Report on Auditing and Accounting: Liquidity, Solvency, and Assurance

VerifiedAdded on 2022/03/29

|7

|1320

|30

Report

AI Summary

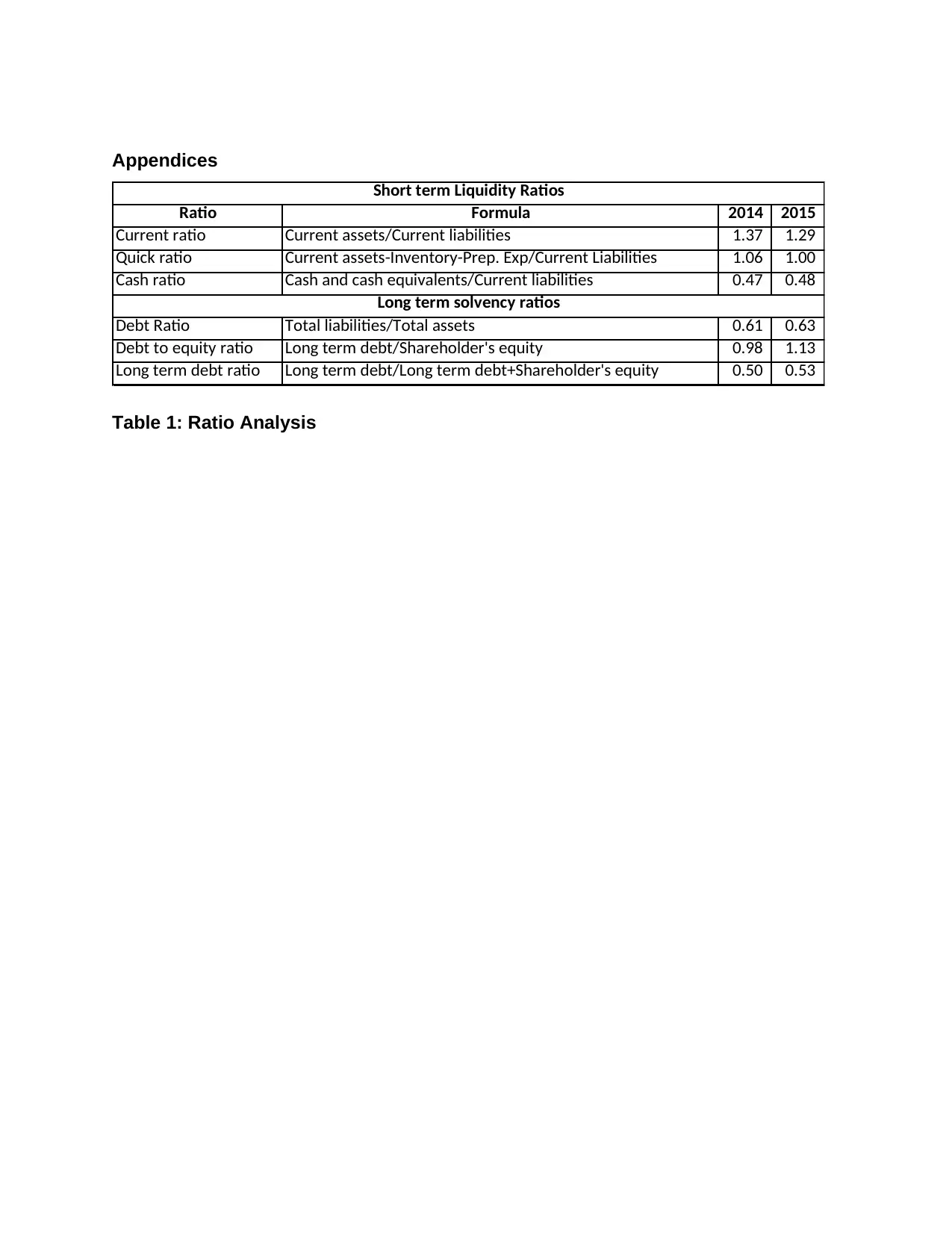

This report delves into the critical aspects of auditing and accounting, exploring both short-term liquidity and long-term solvency. It begins with an introduction to liquidity and solvency ratios, highlighting their importance in assessing a company's financial health. The report then presents an analysis of BP Plc, calculating and interpreting various financial ratios such as current ratio, quick ratio, cash ratio, debt ratio, debt-to-equity ratio, and long-term debt ratio for the year 2015. The analysis provides insights into BP Plc's ability to meet its short-term liabilities, manage its debt, and generate income from long-term liabilities. Furthermore, the report emphasizes the importance of auditing and assurance in building investor confidence. It explains how auditing of financial statements ensures the authenticity of provided figures, while assurance confirms the reliability of audit reports. The report discusses the expectations of stakeholders regarding transparency in financial statements and the role of assurance committees in validating audit findings. It concludes by stressing the necessity of regular audits for maintaining investor trust and the significance of external opinions in investment decisions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.