Auditing and Assurance: BHP Billiton's Annual Report Executive Summary

VerifiedAdded on 2021/01/02

|13

|3687

|480

Report

AI Summary

This report provides an executive summary of an audit, assurance, and compliance analysis, using BHP Billiton's annual report as a case study. The report begins with an overview of BHP Billiton and then delves into key aspects of the audit process, including auditor independence declarations, non-audit services, and auditor remuneration. It examines the role, functions, and composition of the audit committee, including its responsibilities in overseeing financial statements and risk management. The report also details the audit opinion provided by KPMG UK, the key audit matters identified, such as asset valuation, and the procedures undertaken to assess these matters. Furthermore, it explores the responsibilities of directors, managers, and auditors, the assessment of material information, and follow-up questions from the auditor in the annual general meeting. Overall, the report offers a comprehensive understanding of the auditing process and its application within a large organization.

AUDITING

ASSURANCE AND

COMPLAINCE

ASSURANCE AND

COMPLAINCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This project summarises concept of audit, assurance and compliance. In this present

assignment, BHP Billiton's annual report will be assessed for present a proper understanding on

the auditing process. Numerous core audit matters has been evaluated in this paper with audit

committee suggestions in order to prepare an audit report of organisation and analyse it

accordingly.

This project summarises concept of audit, assurance and compliance. In this present

assignment, BHP Billiton's annual report will be assessed for present a proper understanding on

the auditing process. Numerous core audit matters has been evaluated in this paper with audit

committee suggestions in order to prepare an audit report of organisation and analyse it

accordingly.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

Overview of the company......................................................................................................1

Auditor's independence declaration........................................................................................1

Non audit services formed by the auditor...............................................................................2

Auditor's remuneration...........................................................................................................3

Role, functions and composition of the audit committee.......................................................4

Audit Opinion.........................................................................................................................5

Key Audit Matters..................................................................................................................5

Responsibilities of Director, manager and auditor.................................................................8

Assessment of the effectiveness of the material information reported by the auditor...........9

Follow up questions from auditor in AGM............................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................1

Overview of the company......................................................................................................1

Auditor's independence declaration........................................................................................1

Non audit services formed by the auditor...............................................................................2

Auditor's remuneration...........................................................................................................3

Role, functions and composition of the audit committee.......................................................4

Audit Opinion.........................................................................................................................5

Key Audit Matters..................................................................................................................5

Responsibilities of Director, manager and auditor.................................................................8

Assessment of the effectiveness of the material information reported by the auditor...........9

Follow up questions from auditor in AGM............................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Audit refers to the process of analysing annual reports, accounts, vouchers of a business

enterprise to analyse that the financial and non-financial statements shows the actual position of

the company or not (what is auditing, 2017). The auditor is liable to check the annual reports

physically and give his opinion on those reports. The main reason behind audit is to ensure that

the transactions recorded in financial statements are fair or not, and is there any

misrepresentation in the reports. Auditor is the person who is appointed by the executives of an

organisation and responsible to analyse annual reports of a company and then prepare a report

which is based on his opinion. The company chosen for this report is BHP Billiton Ltd, which is

a metals and mining company.

This project report is based on auditor's independence declaration and his report, non-

audit services performed by the auditor, auditor's remuneration, audit committee and its roles

function and composition, independent auditor's report to the shareholders and key audit matters

associated and noted in audit procedure.

Overview of the company

BHP Billiton Ltd is a global resources company, which is a producer of different

commodities like iron ore, uranium, copper, metallurgical coal etc. It has four segments that are

copper, coal, petroleum and iron ore (Mills, 2012). These segments are occupied by different

production such as coal involves mining of metallurgical coal and thermal energy, copper

segment is engaged with excavation of silver, lead, zinc, gold, copper uranium etc., the

petroleum segment is concerned with development, exploration of oil and gas. The product

distribution of the company is managed through global logistic chain of the organisation. The

products are sold by the organisation through supply agreements with its clients. It has three

outlets, Minerals Australia, Minerals America and Petroleum and Marketing.

Auditor's independence declaration

Auditor's independence: It refers to the independence of internal as well as external

auditors from the parties who may have financial involvement in the business which is going to

be audited by the auditor. It requires honesty and a neutral formulation to the audit procedure.

The auditor of the company is liable to present actual and original information to the

1

Audit refers to the process of analysing annual reports, accounts, vouchers of a business

enterprise to analyse that the financial and non-financial statements shows the actual position of

the company or not (what is auditing, 2017). The auditor is liable to check the annual reports

physically and give his opinion on those reports. The main reason behind audit is to ensure that

the transactions recorded in financial statements are fair or not, and is there any

misrepresentation in the reports. Auditor is the person who is appointed by the executives of an

organisation and responsible to analyse annual reports of a company and then prepare a report

which is based on his opinion. The company chosen for this report is BHP Billiton Ltd, which is

a metals and mining company.

This project report is based on auditor's independence declaration and his report, non-

audit services performed by the auditor, auditor's remuneration, audit committee and its roles

function and composition, independent auditor's report to the shareholders and key audit matters

associated and noted in audit procedure.

Overview of the company

BHP Billiton Ltd is a global resources company, which is a producer of different

commodities like iron ore, uranium, copper, metallurgical coal etc. It has four segments that are

copper, coal, petroleum and iron ore (Mills, 2012). These segments are occupied by different

production such as coal involves mining of metallurgical coal and thermal energy, copper

segment is engaged with excavation of silver, lead, zinc, gold, copper uranium etc., the

petroleum segment is concerned with development, exploration of oil and gas. The product

distribution of the company is managed through global logistic chain of the organisation. The

products are sold by the organisation through supply agreements with its clients. It has three

outlets, Minerals Australia, Minerals America and Petroleum and Marketing.

Auditor's independence declaration

Auditor's independence: It refers to the independence of internal as well as external

auditors from the parties who may have financial involvement in the business which is going to

be audited by the auditor. It requires honesty and a neutral formulation to the audit procedure.

The auditor of the company is liable to present actual and original information to the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shareholders (Ryan and et. al., 2012). Following is the declaration that has been made by the

auditor:

No contraventions of the auditor independence requirements as set out in the Australian

Corporations Act 2001 in relation to the audit.

No contraventions of any applicable code of professional conduct in relation to the audit.

There are two auditors who have hired by the company they are KPMG and Anthony Young.

Both the auditors have made a declaration under section 307 c of the Australian Corporations act

2001, that consist above mentioned points.

The auditors are complied with the independence requirements because both of them declared

and signed an agreement under section 307 c of the Australian Corporations act 2001.

Non audit services formed by the auditor

Non audit services: It includes such services that are not involved in the audit process of

the company's financial statements. For example, tax planning, business consulting, system

integration etc.

All non-audit services are sanctioned in conformity with the procedure which have been

set out in the argumentation on condition of audit and other services by extrinsic auditor of BHP

Billiton Ltd. There are no non audit services were found out that were generally eliminated by

the logical argument on provision of audit and other non-audit services. Based on advice

provided by the risk and audit committee, it was formed by the directors that provision for non-

audit services are compatible or not with special regulation of independence for auditors. It was

also identified that nature of non-audit services will never affect the independence of auditors

(Prempeh, Twumasi and Kyeremeh, 2015). The external auditor does provide some non-audit

services. These services can be undertaken by the auditor with the prior approval of the RAC, but

the other services are not undertaken. These services are required to the external auditor to audit

his own work, to participate in the activities that are normally directed by the owner of the

company to act in the advocacy role of BHP Billiton Ltd. Although, the outside auditor does

convey certain non-audit services. the objectively and independence of external auditors are

defence by restriction on the overall provision of below mentioned services. Those services are:

Auditor may need to audit their own work.

In some situation, auditors can also take participation in various activities that would be

basically undertaken by the management.

2

auditor:

No contraventions of the auditor independence requirements as set out in the Australian

Corporations Act 2001 in relation to the audit.

No contraventions of any applicable code of professional conduct in relation to the audit.

There are two auditors who have hired by the company they are KPMG and Anthony Young.

Both the auditors have made a declaration under section 307 c of the Australian Corporations act

2001, that consist above mentioned points.

The auditors are complied with the independence requirements because both of them declared

and signed an agreement under section 307 c of the Australian Corporations act 2001.

Non audit services formed by the auditor

Non audit services: It includes such services that are not involved in the audit process of

the company's financial statements. For example, tax planning, business consulting, system

integration etc.

All non-audit services are sanctioned in conformity with the procedure which have been

set out in the argumentation on condition of audit and other services by extrinsic auditor of BHP

Billiton Ltd. There are no non audit services were found out that were generally eliminated by

the logical argument on provision of audit and other non-audit services. Based on advice

provided by the risk and audit committee, it was formed by the directors that provision for non-

audit services are compatible or not with special regulation of independence for auditors. It was

also identified that nature of non-audit services will never affect the independence of auditors

(Prempeh, Twumasi and Kyeremeh, 2015). The external auditor does provide some non-audit

services. These services can be undertaken by the auditor with the prior approval of the RAC, but

the other services are not undertaken. These services are required to the external auditor to audit

his own work, to participate in the activities that are normally directed by the owner of the

company to act in the advocacy role of BHP Billiton Ltd. Although, the outside auditor does

convey certain non-audit services. the objectively and independence of external auditors are

defence by restriction on the overall provision of below mentioned services. Those services are:

Auditor may need to audit their own work.

In some situation, auditors can also take participation in various activities that would be

basically undertaken by the management.

2

Auditor remunerated by a success fee structure that is design by the BHP Billiton.

Acts in an advocacy role for the BHP company.

The RAC has adopted an effective policy that is entitled with the specific provision of

audit and external services that is being done by the auditors of BHP.

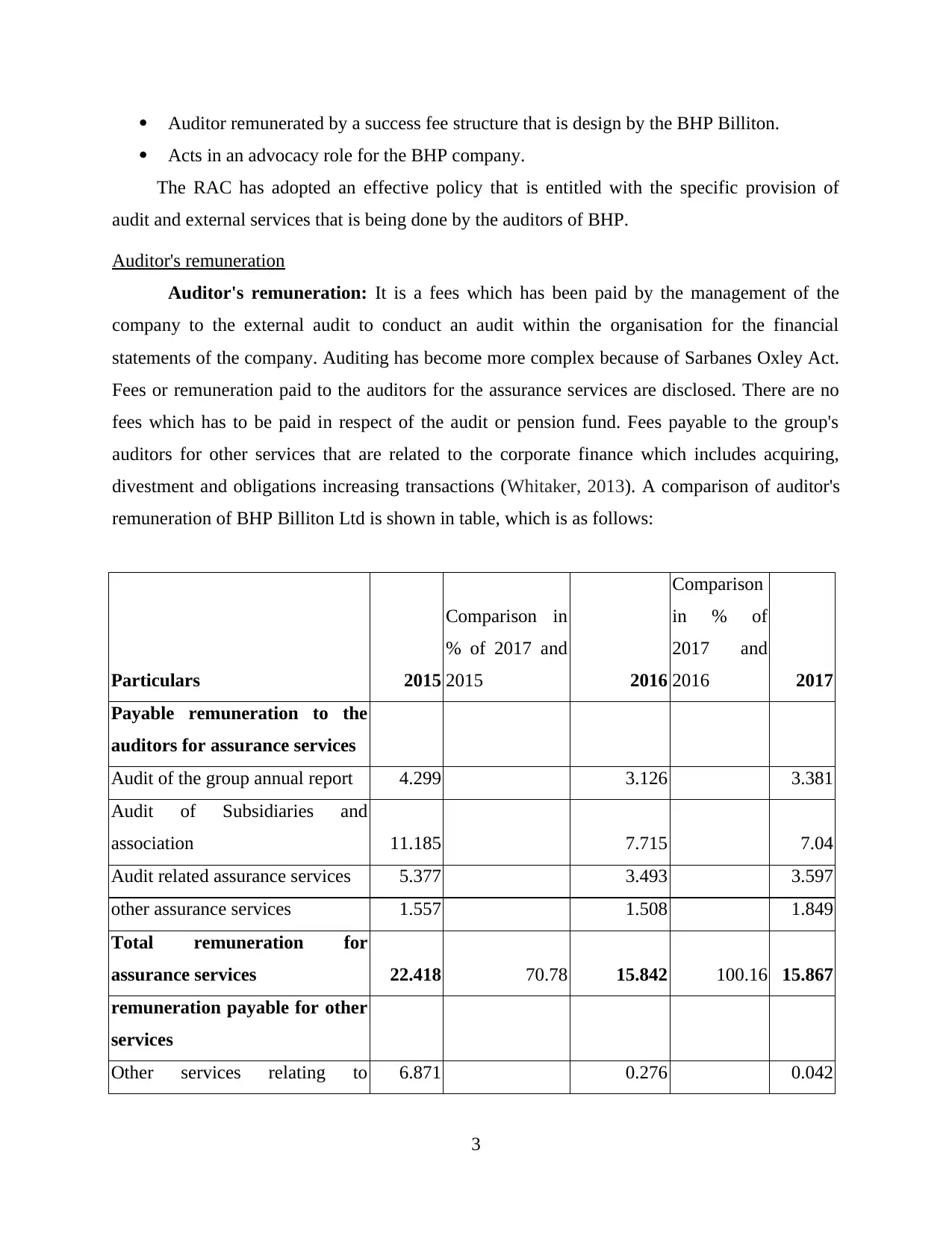

Auditor's remuneration

Auditor's remuneration: It is a fees which has been paid by the management of the

company to the external audit to conduct an audit within the organisation for the financial

statements of the company. Auditing has become more complex because of Sarbanes Oxley Act.

Fees or remuneration paid to the auditors for the assurance services are disclosed. There are no

fees which has to be paid in respect of the audit or pension fund. Fees payable to the group's

auditors for other services that are related to the corporate finance which includes acquiring,

divestment and obligations increasing transactions (Whitaker, 2013). A comparison of auditor's

remuneration of BHP Billiton Ltd is shown in table, which is as follows:

Particulars 2015

Comparison in

% of 2017 and

2015 2016

Comparison

in % of

2017 and

2016 2017

Payable remuneration to the

auditors for assurance services

Audit of the group annual report 4.299 3.126 3.381

Audit of Subsidiaries and

association 11.185 7.715 7.04

Audit related assurance services 5.377 3.493 3.597

other assurance services 1.557 1.508 1.849

Total remuneration for

assurance services 22.418 70.78 15.842 100.16 15.867

remuneration payable for other

services

Other services relating to 6.871 0.276 0.042

3

Acts in an advocacy role for the BHP company.

The RAC has adopted an effective policy that is entitled with the specific provision of

audit and external services that is being done by the auditors of BHP.

Auditor's remuneration

Auditor's remuneration: It is a fees which has been paid by the management of the

company to the external audit to conduct an audit within the organisation for the financial

statements of the company. Auditing has become more complex because of Sarbanes Oxley Act.

Fees or remuneration paid to the auditors for the assurance services are disclosed. There are no

fees which has to be paid in respect of the audit or pension fund. Fees payable to the group's

auditors for other services that are related to the corporate finance which includes acquiring,

divestment and obligations increasing transactions (Whitaker, 2013). A comparison of auditor's

remuneration of BHP Billiton Ltd is shown in table, which is as follows:

Particulars 2015

Comparison in

% of 2017 and

2015 2016

Comparison

in % of

2017 and

2016 2017

Payable remuneration to the

auditors for assurance services

Audit of the group annual report 4.299 3.126 3.381

Audit of Subsidiaries and

association 11.185 7.715 7.04

Audit related assurance services 5.377 3.493 3.597

other assurance services 1.557 1.508 1.849

Total remuneration for

assurance services 22.418 70.78 15.842 100.16 15.867

remuneration payable for other

services

Other services relating to 6.871 0.276 0.042

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corporate finance

All other services 1.093 0.815 0.589

Total other services 7.964 7.92 1.091 57.84 0.631

Total remuneration 30.382 54.30 16.933 97.43 16.498

From the above table it has been analysed that when total remunerations for assured services of

2017 compared with 2016 than the percentage changes were 100.16% and when it was compared

to 2015 the changing percentage was 70.78%. Percentage changed in total other services while

comparing with 2016 is 1.091% and for 2015 it was 7.92%. When total remuneration of 2017

was compared to 2016 the total percentage changed was 97.43% and when it was compared to

2015 the percentage changed was 54.30%.

Role, functions and composition of the audit committee

Audit committee: Audit committee is a group is persons who are liable to keep a track

record of all financial activities of the company (Knechel, and Salterio, 2016). All the companies

are directed to form an audit committee to control the activities within the organisation. The

members are selected from the board of directors of the company and they may take help of

other auditors to analyse the truthfulness of the transactions of the company.

There is also an audit committee in BHP Billiton Ltd to analyse the transparency of the financial

statements. There are four different non-executive directors in audit committee and all the

members are independent and three of them have full attendance. The members are Mindsey

Maxsted who is chairman of the company and member for whole life, Malcolm Broomhead, he

is member for whole life, Anita Frew, who is member for whole life and her attendance is 11 out

of 12, Wayne Murdy who is a member of the organisation for whole life (Fiolleau, and et. al.,

2013).

Role, functions and responsibilities of audit committee:

Audit committee is liable to oversee the transparency of financial statements and annual

reports of BHP Billiton Ltd.

To analyse the performance, appointment and remuneration of external auditors and the

audit process of the company.

To judge the effectiveness of the risk management system of the company.

To control the internal environment.

4

All other services 1.093 0.815 0.589

Total other services 7.964 7.92 1.091 57.84 0.631

Total remuneration 30.382 54.30 16.933 97.43 16.498

From the above table it has been analysed that when total remunerations for assured services of

2017 compared with 2016 than the percentage changes were 100.16% and when it was compared

to 2015 the changing percentage was 70.78%. Percentage changed in total other services while

comparing with 2016 is 1.091% and for 2015 it was 7.92%. When total remuneration of 2017

was compared to 2016 the total percentage changed was 97.43% and when it was compared to

2015 the percentage changed was 54.30%.

Role, functions and composition of the audit committee

Audit committee: Audit committee is a group is persons who are liable to keep a track

record of all financial activities of the company (Knechel, and Salterio, 2016). All the companies

are directed to form an audit committee to control the activities within the organisation. The

members are selected from the board of directors of the company and they may take help of

other auditors to analyse the truthfulness of the transactions of the company.

There is also an audit committee in BHP Billiton Ltd to analyse the transparency of the financial

statements. There are four different non-executive directors in audit committee and all the

members are independent and three of them have full attendance. The members are Mindsey

Maxsted who is chairman of the company and member for whole life, Malcolm Broomhead, he

is member for whole life, Anita Frew, who is member for whole life and her attendance is 11 out

of 12, Wayne Murdy who is a member of the organisation for whole life (Fiolleau, and et. al.,

2013).

Role, functions and responsibilities of audit committee:

Audit committee is liable to oversee the transparency of financial statements and annual

reports of BHP Billiton Ltd.

To analyse the performance, appointment and remuneration of external auditors and the

audit process of the company.

To judge the effectiveness of the risk management system of the company.

To control the internal environment.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

To examine the plans, objectives and leadership of the internal audit process and check

its liableness.

To handle capital managements and other matters of the company.

Audit Opinion

The auditor of BHP Billiton Ltd who is KPMG UK has given following opinions on the

annual reports of the organisation:

According to KPMG the financial statements of the company shows the fair and true

transactions for the year ended 30 June 2017.

The managers of the company have properly prepared consolidated balance sheet as well

as income statements of the organisation.

The financial statements are properly prepared according to the accounting standard of

UK.

The annual reports of the company are generated according to the UK's Companies Act

2006.

Key Audit Matters

Key audit matters covers those matters, that are mainly based on the professional

judgement of the auditor, it includes the most significant assessed risks of material. It consists

the material information which is required to analyse the actual performance of the company

(Tepalagul and Lin, 2015). Few of the key audit matters that are identified in BHP Billiton Ltd.

are defined below:

Asset valuation: The carrying value of the group's functions of possession has been

wedged by continuous excitability in commodity prices. The key area of the judgement is related

to the assessment of the company of future cash flow for every cash creating unit, that is used to

analyse the redeemable value of the property. The future cash flows help to determine the future

events where cash is required. Assets valuation is the key matter for the company because of the

judgement which has been applied by auditors when examining the redeemable values of the

assets.

Procedure:

Investigating the central activities over the evaluation of the assets or the property of the

company. It includes evaluation and control of to identify the material weakness.

5

its liableness.

To handle capital managements and other matters of the company.

Audit Opinion

The auditor of BHP Billiton Ltd who is KPMG UK has given following opinions on the

annual reports of the organisation:

According to KPMG the financial statements of the company shows the fair and true

transactions for the year ended 30 June 2017.

The managers of the company have properly prepared consolidated balance sheet as well

as income statements of the organisation.

The financial statements are properly prepared according to the accounting standard of

UK.

The annual reports of the company are generated according to the UK's Companies Act

2006.

Key Audit Matters

Key audit matters covers those matters, that are mainly based on the professional

judgement of the auditor, it includes the most significant assessed risks of material. It consists

the material information which is required to analyse the actual performance of the company

(Tepalagul and Lin, 2015). Few of the key audit matters that are identified in BHP Billiton Ltd.

are defined below:

Asset valuation: The carrying value of the group's functions of possession has been

wedged by continuous excitability in commodity prices. The key area of the judgement is related

to the assessment of the company of future cash flow for every cash creating unit, that is used to

analyse the redeemable value of the property. The future cash flows help to determine the future

events where cash is required. Assets valuation is the key matter for the company because of the

judgement which has been applied by auditors when examining the redeemable values of the

assets.

Procedure:

Investigating the central activities over the evaluation of the assets or the property of the

company. It includes evaluation and control of to identify the material weakness.

5

Examining the predicted commodity prices integrated into the asset's modification testing

considering comparison to accessible market data.

Comparison of the future capital expenditures and reserves to the actual or current plans.

Evaluating the competency and objectivity of experienced persons who have forecasted

the reserves that are used in the valuation and based on the experience and qualification

of experts.

Working with the experts to compare the assumptions that are commodity prices,

inflation rate or discount rates.

Conducting a sensitivity analysis which is based on the assumptions of the specialists.

Evaluation of potential financial implications to control the deficiencies of the

organisation.

Analysing the impacts of the alteration in the evaluation of those properties on the

transfer value of investment.

Taxation: The company has operation in multiple countries, and every country has its

own taxation rules and regulations. It affects the taxation policy of the company and also trigger

various taxation obligations. It includes corporate tax, royalties and other sources. The nature of

the company which is cross border also affects the international transfer pricing of the company

(Ng, Chong and Ismail, 2012). Taxation is a key matter because of the different regulation

authorities of various countries in which the company is running its business.

Procedure:

Testing the main points that are related to the accounting for the uncovering of the

taxation related transactions of BHP Billiton Ltd.

Work with the different taxation authorities of different countries like Australia, Chile,

US etc. to evaluate the exact taxation liability of the company for the year ending 30 June

2017. It also involves the documentation of from recent similar tax rulings to evaluate the

completeness of taxation matters.

Analysing the uniformity of various assumptions that are used in the contamination of

different provisions and uncertain liabilities for key taxation disclosure.

Evaluate the adequacy of the company's presentation which is related to the tax and its

ongoing matters.

6

considering comparison to accessible market data.

Comparison of the future capital expenditures and reserves to the actual or current plans.

Evaluating the competency and objectivity of experienced persons who have forecasted

the reserves that are used in the valuation and based on the experience and qualification

of experts.

Working with the experts to compare the assumptions that are commodity prices,

inflation rate or discount rates.

Conducting a sensitivity analysis which is based on the assumptions of the specialists.

Evaluation of potential financial implications to control the deficiencies of the

organisation.

Analysing the impacts of the alteration in the evaluation of those properties on the

transfer value of investment.

Taxation: The company has operation in multiple countries, and every country has its

own taxation rules and regulations. It affects the taxation policy of the company and also trigger

various taxation obligations. It includes corporate tax, royalties and other sources. The nature of

the company which is cross border also affects the international transfer pricing of the company

(Ng, Chong and Ismail, 2012). Taxation is a key matter because of the different regulation

authorities of various countries in which the company is running its business.

Procedure:

Testing the main points that are related to the accounting for the uncovering of the

taxation related transactions of BHP Billiton Ltd.

Work with the different taxation authorities of different countries like Australia, Chile,

US etc. to evaluate the exact taxation liability of the company for the year ending 30 June

2017. It also involves the documentation of from recent similar tax rulings to evaluate the

completeness of taxation matters.

Analysing the uniformity of various assumptions that are used in the contamination of

different provisions and uncertain liabilities for key taxation disclosure.

Evaluate the adequacy of the company's presentation which is related to the tax and its

ongoing matters.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Samarco: There are various accounting judgements that are complex and results as a

failure of the Samarco Dam, it includes:

estimating the legal status of claims made against Samarco and BHP Billiton Ltd. and the

suitable accounting treatment for the same.

Estimating the magnitude of BHP Billiton Ltd.’s legal obligations to provide monetary

sources to Samarco.

Revelation of different liabilities that are related to various claims and different events

that shows the aspect of Samarco and BHP Billiton Ltd.

Procedure:

analysing the key control system over accounting and exposure that are related to the dam

failure.

Analysing the presence of legal or constructive rules under the Samarco Stakeholder's

agreement and determining Brazilian legal interference.

Examining the main assumptions that are used to analyse the provisions which are

recorded by BHP Billiton Ltd. in relation to its possible funding causes. It has been

assessed that the events described in the framework statement and compared the same to

the cash flow estimation of the company.

Directing the auditors of Samarco and analysing the outcome of the process which is

undertaken in relation to the causes that are required under framework and other

statements.

Assessing that the disclosure of the liabilities is complete and relevant or not. It is

possible with the help of legal and other documents that are presented by the external

auditor.

Analysing the discloser of the group of the company whether it is significantly following

legal obligations or not.

Closure and rehabilitation provisions: It has been provided that to run the operations

successfully the company has to follow the legal obligations to close, restore and rehabilitate its

different outlets. Closure and rehabilitations events are controlled by legal authority and other

legislations (Greiner, Kohlbeck and Smith, 2013). The calculation of different closers and other

provisions require significant judgement due to the complexness in the estimation of future costs.

7

failure of the Samarco Dam, it includes:

estimating the legal status of claims made against Samarco and BHP Billiton Ltd. and the

suitable accounting treatment for the same.

Estimating the magnitude of BHP Billiton Ltd.’s legal obligations to provide monetary

sources to Samarco.

Revelation of different liabilities that are related to various claims and different events

that shows the aspect of Samarco and BHP Billiton Ltd.

Procedure:

analysing the key control system over accounting and exposure that are related to the dam

failure.

Analysing the presence of legal or constructive rules under the Samarco Stakeholder's

agreement and determining Brazilian legal interference.

Examining the main assumptions that are used to analyse the provisions which are

recorded by BHP Billiton Ltd. in relation to its possible funding causes. It has been

assessed that the events described in the framework statement and compared the same to

the cash flow estimation of the company.

Directing the auditors of Samarco and analysing the outcome of the process which is

undertaken in relation to the causes that are required under framework and other

statements.

Assessing that the disclosure of the liabilities is complete and relevant or not. It is

possible with the help of legal and other documents that are presented by the external

auditor.

Analysing the discloser of the group of the company whether it is significantly following

legal obligations or not.

Closure and rehabilitation provisions: It has been provided that to run the operations

successfully the company has to follow the legal obligations to close, restore and rehabilitate its

different outlets. Closure and rehabilitations events are controlled by legal authority and other

legislations (Greiner, Kohlbeck and Smith, 2013). The calculation of different closers and other

provisions require significant judgement due to the complexness in the estimation of future costs.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It was a key audit matter due to the momentous size which is related to the company's financial

position.

Procedure:

Analysing the key controls of closure and different rehabilitation provisions.

Employing with the experts to assess the reasons of estimation of the mining process and

reserves used by BHP Billiton Ltd.

Analysing the activities of the company's hired experts to identify rehabilitation activities

against legislative activities. It is mainly based on the qualification, experience and

working style of the company.

Evaluating the main economic estimation that are used in the calculation of important

closure and other provisions and it also include the discount rates that are applied to

calculate the net present value of the company and help to identify the risks.

Material subsequent events and missing material information: According to the annual

reports of BHP Billiton Ltd. for the year ending 30 June 2017, there are no material subsequent

events and missing material information that are found by the auditor of the company.

Responsibilities of Director, manager and auditor

Director of the company is liable to direct the managers and auditors for their duties.

Director of BHP Billiton Ltd. Is the person who has all the powers of the company and have

rights to ask about any information from the auditor and managers. The mangers of the company

are liable to manage the activities that happen in and out of the organisation. The auditor

analyses the annual reports that are generated by the managers (Nicolăescu, 2013).

The auditor of BHP Billiton Ltd. Examine the financial statements of the organisation

and find out that the transactions that are recorded are relevant or not is there any missing

information which needs to be recorded in the financial reports. If the auditor finds any

misrepresentation in the annual reports than he may give the information to the director and then

the director is liable to take the action. In such way the roles of auditor, director and managers

differ from each other (Sarkar and Sarkar, 2012).

Assessment of the effectiveness of the material information reported by the auditor

As a stakeholder such as investor or debtor, effectiveness of the material information

reported by auditor is most important. For example, the most important information for these

stakeholders is debt equity position and profitability position of an organisation.

8

position.

Procedure:

Analysing the key controls of closure and different rehabilitation provisions.

Employing with the experts to assess the reasons of estimation of the mining process and

reserves used by BHP Billiton Ltd.

Analysing the activities of the company's hired experts to identify rehabilitation activities

against legislative activities. It is mainly based on the qualification, experience and

working style of the company.

Evaluating the main economic estimation that are used in the calculation of important

closure and other provisions and it also include the discount rates that are applied to

calculate the net present value of the company and help to identify the risks.

Material subsequent events and missing material information: According to the annual

reports of BHP Billiton Ltd. for the year ending 30 June 2017, there are no material subsequent

events and missing material information that are found by the auditor of the company.

Responsibilities of Director, manager and auditor

Director of the company is liable to direct the managers and auditors for their duties.

Director of BHP Billiton Ltd. Is the person who has all the powers of the company and have

rights to ask about any information from the auditor and managers. The mangers of the company

are liable to manage the activities that happen in and out of the organisation. The auditor

analyses the annual reports that are generated by the managers (Nicolăescu, 2013).

The auditor of BHP Billiton Ltd. Examine the financial statements of the organisation

and find out that the transactions that are recorded are relevant or not is there any missing

information which needs to be recorded in the financial reports. If the auditor finds any

misrepresentation in the annual reports than he may give the information to the director and then

the director is liable to take the action. In such way the roles of auditor, director and managers

differ from each other (Sarkar and Sarkar, 2012).

Assessment of the effectiveness of the material information reported by the auditor

As a stakeholder such as investor or debtor, effectiveness of the material information

reported by auditor is most important. For example, the most important information for these

stakeholders is debt equity position and profitability position of an organisation.

8

Follow up questions from auditor in AGM

Q1. Do the information which is recorded in the annual reports of BHP Billiton Ltd. Was

relevant or not?

Q2. whether the procedure of calling AGM is followed properly or not?

Q3. Whether the conceptual framework of financial reporting is followed by the company or

not?

Q4. Do the organisation have followed all the accounting standards while recording transactions

in financial reports?

CONCLUSION

From the above project report it has been concluded that in order to enhance the auditing,

assurance and complains company need to analyse various financial statements those are

evaluated by the auditor. In order to analysis the performance of the company and enhance the

auditing assurance key audit matters and its procedures has been clearly provided in context to

the company. However, to get more reliable results in near future all the essential requirements

which are mentioned in the annual report of the company in context to the auditor is being

analyse effectively.

9

Q1. Do the information which is recorded in the annual reports of BHP Billiton Ltd. Was

relevant or not?

Q2. whether the procedure of calling AGM is followed properly or not?

Q3. Whether the conceptual framework of financial reporting is followed by the company or

not?

Q4. Do the organisation have followed all the accounting standards while recording transactions

in financial reports?

CONCLUSION

From the above project report it has been concluded that in order to enhance the auditing,

assurance and complains company need to analyse various financial statements those are

evaluated by the auditor. In order to analysis the performance of the company and enhance the

auditing assurance key audit matters and its procedures has been clearly provided in context to

the company. However, to get more reliable results in near future all the essential requirements

which are mentioned in the annual report of the company in context to the auditor is being

analyse effectively.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.