Auditing and Assurance Report: C&B Partners' DecaSport Audit Analysis

VerifiedAdded on 2022/12/14

|11

|1853

|433

Report

AI Summary

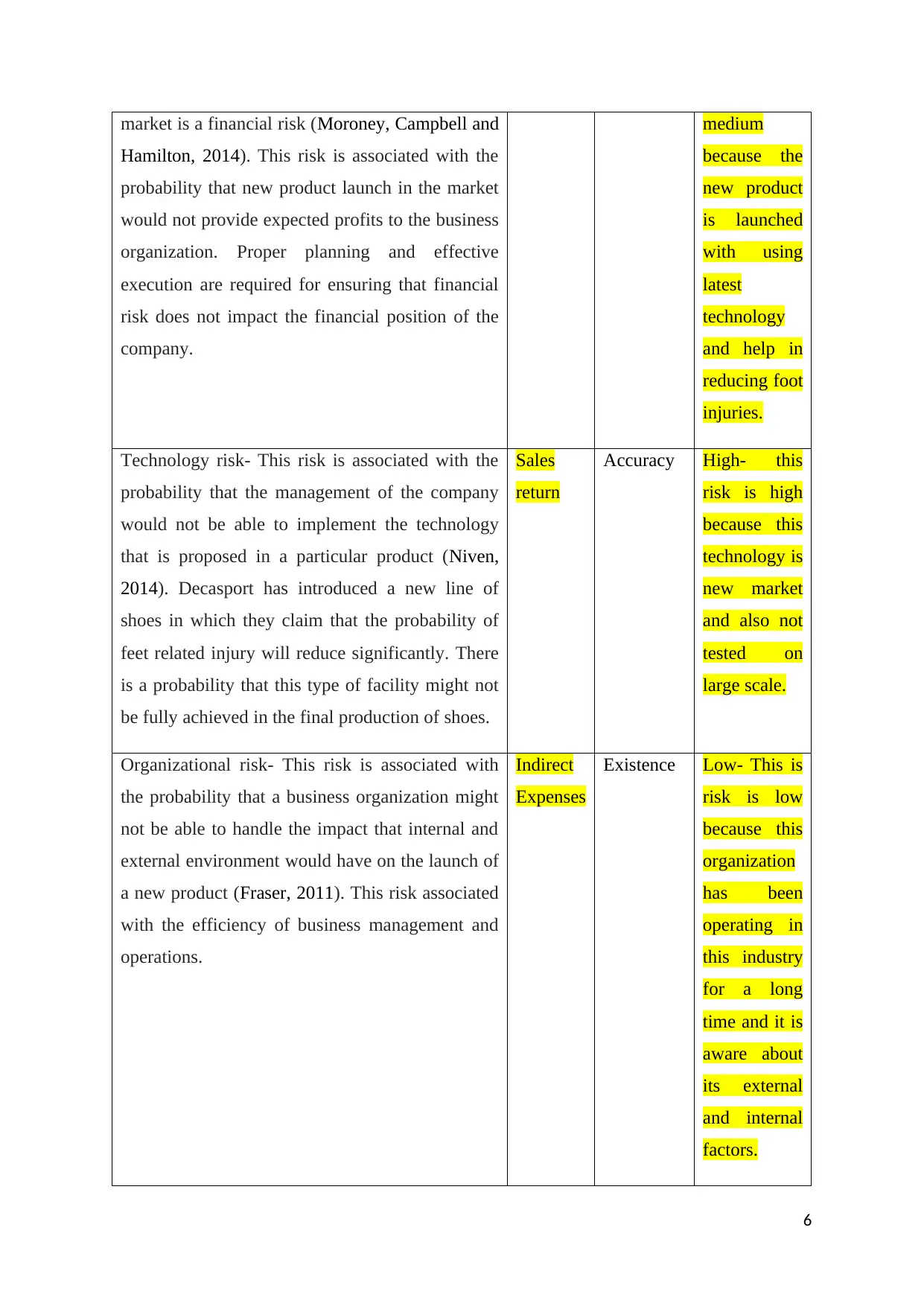

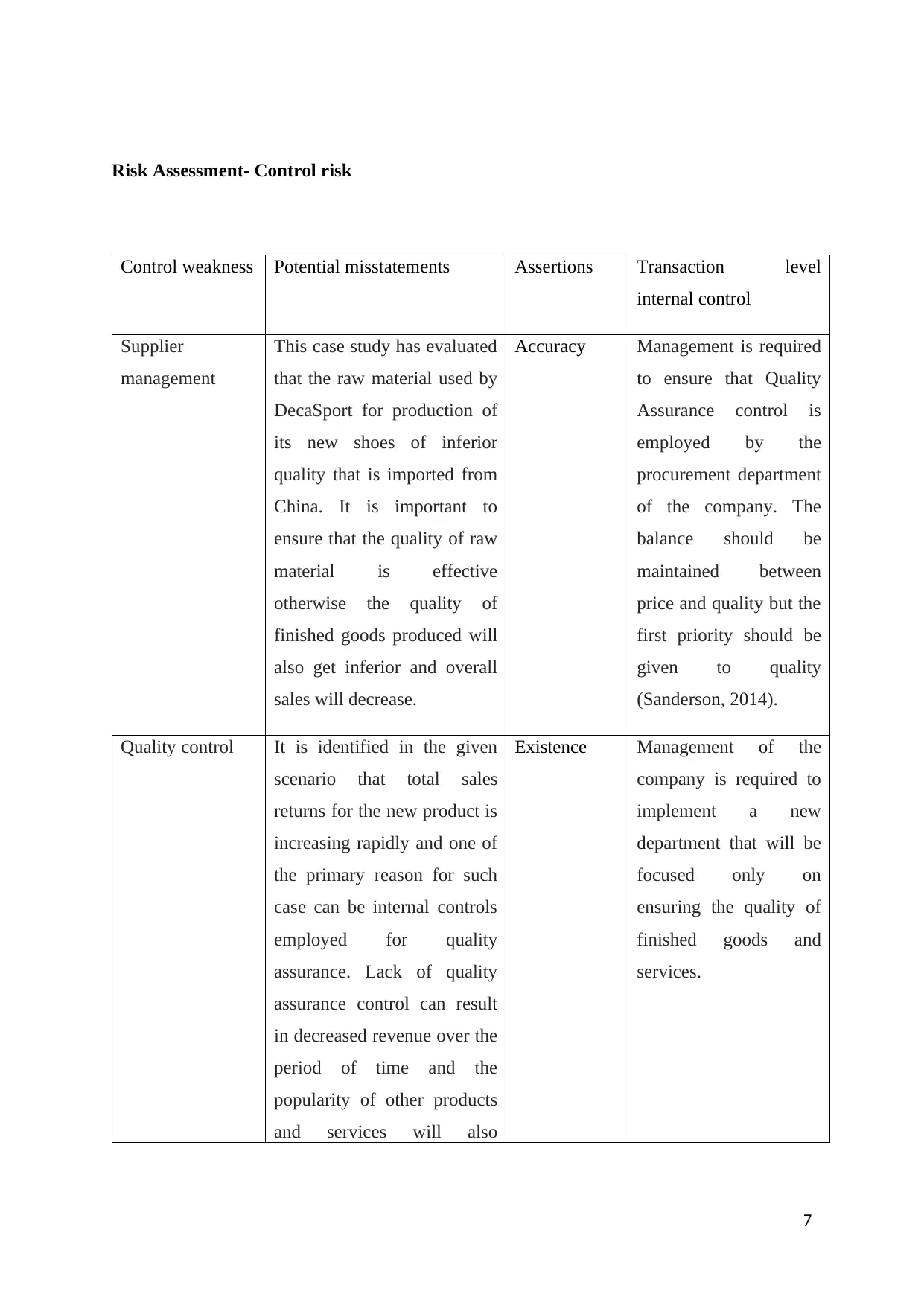

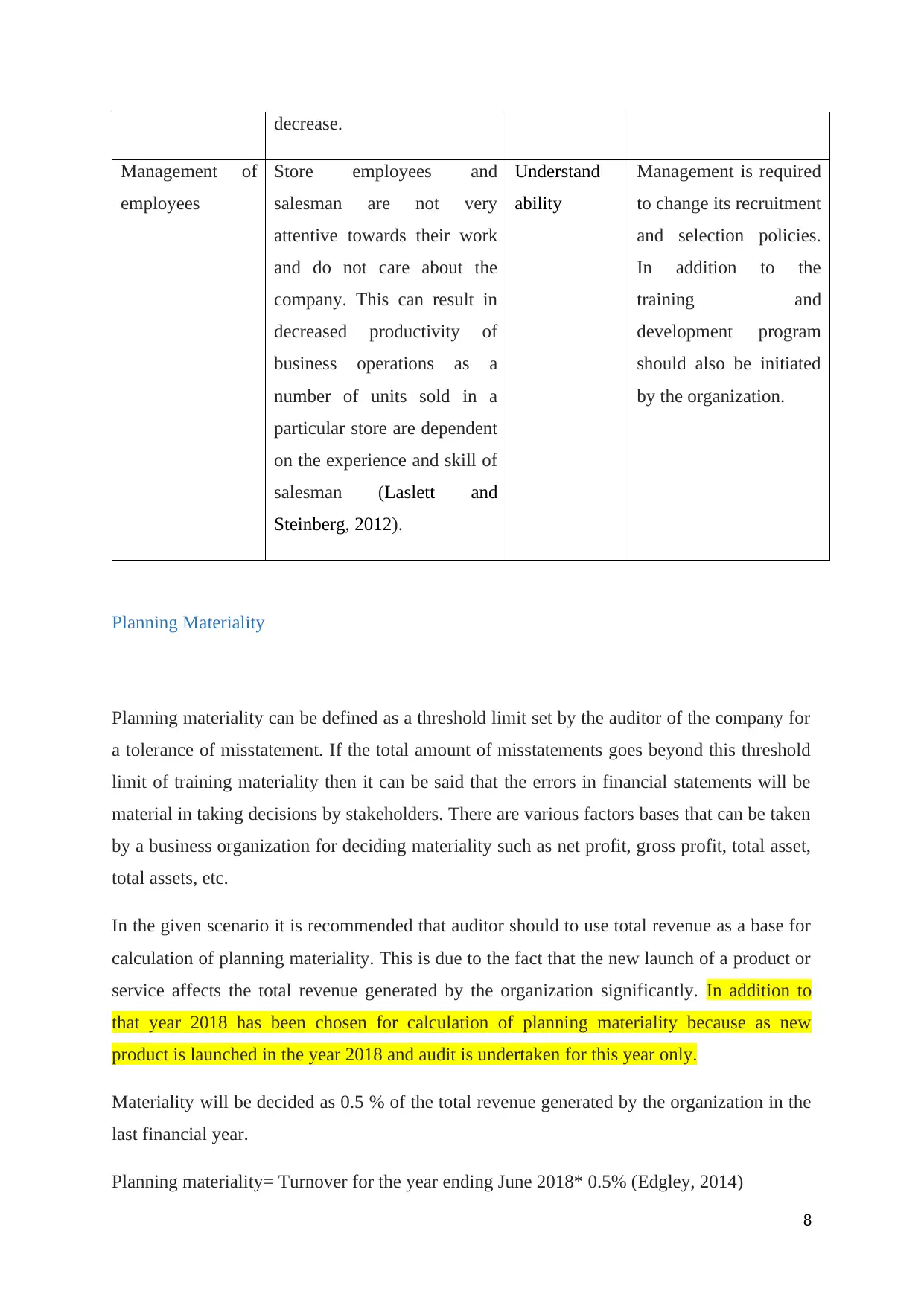

This report provides an analysis of the audit of DecaSport, a listed company specializing in luxury sport shoes, conducted by C&B Partners. The report identifies key issues, including the impact of competition on auditor independence due to non-audit services. It assesses inherent risks associated with DecaSport's new product launch, categorizing them as financial, technological, and organizational risks. Control risks, such as supplier management and quality control, are also evaluated. Furthermore, the report determines planning materiality, calculating a threshold for material misstatements based on the company's turnover. The conclusion emphasizes the importance of professional auditor behavior in accurately reflecting a company's financial position. The report draws on various academic sources to support its findings and recommendations, offering insights into auditing practices and risk management within the context of DecaSport's operations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.