Auditing and Assurance in Australia: SBF's Bletchington Audit Report

VerifiedAdded on 2022/10/10

|7

|1363

|60

Report

AI Summary

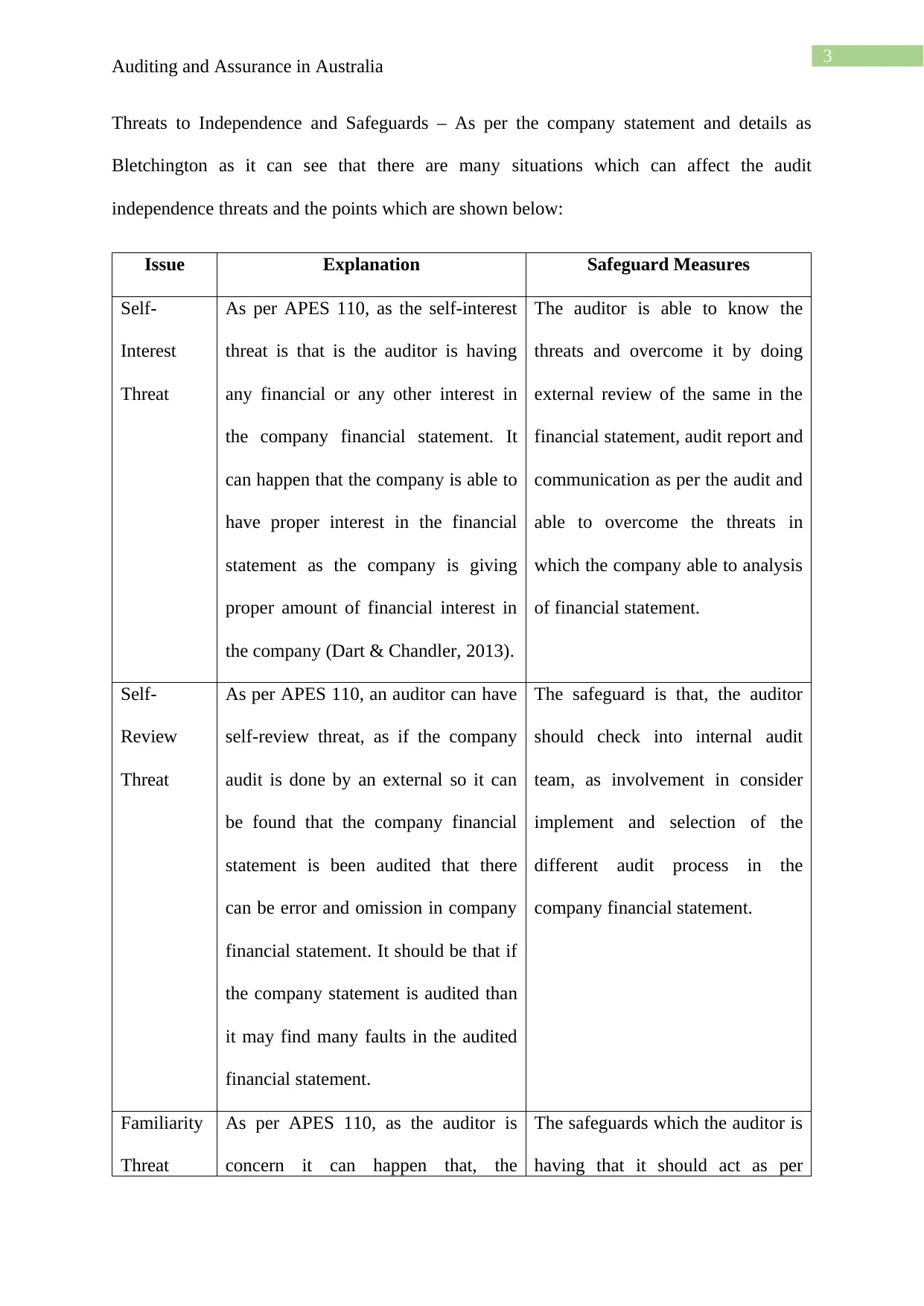

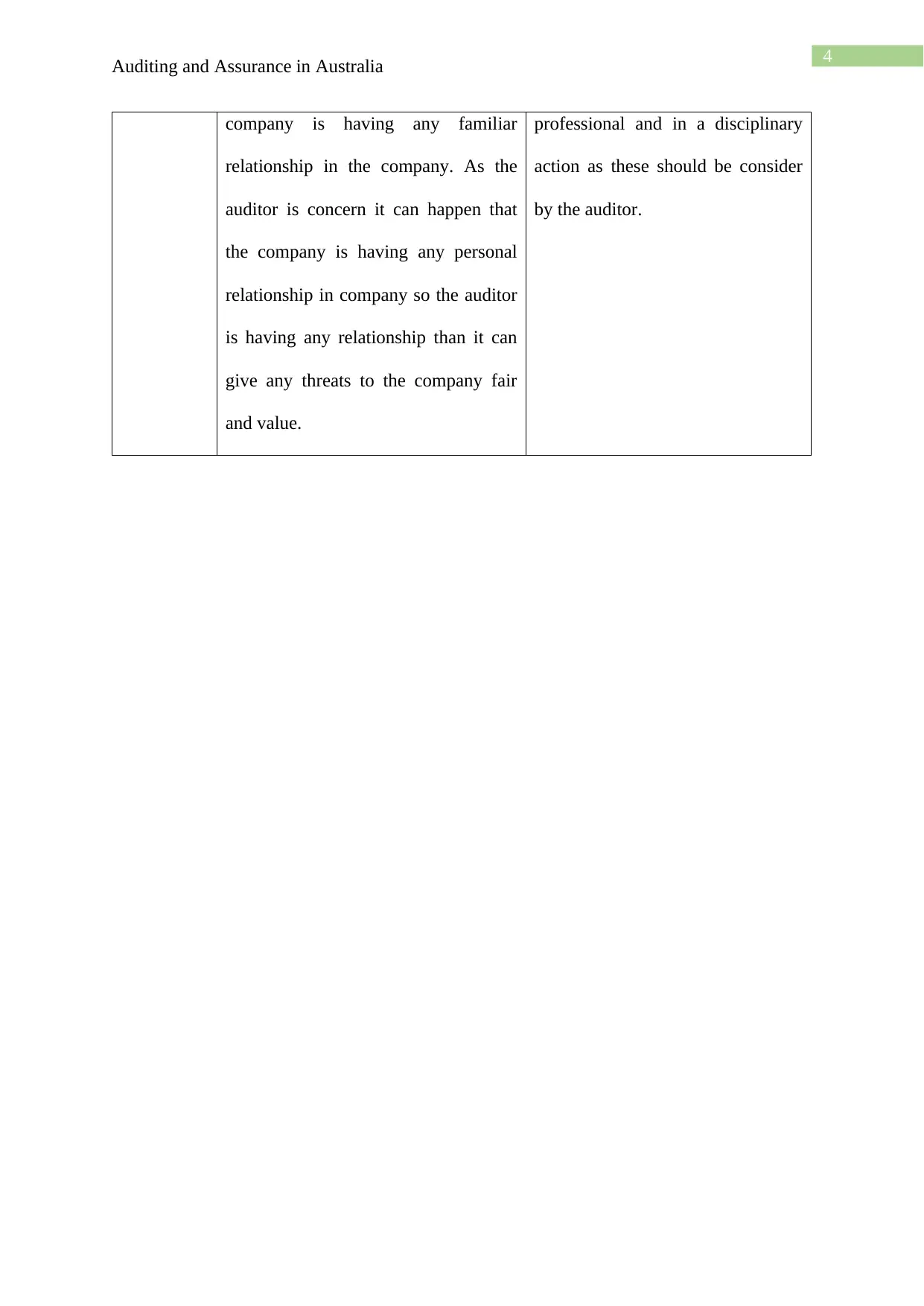

This report, prepared by an audit manager at Samway Baker Fitzgerald (SBF), examines the audit of Bletchington Limited, a defense industry manufacturing company. The report addresses the audit expectation gap, highlighting the difference between auditor assurance and user expectations, particularly given Bletchington's dealings with government contracts and international trade. It identifies potential issues in the audit process and the auditor's ability to meet user expectations. Furthermore, the report analyzes threats to audit independence, including self-interest, self-review, and familiarity threats, as per APES 110. For each threat, the report outlines potential safeguard measures. The analysis considers Bletchington's unique business context, including its reliance on competitive government tenders and sensitive product designs, to provide a comprehensive assessment of audit risks and mitigation strategies. The report concludes with a discussion on how these factors influence the audit process and the auditor's responsibility to maintain independence and provide reliable financial reporting.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.