ACCT3000 Case Study: Auditing and Assurance - Independence and Ethics

VerifiedAdded on 2023/04/08

|6

|1021

|260

Case Study

AI Summary

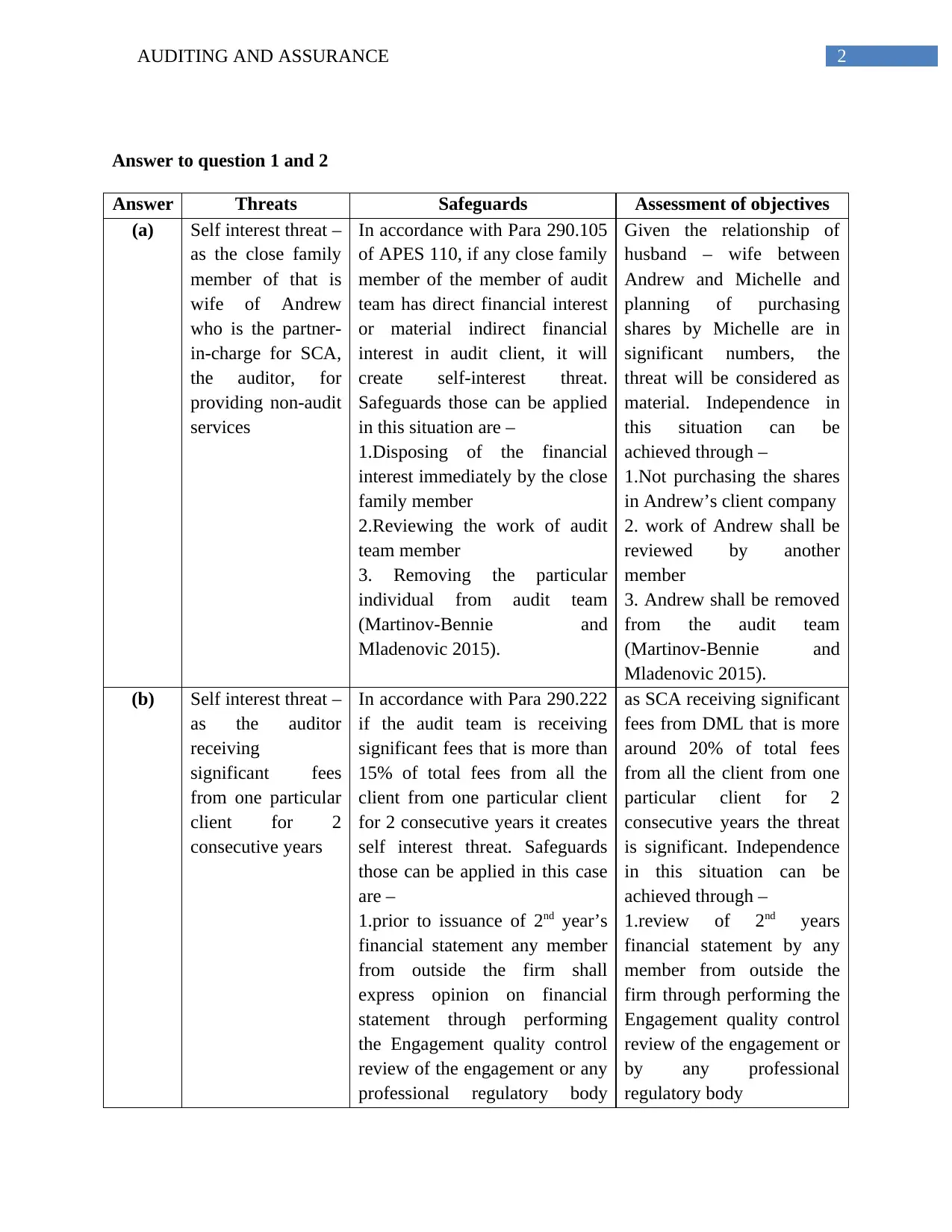

This case study analyzes five scenarios related to auditing and assurance, focusing on the application of APES 110 (Code of Ethics for Professional Accountants). The scenarios involve potential threats to auditor independence, including self-interest and familiarity threats, arising from family relationships, significant fees, unpaid fees, and the involvement of family members in client financial reporting. For each situation, the document identifies the specific threats, proposes relevant safeguards to mitigate these threats, and provides an objective assessment of the materiality of the threats. The case study emphasizes the importance of maintaining auditor independence to ensure the reliability and integrity of financial statements. The analysis considers the potential impact of various factors on independence and suggests appropriate actions to address these concerns, such as removing individuals from audit teams or implementing engagement quality control reviews. The document concludes by referencing relevant academic literature to support its findings.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.