Auditing and Assurance: Risk Analysis of CBA and JB hi-fi

VerifiedAdded on 2020/05/28

|10

|1982

|75

Homework Assignment

AI Summary

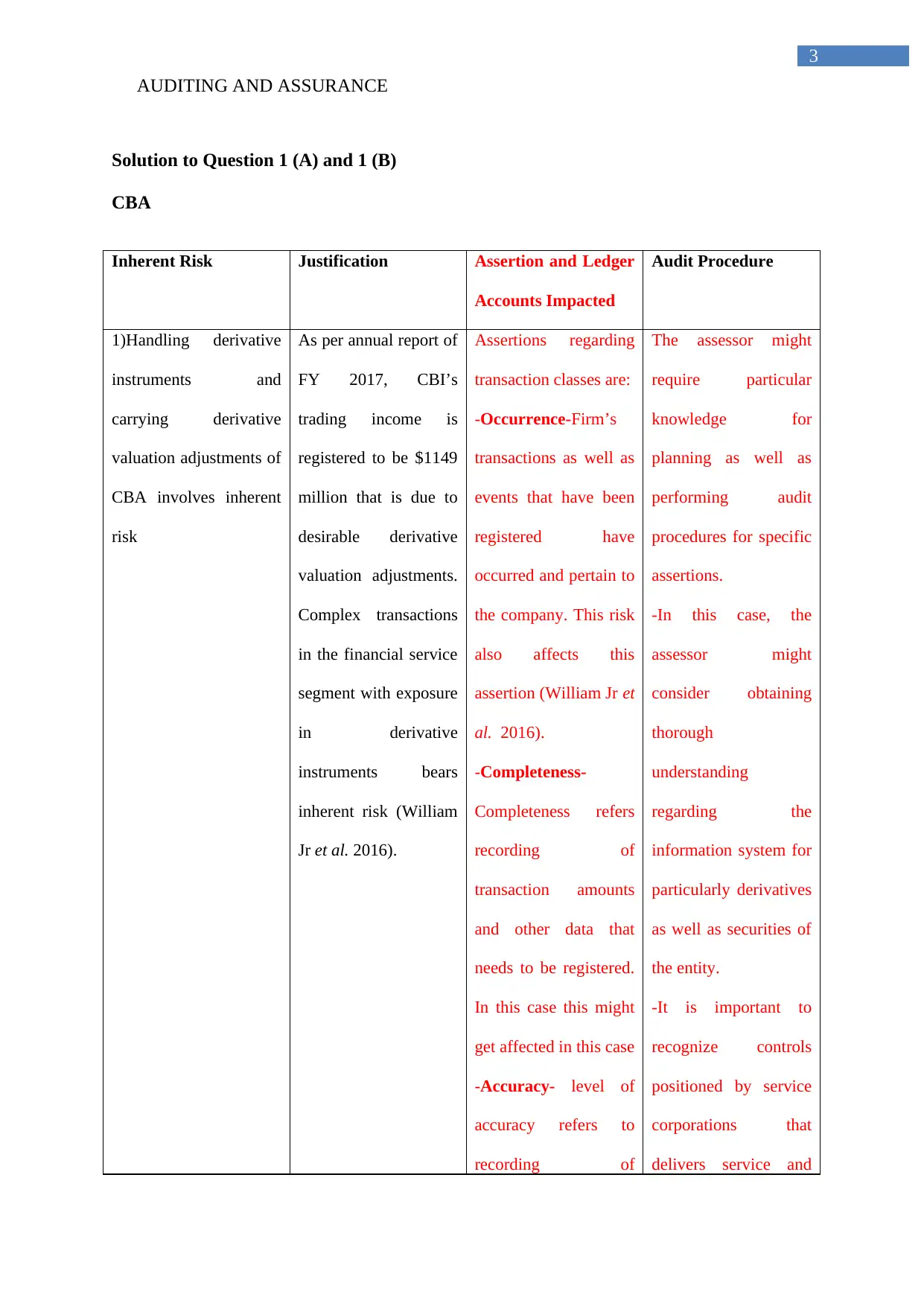

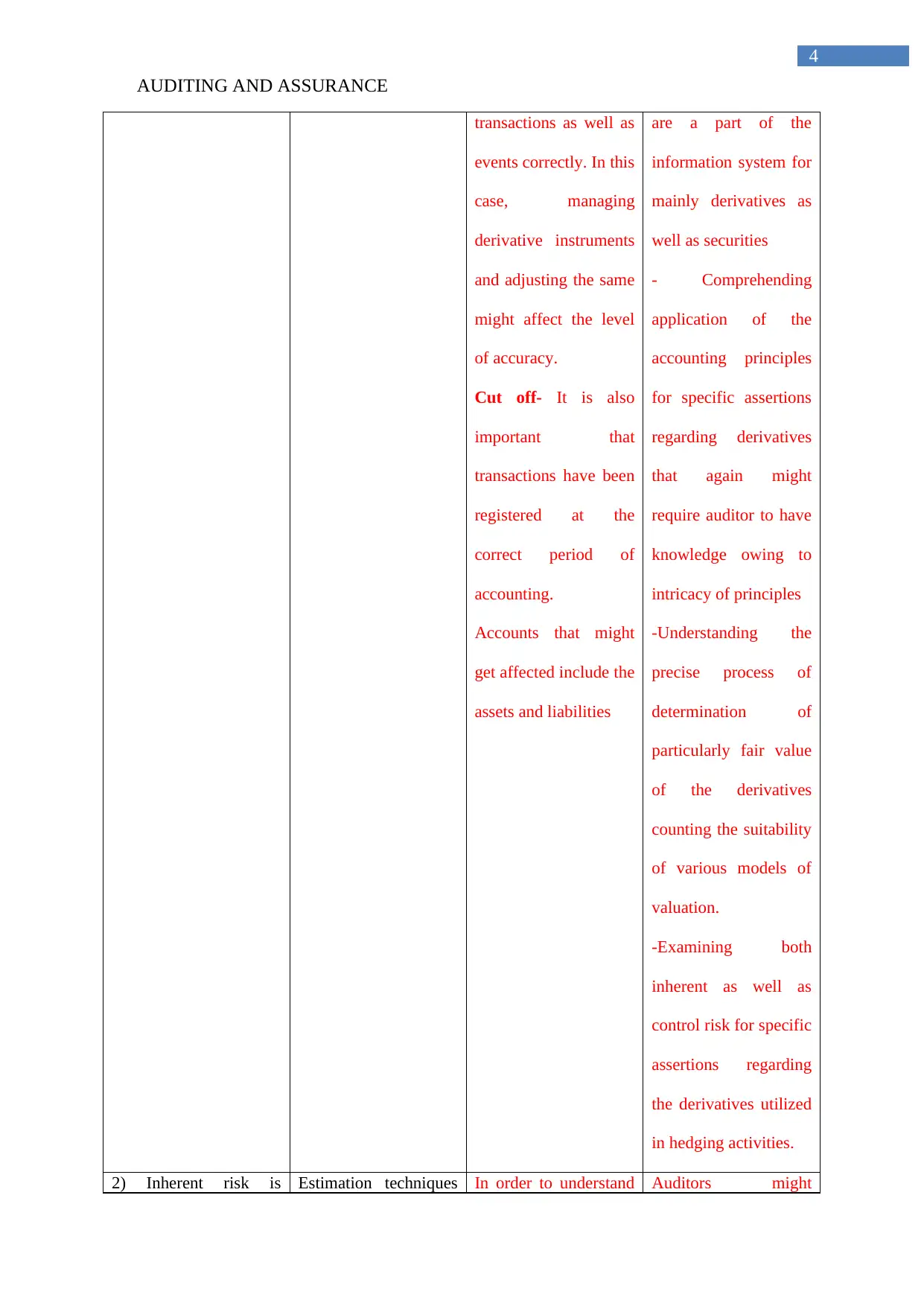

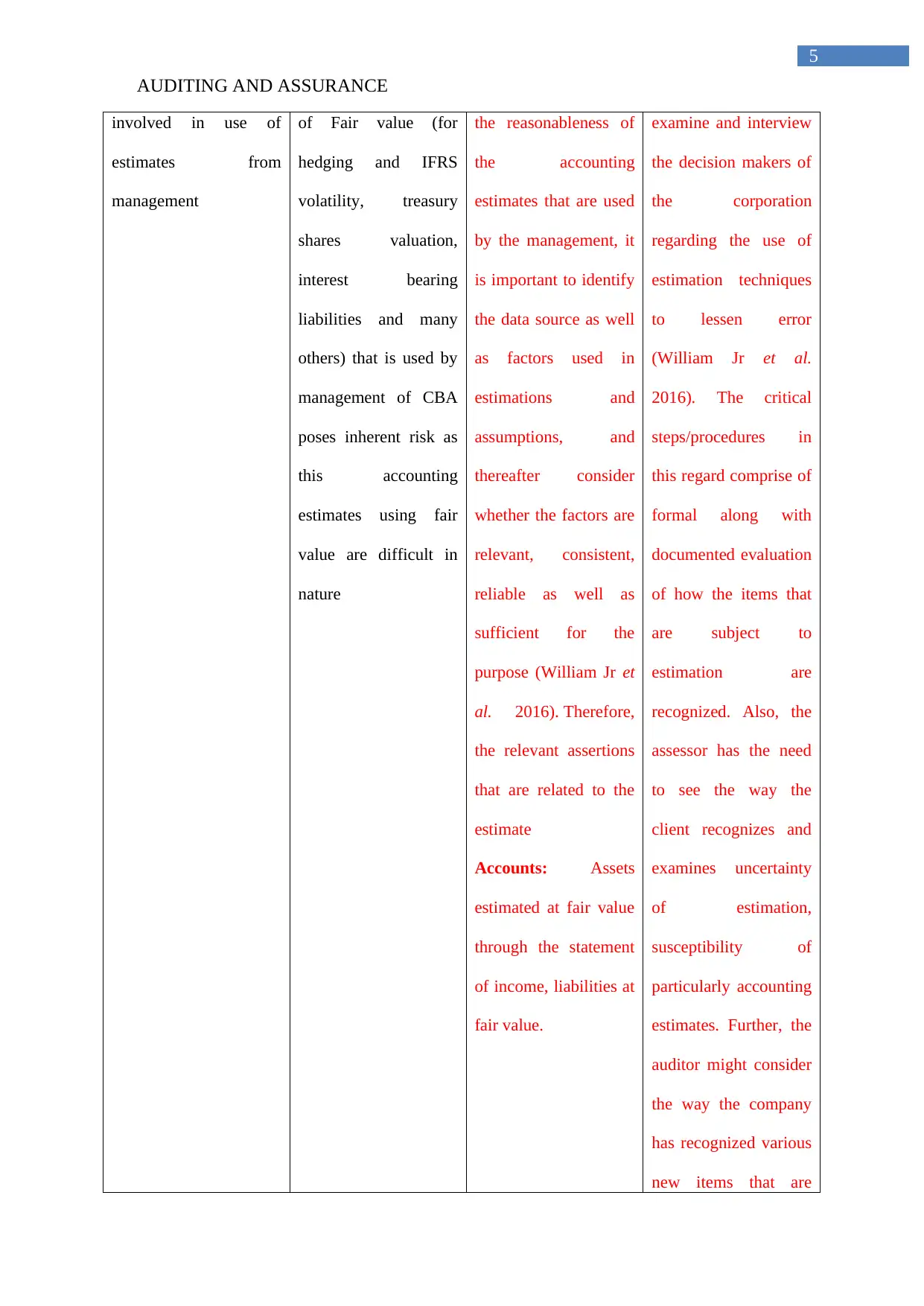

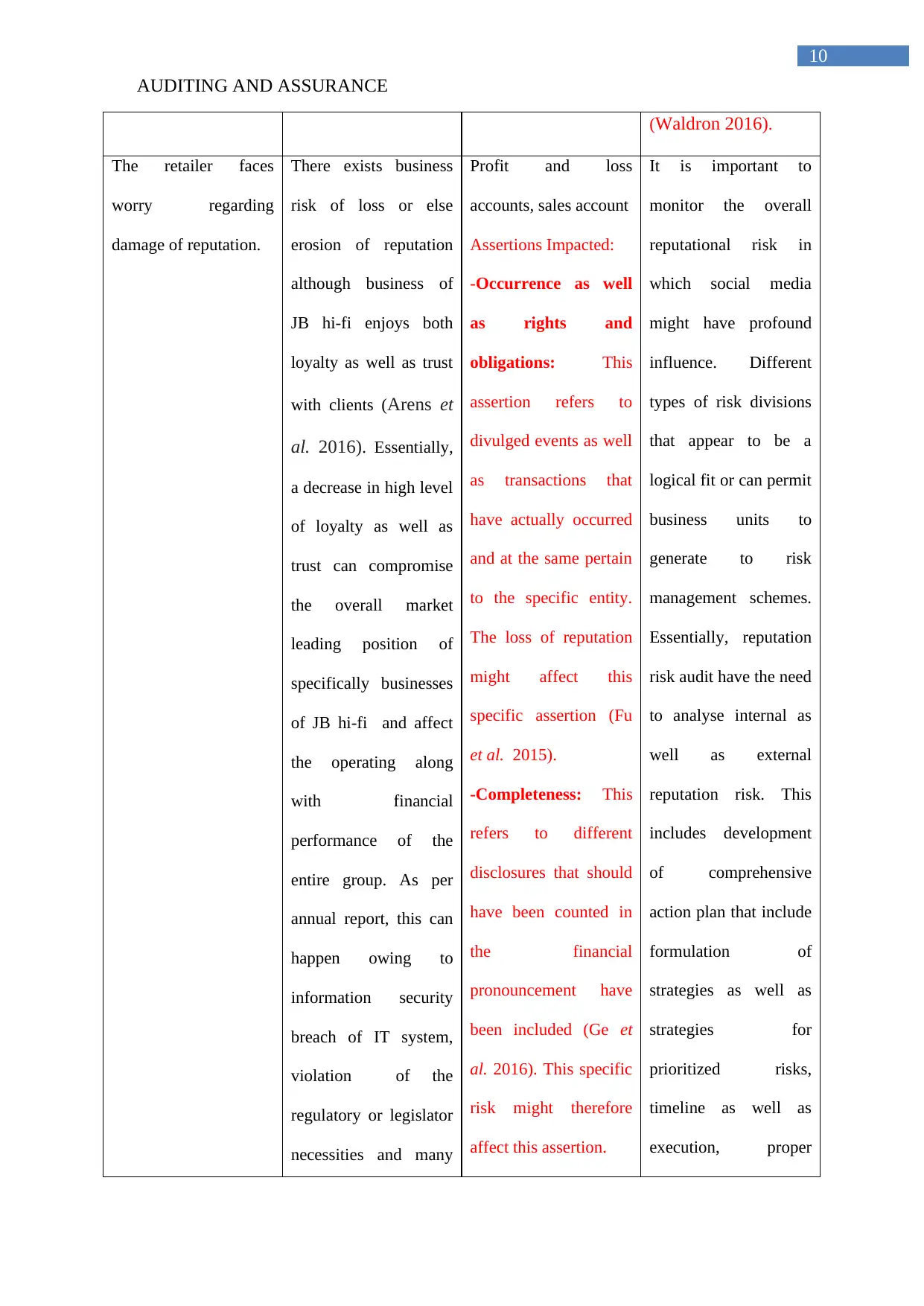

This assignment analyzes the inherent risks and audit procedures for two companies, CBA and JB hi-fi. For CBA, the assignment addresses risks related to derivative instruments, management estimates, and the relationship with auditors. It examines the impact on financial statement assertions like occurrence, completeness, accuracy, and cutoff, detailing specific audit procedures. For JB hi-fi, the assignment focuses on risks associated with increased competition, damage to reputation, and digital assets. It explores how these risks affect assertions such as occurrence, rights and obligations, and completeness, and outlines corresponding audit procedures. The solution includes justifications for inherent risks, affected assertions, and ledger accounts, along with detailed audit procedures for each identified risk. The assignment uses financial data and industry knowledge to provide a comprehensive analysis of the audit process.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.