Auditing and Assurance Services: Key Audit Matters Analysis

VerifiedAdded on 2022/05/10

|14

|3594

|35

Report

AI Summary

This report provides an in-depth analysis of auditing and assurance services, focusing on the identification and communication of key audit matters (KAM). It examines two case studies, Advanced Computer Solutions and Green Machine Ltd, to illustrate the application of ASA 701 in determining and disclosing KAM. The analysis includes assessing audit assertions related to inventory and property, plant, and equipment (PPE), identifying risks of material misstatement, and developing substantive audit procedures. For Advanced Computer Solutions, the report addresses accuracy/valuation and cut-off assertions related to inventory, while for Green Machine Ltd, it focuses on accuracy and valuation assertions concerning PPE. The report details the rationale behind determining specific issues as KAM and provides a structured disclosure of these matters, including their significance and the audit procedures employed to address them. The report concludes by emphasizing the importance of effectively communicating KAM to enhance the transparency and reliability of financial reporting.

Running head: AUDITING AND ASSURANCE SERVICES

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Auditing and Assurance Services

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE SERVICES

Table of Contents

Introduction................................................................................................................................2

Question 1: Advanced Computer Solutions...............................................................................2

Answer to [a]..........................................................................................................................2

Answer to [b]..........................................................................................................................3

Answer to [c]..........................................................................................................................4

ASA 701 Communicating the Key Audit Matters..............................................................4

Rationales for Determination.............................................................................................5

Disclosure of Key Audit Matters.......................................................................................5

Question 2: Green Machine Ltd.................................................................................................6

Answer to [a]..........................................................................................................................6

Answer to [b]..........................................................................................................................7

Answer to [c]..........................................................................................................................8

ASA 701 Communicating the Key Audit Matters..............................................................8

Rationales for Determination.............................................................................................9

Disclosure of Key Audit Matters.......................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Introduction

Table of Contents

Introduction................................................................................................................................2

Question 1: Advanced Computer Solutions...............................................................................2

Answer to [a]..........................................................................................................................2

Answer to [b]..........................................................................................................................3

Answer to [c]..........................................................................................................................4

ASA 701 Communicating the Key Audit Matters..............................................................4

Rationales for Determination.............................................................................................5

Disclosure of Key Audit Matters.......................................................................................5

Question 2: Green Machine Ltd.................................................................................................6

Answer to [a]..........................................................................................................................6

Answer to [b]..........................................................................................................................7

Answer to [c]..........................................................................................................................8

ASA 701 Communicating the Key Audit Matters..............................................................8

Rationales for Determination.............................................................................................9

Disclosure of Key Audit Matters.......................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Introduction

2AUDITING AND ASSURANCE SERVICES

The prime responsibility of the auditors can be found in the examination as well as

analysis of the financial statements of the companies in order to ensure the fact that there is

not any material misstatements in them as a result of errors and frauds; and the key

stakeholders of the companies use the report of the auditors to verify the fairness and

truthfulness of the company’s financial statements (Bédard and Courteau 2015). At the time

of the development of these financial statements and reports, the managements of the audit

clients use certain assertions. Audit assertions are the implicit or explicit claims along with

certain representations that the managements of the clients make for the preparation of

financial statements concerning its appropriateness of various financial statements elements

and disclosures. Managements of the companies use different audit assertions for inventory,

property, plant and equipment and others; such as accuracy, valuation, cut off, completeness,

existence, occurrence and others (Knechel and Salterio 2016). At the time of auditing the

clients’ financial statements, it is essential for the auditors to consider examining these audit

assertions with the aim to verify the truthfulness of the used judgements and assumptions by

the managements for the preparation of financial statements. After that, they need to

determine the Key Audit Matters in case the risks have significance in auditing (Louwers et

al. 2015). This report sheds light on the used assertion of the given companies from the

perspective of an auditor for the determination of key audit matters.

Question 1: Advanced Computer Solutions

Answer to [a]

Accuracy/Valuation

At the time to test this audit assertion, the two significant matter faced by the auditors

are to provide the necessary assurance on the correctness of all the values and figures of

physical inventory count and to provide assurance on the aspect that correct amount of

The prime responsibility of the auditors can be found in the examination as well as

analysis of the financial statements of the companies in order to ensure the fact that there is

not any material misstatements in them as a result of errors and frauds; and the key

stakeholders of the companies use the report of the auditors to verify the fairness and

truthfulness of the company’s financial statements (Bédard and Courteau 2015). At the time

of the development of these financial statements and reports, the managements of the audit

clients use certain assertions. Audit assertions are the implicit or explicit claims along with

certain representations that the managements of the clients make for the preparation of

financial statements concerning its appropriateness of various financial statements elements

and disclosures. Managements of the companies use different audit assertions for inventory,

property, plant and equipment and others; such as accuracy, valuation, cut off, completeness,

existence, occurrence and others (Knechel and Salterio 2016). At the time of auditing the

clients’ financial statements, it is essential for the auditors to consider examining these audit

assertions with the aim to verify the truthfulness of the used judgements and assumptions by

the managements for the preparation of financial statements. After that, they need to

determine the Key Audit Matters in case the risks have significance in auditing (Louwers et

al. 2015). This report sheds light on the used assertion of the given companies from the

perspective of an auditor for the determination of key audit matters.

Question 1: Advanced Computer Solutions

Answer to [a]

Accuracy/Valuation

At the time to test this audit assertion, the two significant matter faced by the auditors

are to provide the necessary assurance on the correctness of all the values and figures of

physical inventory count and to provide assurance on the aspect that correct amount of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE SERVICES

inventory has come as cost of goods sold in the income statements from the balance sheet

(Stagg et al. 2018). For these reasons, accuracy or valuation of inventory needs to be tested

by the auditors. The case study of Advanced Computer Solutions shows that the inventories

of the company are transferred to six new regional warehouses and this incident can lead to

the miscalculation in the physical inventory count which can reduce the inventory turnover in

2018. In addition, issues in software can cause error in the inventory valuation process (Ma

2016). These reasons states that this assertion is at risk.

Cut Off

It is needed for the managements of the audit clients to ensure proper recording of the

values of inventory in the correct accounting period when they take place. Considering

examination of the shipping and receiving documents of inventory is a crucial aspect as it

assists in cut off of inventory (Bumgarner and Vasarhelyi 2018). Hence, the companies

cannot record the value of inventory of past year in the accounting book of the present year.

However, this aspect can be seen in case of Advanced Computer Solution as the inventory of

the year 2018 consists of the sales of both 2018 and 2017. This event is the proof that there is

an error or errors in the recording of inventory in the correct year’s accounting books. It can

also be happened that the problem in software might lead to this issue or any staff is

responsible for the same (Kharisova and Kozlova 2014). Hence, it is evident that this

assertion is at risk.

Answer to [b]

Substantive Audit Procedure 1: For addressing this risk, the main audit procedure is the

methodical surveillance of every aspect of the physical inventory count procedure of

Advanced Computer Solutions (Glover, Prawitt and Drake 2014). Certain initiatives that the

auditor needs to take are conversing about the strengths and weaknesses of internal control

inventory has come as cost of goods sold in the income statements from the balance sheet

(Stagg et al. 2018). For these reasons, accuracy or valuation of inventory needs to be tested

by the auditors. The case study of Advanced Computer Solutions shows that the inventories

of the company are transferred to six new regional warehouses and this incident can lead to

the miscalculation in the physical inventory count which can reduce the inventory turnover in

2018. In addition, issues in software can cause error in the inventory valuation process (Ma

2016). These reasons states that this assertion is at risk.

Cut Off

It is needed for the managements of the audit clients to ensure proper recording of the

values of inventory in the correct accounting period when they take place. Considering

examination of the shipping and receiving documents of inventory is a crucial aspect as it

assists in cut off of inventory (Bumgarner and Vasarhelyi 2018). Hence, the companies

cannot record the value of inventory of past year in the accounting book of the present year.

However, this aspect can be seen in case of Advanced Computer Solution as the inventory of

the year 2018 consists of the sales of both 2018 and 2017. This event is the proof that there is

an error or errors in the recording of inventory in the correct year’s accounting books. It can

also be happened that the problem in software might lead to this issue or any staff is

responsible for the same (Kharisova and Kozlova 2014). Hence, it is evident that this

assertion is at risk.

Answer to [b]

Substantive Audit Procedure 1: For addressing this risk, the main audit procedure is the

methodical surveillance of every aspect of the physical inventory count procedure of

Advanced Computer Solutions (Glover, Prawitt and Drake 2014). Certain initiatives that the

auditor needs to take are conversing about the strengths and weaknesses of internal control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE SERVICES

related to inventory, verifying the tags made for the inventory count and to be present when

the inventory counts process is on progress. Moreover, the inventories need to be examines in

all the warehouses. Lastly, the auditor needs to test the judgments and assumptions of the

management along with their compliance with the required accounting standards (Glover,

Prawitt and Drake 2014).

Substantive Audit Procedure 2: For the examination of cut offs, the substantive audit

procedure will be the verification of all the notes for goods received and goods supplied so

that the reporting date can be identified (Byrnes et al. 2018). After that, the auditor needs to

undertake examining whether the inventory moved slowly or there was any irrational

adjustments in them. Moreover, the auditor need to verify whether the company has provided

any stop order in receiving the inventories in the warehouses as these aspects together can

create the issue of inventory cut offs (Byrnes et al. 2018).

Answer to [c]

ASA 701 Communicating the Key Audit Matters

As per Section 7 of ASA 701, the objectives of the auditors are the ascertainment of

the key audit matters, formulation of the key audit matters based on them and disclose as well

as communicate them in the auditor’s report (auasb.gov.au 2019).

According to the definition of Key Audit Matters in Section 8 of ASA 701, these are

the issues or matters that are important to the auditors to audit the financial reports of the

clients; and they need to be selected from the discussion with the governance team

(auasb.gov.au 2019).

According to Section 9 of ASA 701, the auditors are required to consider three

specific requirements in determining the key audit matters; they are the parts in the financial

statements with the higher risk of material misstatements in accordance with ASA 315, the

related to inventory, verifying the tags made for the inventory count and to be present when

the inventory counts process is on progress. Moreover, the inventories need to be examines in

all the warehouses. Lastly, the auditor needs to test the judgments and assumptions of the

management along with their compliance with the required accounting standards (Glover,

Prawitt and Drake 2014).

Substantive Audit Procedure 2: For the examination of cut offs, the substantive audit

procedure will be the verification of all the notes for goods received and goods supplied so

that the reporting date can be identified (Byrnes et al. 2018). After that, the auditor needs to

undertake examining whether the inventory moved slowly or there was any irrational

adjustments in them. Moreover, the auditor need to verify whether the company has provided

any stop order in receiving the inventories in the warehouses as these aspects together can

create the issue of inventory cut offs (Byrnes et al. 2018).

Answer to [c]

ASA 701 Communicating the Key Audit Matters

As per Section 7 of ASA 701, the objectives of the auditors are the ascertainment of

the key audit matters, formulation of the key audit matters based on them and disclose as well

as communicate them in the auditor’s report (auasb.gov.au 2019).

According to the definition of Key Audit Matters in Section 8 of ASA 701, these are

the issues or matters that are important to the auditors to audit the financial reports of the

clients; and they need to be selected from the discussion with the governance team

(auasb.gov.au 2019).

According to Section 9 of ASA 701, the auditors are required to consider three

specific requirements in determining the key audit matters; they are the parts in the financial

statements with the higher risk of material misstatements in accordance with ASA 315, the

5AUDITING AND ASSURANCE SERVICES

judgements as well as accounting estimates used by the management of clients that are in

uncertainty and the impact of the significant transactions or issues on auditing that occurred

during the accounting period (auasb.gov.au 2019).

According to Section 10 of ASA 701, key audit matters need to be determined by the

auditors after the consideration of the significant events and their impact on auditing

(auasb.gov.au 2019).

Rationales for Determination

The presence of errors in inventory valuation can be considered as significant area in

the financial statements having higher risk of material misstatements.

The presence of errors in inventory valuation indicates that there may be some

uncertainties in the used judgments and accounting estimates used by the management

for the inventory valuation.

The occurrence of significant events can be seen that is the transfer of inventories in

six different warehouses from the central warehouse that can have impact on the

process of inventory count and valuation (Kachelmeier, Schmidt and Valentine 2017).

Disclosure of Key Audit Matters

Why Significant How Audit Addressed the Key Audit

Mattes

Transfer of inventory on March 2018

The company has recently transferred their

huge inventory base from one central

warehouse to six different warehouses and

the physical inventory count process can be

impacted with this incident. In addition,

inventory valuation includes significant

judgment and accounting estimated of the

management that are significant for the audit.

The undertaken audit procedures are:

- Methodical surveillance of every aspect of

the physical inventory count procedure

- Conversing about the strengths and

weaknesses of internal control related to

inventory

- Verifying the tags made for the inventory

count

- Observe when the inventory counts process

judgements as well as accounting estimates used by the management of clients that are in

uncertainty and the impact of the significant transactions or issues on auditing that occurred

during the accounting period (auasb.gov.au 2019).

According to Section 10 of ASA 701, key audit matters need to be determined by the

auditors after the consideration of the significant events and their impact on auditing

(auasb.gov.au 2019).

Rationales for Determination

The presence of errors in inventory valuation can be considered as significant area in

the financial statements having higher risk of material misstatements.

The presence of errors in inventory valuation indicates that there may be some

uncertainties in the used judgments and accounting estimates used by the management

for the inventory valuation.

The occurrence of significant events can be seen that is the transfer of inventories in

six different warehouses from the central warehouse that can have impact on the

process of inventory count and valuation (Kachelmeier, Schmidt and Valentine 2017).

Disclosure of Key Audit Matters

Why Significant How Audit Addressed the Key Audit

Mattes

Transfer of inventory on March 2018

The company has recently transferred their

huge inventory base from one central

warehouse to six different warehouses and

the physical inventory count process can be

impacted with this incident. In addition,

inventory valuation includes significant

judgment and accounting estimated of the

management that are significant for the audit.

The undertaken audit procedures are:

- Methodical surveillance of every aspect of

the physical inventory count procedure

- Conversing about the strengths and

weaknesses of internal control related to

inventory

- Verifying the tags made for the inventory

count

- Observe when the inventory counts process

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE SERVICES

is on progress

- Test the judgments and assumptions of the

management along with their compliance

with the required accounting standards

-Testing the inventories in all warehouses

Inclusion of previous year’s sales in the

inventory of 2018

The inventory of 2018 consists of the sales of

2018 and 2017 that indicates the presence of

error. In addition, involvement of significant

management’s judgements and accounting

estimates are there. These can have material

impacts.

The undertaken audit procedures are:

- Verification of all the notes for goods

received and goods supplied so that the

reporting date can be identified

- Examining whether the inventory moved

slowly or there was any irrational

adjustments in them

- Verify whether the company has provided

any stop order in receiving the inventories in

the warehouses

Question 2: Green Machine Ltd

Answer to [a]

Accuracy: The use of this particular assertion demands the commitment of the companies to

accurately record all the transactions related to property, plant and equipment. It means the

companies need to ensure the appropriate classification and distinction of all the expenses

related to the property, plant and equipment (Peytcheva 2013). The case study of Green

Machine Ltd shows the inaccurate distinction of the revenue and capital expenditures by the

company. Certain revenue expenses are capitalized and certain capital expenditures are

showed as revenue expenses in the income statements. Thus, it is clear from this aspect that

there is error in the classification of major expenses related to property, plant and equipment

in the company which can create material effects on the company’s financial statements

(Omer, Sharp and Wang 2018). For this reason, this assertion is at risk.

is on progress

- Test the judgments and assumptions of the

management along with their compliance

with the required accounting standards

-Testing the inventories in all warehouses

Inclusion of previous year’s sales in the

inventory of 2018

The inventory of 2018 consists of the sales of

2018 and 2017 that indicates the presence of

error. In addition, involvement of significant

management’s judgements and accounting

estimates are there. These can have material

impacts.

The undertaken audit procedures are:

- Verification of all the notes for goods

received and goods supplied so that the

reporting date can be identified

- Examining whether the inventory moved

slowly or there was any irrational

adjustments in them

- Verify whether the company has provided

any stop order in receiving the inventories in

the warehouses

Question 2: Green Machine Ltd

Answer to [a]

Accuracy: The use of this particular assertion demands the commitment of the companies to

accurately record all the transactions related to property, plant and equipment. It means the

companies need to ensure the appropriate classification and distinction of all the expenses

related to the property, plant and equipment (Peytcheva 2013). The case study of Green

Machine Ltd shows the inaccurate distinction of the revenue and capital expenditures by the

company. Certain revenue expenses are capitalized and certain capital expenditures are

showed as revenue expenses in the income statements. Thus, it is clear from this aspect that

there is error in the classification of major expenses related to property, plant and equipment

in the company which can create material effects on the company’s financial statements

(Omer, Sharp and Wang 2018). For this reason, this assertion is at risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE SERVICES

Valuation: This particular assertion demands the commitment of the audit clients that they

will record all the assets, liabilities and equity at their cost value after the deduction of

accumulated depreciation; and thus, they must apply the correct rate of depreciation. This is

an essential requirement for the companies (Mock and Fukukawa 2015). As per the case

study of Green Machine Ltd, the rates of depreciation charged on property, plant and

equipment are too low and this aspect can lead to the incorrect valuation of property, plant

and equipment. Apart from this, application of the low depreciation rate can create different

in operating expenses of the company which can ultimately leads to the misstatements of

company’s net profit. In the presence of all these reasons, this assertion can be considered at

risk (Bowlin, Hobson and Piercey 2015).

Answer to [b]

Substantive Audit Procedure 1: In the part of substantive audit procedures, the auditor of

Green Machine Ltd must review the policies and procedures of the company for the

determination of the capital and revenue expenditures related to property, plant and

equipment (Kuenkaikaew and Vasarhelyi 2013). In order to do this, it is needed for the

auditor to collect the list of property, plant and equipment and must ensure verifying the fact

that the company has complied with the necessary accounting regulation and standards

related to the expense of property, plant and equipment (Kuenkaikaew and Vasarhelyi 2013).

Substantive Audit Procedure 2: In this part of the substantive audit procedure, it is essential

for the auditor of the company to review the deprecation policies of the company along with

reviewing the judgments and accounting estimated used by the management (Pizzini, Lin and

Ziegenfuss 2014). After that, the auditor needs to consider recalculating the rate of

depreciation after analyzing the property, plant and equipment’s residual value and any gain

or loss from the sale of them. In this process, comparison of the ratios of depreciation needs

Valuation: This particular assertion demands the commitment of the audit clients that they

will record all the assets, liabilities and equity at their cost value after the deduction of

accumulated depreciation; and thus, they must apply the correct rate of depreciation. This is

an essential requirement for the companies (Mock and Fukukawa 2015). As per the case

study of Green Machine Ltd, the rates of depreciation charged on property, plant and

equipment are too low and this aspect can lead to the incorrect valuation of property, plant

and equipment. Apart from this, application of the low depreciation rate can create different

in operating expenses of the company which can ultimately leads to the misstatements of

company’s net profit. In the presence of all these reasons, this assertion can be considered at

risk (Bowlin, Hobson and Piercey 2015).

Answer to [b]

Substantive Audit Procedure 1: In the part of substantive audit procedures, the auditor of

Green Machine Ltd must review the policies and procedures of the company for the

determination of the capital and revenue expenditures related to property, plant and

equipment (Kuenkaikaew and Vasarhelyi 2013). In order to do this, it is needed for the

auditor to collect the list of property, plant and equipment and must ensure verifying the fact

that the company has complied with the necessary accounting regulation and standards

related to the expense of property, plant and equipment (Kuenkaikaew and Vasarhelyi 2013).

Substantive Audit Procedure 2: In this part of the substantive audit procedure, it is essential

for the auditor of the company to review the deprecation policies of the company along with

reviewing the judgments and accounting estimated used by the management (Pizzini, Lin and

Ziegenfuss 2014). After that, the auditor needs to consider recalculating the rate of

depreciation after analyzing the property, plant and equipment’s residual value and any gain

or loss from the sale of them. In this process, comparison of the ratios of depreciation needs

8AUDITING AND ASSURANCE SERVICES

to be done. In this process, the auditor will be able to recalculate the revised rates of

depreciation along with the revised depreciation expenses (Pizzini, Lin and Ziegenfuss 2014).

Answer to [c]

ASA 701 Communicating the Key Audit Matters

According to Section 7 of ASA 701, the auditor’s objectives are the determination of

the key audit matters, development of appropriate audit opinion based on them and reveal as

well as converse them in the report of the auditor (legislation.gov.au 2019).

As per the description of Key Audit Matters in Section 8 of ASA 701, they are the

issues or substances that are significant to the auditors to audit the financial reports of the

clients; and they need to be selected from the conversation with the governance authorities of

the companies (legislation.gov.au 2019).

As per Section 9 of ASA 701, the auditors must take into account three specific

requirements for the determination of the key audit matters; they are the regions in the

financial statements with the superior risk of material misstatements according to the

standards of ASA 315, the judgements and accounting estimates utilized by the management

of clients that are in doubt and the impact of the significant transactions or issues on auditing

that took place during the accounting period (legislation.gov.au 2019).

According to Section 10 of ASA 701, the auditors are needed to determine the key

audit matters after taking into account the significant events and their impact on auditing

(legislation.gov.au 2019).

Rationales for Determination

The inappropriateness in the distinction of capital and revenue expenses along with

the incorrect valuation of depreciation are the areas in the financial statements of

Green Machine Ltd containing greater material misstatements risks.

to be done. In this process, the auditor will be able to recalculate the revised rates of

depreciation along with the revised depreciation expenses (Pizzini, Lin and Ziegenfuss 2014).

Answer to [c]

ASA 701 Communicating the Key Audit Matters

According to Section 7 of ASA 701, the auditor’s objectives are the determination of

the key audit matters, development of appropriate audit opinion based on them and reveal as

well as converse them in the report of the auditor (legislation.gov.au 2019).

As per the description of Key Audit Matters in Section 8 of ASA 701, they are the

issues or substances that are significant to the auditors to audit the financial reports of the

clients; and they need to be selected from the conversation with the governance authorities of

the companies (legislation.gov.au 2019).

As per Section 9 of ASA 701, the auditors must take into account three specific

requirements for the determination of the key audit matters; they are the regions in the

financial statements with the superior risk of material misstatements according to the

standards of ASA 315, the judgements and accounting estimates utilized by the management

of clients that are in doubt and the impact of the significant transactions or issues on auditing

that took place during the accounting period (legislation.gov.au 2019).

According to Section 10 of ASA 701, the auditors are needed to determine the key

audit matters after taking into account the significant events and their impact on auditing

(legislation.gov.au 2019).

Rationales for Determination

The inappropriateness in the distinction of capital and revenue expenses along with

the incorrect valuation of depreciation are the areas in the financial statements of

Green Machine Ltd containing greater material misstatements risks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE SERVICES

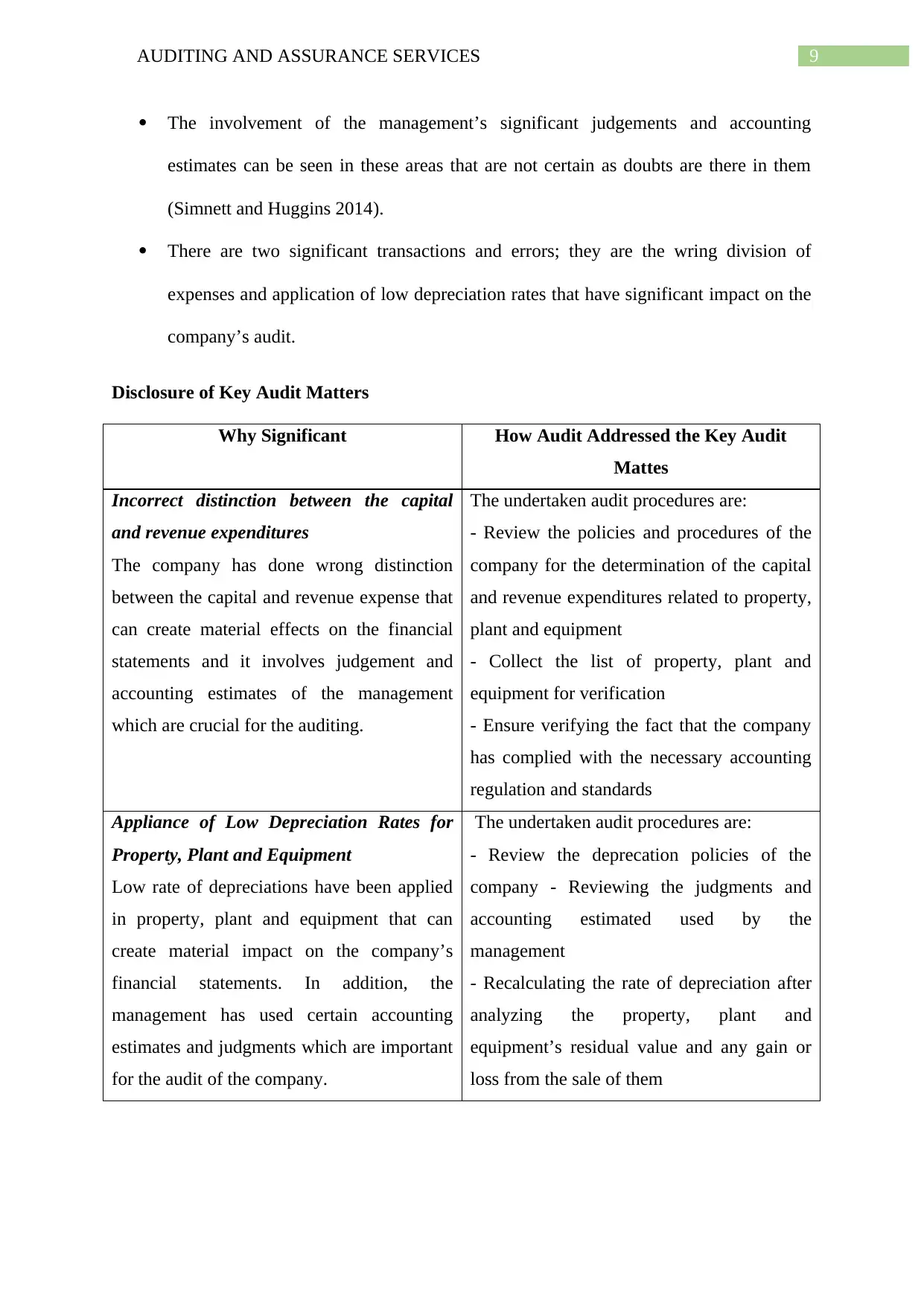

The involvement of the management’s significant judgements and accounting

estimates can be seen in these areas that are not certain as doubts are there in them

(Simnett and Huggins 2014).

There are two significant transactions and errors; they are the wring division of

expenses and application of low depreciation rates that have significant impact on the

company’s audit.

Disclosure of Key Audit Matters

Why Significant How Audit Addressed the Key Audit

Mattes

Incorrect distinction between the capital

and revenue expenditures

The company has done wrong distinction

between the capital and revenue expense that

can create material effects on the financial

statements and it involves judgement and

accounting estimates of the management

which are crucial for the auditing.

The undertaken audit procedures are:

- Review the policies and procedures of the

company for the determination of the capital

and revenue expenditures related to property,

plant and equipment

- Collect the list of property, plant and

equipment for verification

- Ensure verifying the fact that the company

has complied with the necessary accounting

regulation and standards

Appliance of Low Depreciation Rates for

Property, Plant and Equipment

Low rate of depreciations have been applied

in property, plant and equipment that can

create material impact on the company’s

financial statements. In addition, the

management has used certain accounting

estimates and judgments which are important

for the audit of the company.

The undertaken audit procedures are:

- Review the deprecation policies of the

company - Reviewing the judgments and

accounting estimated used by the

management

- Recalculating the rate of depreciation after

analyzing the property, plant and

equipment’s residual value and any gain or

loss from the sale of them

The involvement of the management’s significant judgements and accounting

estimates can be seen in these areas that are not certain as doubts are there in them

(Simnett and Huggins 2014).

There are two significant transactions and errors; they are the wring division of

expenses and application of low depreciation rates that have significant impact on the

company’s audit.

Disclosure of Key Audit Matters

Why Significant How Audit Addressed the Key Audit

Mattes

Incorrect distinction between the capital

and revenue expenditures

The company has done wrong distinction

between the capital and revenue expense that

can create material effects on the financial

statements and it involves judgement and

accounting estimates of the management

which are crucial for the auditing.

The undertaken audit procedures are:

- Review the policies and procedures of the

company for the determination of the capital

and revenue expenditures related to property,

plant and equipment

- Collect the list of property, plant and

equipment for verification

- Ensure verifying the fact that the company

has complied with the necessary accounting

regulation and standards

Appliance of Low Depreciation Rates for

Property, Plant and Equipment

Low rate of depreciations have been applied

in property, plant and equipment that can

create material impact on the company’s

financial statements. In addition, the

management has used certain accounting

estimates and judgments which are important

for the audit of the company.

The undertaken audit procedures are:

- Review the deprecation policies of the

company - Reviewing the judgments and

accounting estimated used by the

management

- Recalculating the rate of depreciation after

analyzing the property, plant and

equipment’s residual value and any gain or

loss from the sale of them

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE SERVICES

Conclusion

It can be seen from the above discussion that the key assertions at risk for Advanced

Computer Solutions are accuracy/valuation and cut off; and the key assertions at risk for

Green Machine Ltd are accuracy and valuation. It can be seen from the discussion part of the

report that the auditors are needed to take into account the assertions at risk at the time to plan

the substantive audit procedures as these procedures must be able to minimize the risks. ASA

701 provides the auditors with the necessary guidelines and principles for the determination

of the key audit matters. The above discussion shows the responsibility of both the auditors of

the companies to effectively communicate and disclose the key audit matters in the respective

section of the audit report. Hence, it is the obligation on the auditors to adhere to the

standards of ASA 701 for determining the key audit matters.

Conclusion

It can be seen from the above discussion that the key assertions at risk for Advanced

Computer Solutions are accuracy/valuation and cut off; and the key assertions at risk for

Green Machine Ltd are accuracy and valuation. It can be seen from the discussion part of the

report that the auditors are needed to take into account the assertions at risk at the time to plan

the substantive audit procedures as these procedures must be able to minimize the risks. ASA

701 provides the auditors with the necessary guidelines and principles for the determination

of the key audit matters. The above discussion shows the responsibility of both the auditors of

the companies to effectively communicate and disclose the key audit matters in the respective

section of the audit report. Hence, it is the obligation on the auditors to adhere to the

standards of ASA 701 for determining the key audit matters.

11AUDITING AND ASSURANCE SERVICES

References

Auasb.gov.au. 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 18 Jan.

2019].

Bédard, J. and Courteau, L., 2015. Benefits and costs of auditor's assurance: Evidence from

the review of quarterly financial statements. Contemporary Accounting Research, 32(1),

pp.308-335.

Bowlin, K.O., Hobson, J.L. and Piercey, M.D., 2015. The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Bumgarner, N. and Vasarhelyi, M.A., 2018. Continuous auditing—a new view.

In Continuous Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

Glover, S.M., Prawitt, D.F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory, 34(3), pp.161-179.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

References

Auasb.gov.au. 2019. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 18 Jan.

2019].

Bédard, J. and Courteau, L., 2015. Benefits and costs of auditor's assurance: Evidence from

the review of quarterly financial statements. Contemporary Accounting Research, 32(1),

pp.308-335.

Bowlin, K.O., Hobson, J.L. and Piercey, M.D., 2015. The effects of auditor rotation,

professional skepticism, and interactions with managers on audit quality. The Accounting

Review, 90(4), pp.1363-1393.

Bumgarner, N. and Vasarhelyi, M.A., 2018. Continuous auditing—a new view.

In Continuous Auditing: Theory and Application (pp. 7-51). Emerald Publishing Limited.

Byrnes, P.E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J.D. and

Vasarhelyi, M., 2018. Evolution of Auditing: From the Traditional Approach to the Future

Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297). Emerald Publishing

Limited.

Glover, S.M., Prawitt, D.F. and Drake, M.S., 2014. Between a rock and a hard place: A path

forward for using substantive analytical procedures in auditing large P&L accounts:

Commentary and analysis. Auditing: A Journal of Practice & Theory, 34(3), pp.161-179.

Kachelmeier, S.J., Schmidt, J.J. and Valentine, K., 2017. The disclaimer effect of disclosing

critical audit matters in the auditor’s report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.