2015).

values, principles and rules. It is noteworthy to mention that

the auditors need to be responsible for maintaining the

integrity associated with the profession by maintaining

honesty and straightforwardness (Earley et al., 2016). Along

with this, the professionals would not compromise their

responsibilities and duties in any type of circumstances.

Moreover, they need to adhere to the pertinent regulations and

laws so that any type of unprofessional acts could be avoided

(Apesb.org.au, 2018).

4. Specify the alternatives In this scenario, two courses of action are deemed to be

inherent. In accordance with the initial course of action, David

Little needs to coordinate with his other members regarding

the illegitimate action of John for assuring that the other

members receive more appreciation than John. The second

course of action states that David would not disclose any

actions of John and thus, he would allow John to receive the

same credit for the job despite of restricted efforts.

5. Compare values and alternatives It could be found that the initial course of action fully ensures

adherence to all the values, principles and norms related to

auditing profession. David is required to share such action

with his other team members, since John has not acted in

professional, honest and integrated manner in his auditing

profession (Collier, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING THEORY AND PRACTICE

6. Assess the consequences In the initial course of action, it is necessary for David to

inform his team members regarding the illegitimate action of

John in order to assure that John receives the same

appreciation. From such aspect, John would obtain a lesson

associated with integrity, professionalism and honesty

required in audit profession, which would debar him from

undertaking such kind of action in future.

From the second course of action, David would abstain from

informing his team members regarding the actions of John

and thus, he would restrict John from obtaining the same

credit like his fellow colleagues. This might lead to the fact

that John would repeat the same action in future (Williams &

Ravenscroft, 2015).

7. Make your decision Based on the above evaluation, the initial course of action is

recommended, as David should inform his other team

members about the actions of John.

Answer to Question 3:

A significant role of the inclusion of auditors as well as statutory cap could be observed

on the restriction of the auditors’ liability. In this statutory cap, the availability of few alternative

liability arrangements could be seen (Hu, 2015). In accordance with the first agreement, at the

6. Assess the consequences In the initial course of action, it is necessary for David to

inform his team members regarding the illegitimate action of

John in order to assure that John receives the same

appreciation. From such aspect, John would obtain a lesson

associated with integrity, professionalism and honesty

required in audit profession, which would debar him from

undertaking such kind of action in future.

From the second course of action, David would abstain from

informing his team members regarding the actions of John

and thus, he would restrict John from obtaining the same

credit like his fellow colleagues. This might lead to the fact

that John would repeat the same action in future (Williams &

Ravenscroft, 2015).

7. Make your decision Based on the above evaluation, the initial course of action is

recommended, as David should inform his other team

members about the actions of John.

Answer to Question 3:

A significant role of the inclusion of auditors as well as statutory cap could be observed

on the restriction of the auditors’ liability. In this statutory cap, the availability of few alternative

liability arrangements could be seen (Hu, 2015). In accordance with the first agreement, at the

11AUDITING THEORY AND PRACTICE

time an injured party is involved in filing a claim, they have the accountability for obtaining the

damages caused. Along with this, the injured parties possess the accountability of claiming all

damages from the auditors, if the misinterpretation aspect could be observed in the financial

statements. The presence of this alternative could be witnessed to the injured part, if the

tortfeasors are accountable for the damages (Paolini, 2015).

For this option, it is the duty of the auditors to assure entire compensation or a bigger

portion of the compensation for the fault conducted. In case of the second agreement, the liability

percentage for every tortfeasor to the injured party is considered as a part of fault. Due to this

reason, the injured parties do not enjoy the right of raising the overall share of compensation

(Gimbar, Hansen & Ozlanski, 2016). According to the rule, the auditors are responsible for

paying compensation exceeding the proportionate fault level, if the tortfeasors could not bear the

total payment. Due to this reason, the higher risk proportion remains with the injured party,

instead of the auditors and tortfeasors. This implies minimisation in the overall liability of the

auditors.

The formulation of a compensation cap could be observed in third type of arrangement.

In this arrangement, a maximum cap amount has been set for compensation to be imposed on

defendants. Therefore, when the auditors’ share is more than or equal to the set cap,

compensation could not be charged above the cap to the auditors (Abugu, 2014). The regulation

is similar for tortfeasors as well not able to pay their compensation portions. Hence, this system

plays a crucial role in minimising the liability of the auditors.

time an injured party is involved in filing a claim, they have the accountability for obtaining the

damages caused. Along with this, the injured parties possess the accountability of claiming all

damages from the auditors, if the misinterpretation aspect could be observed in the financial

statements. The presence of this alternative could be witnessed to the injured part, if the

tortfeasors are accountable for the damages (Paolini, 2015).

For this option, it is the duty of the auditors to assure entire compensation or a bigger

portion of the compensation for the fault conducted. In case of the second agreement, the liability

percentage for every tortfeasor to the injured party is considered as a part of fault. Due to this

reason, the injured parties do not enjoy the right of raising the overall share of compensation

(Gimbar, Hansen & Ozlanski, 2016). According to the rule, the auditors are responsible for

paying compensation exceeding the proportionate fault level, if the tortfeasors could not bear the

total payment. Due to this reason, the higher risk proportion remains with the injured party,

instead of the auditors and tortfeasors. This implies minimisation in the overall liability of the

auditors.

The formulation of a compensation cap could be observed in third type of arrangement.

In this arrangement, a maximum cap amount has been set for compensation to be imposed on

defendants. Therefore, when the auditors’ share is more than or equal to the set cap,

compensation could not be charged above the cap to the auditors (Abugu, 2014). The regulation

is similar for tortfeasors as well not able to pay their compensation portions. Hence, this system

plays a crucial role in minimising the liability of the auditors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.