Auditing and Assurance Assignment 1: Beta Limited Case Study

VerifiedAdded on 2023/06/04

|8

|2498

|326

Report

AI Summary

This assignment solution delves into various aspects of auditing and assurance, focusing on a case study involving Beta Limited. It analyzes audit risks associated with different scenarios, including product quality issues, segregation of duties, and employee theft. The report identifies material accounts affected and discusses the components of audit risk, particularly inherent and detection risks. Furthermore, it examines internal control weaknesses within the organization, proposes improvements, and evaluates the impact of these weaknesses on financial statement misstatements. The assignment also addresses the appropriate audit opinions to be issued under different circumstances, such as limitations in scope or going concern issues. Finally, it outlines the auditor's responsibilities regarding events occurring after the balance sheet date, including contract signings, patent applications, reported fraud, and accounts receivable collectability.

Auditing and

Assurance Assignment

Assurance Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Table of Contents

Background and Abstract............................................................................................................................3

Discussion and Analysis...............................................................................................................................3

Section A..................................................................................................................................................3

Section B..................................................................................................................................................5

Section C..................................................................................................................................................6

References...................................................................................................................................................7

2 | P a g e

Table of Contents

Background and Abstract............................................................................................................................3

Discussion and Analysis...............................................................................................................................3

Section A..................................................................................................................................................3

Section B..................................................................................................................................................5

Section C..................................................................................................................................................6

References...................................................................................................................................................7

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Background and Abstract

In the given assignment on audit and assurance, four individual case studies have been given on the

audit of the entity and what are risks encountered in the financials during the audit of an entity. The

requisite audit procedures to be employed in such a case has also been explained in detail. In Question

two of the assignment, the internal control weaknesses in the organization and how to correct and

improve them has been suggested. Section B of the assignment deals with the audit opinion and Section

C deals with the actions that the auditor would have taken in the different circumstances, which have

been given.

Discussion and Analysis

Section A

Question 1:

i. As per the three scenarios, which have been given for the company, Beta Limited. The

accounts which are likely to be affected materially and the components of audit risks that

are going to be affected have been mentioned below in the table:

Matter # Audit Risk Component(s) Account(s)

1 In the first case, the company is selling an inexpensive sandwich

maker which has a very low cost heating element and is the main

reason behind excessive heating of its parts due to which the

complaints of the products have increased by more than 4 times

from 3% of sales to 12% of sales. This affects one of the audit risk

components of inherent risk as it is quite evident that low price

goods will compromise on the quality (Bailey, Collins, & Abbott,

2017).

Sales

account,

debtors

accounts,

warranty

expenses

account,

inventory

account

2 In the given case, a newly graduated Roberta is being given

additional responsibilities which includes handling of customer

queries, creating the sales invoice in different currencies,

maintaining and adjustment of stock levels and recording of sales

in accounting books. This shows that there is overlapping of the

functions and the non-segregation of the duties might lead to

chances of material misstatement door to the failure of the control

as she is not well aware about the foreign exchange translation.

Sales

account,

foreign

exchange

translation

reserve,

inventory

account

3 In the given case, three employees of the company have been

terminated on account of theft who were from different

departments and stole the stock and sold it at lower prices. They

made false journal entries in the books to cover up for these illicit

activities. The CFO of the company believes that these were the

only three and this clearly points out the detection risk in the

organization as the auditor might miss out on finding the

misstatement in the company despite having sufficient internal

control within the organization (Kuhn & Morris, 2016).

Inventory

account,

sales and

purchases

accounts

3 | P a g e

Background and Abstract

In the given assignment on audit and assurance, four individual case studies have been given on the

audit of the entity and what are risks encountered in the financials during the audit of an entity. The

requisite audit procedures to be employed in such a case has also been explained in detail. In Question

two of the assignment, the internal control weaknesses in the organization and how to correct and

improve them has been suggested. Section B of the assignment deals with the audit opinion and Section

C deals with the actions that the auditor would have taken in the different circumstances, which have

been given.

Discussion and Analysis

Section A

Question 1:

i. As per the three scenarios, which have been given for the company, Beta Limited. The

accounts which are likely to be affected materially and the components of audit risks that

are going to be affected have been mentioned below in the table:

Matter # Audit Risk Component(s) Account(s)

1 In the first case, the company is selling an inexpensive sandwich

maker which has a very low cost heating element and is the main

reason behind excessive heating of its parts due to which the

complaints of the products have increased by more than 4 times

from 3% of sales to 12% of sales. This affects one of the audit risk

components of inherent risk as it is quite evident that low price

goods will compromise on the quality (Bailey, Collins, & Abbott,

2017).

Sales

account,

debtors

accounts,

warranty

expenses

account,

inventory

account

2 In the given case, a newly graduated Roberta is being given

additional responsibilities which includes handling of customer

queries, creating the sales invoice in different currencies,

maintaining and adjustment of stock levels and recording of sales

in accounting books. This shows that there is overlapping of the

functions and the non-segregation of the duties might lead to

chances of material misstatement door to the failure of the control

as she is not well aware about the foreign exchange translation.

Sales

account,

foreign

exchange

translation

reserve,

inventory

account

3 In the given case, three employees of the company have been

terminated on account of theft who were from different

departments and stole the stock and sold it at lower prices. They

made false journal entries in the books to cover up for these illicit

activities. The CFO of the company believes that these were the

only three and this clearly points out the detection risk in the

organization as the auditor might miss out on finding the

misstatement in the company despite having sufficient internal

control within the organization (Kuhn & Morris, 2016).

Inventory

account,

sales and

purchases

accounts

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

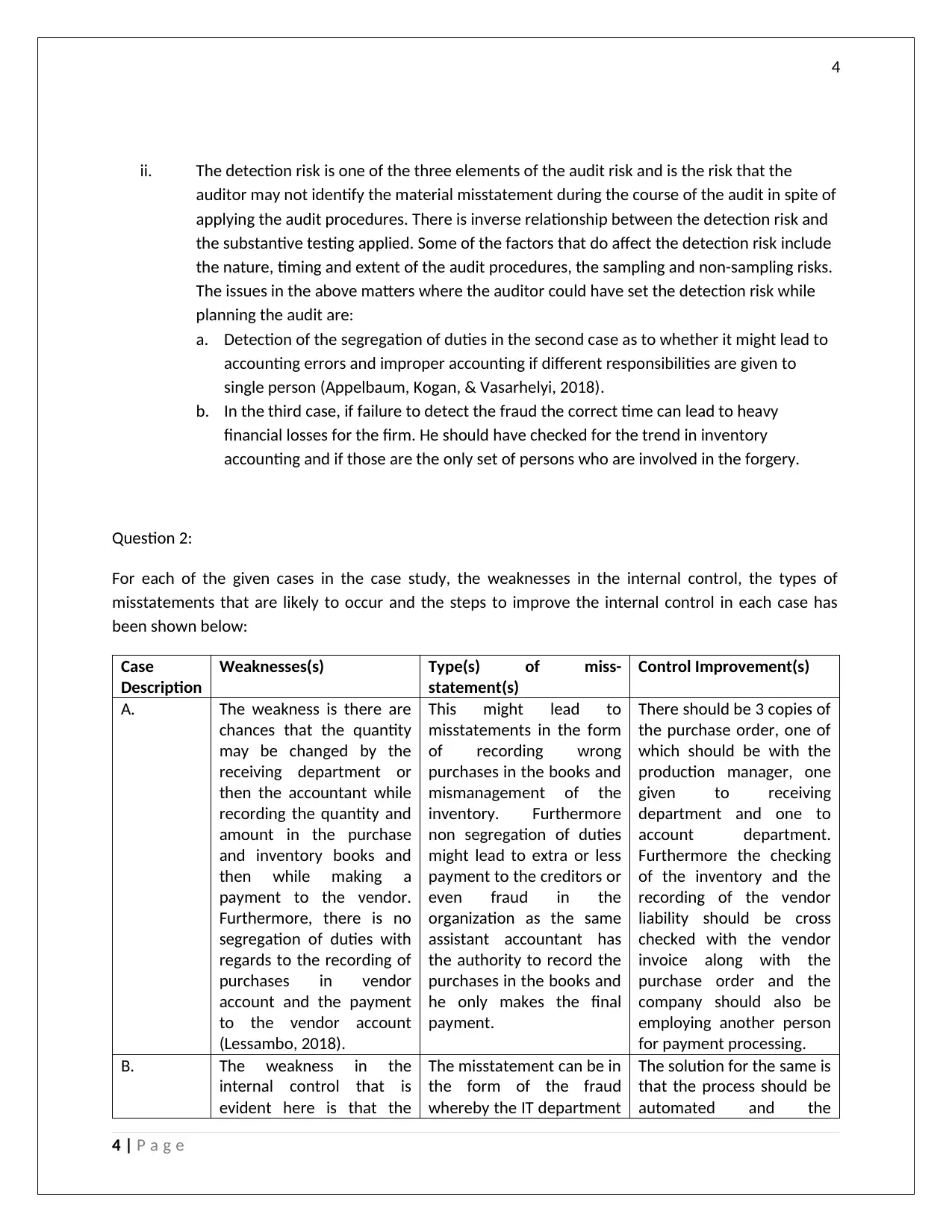

ii. The detection risk is one of the three elements of the audit risk and is the risk that the

auditor may not identify the material misstatement during the course of the audit in spite of

applying the audit procedures. There is inverse relationship between the detection risk and

the substantive testing applied. Some of the factors that do affect the detection risk include

the nature, timing and extent of the audit procedures, the sampling and non-sampling risks.

The issues in the above matters where the auditor could have set the detection risk while

planning the audit are:

a. Detection of the segregation of duties in the second case as to whether it might lead to

accounting errors and improper accounting if different responsibilities are given to

single person (Appelbaum, Kogan, & Vasarhelyi, 2018).

b. In the third case, if failure to detect the fraud the correct time can lead to heavy

financial losses for the firm. He should have checked for the trend in inventory

accounting and if those are the only set of persons who are involved in the forgery.

Question 2:

For each of the given cases in the case study, the weaknesses in the internal control, the types of

misstatements that are likely to occur and the steps to improve the internal control in each case has

been shown below:

Case

Description

Weaknesses(s) Type(s) of miss-

statement(s)

Control Improvement(s)

A. The weakness is there are

chances that the quantity

may be changed by the

receiving department or

then the accountant while

recording the quantity and

amount in the purchase

and inventory books and

then while making a

payment to the vendor.

Furthermore, there is no

segregation of duties with

regards to the recording of

purchases in vendor

account and the payment

to the vendor account

(Lessambo, 2018).

This might lead to

misstatements in the form

of recording wrong

purchases in the books and

mismanagement of the

inventory. Furthermore

non segregation of duties

might lead to extra or less

payment to the creditors or

even fraud in the

organization as the same

assistant accountant has

the authority to record the

purchases in the books and

he only makes the final

payment.

There should be 3 copies of

the purchase order, one of

which should be with the

production manager, one

given to receiving

department and one to

account department.

Furthermore the checking

of the inventory and the

recording of the vendor

liability should be cross

checked with the vendor

invoice along with the

purchase order and the

company should also be

employing another person

for payment processing.

B. The weakness in the

internal control that is

evident here is that the

The misstatement can be in

the form of the fraud

whereby the IT department

The solution for the same is

that the process should be

automated and the

4 | P a g e

ii. The detection risk is one of the three elements of the audit risk and is the risk that the

auditor may not identify the material misstatement during the course of the audit in spite of

applying the audit procedures. There is inverse relationship between the detection risk and

the substantive testing applied. Some of the factors that do affect the detection risk include

the nature, timing and extent of the audit procedures, the sampling and non-sampling risks.

The issues in the above matters where the auditor could have set the detection risk while

planning the audit are:

a. Detection of the segregation of duties in the second case as to whether it might lead to

accounting errors and improper accounting if different responsibilities are given to

single person (Appelbaum, Kogan, & Vasarhelyi, 2018).

b. In the third case, if failure to detect the fraud the correct time can lead to heavy

financial losses for the firm. He should have checked for the trend in inventory

accounting and if those are the only set of persons who are involved in the forgery.

Question 2:

For each of the given cases in the case study, the weaknesses in the internal control, the types of

misstatements that are likely to occur and the steps to improve the internal control in each case has

been shown below:

Case

Description

Weaknesses(s) Type(s) of miss-

statement(s)

Control Improvement(s)

A. The weakness is there are

chances that the quantity

may be changed by the

receiving department or

then the accountant while

recording the quantity and

amount in the purchase

and inventory books and

then while making a

payment to the vendor.

Furthermore, there is no

segregation of duties with

regards to the recording of

purchases in vendor

account and the payment

to the vendor account

(Lessambo, 2018).

This might lead to

misstatements in the form

of recording wrong

purchases in the books and

mismanagement of the

inventory. Furthermore

non segregation of duties

might lead to extra or less

payment to the creditors or

even fraud in the

organization as the same

assistant accountant has

the authority to record the

purchases in the books and

he only makes the final

payment.

There should be 3 copies of

the purchase order, one of

which should be with the

production manager, one

given to receiving

department and one to

account department.

Furthermore the checking

of the inventory and the

recording of the vendor

liability should be cross

checked with the vendor

invoice along with the

purchase order and the

company should also be

employing another person

for payment processing.

B. The weakness in the

internal control that is

evident here is that the

The misstatement can be in

the form of the fraud

whereby the IT department

The solution for the same is

that the process should be

automated and the

4 | P a g e

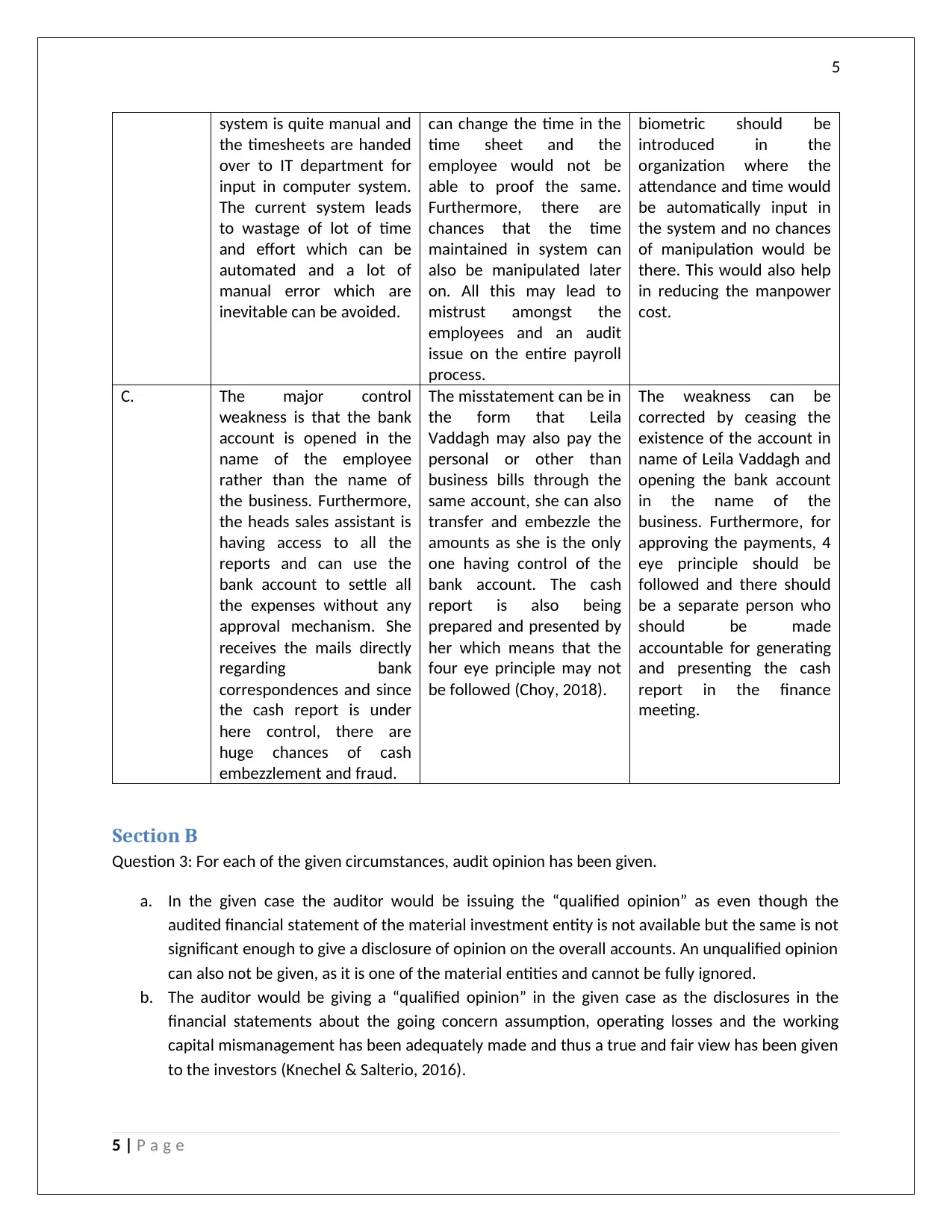

5

system is quite manual and

the timesheets are handed

over to IT department for

input in computer system.

The current system leads

to wastage of lot of time

and effort which can be

automated and a lot of

manual error which are

inevitable can be avoided.

can change the time in the

time sheet and the

employee would not be

able to proof the same.

Furthermore, there are

chances that the time

maintained in system can

also be manipulated later

on. All this may lead to

mistrust amongst the

employees and an audit

issue on the entire payroll

process.

biometric should be

introduced in the

organization where the

attendance and time would

be automatically input in

the system and no chances

of manipulation would be

there. This would also help

in reducing the manpower

cost.

C. The major control

weakness is that the bank

account is opened in the

name of the employee

rather than the name of

the business. Furthermore,

the heads sales assistant is

having access to all the

reports and can use the

bank account to settle all

the expenses without any

approval mechanism. She

receives the mails directly

regarding bank

correspondences and since

the cash report is under

here control, there are

huge chances of cash

embezzlement and fraud.

The misstatement can be in

the form that Leila

Vaddagh may also pay the

personal or other than

business bills through the

same account, she can also

transfer and embezzle the

amounts as she is the only

one having control of the

bank account. The cash

report is also being

prepared and presented by

her which means that the

four eye principle may not

be followed (Choy, 2018).

The weakness can be

corrected by ceasing the

existence of the account in

name of Leila Vaddagh and

opening the bank account

in the name of the

business. Furthermore, for

approving the payments, 4

eye principle should be

followed and there should

be a separate person who

should be made

accountable for generating

and presenting the cash

report in the finance

meeting.

Section B

Question 3: For each of the given circumstances, audit opinion has been given.

a. In the given case the auditor would be issuing the “qualified opinion” as even though the

audited financial statement of the material investment entity is not available but the same is not

significant enough to give a disclosure of opinion on the overall accounts. An unqualified opinion

can also not be given, as it is one of the material entities and cannot be fully ignored.

b. The auditor would be giving a “qualified opinion” in the given case as the disclosures in the

financial statements about the going concern assumption, operating losses and the working

capital mismanagement has been adequately made and thus a true and fair view has been given

to the investors (Knechel & Salterio, 2016).

5 | P a g e

system is quite manual and

the timesheets are handed

over to IT department for

input in computer system.

The current system leads

to wastage of lot of time

and effort which can be

automated and a lot of

manual error which are

inevitable can be avoided.

can change the time in the

time sheet and the

employee would not be

able to proof the same.

Furthermore, there are

chances that the time

maintained in system can

also be manipulated later

on. All this may lead to

mistrust amongst the

employees and an audit

issue on the entire payroll

process.

biometric should be

introduced in the

organization where the

attendance and time would

be automatically input in

the system and no chances

of manipulation would be

there. This would also help

in reducing the manpower

cost.

C. The major control

weakness is that the bank

account is opened in the

name of the employee

rather than the name of

the business. Furthermore,

the heads sales assistant is

having access to all the

reports and can use the

bank account to settle all

the expenses without any

approval mechanism. She

receives the mails directly

regarding bank

correspondences and since

the cash report is under

here control, there are

huge chances of cash

embezzlement and fraud.

The misstatement can be in

the form that Leila

Vaddagh may also pay the

personal or other than

business bills through the

same account, she can also

transfer and embezzle the

amounts as she is the only

one having control of the

bank account. The cash

report is also being

prepared and presented by

her which means that the

four eye principle may not

be followed (Choy, 2018).

The weakness can be

corrected by ceasing the

existence of the account in

name of Leila Vaddagh and

opening the bank account

in the name of the

business. Furthermore, for

approving the payments, 4

eye principle should be

followed and there should

be a separate person who

should be made

accountable for generating

and presenting the cash

report in the finance

meeting.

Section B

Question 3: For each of the given circumstances, audit opinion has been given.

a. In the given case the auditor would be issuing the “qualified opinion” as even though the

audited financial statement of the material investment entity is not available but the same is not

significant enough to give a disclosure of opinion on the overall accounts. An unqualified opinion

can also not be given, as it is one of the material entities and cannot be fully ignored.

b. The auditor would be giving a “qualified opinion” in the given case as the disclosures in the

financial statements about the going concern assumption, operating losses and the working

capital mismanagement has been adequately made and thus a true and fair view has been given

to the investors (Knechel & Salterio, 2016).

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

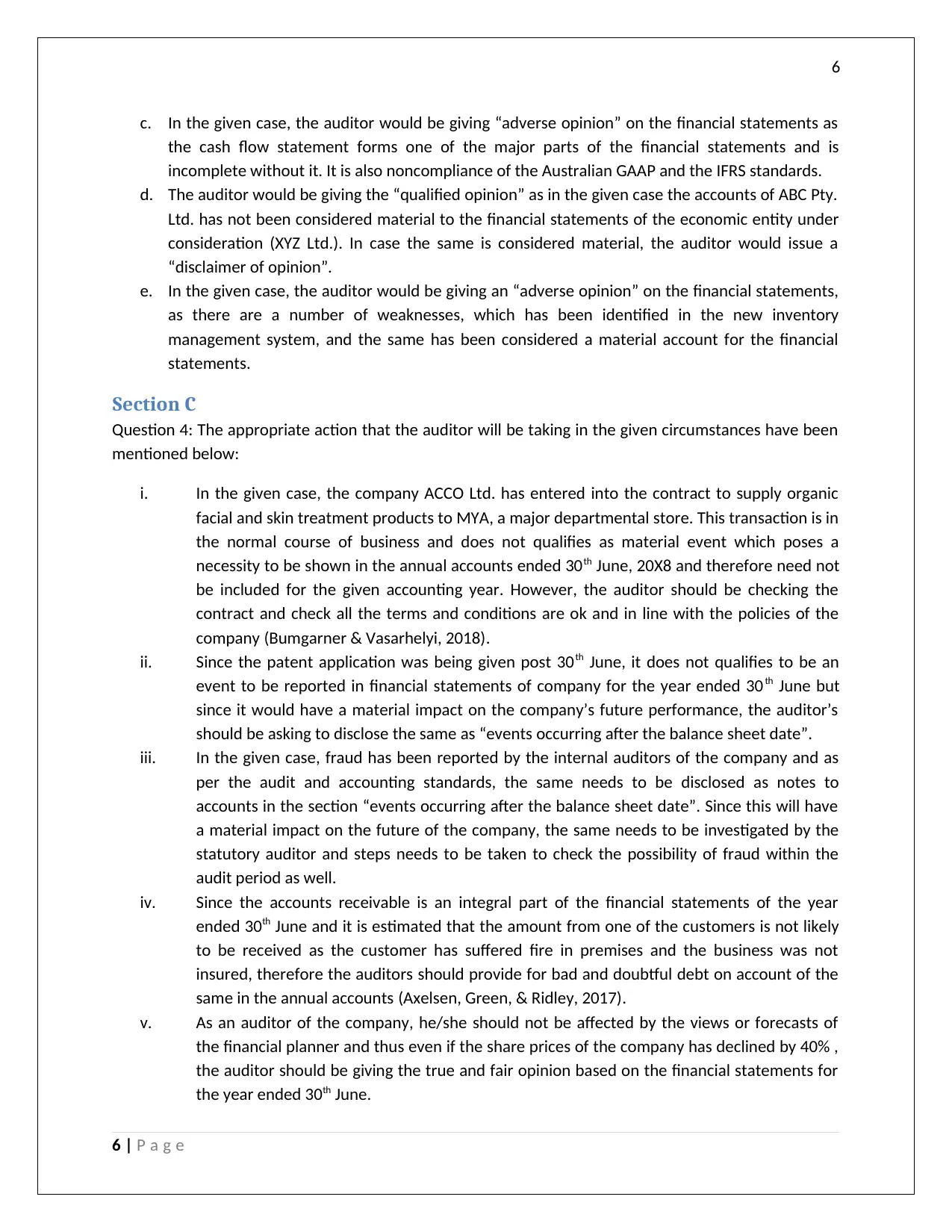

c. In the given case, the auditor would be giving “adverse opinion” on the financial statements as

the cash flow statement forms one of the major parts of the financial statements and is

incomplete without it. It is also noncompliance of the Australian GAAP and the IFRS standards.

d. The auditor would be giving the “qualified opinion” as in the given case the accounts of ABC Pty.

Ltd. has not been considered material to the financial statements of the economic entity under

consideration (XYZ Ltd.). In case the same is considered material, the auditor would issue a

“disclaimer of opinion”.

e. In the given case, the auditor would be giving an “adverse opinion” on the financial statements,

as there are a number of weaknesses, which has been identified in the new inventory

management system, and the same has been considered a material account for the financial

statements.

Section C

Question 4: The appropriate action that the auditor will be taking in the given circumstances have been

mentioned below:

i. In the given case, the company ACCO Ltd. has entered into the contract to supply organic

facial and skin treatment products to MYA, a major departmental store. This transaction is in

the normal course of business and does not qualifies as material event which poses a

necessity to be shown in the annual accounts ended 30th June, 20X8 and therefore need not

be included for the given accounting year. However, the auditor should be checking the

contract and check all the terms and conditions are ok and in line with the policies of the

company (Bumgarner & Vasarhelyi, 2018).

ii. Since the patent application was being given post 30th June, it does not qualifies to be an

event to be reported in financial statements of company for the year ended 30 th June but

since it would have a material impact on the company’s future performance, the auditor’s

should be asking to disclose the same as “events occurring after the balance sheet date”.

iii. In the given case, fraud has been reported by the internal auditors of the company and as

per the audit and accounting standards, the same needs to be disclosed as notes to

accounts in the section “events occurring after the balance sheet date”. Since this will have

a material impact on the future of the company, the same needs to be investigated by the

statutory auditor and steps needs to be taken to check the possibility of fraud within the

audit period as well.

iv. Since the accounts receivable is an integral part of the financial statements of the year

ended 30th June and it is estimated that the amount from one of the customers is not likely

to be received as the customer has suffered fire in premises and the business was not

insured, therefore the auditors should provide for bad and doubtful debt on account of the

same in the annual accounts (Axelsen, Green, & Ridley, 2017).

v. As an auditor of the company, he/she should not be affected by the views or forecasts of

the financial planner and thus even if the share prices of the company has declined by 40% ,

the auditor should be giving the true and fair opinion based on the financial statements for

the year ended 30th June.

6 | P a g e

c. In the given case, the auditor would be giving “adverse opinion” on the financial statements as

the cash flow statement forms one of the major parts of the financial statements and is

incomplete without it. It is also noncompliance of the Australian GAAP and the IFRS standards.

d. The auditor would be giving the “qualified opinion” as in the given case the accounts of ABC Pty.

Ltd. has not been considered material to the financial statements of the economic entity under

consideration (XYZ Ltd.). In case the same is considered material, the auditor would issue a

“disclaimer of opinion”.

e. In the given case, the auditor would be giving an “adverse opinion” on the financial statements,

as there are a number of weaknesses, which has been identified in the new inventory

management system, and the same has been considered a material account for the financial

statements.

Section C

Question 4: The appropriate action that the auditor will be taking in the given circumstances have been

mentioned below:

i. In the given case, the company ACCO Ltd. has entered into the contract to supply organic

facial and skin treatment products to MYA, a major departmental store. This transaction is in

the normal course of business and does not qualifies as material event which poses a

necessity to be shown in the annual accounts ended 30th June, 20X8 and therefore need not

be included for the given accounting year. However, the auditor should be checking the

contract and check all the terms and conditions are ok and in line with the policies of the

company (Bumgarner & Vasarhelyi, 2018).

ii. Since the patent application was being given post 30th June, it does not qualifies to be an

event to be reported in financial statements of company for the year ended 30 th June but

since it would have a material impact on the company’s future performance, the auditor’s

should be asking to disclose the same as “events occurring after the balance sheet date”.

iii. In the given case, fraud has been reported by the internal auditors of the company and as

per the audit and accounting standards, the same needs to be disclosed as notes to

accounts in the section “events occurring after the balance sheet date”. Since this will have

a material impact on the future of the company, the same needs to be investigated by the

statutory auditor and steps needs to be taken to check the possibility of fraud within the

audit period as well.

iv. Since the accounts receivable is an integral part of the financial statements of the year

ended 30th June and it is estimated that the amount from one of the customers is not likely

to be received as the customer has suffered fire in premises and the business was not

insured, therefore the auditors should provide for bad and doubtful debt on account of the

same in the annual accounts (Axelsen, Green, & Ridley, 2017).

v. As an auditor of the company, he/she should not be affected by the views or forecasts of

the financial planner and thus even if the share prices of the company has declined by 40% ,

the auditor should be giving the true and fair opinion based on the financial statements for

the year ended 30th June.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

References

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Axelsen, M., Green, P., & Ridley, G. (2017). Explaining the information systems auditor role in the public

sector financial audit. International Journal of Accounting Information Systems, 24(1), 15-31.

Bailey, C., Collins, D., & Abbott, L. (2017). The Impact of Enterprise Risk Management on the Audit

Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of Practice & Theory,

37(3), 25-46.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

7 | P a g e

References

Appelbaum, D., Kogan, A., & Vasarhelyi, M. (2018). Analytical procedures in external auditing: A

comprehensive literature survey and framework for external audit analytics. . Journal of

Accounting Literature, 40(1), 83-101.

Axelsen, M., Green, P., & Ridley, G. (2017). Explaining the information systems auditor role in the public

sector financial audit. International Journal of Accounting Information Systems, 24(1), 15-31.

Bailey, C., Collins, D., & Abbott, L. (2017). The Impact of Enterprise Risk Management on the Audit

Process: Evidence from Audit Fees and Audit Delay. Auditing: A Journal of Practice & Theory,

37(3), 25-46.

Bumgarner, N., & Vasarhelyi, M. (2018). Continuous auditing—a new view. Continuous Auditing: Theory

and Application, 20(1), 7-51.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Knechel, W., & Salterio, S. (2016). Auditing:Assurance and Risk (fourth ed.). New York: Routledge.

Kuhn, J., & Morris, B. (2016). IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

7 | P a g e

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.