ACC302 Auditing & Assurance: Assessment 3 - Audit Scenario Analysis

VerifiedAdded on 2022/11/25

|9

|2039

|181

Report

AI Summary

This report provides a comprehensive analysis of a practical audit scenario, focusing on the financial performance and corporate governance of Woolworth's Group. The assignment begins with an introduction that outlines the objectives of the report, followed by an analytical review of the company's financial statements using various ratios to assess liquidity, leverage, efficiency, and profitability. Areas of concern are identified, including the adoption of new accounting standards, critical judgments, and regulatory changes impacting the business. The report then details key audit procedures, emphasizing analytical review, inquiry, and computer-assisted audit techniques (CAAT). It also evaluates the company's corporate governance mechanisms and the role and benefits of the audit committee. The report concludes by highlighting the positive impacts of an effective audit committee on internal controls, fraud reduction, and stakeholder value, supported by relevant references.

Assessment 3: A Practical Audit Scenario

ACC302

Auditing & Assurance

ACC302

Auditing & Assurance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................2

Analytical review of Financial Statements.............................................................................................3

Areas of Concern...................................................................................................................................5

Audit Procedures...................................................................................................................................5

Corporate Governance..........................................................................................................................6

Audit Committee...................................................................................................................................6

Benefits of Audit Committee.................................................................................................................7

References.............................................................................................................................................8

1 | P a g e

Introduction...........................................................................................................................................2

Analytical review of Financial Statements.............................................................................................3

Areas of Concern...................................................................................................................................5

Audit Procedures...................................................................................................................................5

Corporate Governance..........................................................................................................................6

Audit Committee...................................................................................................................................6

Benefits of Audit Committee.................................................................................................................7

References.............................................................................................................................................8

1 | P a g e

Introduction

This assignment aims to highlight key audit performance of a company along with its corporate

governance, in order to effectively understand and review the audit and corporate governance the

latest annual report of the company (Woolworth’s group) is considered.

The financial statements of the company is analysed through various ratios to determine the nature

of business and its workings, deviation or significant areas of audit are noted based on the

summaries in the annual report of the company, audit committee is reviewed by checking the audit

committee report and also the annual report of the company.

This assignment also provides various procedures an auditor can perform further that would be

beneficial during the audit of financial statements (Visinescu, et al., 2017).

A wide review made on the business of the company for understanding the nature of control and

the corporate governance framework that incorporated in the company.

A conclusion formed on the benefits of audit committee by taking few instances that could positively

influence the growth of business, which would indirectly increase stakeholders’ wealth.

2 | P a g e

This assignment aims to highlight key audit performance of a company along with its corporate

governance, in order to effectively understand and review the audit and corporate governance the

latest annual report of the company (Woolworth’s group) is considered.

The financial statements of the company is analysed through various ratios to determine the nature

of business and its workings, deviation or significant areas of audit are noted based on the

summaries in the annual report of the company, audit committee is reviewed by checking the audit

committee report and also the annual report of the company.

This assignment also provides various procedures an auditor can perform further that would be

beneficial during the audit of financial statements (Visinescu, et al., 2017).

A wide review made on the business of the company for understanding the nature of control and

the corporate governance framework that incorporated in the company.

A conclusion formed on the benefits of audit committee by taking few instances that could positively

influence the growth of business, which would indirectly increase stakeholders’ wealth.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

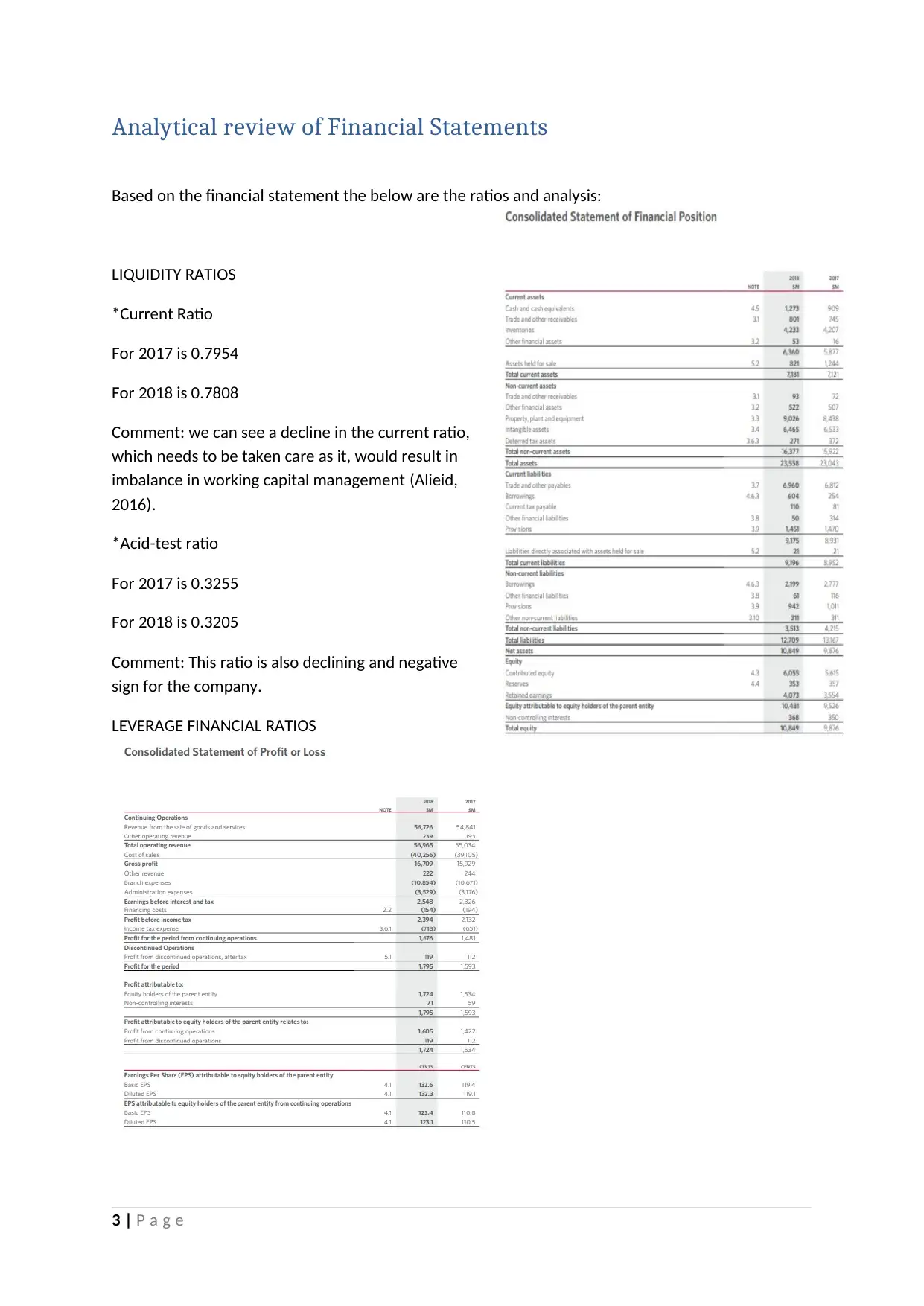

Analytical review of Financial Statements

Based on the financial statement the below are the ratios and analysis:

LIQUIDITY RATIOS

*Current Ratio

For 2017 is 0.7954

For 2018 is 0.7808

Comment: we can see a decline in the current ratio,

which needs to be taken care as it, would result in

imbalance in working capital management (Alieid,

2016).

*Acid-test ratio

For 2017 is 0.3255

For 2018 is 0.3205

Comment: This ratio is also declining and negative

sign for the company.

LEVERAGE FINANCIAL RATIOS

3 | P a g e

Based on the financial statement the below are the ratios and analysis:

LIQUIDITY RATIOS

*Current Ratio

For 2017 is 0.7954

For 2018 is 0.7808

Comment: we can see a decline in the current ratio,

which needs to be taken care as it, would result in

imbalance in working capital management (Alieid,

2016).

*Acid-test ratio

For 2017 is 0.3255

For 2018 is 0.3205

Comment: This ratio is also declining and negative

sign for the company.

LEVERAGE FINANCIAL RATIOS

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*Debt ratio

For 2017 is 0.5714

For 2018 is 0.5394

Comment: this shows a positive indicator as the debt over assets are reducing which can be

considered as a growth in investment prospective of company.

*Debt to Equity Ratio

For 2017 is 1.3332

For 2018 is 1.1714

Comment: a positive indicator for the business as the debt over equity Is in a downward trend that

indicates a beneficial growth of earnings for the shareholders of the company (Jones, 2017).

EFFICIENCY RATIOS

*Asset Turnover Ratio

For 2017 is 2.3799

For 2018 is 2.4079

Comment: a good indicator for the business company is able to sell more on percentage to that of

the increase in the investment on assets

*Inventory Turnover Ratios

For 2017 is 9.2961

For 2018 is 9.5100

Comment: another positive indicator for the company as it involves a growing trend in utilising

inventory and reducing idle resources.

PROFITABILITY RATIOS

*Gross profit Ratio

For 2017 is 0.2904

For 2018 is 0.2945

Comment: a positive indicator as there is an increase in the percentage of gross profit to that of

revenue (Bumgarner & Vasarhelyi, 2018).

*RETURN ON ASSETS RATIO

For 2017 is 0.0691

4 | P a g e

For 2017 is 0.5714

For 2018 is 0.5394

Comment: this shows a positive indicator as the debt over assets are reducing which can be

considered as a growth in investment prospective of company.

*Debt to Equity Ratio

For 2017 is 1.3332

For 2018 is 1.1714

Comment: a positive indicator for the business as the debt over equity Is in a downward trend that

indicates a beneficial growth of earnings for the shareholders of the company (Jones, 2017).

EFFICIENCY RATIOS

*Asset Turnover Ratio

For 2017 is 2.3799

For 2018 is 2.4079

Comment: a good indicator for the business company is able to sell more on percentage to that of

the increase in the investment on assets

*Inventory Turnover Ratios

For 2017 is 9.2961

For 2018 is 9.5100

Comment: another positive indicator for the company as it involves a growing trend in utilising

inventory and reducing idle resources.

PROFITABILITY RATIOS

*Gross profit Ratio

For 2017 is 0.2904

For 2018 is 0.2945

Comment: a positive indicator as there is an increase in the percentage of gross profit to that of

revenue (Bumgarner & Vasarhelyi, 2018).

*RETURN ON ASSETS RATIO

For 2017 is 0.0691

4 | P a g e

For 2018 is 0.1654

Comment: a positive indicator showing that the company is effectively using its assets to generate

profit and it is increasing.

Based on the analysis of financials there is growth in overall growth of profits for the company

including the profit after tax and this also was reflecting in the increase in EPS to the shareholders,

We can see that changes in few accounting standards had an influence in the financial statements.

There is an increase in customer base and the increase in revenues are indicator for a prosperous

growth to the business as the percentage increase in revenue is more than that of percentage

increase in cost for such sale.

Overall comment

An overall analysis based on various important market-driving ratios, we can say that the company is

doing well in terms of sales as well as in terms of financial lending.

The growth is moving forward and the nature of business not affected in the financial year by any

means (Heminway, 2017).

There is a value addition to the stakeholders as the company promoted the employee growth based

on the administration cost and the shareholders revenue was not compromised for any increased

cost.

Areas of Concern

# Few Significant accounting policies not adopted earlier such as AASB 15 Revenue from contracts

with customers, AASB 9 Financial Instruments, AASB 16 Leases due to which there would be

differences in the actual interpretations in the financials with the presented amounts.

# Critical judgements and accounting estimates such as identifying and measurement of the useful

life of assets and impairment on non-financial assets and provision including onerous leases.

# Where assumptions are made should be carefully audited which could be of major concern as it

influences the nature of business (Kuhn & Morris, 2016).

# Company being involved in food business affected by various regulatory changes, which needed to

be checked in order to avoid future contingent liabilities.

Audit Procedures

The key audit procedures that need to perform in the given company would be analytical review and

inquiry based on various assertions, which followed with observation, inspection and recalculation.

5 | P a g e

Comment: a positive indicator showing that the company is effectively using its assets to generate

profit and it is increasing.

Based on the analysis of financials there is growth in overall growth of profits for the company

including the profit after tax and this also was reflecting in the increase in EPS to the shareholders,

We can see that changes in few accounting standards had an influence in the financial statements.

There is an increase in customer base and the increase in revenues are indicator for a prosperous

growth to the business as the percentage increase in revenue is more than that of percentage

increase in cost for such sale.

Overall comment

An overall analysis based on various important market-driving ratios, we can say that the company is

doing well in terms of sales as well as in terms of financial lending.

The growth is moving forward and the nature of business not affected in the financial year by any

means (Heminway, 2017).

There is a value addition to the stakeholders as the company promoted the employee growth based

on the administration cost and the shareholders revenue was not compromised for any increased

cost.

Areas of Concern

# Few Significant accounting policies not adopted earlier such as AASB 15 Revenue from contracts

with customers, AASB 9 Financial Instruments, AASB 16 Leases due to which there would be

differences in the actual interpretations in the financials with the presented amounts.

# Critical judgements and accounting estimates such as identifying and measurement of the useful

life of assets and impairment on non-financial assets and provision including onerous leases.

# Where assumptions are made should be carefully audited which could be of major concern as it

influences the nature of business (Kuhn & Morris, 2016).

# Company being involved in food business affected by various regulatory changes, which needed to

be checked in order to avoid future contingent liabilities.

Audit Procedures

The key audit procedures that need to perform in the given company would be analytical review and

inquiry based on various assertions, which followed with observation, inspection and recalculation.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analytical procedures be done based on the criteria of covering major key areas that could affect the

financials, various categories have to be made based on importance that could depend on

occurrence and the amount involved.

Computer assisted audit technique (CAAT) should be used in order to have efficiency and

effectiveness in conducting the audit (Mun, 2018).

Provision and judgements made are few key areas to focus during audit as it could involve deviations

from the actual standards.

Substantive testing of individuals account details done in the areas where the accounting standards

were not well implemented such as leasing; the auditor has to conduct test check on various

operation processes to check for its consistency and accountability.

Sampling method used in accordance to the available past audit information and experience as

random sampling could prove fatal at few times.

Account details checked based on nature of occurrence and its nature, which would be of use to the

audit.

The key concern during the analysis, which mentioned above, required audit carefully with proper

explanations from the management where necessary.

The accounting ratios also have to take into account while concluding an audit, which would show

any potential change in the observations and assertions, made during the audit.

Completeness testing on the transactions at business need a check during audit as this could

influence the nature of accounting and leakage of revenue could have happened.

Deviation from the standard operating procedures need audit as it could affect the internal controls

in the business.

Corporate Governance

Yes, the group company (Woolworth’s group) has an effective corporate governance mechanism in

place that would balance the interests of stakeholders.

In the reports of the Chairman and The CEO of the company in the annual report, we could see that

the shareholders’ value enhanced along with enhancing the innovation among employees and

contributing to the growth of the community.

Under our key priorities page in the annual report, the priorities were given to customers and

employees and then to the economy which would balance the interest of all the stakeholders.

Employment opportunities were increased and under Planet page in the report, the environmental

impact made by the business is analysed and dealt with through reducing the carbon emissions and

various other aspects (Raiborn, et al., 2016).

6 | P a g e

financials, various categories have to be made based on importance that could depend on

occurrence and the amount involved.

Computer assisted audit technique (CAAT) should be used in order to have efficiency and

effectiveness in conducting the audit (Mun, 2018).

Provision and judgements made are few key areas to focus during audit as it could involve deviations

from the actual standards.

Substantive testing of individuals account details done in the areas where the accounting standards

were not well implemented such as leasing; the auditor has to conduct test check on various

operation processes to check for its consistency and accountability.

Sampling method used in accordance to the available past audit information and experience as

random sampling could prove fatal at few times.

Account details checked based on nature of occurrence and its nature, which would be of use to the

audit.

The key concern during the analysis, which mentioned above, required audit carefully with proper

explanations from the management where necessary.

The accounting ratios also have to take into account while concluding an audit, which would show

any potential change in the observations and assertions, made during the audit.

Completeness testing on the transactions at business need a check during audit as this could

influence the nature of accounting and leakage of revenue could have happened.

Deviation from the standard operating procedures need audit as it could affect the internal controls

in the business.

Corporate Governance

Yes, the group company (Woolworth’s group) has an effective corporate governance mechanism in

place that would balance the interests of stakeholders.

In the reports of the Chairman and The CEO of the company in the annual report, we could see that

the shareholders’ value enhanced along with enhancing the innovation among employees and

contributing to the growth of the community.

Under our key priorities page in the annual report, the priorities were given to customers and

employees and then to the economy which would balance the interest of all the stakeholders.

Employment opportunities were increased and under Planet page in the report, the environmental

impact made by the business is analysed and dealt with through reducing the carbon emissions and

various other aspects (Raiborn, et al., 2016).

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In response to climatic change, the group has said that they support the recommendation of the

Task Force on climate related financial disclosures (TFCD). In addition, focusing on enhancing the

greenhouse gas utilisation in the production process, which would also reduce operation cost.

Audit Committee

Yes, there exists an audit committee in the name of Audit, Risk Management and Compliance

Committee.

The composition of the committee is in accordance with the applicable regulatory requirements

where there are a minimum of three directors with majority of them being independent directors as

assessed by the board

The company secretary will be the secretary of the committee and the chairperson of the committee

will be an independent director appointed by the board from the committee’s members and will not

be the chairperson of the board (Swarnapali, 2017).

Benefits of Audit Committee

Yes according to my opinion, a committee exclusively dealing with the responsibilities of audit, which

is an audit committee, is definitely a benefit to the statutory auditor.

As this could reduce, the risk involved in the audit and it will reduce the time taken for external

auditors making it much easier and effective for conducting the audit to them.

An audit committee would enhance the internal process and internal controls in the business, which

could reduce the occurrence of fraud.

For the society, which will develop only when a company is growing as the stakeholders, would

affect as a whole, an audit committee would definitely be of a beneficial use.

Audit committee manages the outcomes of internal auditors findings along with follow up of

implementation of necessary amendments to the internal controls as and when required based on

the internal and external auditors review, it is important that the audit committee be present at the

board meetings during discussion about the financial statements before its submission to the

shareholders at large (Grenier, 2017).

It manages the conduct of business in accordance with compliance requirements and checks for the

integrity in process of doing business by the company that can reduce any further irregularities in

governance and eliminate penalties.

7 | P a g e

Task Force on climate related financial disclosures (TFCD). In addition, focusing on enhancing the

greenhouse gas utilisation in the production process, which would also reduce operation cost.

Audit Committee

Yes, there exists an audit committee in the name of Audit, Risk Management and Compliance

Committee.

The composition of the committee is in accordance with the applicable regulatory requirements

where there are a minimum of three directors with majority of them being independent directors as

assessed by the board

The company secretary will be the secretary of the committee and the chairperson of the committee

will be an independent director appointed by the board from the committee’s members and will not

be the chairperson of the board (Swarnapali, 2017).

Benefits of Audit Committee

Yes according to my opinion, a committee exclusively dealing with the responsibilities of audit, which

is an audit committee, is definitely a benefit to the statutory auditor.

As this could reduce, the risk involved in the audit and it will reduce the time taken for external

auditors making it much easier and effective for conducting the audit to them.

An audit committee would enhance the internal process and internal controls in the business, which

could reduce the occurrence of fraud.

For the society, which will develop only when a company is growing as the stakeholders, would

affect as a whole, an audit committee would definitely be of a beneficial use.

Audit committee manages the outcomes of internal auditors findings along with follow up of

implementation of necessary amendments to the internal controls as and when required based on

the internal and external auditors review, it is important that the audit committee be present at the

board meetings during discussion about the financial statements before its submission to the

shareholders at large (Grenier, 2017).

It manages the conduct of business in accordance with compliance requirements and checks for the

integrity in process of doing business by the company that can reduce any further irregularities in

governance and eliminate penalties.

7 | P a g e

References

Alieid, E. E. M., 2016. The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), pp. 233-242.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jones, P., 2017. Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Mun, K. a. S. I., 2018. A close look at the role of regulatory fit in consumers’ responses to unethical

firms.. s.l.:s.n.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Swarnapali, N., 2017. Corporate sustainability: A Literature review. Research Gate, 1(3), pp. 1-5.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

8 | P a g e

Alieid, E. E. M., 2016. The Role of Accounting Information Systems in Making Investment Decisions.

Internal Auditing & Risk Management, 11(2), pp. 233-242.

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing:

Theory and Application, 20(1), pp. 7-51.

Grenier, J., 2017. Encouraging Professional Skepticism in the Industry Specialization Era. Journal of

Business Ethics, 142(2), pp. 241-256.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Jones, P., 2017. Statistical Sampling and Risk Analysis in Auditing. NY: Routledge.

Kuhn, J. & Morris, B., 2016. IT internal control weaknesses and the market value of firms. Journal of

Enterprise Information Management, 30(6).

Mun, K. a. S. I., 2018. A close look at the role of regulatory fit in consumers’ responses to unethical

firms.. s.l.:s.n.

Raiborn, C., Butler, J. & Martin, K., 2016. The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), pp. 10-21.

Swarnapali, N., 2017. Corporate sustainability: A Literature review. Research Gate, 1(3), pp. 1-5.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.