Detailed Report on Auditing and Assurance Standards for Morris Ltd

VerifiedAdded on 2022/08/23

|12

|1998

|19

Report

AI Summary

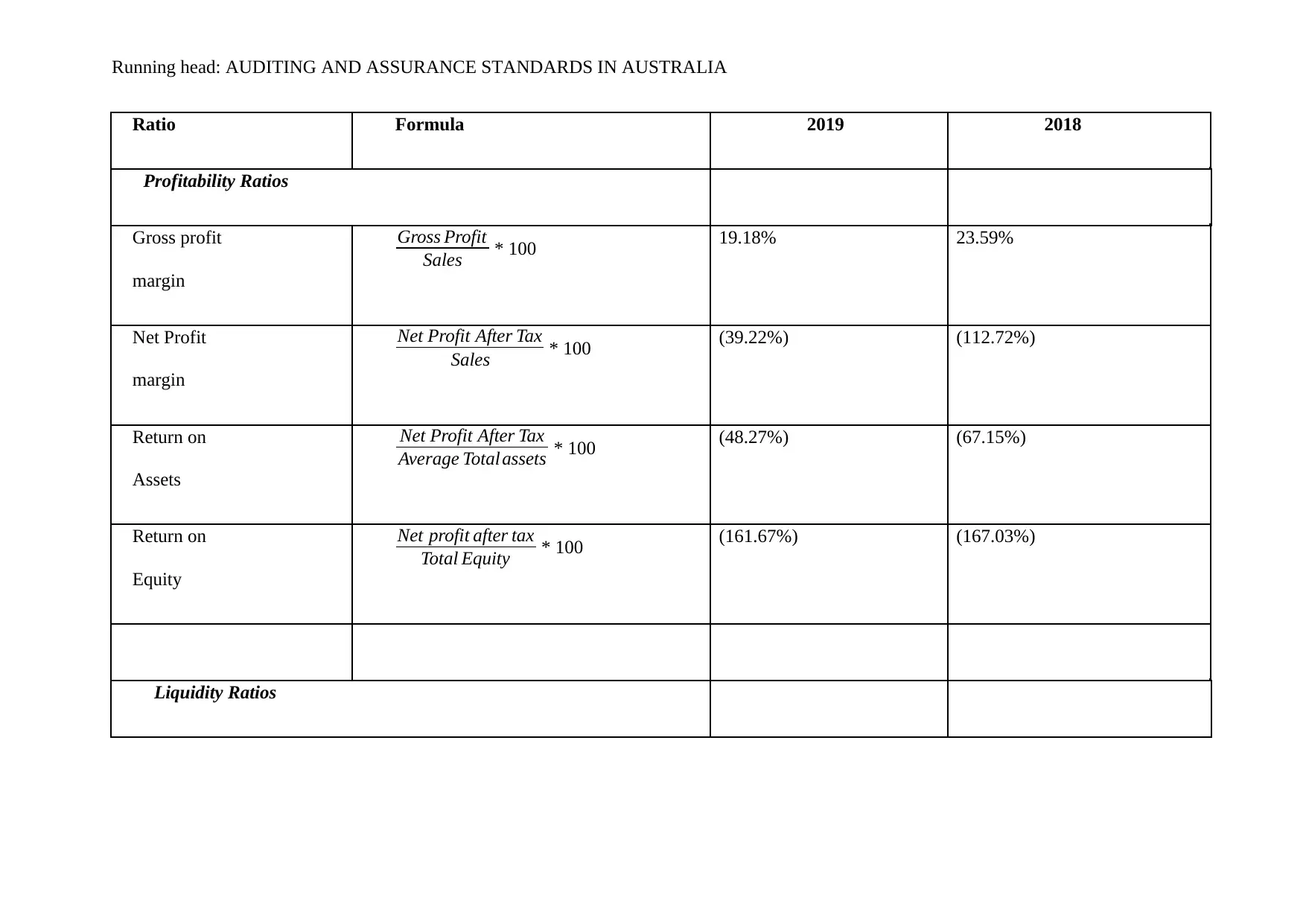

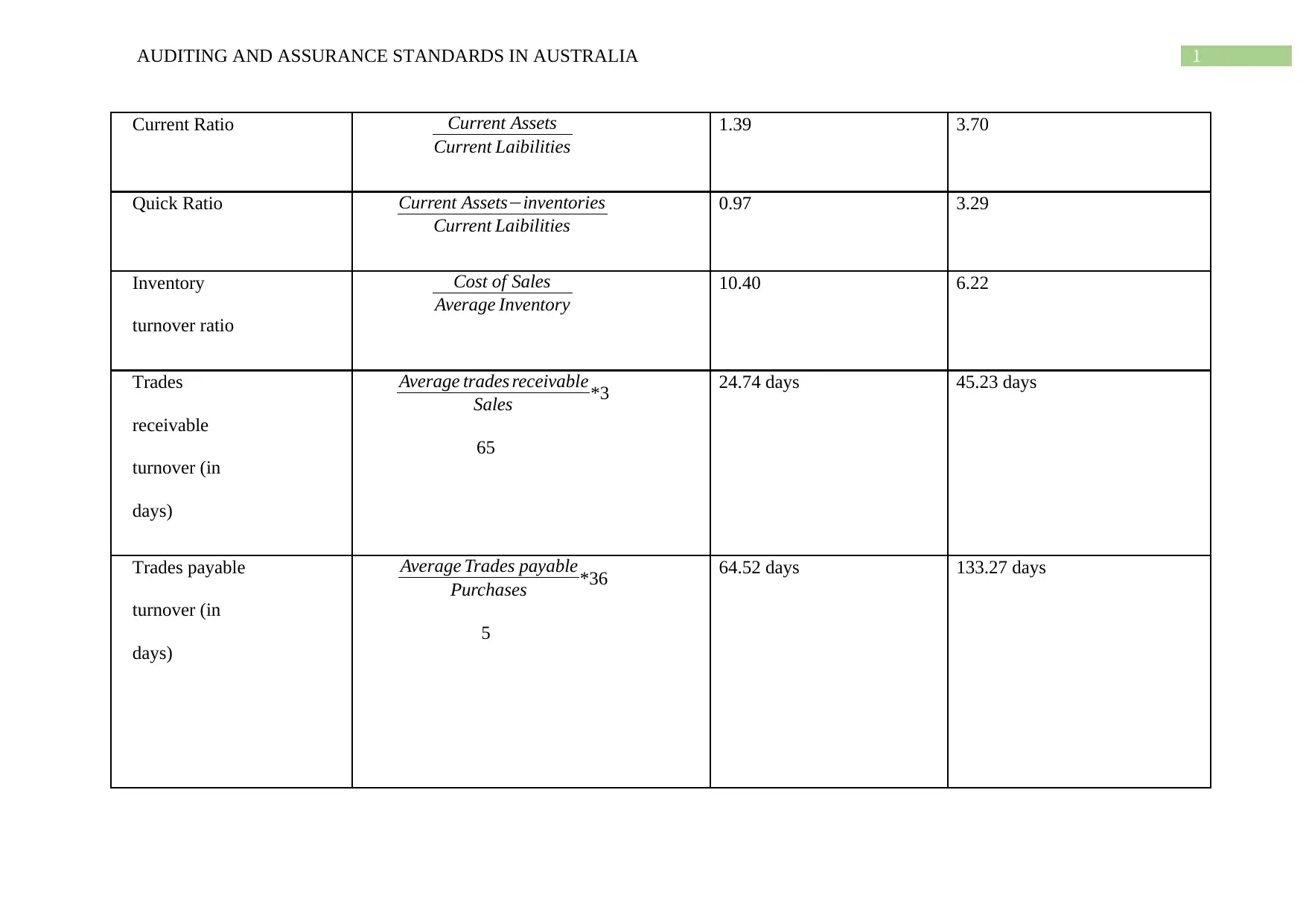

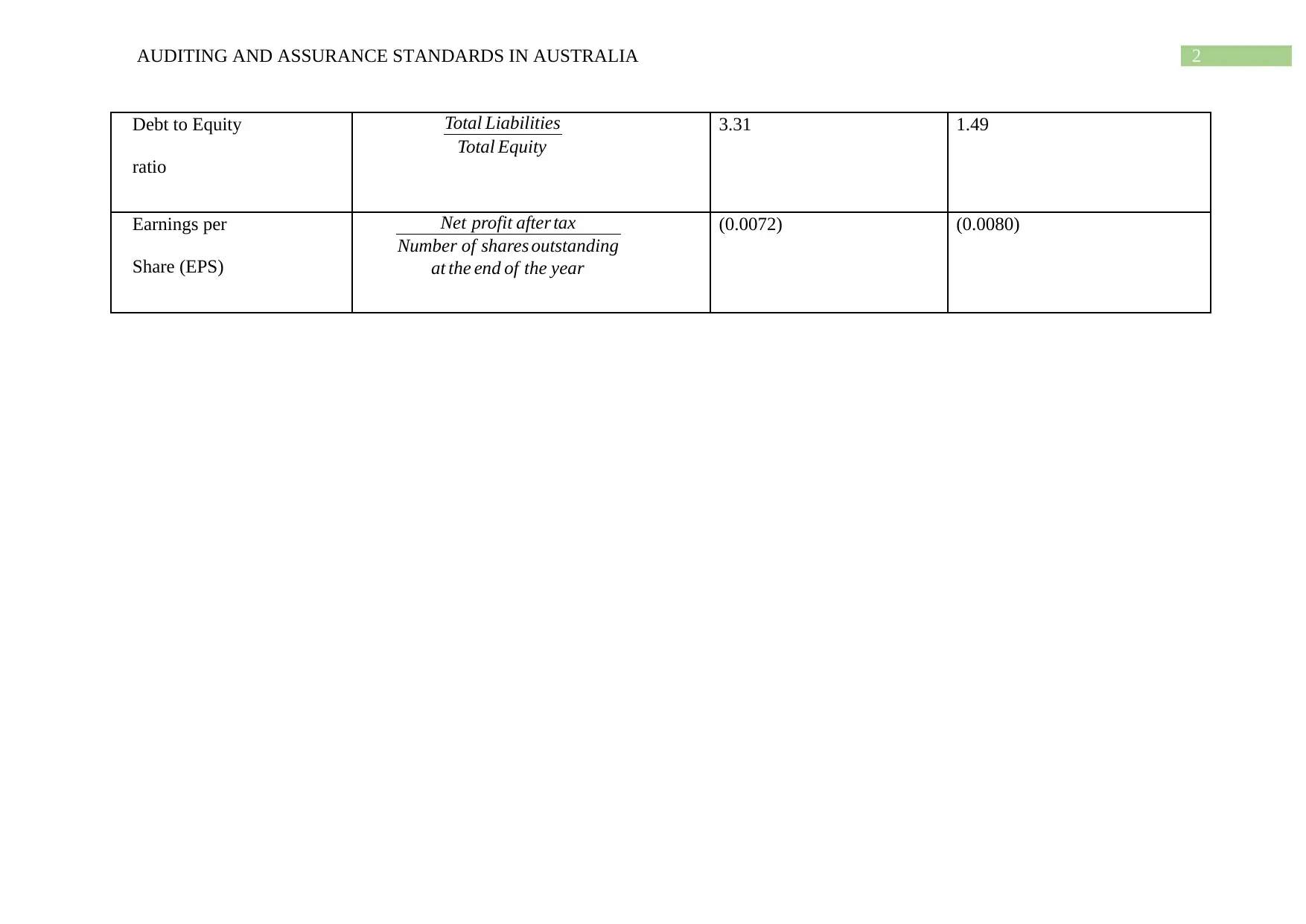

This report delves into the auditing and assurance standards applicable to Morris Ltd, a company recently listed on the Australian Securities Exchange. The analysis begins with an examination of risk assessment procedures, emphasizing the role of analytical procedures in identifying material misstatements. It then explores the importance of professional skepticism in auditing, highlighting its significance in evaluating management's information and detecting potential errors. The report further addresses the concept of materiality, outlining its application in audit planning and performance, and providing calculations based on financial data. Ratio analysis is performed to evaluate the company's profitability, liquidity, and solvency, comparing key financial metrics over two years. Finally, the report assesses Morris Ltd's going concern status, identifying potential risks based on financial ratios and other factors, such as declining current ratios, negative profit margins, and high debt levels. The report also highlights the potential impact of external factors, such as tropical cyclones on the company's operations, providing a comprehensive overview of the audit considerations.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.