ACC302: Auditing & Assurance - Assessment 3: Practical Audit Scenario

VerifiedAdded on 2022/11/14

|13

|2479

|457

Report

AI Summary

This report is an analysis of a practical audit scenario for ACC302 Auditing & Assurance, focusing on the audit of Woolworths Group Limited. The report begins with an executive summary and then delves into audit planning, including an analytical review of areas of concern such as supplier rebates, foreign currency risk, and shareholder returns. It examines relevant audit procedures to address these concerns. Part B of the report discusses corporate governance, including reporting, the role of the audit committee, and its benefits. The financial performance of the company is evaluated using financial ratios, and the report concludes with suggestions for improvement. The report is structured to provide a comprehensive overview of the audit process and the importance of corporate governance in ensuring financial transparency and accountability.

Assessment Information Subject Code: ACC302

Subject Name: Auditing & Assurance

Assessment Title: Assessment 3: A Practical Audit Scenario

Subject Name: Auditing & Assurance

Assessment Title: Assessment 3: A Practical Audit Scenario

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

Executive Summary

The report is primarily based on the audit of the company listed on the ASX. For this,

Woolworth’s group has been selected and the company is analysed in terms of analytical

review, planning phase and the concerned area. Further, the audit procedure is framed in

terms of the concern that the company faces such as supplier rebate, returns from shareholder,

etc. In addition, the corporate governance of the company is discussed and the benefits of the

audit committee for the company.

2

Executive Summary

The report is primarily based on the audit of the company listed on the ASX. For this,

Woolworth’s group has been selected and the company is analysed in terms of analytical

review, planning phase and the concerned area. Further, the audit procedure is framed in

terms of the concern that the company faces such as supplier rebate, returns from shareholder,

etc. In addition, the corporate governance of the company is discussed and the benefits of the

audit committee for the company.

2

Woolworths

Contents

Introduction...........................................................................................................................................3

1. Analytical Review............................................................................................................................3

2. Relevant Audit Procedure...............................................................................................................4

Part B.....................................................................................................................................................7

Corporate Governance..........................................................................................................................7

1. Reporting under corporate governance........................................................................................7

2. Audit Committee...........................................................................................................................7

3. Benefits of the Audit Committee....................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Appendix.............................................................................................................................................11

3

Contents

Introduction...........................................................................................................................................3

1. Analytical Review............................................................................................................................3

2. Relevant Audit Procedure...............................................................................................................4

Part B.....................................................................................................................................................7

Corporate Governance..........................................................................................................................7

1. Reporting under corporate governance........................................................................................7

2. Audit Committee...........................................................................................................................7

3. Benefits of the Audit Committee....................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

Appendix.............................................................................................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

Introduction

Audit planning is a very important part of the audit function. It is conducted in the very initial

phase of an audit function. Audit planning is a process in which an auditor takes the initiative

of knowing the organization in a better way. The auditor tries to determine the nature of the

business of an organization along with the risks that the same is prone to. Upon learning the

present and potential risks, the auditor evaluates the materiality of these risks. Thereafter, the

auditor plans an audit strategy on the basis of his findings so as to address these risks. This

ultimately reflects the significance of audit planning. Audit planning is the foundation of an

overall audit process and it is a known fact that stronger the foundation, stronger shall be the

overall structure.

1. Analytical Review

The following report highlights the area of concern for Woolworths Group Limited for the

year ending 2018-

a. Area of Concern-

Rebates from the suppliers – The organization faces various risks pertaining to rebates it

received from the suppliers. The rebates received are of standard and non-standard nature.

The organization faces rebates risks on account of its genuineness and accuracy that needs to

be verified. The way these rebates received are dealt with in the company highlights the risks

related to its reporting and accounting treatment. The rebates received from suppliers have an

influence on the inventories account, cost of sales and trade and other receivables

(Woolworths limited, 2018).

The company gets a discount from its suppliers in the form of normal discounts pertaining to

purchase of raw materials. These rebates received from suppliers must be recorded as a

separate item in the company’s balance sheet. This reflects the presence of transparency in

the financial statements of the company (Woolworths limited, 2018). However, the company

has reported an amount of $100 million as rebates received from suppliers in the account

receivables. This accounting treatment reflects that the rebates received from suppliers are

not received in the ongoing FY and is only recorded as trade receivables.

4

Introduction

Audit planning is a very important part of the audit function. It is conducted in the very initial

phase of an audit function. Audit planning is a process in which an auditor takes the initiative

of knowing the organization in a better way. The auditor tries to determine the nature of the

business of an organization along with the risks that the same is prone to. Upon learning the

present and potential risks, the auditor evaluates the materiality of these risks. Thereafter, the

auditor plans an audit strategy on the basis of his findings so as to address these risks. This

ultimately reflects the significance of audit planning. Audit planning is the foundation of an

overall audit process and it is a known fact that stronger the foundation, stronger shall be the

overall structure.

1. Analytical Review

The following report highlights the area of concern for Woolworths Group Limited for the

year ending 2018-

a. Area of Concern-

Rebates from the suppliers – The organization faces various risks pertaining to rebates it

received from the suppliers. The rebates received are of standard and non-standard nature.

The organization faces rebates risks on account of its genuineness and accuracy that needs to

be verified. The way these rebates received are dealt with in the company highlights the risks

related to its reporting and accounting treatment. The rebates received from suppliers have an

influence on the inventories account, cost of sales and trade and other receivables

(Woolworths limited, 2018).

The company gets a discount from its suppliers in the form of normal discounts pertaining to

purchase of raw materials. These rebates received from suppliers must be recorded as a

separate item in the company’s balance sheet. This reflects the presence of transparency in

the financial statements of the company (Woolworths limited, 2018). However, the company

has reported an amount of $100 million as rebates received from suppliers in the account

receivables. This accounting treatment reflects that the rebates received from suppliers are

not received in the ongoing FY and is only recorded as trade receivables.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

b. Area of Concern-

Foreign Currency Risk-

Woolworths will have to suffer losses arising out of the fluctuations in foreign currency rates.

The constant movement in foreign currency rates leads the organization to a state where it has

to make a higher amount of import payments. When a company indulges into transactions

where it has to make payment in foreign currencies then the same will have to bear losses if

there is a rise in foreign currency rates (Woolworths limited, 2018). The loss borne by the

organization shall be the difference between the amount earlier agreed upon and the actual

amount paid. Woolworths Private Limited must separately record such losses in the books as

a provision for changes in exchange rates. These results are most likely to influence the

decisions of the users of the company’s financial investments.

c. Area of Concern-

Total Shareholders Returns- Dividends, share prices and other re-investible capital returns

such as basic earnings per share are most likely to get affected due to the total shareholder's

returns. There is a drop in the total shareholders return while an increase in the share prices,

dividends and Basic EPS of the Woolworths in comparison with the last year as represented

in the following table (Woolworths limited, 2018).

Changes in the ratio of the company

The ratios are of great help in ascertaining the actual well-being of the company. The

financial ratios are used so as to ascertain the company’s current ratio, acid test ratio, debt-

equity ratio, return on total assets percentage, and so on (Niemi & Sundgren, 2012). The

financial ratios of Woolworths indicate that the liquidity of the company is at a lower level

while there is a constant fluctuation in gross profits and net profits of the company since the

last 3 years. The leverage ratios of Woolworths indicate that the company is in huge debts

which could ultimately be because of the fact that the same is facing a shortage of funds.

2. Relevant Audit Procedure

The company must opt for a relevant audit procedure so as to rectify its shortcomings that are

reflected from its financial ratios. Below are a few suggestions-

5

b. Area of Concern-

Foreign Currency Risk-

Woolworths will have to suffer losses arising out of the fluctuations in foreign currency rates.

The constant movement in foreign currency rates leads the organization to a state where it has

to make a higher amount of import payments. When a company indulges into transactions

where it has to make payment in foreign currencies then the same will have to bear losses if

there is a rise in foreign currency rates (Woolworths limited, 2018). The loss borne by the

organization shall be the difference between the amount earlier agreed upon and the actual

amount paid. Woolworths Private Limited must separately record such losses in the books as

a provision for changes in exchange rates. These results are most likely to influence the

decisions of the users of the company’s financial investments.

c. Area of Concern-

Total Shareholders Returns- Dividends, share prices and other re-investible capital returns

such as basic earnings per share are most likely to get affected due to the total shareholder's

returns. There is a drop in the total shareholders return while an increase in the share prices,

dividends and Basic EPS of the Woolworths in comparison with the last year as represented

in the following table (Woolworths limited, 2018).

Changes in the ratio of the company

The ratios are of great help in ascertaining the actual well-being of the company. The

financial ratios are used so as to ascertain the company’s current ratio, acid test ratio, debt-

equity ratio, return on total assets percentage, and so on (Niemi & Sundgren, 2012). The

financial ratios of Woolworths indicate that the liquidity of the company is at a lower level

while there is a constant fluctuation in gross profits and net profits of the company since the

last 3 years. The leverage ratios of Woolworths indicate that the company is in huge debts

which could ultimately be because of the fact that the same is facing a shortage of funds.

2. Relevant Audit Procedure

The company must opt for a relevant audit procedure so as to rectify its shortcomings that are

reflected from its financial ratios. Below are a few suggestions-

5

Woolworths

i) Rebate from Suppliers-

• The auditor must evaluate the rebates that are received from the suppliers and then

segregate the same as either discounts or incentives received.

• The auditor must trace necessary evidence so as to identify the rebates received as

discounts or incentives. The evidence must be in the form of confirmation received from the

suppliers in the form of written documentation.

ii) Total Shareholders Return-

• The auditor must gather an understanding of how the total shareholder's return can be

computed.

• The auditor must identify the reasons that lead to the drop in the shareholder's return.

• The auditor must ensure that the results ascertained are true and not due to any

mathematical mistake. The same can be done by means of double checks (Gay & Simnet,

2015).

iii) Foreign Currency Rates changes.

• The auditor must gather an understanding of the process used by the organization in

accounting the fluctuations in foreign currency rates.

• The auditor must evaluate the dates on which the profit or loss arising out of foreign

currency rates are recorded (Baldwin, 2010).

• The asset or liability can be written-off if the fluctuation in the foreign currency is

permanent and this must be recorded in the necessary documents and necessary disclosures

with respect to the same must also be provided.

• The users of the financial statements have full rights to know about the financial well

being of the company. Therefore, the auditor must make sure that there are necessary

disclosures in the financial statements of the company with respect to profit or loss arising

out of foreign currency rates changes (Baldwin, 2010).

6

i) Rebate from Suppliers-

• The auditor must evaluate the rebates that are received from the suppliers and then

segregate the same as either discounts or incentives received.

• The auditor must trace necessary evidence so as to identify the rebates received as

discounts or incentives. The evidence must be in the form of confirmation received from the

suppliers in the form of written documentation.

ii) Total Shareholders Return-

• The auditor must gather an understanding of how the total shareholder's return can be

computed.

• The auditor must identify the reasons that lead to the drop in the shareholder's return.

• The auditor must ensure that the results ascertained are true and not due to any

mathematical mistake. The same can be done by means of double checks (Gay & Simnet,

2015).

iii) Foreign Currency Rates changes.

• The auditor must gather an understanding of the process used by the organization in

accounting the fluctuations in foreign currency rates.

• The auditor must evaluate the dates on which the profit or loss arising out of foreign

currency rates are recorded (Baldwin, 2010).

• The asset or liability can be written-off if the fluctuation in the foreign currency is

permanent and this must be recorded in the necessary documents and necessary disclosures

with respect to the same must also be provided.

• The users of the financial statements have full rights to know about the financial well

being of the company. Therefore, the auditor must make sure that there are necessary

disclosures in the financial statements of the company with respect to profit or loss arising

out of foreign currency rates changes (Baldwin, 2010).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

iv) Analysis of the ratio

The factors that led to the enhancement in sales with the rise in inventory level must be

evaluated by the auditor. He must also drill into the sales pattern of the company. The auditor

must assess the contrast between the actual sales and the closing stock of inventory so as to

understand the reasons behind a rise in sales with the enhancement in inventory level

(Lapsley, 2012). The auditor must draw necessary comparisons with the previous year

numbers so as to assess the factors behind the decline in current assets and must also focus on

the reasons behind the fall in the liquidity ratio (Gay & Simnet, 2015).

7

iv) Analysis of the ratio

The factors that led to the enhancement in sales with the rise in inventory level must be

evaluated by the auditor. He must also drill into the sales pattern of the company. The auditor

must assess the contrast between the actual sales and the closing stock of inventory so as to

understand the reasons behind a rise in sales with the enhancement in inventory level

(Lapsley, 2012). The auditor must draw necessary comparisons with the previous year

numbers so as to assess the factors behind the decline in current assets and must also focus on

the reasons behind the fall in the liquidity ratio (Gay & Simnet, 2015).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

Part B

Corporate Governance

1. Reporting under corporate governance

The company is deemed to have sound corporate governance in its system. The management

of the company and the Board of directors have made full disclosures and have maintained

the level of compliance as well. This means that they have duly adhered to all the statutory

requirements and have fulfilled the needs of all the rules and regulations. The Corporate

Governance Statement issued by Woolworths reflects that the company has adhered to ASX

Corporate Council’s Corporate Governance Principles & Recommendations in the entire year

2018 (Woolworths limited, 2018).

2. Audit Committee

Woolworths has an audit committee as well. The audit committee in the company is known

as the Audit, Risk Management & Compliance Committee.

The companies that are enlisted on the Australian Stock Exchange are entitled to follow

various recommendations provided by the ASX Listing Rules and Corporate Governance

Guidelines. Principle 4 of the ASX Listing Rules and Corporate Governance Guidelines

provide that an organization must have a formal set of processes with respect to independent

verification so as to shield the integrity of its corporate reporting (Rezaee & Kedia, 2012).

It is why, Woolworths has formed its own Audit, Risk Management & Compliance

Committee. The composition of the Audit Committee meets the required criteria as-

i. The audit committee of the company has at least 3 members,

ii. The audit committee of the company comprises of only non-executive directors,

8

Part B

Corporate Governance

1. Reporting under corporate governance

The company is deemed to have sound corporate governance in its system. The management

of the company and the Board of directors have made full disclosures and have maintained

the level of compliance as well. This means that they have duly adhered to all the statutory

requirements and have fulfilled the needs of all the rules and regulations. The Corporate

Governance Statement issued by Woolworths reflects that the company has adhered to ASX

Corporate Council’s Corporate Governance Principles & Recommendations in the entire year

2018 (Woolworths limited, 2018).

2. Audit Committee

Woolworths has an audit committee as well. The audit committee in the company is known

as the Audit, Risk Management & Compliance Committee.

The companies that are enlisted on the Australian Stock Exchange are entitled to follow

various recommendations provided by the ASX Listing Rules and Corporate Governance

Guidelines. Principle 4 of the ASX Listing Rules and Corporate Governance Guidelines

provide that an organization must have a formal set of processes with respect to independent

verification so as to shield the integrity of its corporate reporting (Rezaee & Kedia, 2012).

It is why, Woolworths has formed its own Audit, Risk Management & Compliance

Committee. The composition of the Audit Committee meets the required criteria as-

i. The audit committee of the company has at least 3 members,

ii. The audit committee of the company comprises of only non-executive directors,

8

Woolworths

iii. The audit committee of the company has more independent directors and iv. The audit

committee of the company has an independent chairman who is not the chairperson of the

board.

Therefore, the audit committee of the company seemed to have met the required composition.

However, the audit company of the company has refrained from offering disclosure

pertaining to the presence of all non-executive directors. Also, the list of members does not

reflect the presence of all the non-executive directors in the audit committee. This signifies

the incompleteness in the composition of the audit committee.

3. Benefits of the Audit Committee

Yes, from my viewpoint there are huge benefits to having an audit committee. The roles and

responsibilities of the audit committee not only benefit the organization but also its auditors,

board, auditing profession, and society as well. The audit committee takes care of the key

policies of an organization which ultimately benefits the same. The audit committee monitors

and reviews the internal control processes of the company so as to ensure its effectiveness.

The performance of external auditors is monitored and reviewed by the audit committee

along with the board on a yearly basis (Matthew, 2015). The audit committee reviews and

monitors the efficacy of the internal audit team on a regular basis so as to ensure that the team

delivers quality work. The audit committee makes necessary recommendations to the Board

regarding the external auditors and the lead audit partner for the audit conducted in a

particular period (Geoffrey, Joleen, Kelli & David, 2016).

9

iii. The audit committee of the company has more independent directors and iv. The audit

committee of the company has an independent chairman who is not the chairperson of the

board.

Therefore, the audit committee of the company seemed to have met the required composition.

However, the audit company of the company has refrained from offering disclosure

pertaining to the presence of all non-executive directors. Also, the list of members does not

reflect the presence of all the non-executive directors in the audit committee. This signifies

the incompleteness in the composition of the audit committee.

3. Benefits of the Audit Committee

Yes, from my viewpoint there are huge benefits to having an audit committee. The roles and

responsibilities of the audit committee not only benefit the organization but also its auditors,

board, auditing profession, and society as well. The audit committee takes care of the key

policies of an organization which ultimately benefits the same. The audit committee monitors

and reviews the internal control processes of the company so as to ensure its effectiveness.

The performance of external auditors is monitored and reviewed by the audit committee

along with the board on a yearly basis (Matthew, 2015). The audit committee reviews and

monitors the efficacy of the internal audit team on a regular basis so as to ensure that the team

delivers quality work. The audit committee makes necessary recommendations to the Board

regarding the external auditors and the lead audit partner for the audit conducted in a

particular period (Geoffrey, Joleen, Kelli & David, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Woolworths

Conclusion

To conclude, it can be said that the company is not able to perform as per the expectations.

The financial performance of the company is weak as reflected from its financial ratios.

Therefore, the management of the company must take necessary measures so as to trace the

vulnerable areas that need rectification. However, the company seemed to have sound

corporate governance in its system.

10

Conclusion

To conclude, it can be said that the company is not able to perform as per the expectations.

The financial performance of the company is weak as reflected from its financial ratios.

Therefore, the management of the company must take necessary measures so as to trace the

vulnerable areas that need rectification. However, the company seemed to have sound

corporate governance in its system.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Woolworths

References

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309 [Accessed

20 May 2019]

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. [online]. 9(3), pp. 291-292. Available from

https://doi.org/10.1111/1468-0408.00081

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 9 April 2018]

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

796. Available from: https://doi.org/10.1080/09638180.2012.671465 [Accessed 21 April

2018]

Rezaee, Z & Kedia, B. L. (2012) Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative Accounting.

4(2), pp. 176-205. Available from: doi: 10.1016/j.sbspro.2014.06.041 [Accessed 20 May

2019]

Woolworths limited. (2018) Woolworths limited Annual Report and accounts 2018.

Available from: https://www.woolworthsgroup.com.au/page/investors/our-performance/

reports/Reports/Annual_Reports [Accessed 20 May 2019]

11

References

Baldwin, S. (2010) Doing a content audit or inventory. Pearson Press.

Gay, G. and Simnet, R. (2015) Auditing and Assurance Services. McGraw Hill

Geoffrey D. B, Joleen K, K. Kelli S. and David A. W. (2016) Attracting Applicants for In-

House and Outsourced Internal Audit Positions: Views from External Auditors. Accounting

Horizons. 30(1), pp. 143-156. Available from https://doi.org/10.2308/acch-51309 [Accessed

20 May 2019]

Lapsley, I. (2012) Commentary: Financial Accountability & Management. Qualitative

Research in Accounting & Management. [online]. 9(3), pp. 291-292. Available from

https://doi.org/10.1111/1468-0408.00081

Matthew, S. E. (2015) Does Internal Audit Function Quality Deter Management

Misconduct?. The Accounting Review. [online]. 90(2), pp. 495-527. Available from

https://doi.org/10.2308/accr-50871 [Accessed 9 April 2018]

Niemi, L. and Sundgren, S. (2012) Are modified audit opinions related to the availability of

credit? Evidence from Finnish SMEs. European Accounting Review. [online]. 21(4), p. 767-

796. Available from: https://doi.org/10.1080/09638180.2012.671465 [Accessed 21 April

2018]

Rezaee, Z & Kedia, B. L. (2012) Role of Corporate Governance Participants in Preventing

and Detecting Financial Statement Fraud. Journal of Forensic & Investigative Accounting.

4(2), pp. 176-205. Available from: doi: 10.1016/j.sbspro.2014.06.041 [Accessed 20 May

2019]

Woolworths limited. (2018) Woolworths limited Annual Report and accounts 2018.

Available from: https://www.woolworthsgroup.com.au/page/investors/our-performance/

reports/Reports/Annual_Reports [Accessed 20 May 2019]

11

Woolworths

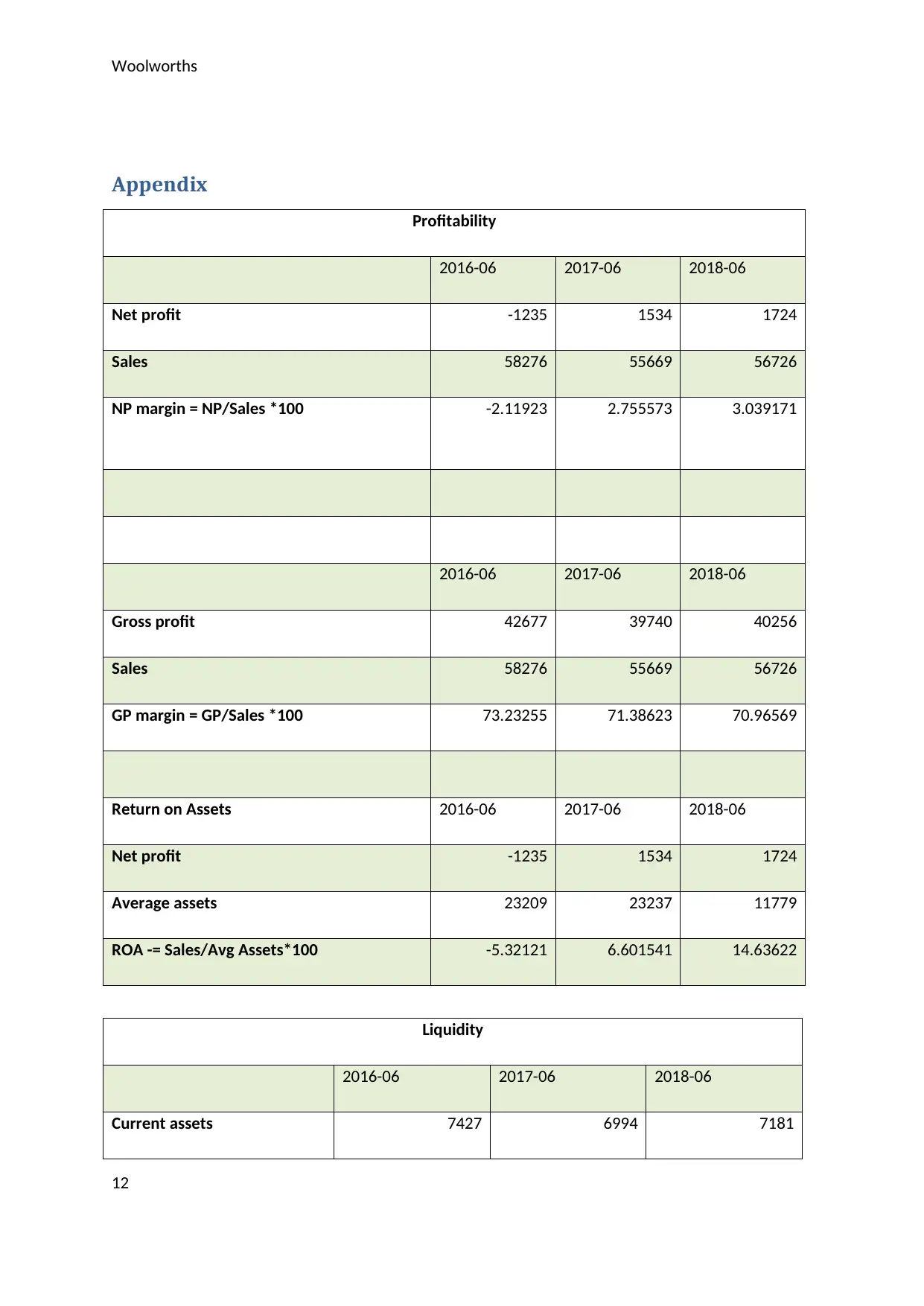

Appendix

Profitability

2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Sales 58276 55669 56726

NP margin = NP/Sales *100 -2.11923 2.755573 3.039171

2016-06 2017-06 2018-06

Gross profit 42677 39740 40256

Sales 58276 55669 56726

GP margin = GP/Sales *100 73.23255 71.38623 70.96569

Return on Assets 2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Average assets 23209 23237 11779

ROA -= Sales/Avg Assets*100 -5.32121 6.601541 14.63622

Liquidity

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

12

Appendix

Profitability

2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Sales 58276 55669 56726

NP margin = NP/Sales *100 -2.11923 2.755573 3.039171

2016-06 2017-06 2018-06

Gross profit 42677 39740 40256

Sales 58276 55669 56726

GP margin = GP/Sales *100 73.23255 71.38623 70.96569

Return on Assets 2016-06 2017-06 2018-06

Net profit -1235 1534 1724

Average assets 23209 23237 11779

ROA -= Sales/Avg Assets*100 -5.32121 6.601541 14.63622

Liquidity

2016-06 2017-06 2018-06

Current assets 7427 6994 7181

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.