Auditing and Assurance Report: Case Study Analysis, Trimester 3 2019

VerifiedAdded on 2022/11/07

|8

|1301

|347

Report

AI Summary

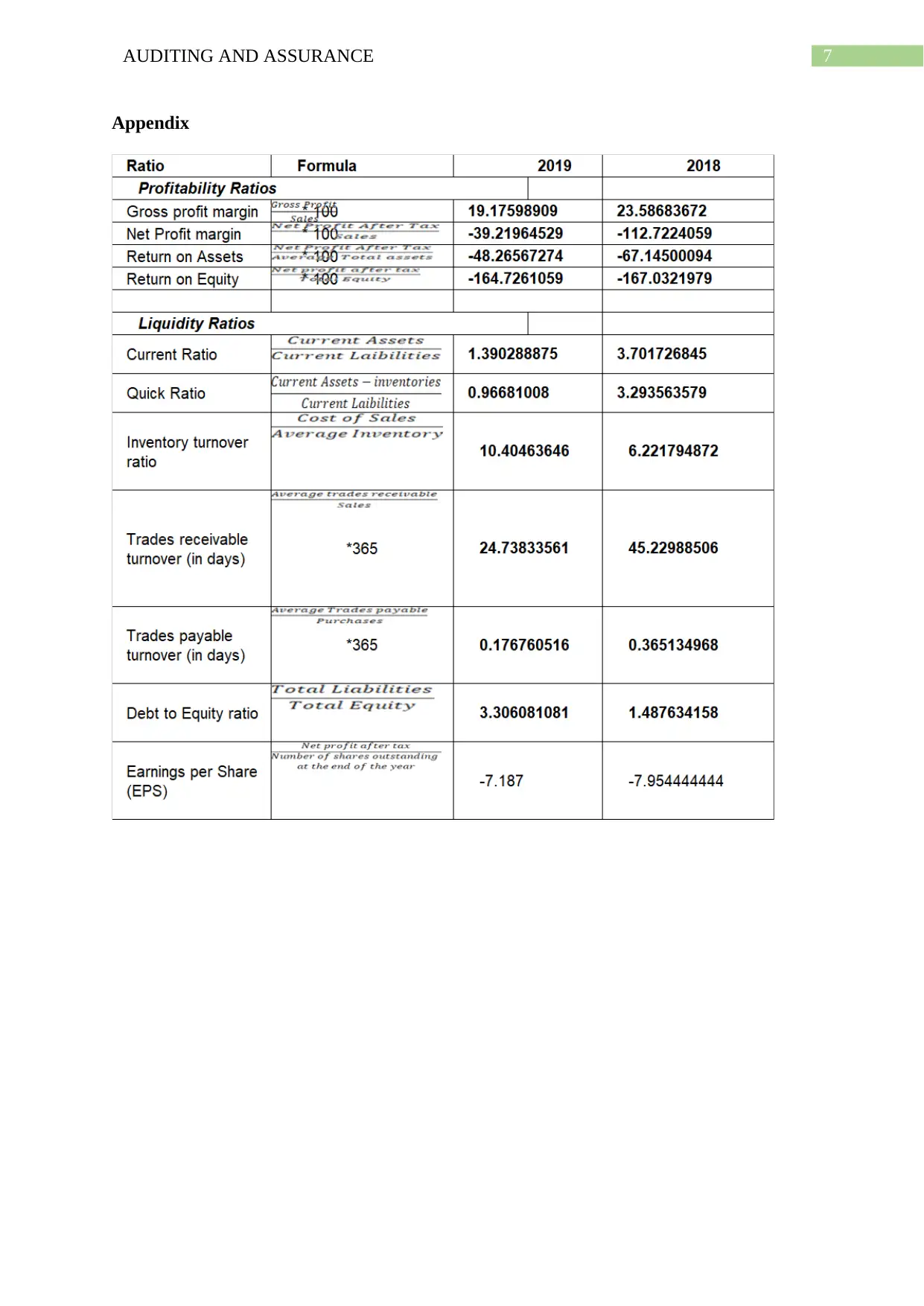

This report on Auditing and Assurance provides a comprehensive analysis of key auditing concepts. It begins by defining and explaining the importance of analytical procedures in risk assessment, referencing ASA315 and highlighting their role in identifying potential misstatements. The report then delves into professional skepticism, emphasizing its crucial role in effective audits, especially in the context of PCAOB standards. It discusses how professional skepticism influences audit procedures and judgments. The report then moves on to the calculation of planning materiality and tolerable misstatement based on provided financial data. Finally, the report analyzes financial ratios, including profitability, liquidity, turnover, and leverage ratios, to assess the financial health of a company and identify areas requiring special audit attention, such as cash and sales revenues. The report concludes by outlining specific areas that demand heightened scrutiny during the audit process.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.