ACCT20075 Auditing and Assurance Report - Mineral Resources Ltd.

VerifiedAdded on 2022/11/26

|13

|2684

|369

Report

AI Summary

This report provides a comprehensive analysis of an auditing and assurance assignment focused on Mineral Resources Limited. The report begins with an introduction to materiality, its significance in financial statement audits, and the different methods for calculating it. It then delves into an analytical review of the company's financial statements from 2015 to 2018, examining key ratios related to efficiency, liquidity, profitability, and capital structure. Based on this review and the materiality level, the report identifies key risk areas, associated audit assertions at risk, and relevant audit procedures. The report also reviews the company's statement of cash flows, highlighting major cash inflows and outflows. Finally, it examines the audit report, including the type of opinion issued and any key audit matters identified by the auditors, such as mine development expenditure, provision for site rehabilitation, and inventory valuation. The report concludes that the company has stable audit risk and would be sustainable in long run.

Auditing and aussrance

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Module Number-

[DATE]

Hewlett-Packard

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction...........................................................................................................................................2

Section 1................................................................................................................................................2

Requirement 1...................................................................................................................................2

Requirement 2...................................................................................................................................3

Section 2................................................................................................................................................4

Analytical review...............................................................................................................................4

Key risk area, audit assertion at risk and audit procedure..................................................................7

Section 3................................................................................................................................................8

Statement of cash flows.....................................................................................................................8

Review of audit report.......................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Introduction...........................................................................................................................................2

Section 1................................................................................................................................................2

Requirement 1...................................................................................................................................2

Requirement 2...................................................................................................................................3

Section 2................................................................................................................................................4

Analytical review...............................................................................................................................4

Key risk area, audit assertion at risk and audit procedure..................................................................7

Section 3................................................................................................................................................8

Statement of cash flows.....................................................................................................................8

Review of audit report.......................................................................................................................9

Conclusion...........................................................................................................................................10

References...........................................................................................................................................11

Introduction

This report reveals the key understanding on the Materiality in respect to financial

statements of the company and helps in evaluating the auditing risk model of the Mineral

resources Company. In the starting of this report nature, description and importance of

materiality in respect to audit of financial statements has been taken into consideration. After

that, analytical review of the undertaken financial statement have been assessed. Afterward,

cash flow statement of the company have been reviewed to evaluate the minimum and

maximum cash outflow and inflow from the particular items recorded in the books of account

of company.

Section 1

Requirement 1

NATURE, DESCRIPTION AND IMPORTANCE OF MATERIALITY IN RESPECT

TO AUDIT OF FINANCIAL STATEMENTS

Materiality in respect to financial statements reflects the importance attached to any financial

information be in respect to its size or nature. Materiality is defined as the ability of an

information to change the user’s decisions from the one which would have been taken in

absence of that material information (Lakis., & Masiulevičius, 2017). The importance of

identification of materiality for a set of financial statements increases when its audit it to be

conducted. Audit cannot be undertaken by checking the entire information available in

financial statements, but has to be conducted on sample basis. The determination of sample

has to be from the population which has high importance and risk attached to it. This

importance and risk is determined by computing and quantifying materiality for financial

statements (Noreen, Brewer, & Garrison, 2014).

DIFFERENT BASIS AND CONSIDERATION FOR COMPUTING MATERIALITY

For quantifying materiality, different basis can be selected from financial statements listed as

follows:

Base account % applied

This report reveals the key understanding on the Materiality in respect to financial

statements of the company and helps in evaluating the auditing risk model of the Mineral

resources Company. In the starting of this report nature, description and importance of

materiality in respect to audit of financial statements has been taken into consideration. After

that, analytical review of the undertaken financial statement have been assessed. Afterward,

cash flow statement of the company have been reviewed to evaluate the minimum and

maximum cash outflow and inflow from the particular items recorded in the books of account

of company.

Section 1

Requirement 1

NATURE, DESCRIPTION AND IMPORTANCE OF MATERIALITY IN RESPECT

TO AUDIT OF FINANCIAL STATEMENTS

Materiality in respect to financial statements reflects the importance attached to any financial

information be in respect to its size or nature. Materiality is defined as the ability of an

information to change the user’s decisions from the one which would have been taken in

absence of that material information (Lakis., & Masiulevičius, 2017). The importance of

identification of materiality for a set of financial statements increases when its audit it to be

conducted. Audit cannot be undertaken by checking the entire information available in

financial statements, but has to be conducted on sample basis. The determination of sample

has to be from the population which has high importance and risk attached to it. This

importance and risk is determined by computing and quantifying materiality for financial

statements (Noreen, Brewer, & Garrison, 2014).

DIFFERENT BASIS AND CONSIDERATION FOR COMPUTING MATERIALITY

For quantifying materiality, different basis can be selected from financial statements listed as

follows:

Base account % applied

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

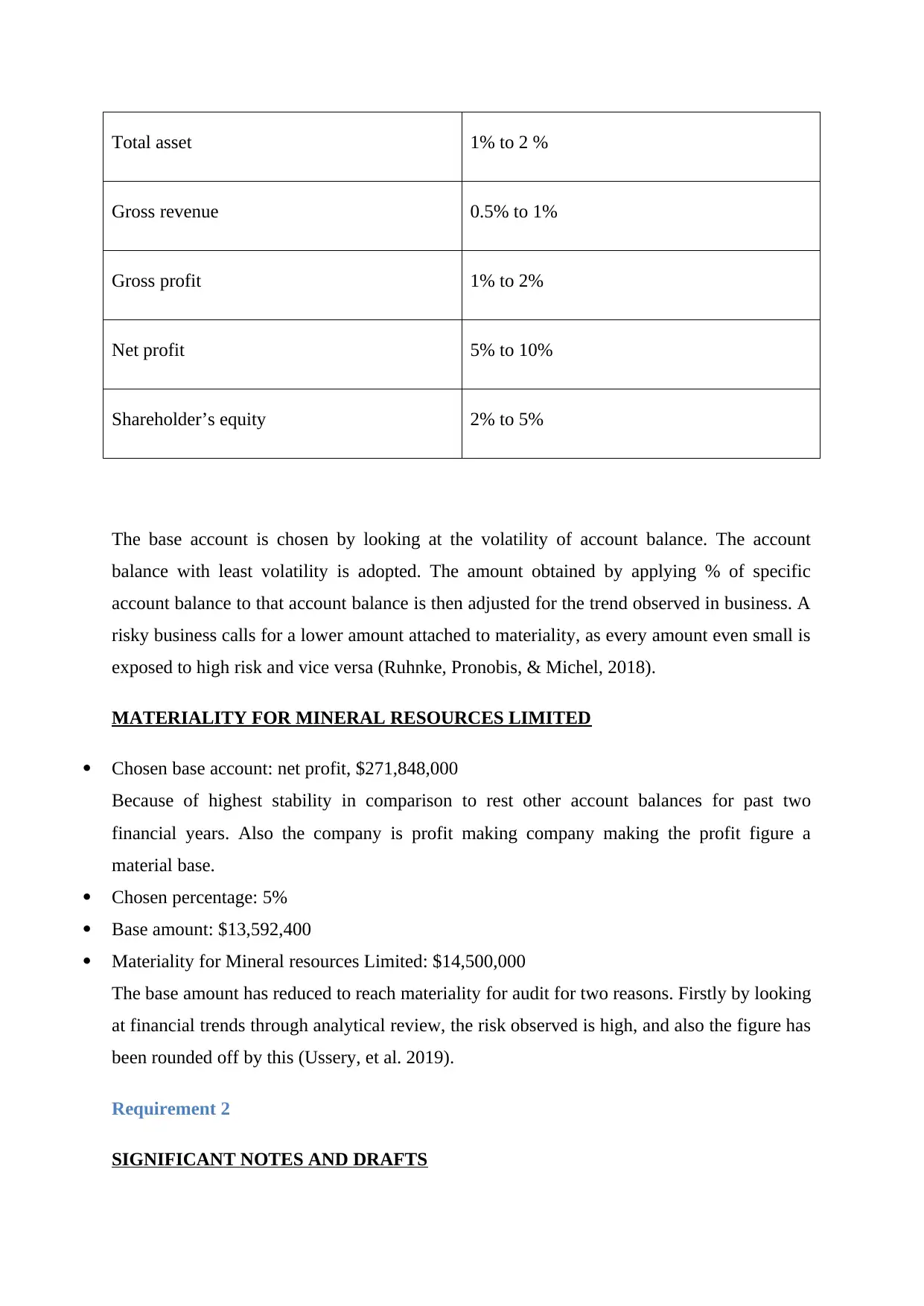

Total asset 1% to 2 %

Gross revenue 0.5% to 1%

Gross profit 1% to 2%

Net profit 5% to 10%

Shareholder’s equity 2% to 5%

The base account is chosen by looking at the volatility of account balance. The account

balance with least volatility is adopted. The amount obtained by applying % of specific

account balance to that account balance is then adjusted for the trend observed in business. A

risky business calls for a lower amount attached to materiality, as every amount even small is

exposed to high risk and vice versa (Ruhnke, Pronobis, & Michel, 2018).

MATERIALITY FOR MINERAL RESOURCES LIMITED

Chosen base account: net profit, $271,848,000

Because of highest stability in comparison to rest other account balances for past two

financial years. Also the company is profit making company making the profit figure a

material base.

Chosen percentage: 5%

Base amount: $13,592,400

Materiality for Mineral resources Limited: $14,500,000

The base amount has reduced to reach materiality for audit for two reasons. Firstly by looking

at financial trends through analytical review, the risk observed is high, and also the figure has

been rounded off by this (Ussery, et al. 2019).

Requirement 2

SIGNIFICANT NOTES AND DRAFTS

Gross revenue 0.5% to 1%

Gross profit 1% to 2%

Net profit 5% to 10%

Shareholder’s equity 2% to 5%

The base account is chosen by looking at the volatility of account balance. The account

balance with least volatility is adopted. The amount obtained by applying % of specific

account balance to that account balance is then adjusted for the trend observed in business. A

risky business calls for a lower amount attached to materiality, as every amount even small is

exposed to high risk and vice versa (Ruhnke, Pronobis, & Michel, 2018).

MATERIALITY FOR MINERAL RESOURCES LIMITED

Chosen base account: net profit, $271,848,000

Because of highest stability in comparison to rest other account balances for past two

financial years. Also the company is profit making company making the profit figure a

material base.

Chosen percentage: 5%

Base amount: $13,592,400

Materiality for Mineral resources Limited: $14,500,000

The base amount has reduced to reach materiality for audit for two reasons. Firstly by looking

at financial trends through analytical review, the risk observed is high, and also the figure has

been rounded off by this (Ussery, et al. 2019).

Requirement 2

SIGNIFICANT NOTES AND DRAFTS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DRAFT OR NOTE AUDIT PROCEDURE

Contingent liabilities: the value of

contingent liabilities has fallen in the

current financial year by around 20%.

This fall might be a signal towards

management not disclosing all the

contingent liabilities in its books of

accounts.

Checking of legal expenses account

extensively.

Review and analysis of the Internal

Revenue Service Report.

Related party transactions: the volume

and value of transactions undertaken

with related parties have increased in the

financial year 2018 as compared to

financial year 2017. Risk relate to non-

accounting of such transactions at arm

length’s price.

Checking minutes of board meeting

relating to the business transactions done

with related parties.

Questioning management and obtaining

written confirmation from them verifying

conduct of related party transactions at

arm’s length price.

Section 2

Analytical review

The following table provides a preliminary analytical review of the financial information of

Mineral Resources Limited for period 2015 to 2018:

RATIO FORMULA MINERAL RESOURCES

LIMITED

Contingent liabilities: the value of

contingent liabilities has fallen in the

current financial year by around 20%.

This fall might be a signal towards

management not disclosing all the

contingent liabilities in its books of

accounts.

Checking of legal expenses account

extensively.

Review and analysis of the Internal

Revenue Service Report.

Related party transactions: the volume

and value of transactions undertaken

with related parties have increased in the

financial year 2018 as compared to

financial year 2017. Risk relate to non-

accounting of such transactions at arm

length’s price.

Checking minutes of board meeting

relating to the business transactions done

with related parties.

Questioning management and obtaining

written confirmation from them verifying

conduct of related party transactions at

arm’s length price.

Section 2

Analytical review

The following table provides a preliminary analytical review of the financial information of

Mineral Resources Limited for period 2015 to 2018:

RATIO FORMULA MINERAL RESOURCES

LIMITED

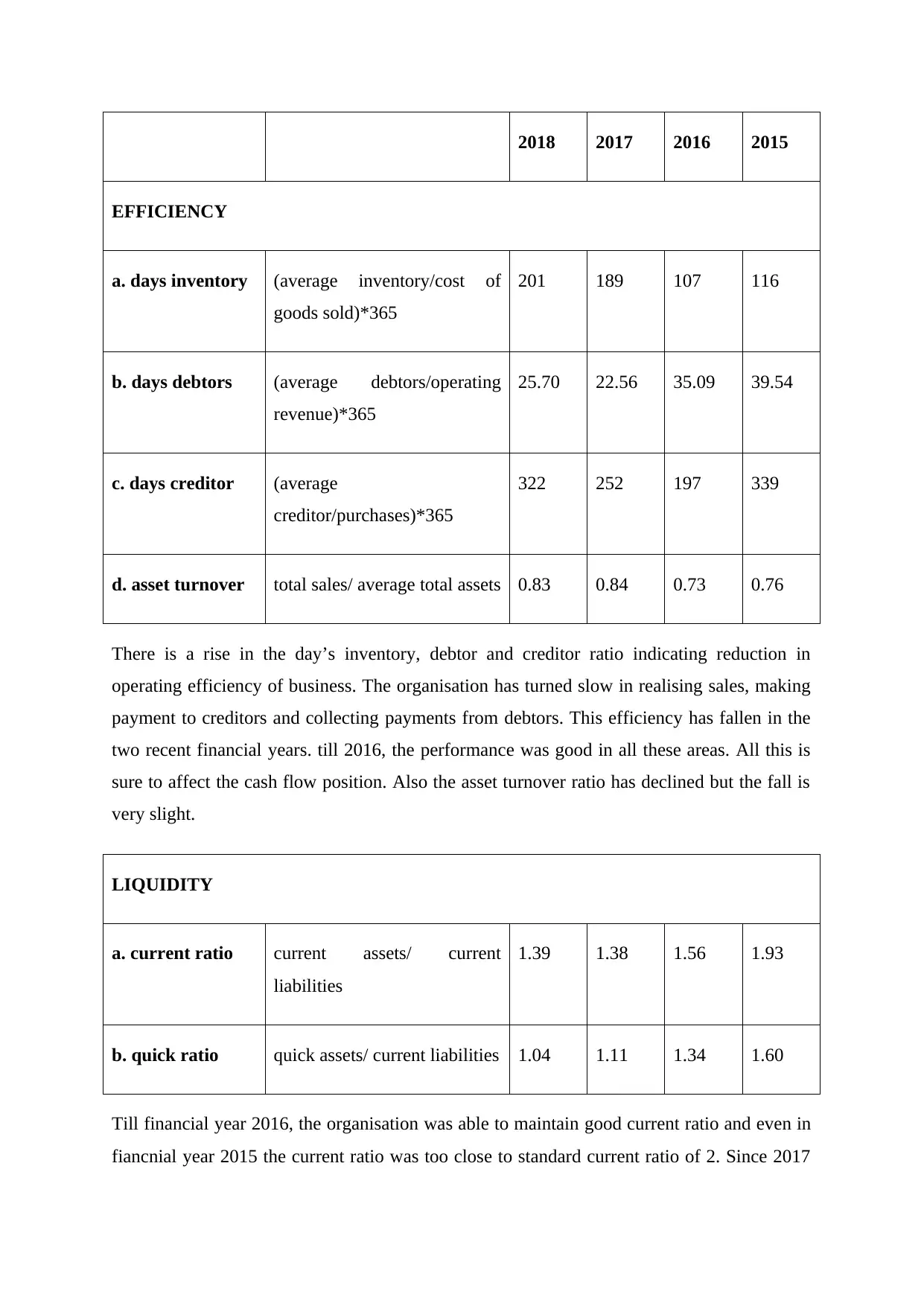

2018 2017 2016 2015

EFFICIENCY

a. days inventory (average inventory/cost of

goods sold)*365

201 189 107 116

b. days debtors (average debtors/operating

revenue)*365

25.70 22.56 35.09 39.54

c. days creditor (average

creditor/purchases)*365

322 252 197 339

d. asset turnover total sales/ average total assets 0.83 0.84 0.73 0.76

There is a rise in the day’s inventory, debtor and creditor ratio indicating reduction in

operating efficiency of business. The organisation has turned slow in realising sales, making

payment to creditors and collecting payments from debtors. This efficiency has fallen in the

two recent financial years. till 2016, the performance was good in all these areas. All this is

sure to affect the cash flow position. Also the asset turnover ratio has declined but the fall is

very slight.

LIQUIDITY

a. current ratio current assets/ current

liabilities

1.39 1.38 1.56 1.93

b. quick ratio quick assets/ current liabilities 1.04 1.11 1.34 1.60

Till financial year 2016, the organisation was able to maintain good current ratio and even in

fiancnial year 2015 the current ratio was too close to standard current ratio of 2. Since 2017

EFFICIENCY

a. days inventory (average inventory/cost of

goods sold)*365

201 189 107 116

b. days debtors (average debtors/operating

revenue)*365

25.70 22.56 35.09 39.54

c. days creditor (average

creditor/purchases)*365

322 252 197 339

d. asset turnover total sales/ average total assets 0.83 0.84 0.73 0.76

There is a rise in the day’s inventory, debtor and creditor ratio indicating reduction in

operating efficiency of business. The organisation has turned slow in realising sales, making

payment to creditors and collecting payments from debtors. This efficiency has fallen in the

two recent financial years. till 2016, the performance was good in all these areas. All this is

sure to affect the cash flow position. Also the asset turnover ratio has declined but the fall is

very slight.

LIQUIDITY

a. current ratio current assets/ current

liabilities

1.39 1.38 1.56 1.93

b. quick ratio quick assets/ current liabilities 1.04 1.11 1.34 1.60

Till financial year 2016, the organisation was able to maintain good current ratio and even in

fiancnial year 2015 the current ratio was too close to standard current ratio of 2. Since 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

both current and quick ratio started to fall, indicating lesser current assets to comply with

current obligations. A doubt is raised upon the short term liquidity of the organisation.

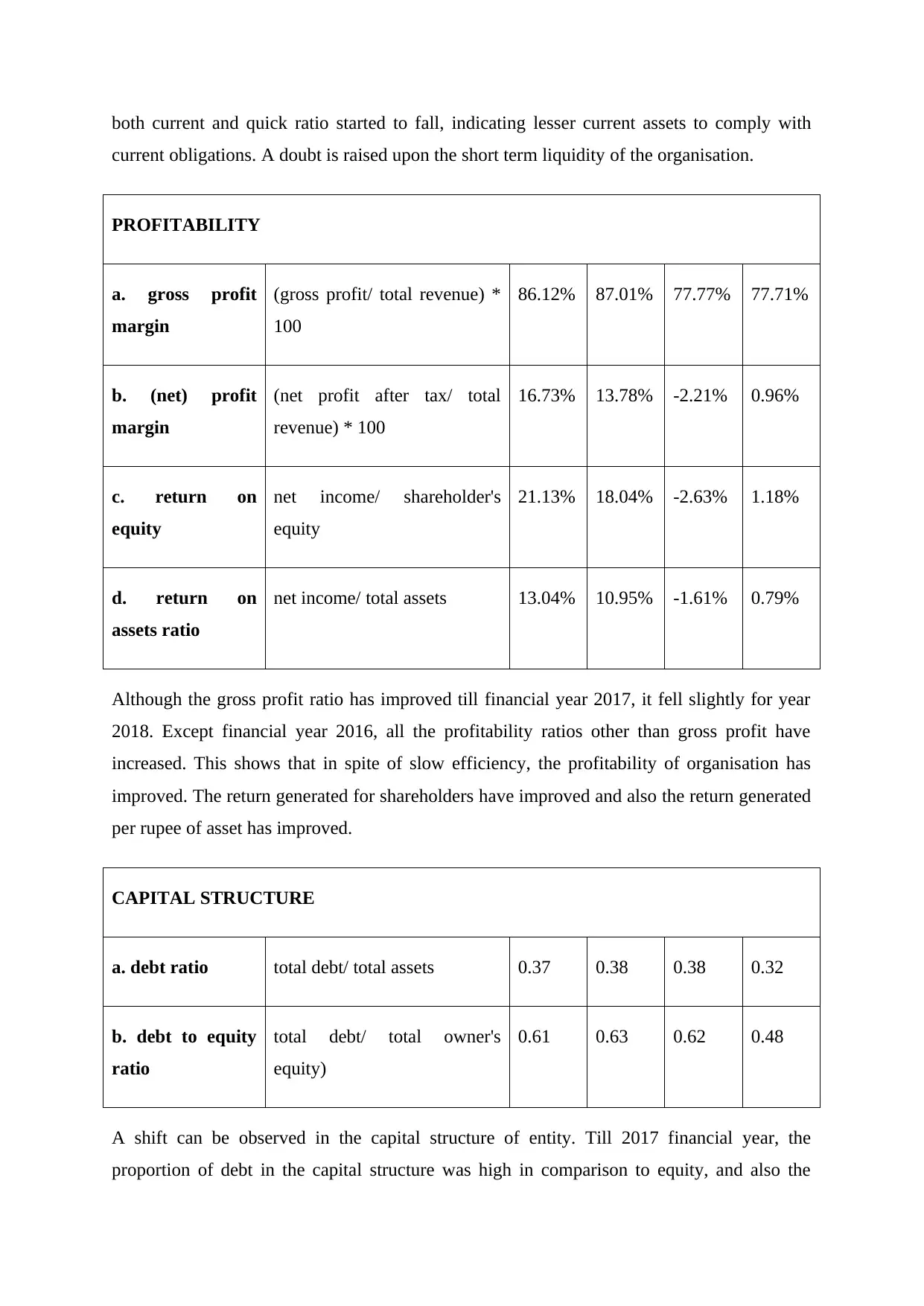

PROFITABILITY

a. gross profit

margin

(gross profit/ total revenue) *

100

86.12% 87.01% 77.77% 77.71%

b. (net) profit

margin

(net profit after tax/ total

revenue) * 100

16.73% 13.78% -2.21% 0.96%

c. return on

equity

net income/ shareholder's

equity

21.13% 18.04% -2.63% 1.18%

d. return on

assets ratio

net income/ total assets 13.04% 10.95% -1.61% 0.79%

Although the gross profit ratio has improved till financial year 2017, it fell slightly for year

2018. Except financial year 2016, all the profitability ratios other than gross profit have

increased. This shows that in spite of slow efficiency, the profitability of organisation has

improved. The return generated for shareholders have improved and also the return generated

per rupee of asset has improved.

CAPITAL STRUCTURE

a. debt ratio total debt/ total assets 0.37 0.38 0.38 0.32

b. debt to equity

ratio

total debt/ total owner's

equity)

0.61 0.63 0.62 0.48

A shift can be observed in the capital structure of entity. Till 2017 financial year, the

proportion of debt in the capital structure was high in comparison to equity, and also the

current obligations. A doubt is raised upon the short term liquidity of the organisation.

PROFITABILITY

a. gross profit

margin

(gross profit/ total revenue) *

100

86.12% 87.01% 77.77% 77.71%

b. (net) profit

margin

(net profit after tax/ total

revenue) * 100

16.73% 13.78% -2.21% 0.96%

c. return on

equity

net income/ shareholder's

equity

21.13% 18.04% -2.63% 1.18%

d. return on

assets ratio

net income/ total assets 13.04% 10.95% -1.61% 0.79%

Although the gross profit ratio has improved till financial year 2017, it fell slightly for year

2018. Except financial year 2016, all the profitability ratios other than gross profit have

increased. This shows that in spite of slow efficiency, the profitability of organisation has

improved. The return generated for shareholders have improved and also the return generated

per rupee of asset has improved.

CAPITAL STRUCTURE

a. debt ratio total debt/ total assets 0.37 0.38 0.38 0.32

b. debt to equity

ratio

total debt/ total owner's

equity)

0.61 0.63 0.62 0.48

A shift can be observed in the capital structure of entity. Till 2017 financial year, the

proportion of debt in the capital structure was high in comparison to equity, and also the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

percentage of assets as financed by external debt was also high. In financial year 2018, a

slight fall is observed in the proportion of debt in business as compared to equity.

Key risk area, audit assertion at risk and audit procedure

Based upon the analytical review of financial statements and the materiality level computed,

the key risk areas, audit assertion at risk and related audit procedures are determined as

follows:

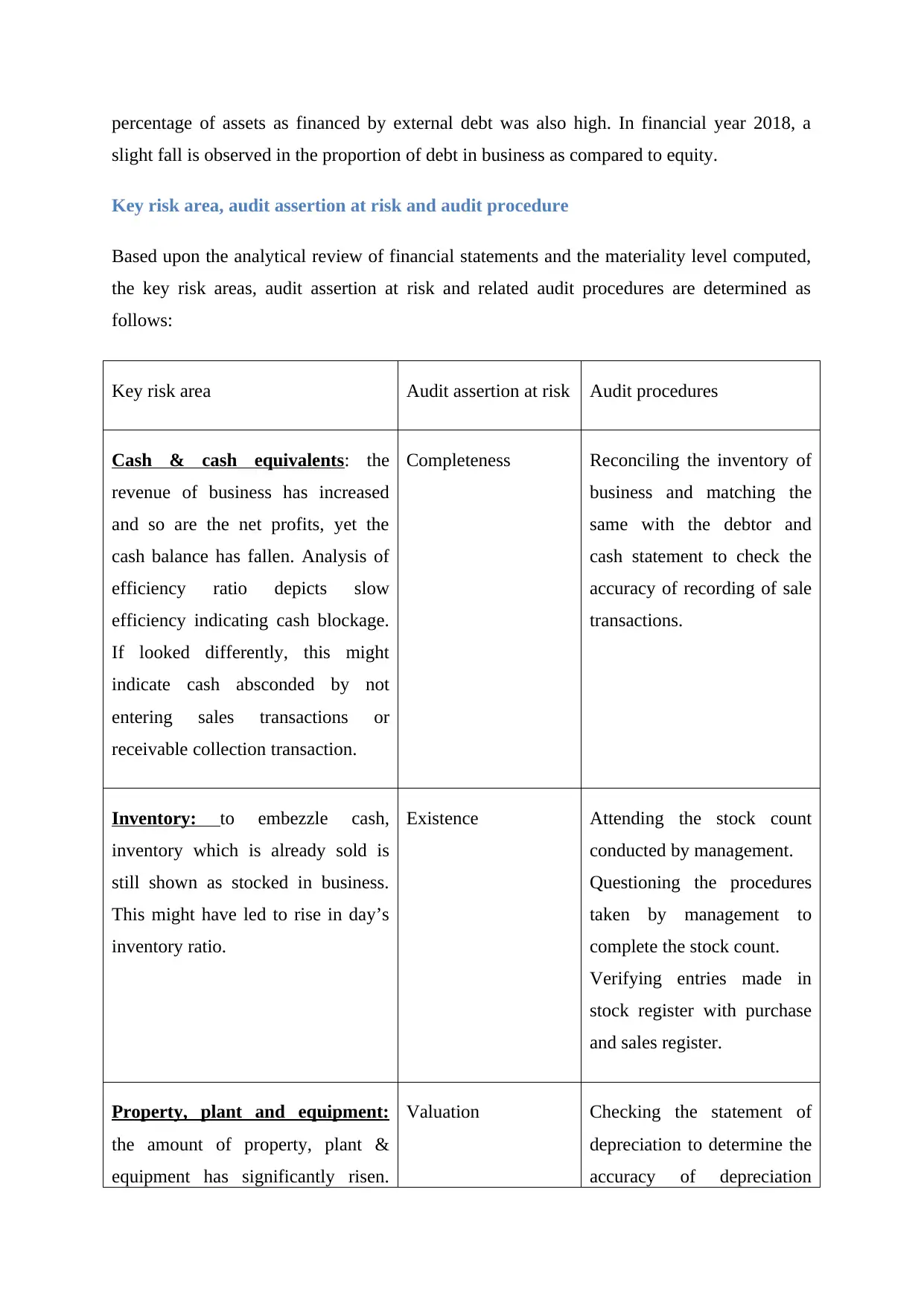

Key risk area Audit assertion at risk Audit procedures

Cash & cash equivalents: the

revenue of business has increased

and so are the net profits, yet the

cash balance has fallen. Analysis of

efficiency ratio depicts slow

efficiency indicating cash blockage.

If looked differently, this might

indicate cash absconded by not

entering sales transactions or

receivable collection transaction.

Completeness Reconciling the inventory of

business and matching the

same with the debtor and

cash statement to check the

accuracy of recording of sale

transactions.

Inventory: to embezzle cash,

inventory which is already sold is

still shown as stocked in business.

This might have led to rise in day’s

inventory ratio.

Existence Attending the stock count

conducted by management.

Questioning the procedures

taken by management to

complete the stock count.

Verifying entries made in

stock register with purchase

and sales register.

Property, plant and equipment:

the amount of property, plant &

equipment has significantly risen.

Valuation Checking the statement of

depreciation to determine the

accuracy of depreciation

slight fall is observed in the proportion of debt in business as compared to equity.

Key risk area, audit assertion at risk and audit procedure

Based upon the analytical review of financial statements and the materiality level computed,

the key risk areas, audit assertion at risk and related audit procedures are determined as

follows:

Key risk area Audit assertion at risk Audit procedures

Cash & cash equivalents: the

revenue of business has increased

and so are the net profits, yet the

cash balance has fallen. Analysis of

efficiency ratio depicts slow

efficiency indicating cash blockage.

If looked differently, this might

indicate cash absconded by not

entering sales transactions or

receivable collection transaction.

Completeness Reconciling the inventory of

business and matching the

same with the debtor and

cash statement to check the

accuracy of recording of sale

transactions.

Inventory: to embezzle cash,

inventory which is already sold is

still shown as stocked in business.

This might have led to rise in day’s

inventory ratio.

Existence Attending the stock count

conducted by management.

Questioning the procedures

taken by management to

complete the stock count.

Verifying entries made in

stock register with purchase

and sales register.

Property, plant and equipment:

the amount of property, plant &

equipment has significantly risen.

Valuation Checking the statement of

depreciation to determine the

accuracy of depreciation

The business has earned profits, yet

the asset turnover has fallen. Assets

might have been overvalued.

charged.

Checking asset ownership

documents to analyse the

cost as well as checking the

computation undertaken for

any revaluation.

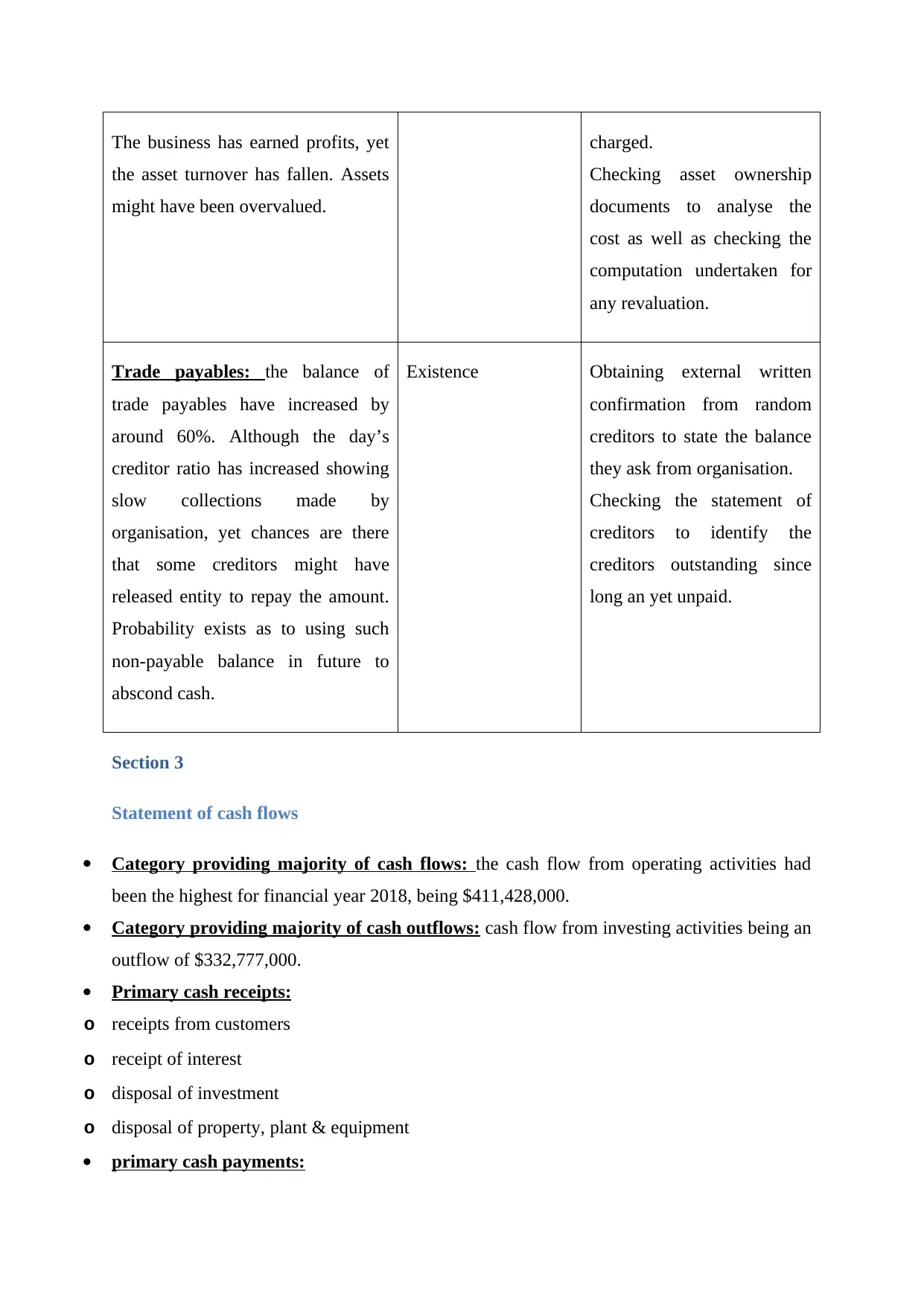

Trade payables: the balance of

trade payables have increased by

around 60%. Although the day’s

creditor ratio has increased showing

slow collections made by

organisation, yet chances are there

that some creditors might have

released entity to repay the amount.

Probability exists as to using such

non-payable balance in future to

abscond cash.

Existence Obtaining external written

confirmation from random

creditors to state the balance

they ask from organisation.

Checking the statement of

creditors to identify the

creditors outstanding since

long an yet unpaid.

Section 3

Statement of cash flows

Category providing majority of cash flows: the cash flow from operating activities had

been the highest for financial year 2018, being $411,428,000.

Category providing majority of cash outflows: cash flow from investing activities being an

outflow of $332,777,000.

Primary cash receipts:

o receipts from customers

o receipt of interest

o disposal of investment

o disposal of property, plant & equipment

primary cash payments:

the asset turnover has fallen. Assets

might have been overvalued.

charged.

Checking asset ownership

documents to analyse the

cost as well as checking the

computation undertaken for

any revaluation.

Trade payables: the balance of

trade payables have increased by

around 60%. Although the day’s

creditor ratio has increased showing

slow collections made by

organisation, yet chances are there

that some creditors might have

released entity to repay the amount.

Probability exists as to using such

non-payable balance in future to

abscond cash.

Existence Obtaining external written

confirmation from random

creditors to state the balance

they ask from organisation.

Checking the statement of

creditors to identify the

creditors outstanding since

long an yet unpaid.

Section 3

Statement of cash flows

Category providing majority of cash flows: the cash flow from operating activities had

been the highest for financial year 2018, being $411,428,000.

Category providing majority of cash outflows: cash flow from investing activities being an

outflow of $332,777,000.

Primary cash receipts:

o receipts from customers

o receipt of interest

o disposal of investment

o disposal of property, plant & equipment

primary cash payments:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

o payment to employees and suppliers

o payment of income tax

o acquisition of investments

o acquisition of property, plant and equipment

o mine development expenditure

o payment of dividends

o repayment of borrowings

Main non-cash financial or investing activities: for Mineral resources Limited, no non-cash

investing or financial activity has been identified in financial year 2018.

Going concern risk for company: from the review of cash flow no risk to going concern is

evident as such. The company’s cash flows have fallen in the year because of new

investments made by company and acquisition of property, plant and equipment. This on the

other hand signals expansion of business, let alone risk to going concern. Also, the

organisation has repaid a large chunk of external borrowings and has switched slightly

towards own money (AICPA., 2017).

Review of audit report

Type of audit opinion

The audit for the financial statements of Mineral Resources Limited is carried by RSM

Australia Partners. The opinion expressed by them on the financials of the company is

unmodified. A clean audit report is issued stating presentation of a true and fair view by the

financial statements of the concern (Eilifsen, Hamilton, & Messier Jr, 2017).

Additional paragraph: Key audit matters

The auditors have included an additional paragraph in their audit report which mentions the

key audit matters identified by them while auditing the financial statements of Mineral

Resources Limited. The issues mentioned in the key audit matter paragraph have been of high

significance as per the judgement of auditor. No separate opinion is expressed on them

however. The issues are discussed as follows (Heikal, Khaddafi, & Ummah, 2014).

1. Carrying value of mine development expenditure and exploration expenditure: the high

volume of judgement involved in respect to amortisation charge, impairment indicators,

o payment of income tax

o acquisition of investments

o acquisition of property, plant and equipment

o mine development expenditure

o payment of dividends

o repayment of borrowings

Main non-cash financial or investing activities: for Mineral resources Limited, no non-cash

investing or financial activity has been identified in financial year 2018.

Going concern risk for company: from the review of cash flow no risk to going concern is

evident as such. The company’s cash flows have fallen in the year because of new

investments made by company and acquisition of property, plant and equipment. This on the

other hand signals expansion of business, let alone risk to going concern. Also, the

organisation has repaid a large chunk of external borrowings and has switched slightly

towards own money (AICPA., 2017).

Review of audit report

Type of audit opinion

The audit for the financial statements of Mineral Resources Limited is carried by RSM

Australia Partners. The opinion expressed by them on the financials of the company is

unmodified. A clean audit report is issued stating presentation of a true and fair view by the

financial statements of the concern (Eilifsen, Hamilton, & Messier Jr, 2017).

Additional paragraph: Key audit matters

The auditors have included an additional paragraph in their audit report which mentions the

key audit matters identified by them while auditing the financial statements of Mineral

Resources Limited. The issues mentioned in the key audit matter paragraph have been of high

significance as per the judgement of auditor. No separate opinion is expressed on them

however. The issues are discussed as follows (Heikal, Khaddafi, & Ummah, 2014).

1. Carrying value of mine development expenditure and exploration expenditure: the high

volume of judgement involved in respect to amortisation charge, impairment indicators,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

recoverable account, impairment risk etc. makes this account a key audit matter and highly

significant for the audit (Aprisilya, & Mawardi, 2016).

2. Provision for site rehabilitation: use of significant judgement, high attached materiality, and

complexity and uncertainty of estimations has made this account a key audit matter.

3. Existence of valuation of inventory: use of judgements significantly to estimate prices of

lithium ore and iron ore, allocation of cost of processing and grading of ores has made this

account a key audit matter. Also the balance pertained to it is material.

In respect of all these key audit matters, extended audit procedures have been undertaken by

the auditors, to resolve the preliminary risk of material misstatement (Barman, & Sengupta,

2017).

Conclusion

This report has shown that the auditors have included an additional paragraph in their

audit report which mentions the key audit matters identified by them while auditing the

financial statements of Mineral Resources Limited. The matching concept has shown that

reconciling the inventory of business and matching the same with the debtor and cash

statement to check the accuracy of recording of sale transactions. The crux of this report

reveals that company has stable audit risk and would be sustainable in long run.

significant for the audit (Aprisilya, & Mawardi, 2016).

2. Provision for site rehabilitation: use of significant judgement, high attached materiality, and

complexity and uncertainty of estimations has made this account a key audit matter.

3. Existence of valuation of inventory: use of judgements significantly to estimate prices of

lithium ore and iron ore, allocation of cost of processing and grading of ores has made this

account a key audit matter. Also the balance pertained to it is material.

In respect of all these key audit matters, extended audit procedures have been undertaken by

the auditors, to resolve the preliminary risk of material misstatement (Barman, & Sengupta,

2017).

Conclusion

This report has shown that the auditors have included an additional paragraph in their

audit report which mentions the key audit matters identified by them while auditing the

financial statements of Mineral Resources Limited. The matching concept has shown that

reconciling the inventory of business and matching the same with the debtor and cash

statement to check the accuracy of recording of sale transactions. The crux of this report

reveals that company has stable audit risk and would be sustainable in long run.

References

AICPA. (2017). Audit guide: Audit sampling. USA: John Wiley & Sons.

Aprisilya, T., & Mawardi, W. (2016). Analisis Pengaruh Total Asset Turnover, Book To Market

Ratio, Debt Equity Ratio Terhadap Expected Return Dengan Trading Volume Acitivity

Sebagai Variabel Intervening (Studi Pada Perusahaan Perbankan yang Terdaftar pada BEI

Periode 2010-2014). Diponegoro Journal of Management, 5(2), 417-430.

Barman, A. N., & Sengupta, P. P. (2017). DETERMINANTS OF PROFITABILITY IN INDIAN

TELECOM INDUSTRY USING FINANCIAL RATIO ANALYSIS. International Journal

of Research in Management & Social Science, 25.

Eilifsen, A., Hamilton, E. L., & Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures

on Investors’ Judgments and Decisions. 4(12), 101.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets (ROA), return

on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lakis, V., & Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR USERS OF

FINANCIAL STATEMENTS. Journal of Management, 2(31).

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for managers. New

York: McGraw-Hill/Irwin.

Ruhnke, K., Pronobis, P., & Michel, M. (2018). Effects of Audit Materiality Disclosures: Evidence

from Credit Lending Decision Adjustments. Betriebswirtschaftliche Forschung und Praxis

(BFuP), 70(4), 440-471.

Ussery, E. N., Omura, J. D., Paul, P., Orr, J., Spoon, C., Geremia, C., & Carlson, S. A. (2019).

Sampling methodology and reliability of a representative walkability audit. Journal of

Transport & Health, 12, 75-85.

AICPA. (2017). Audit guide: Audit sampling. USA: John Wiley & Sons.

Aprisilya, T., & Mawardi, W. (2016). Analisis Pengaruh Total Asset Turnover, Book To Market

Ratio, Debt Equity Ratio Terhadap Expected Return Dengan Trading Volume Acitivity

Sebagai Variabel Intervening (Studi Pada Perusahaan Perbankan yang Terdaftar pada BEI

Periode 2010-2014). Diponegoro Journal of Management, 5(2), 417-430.

Barman, A. N., & Sengupta, P. P. (2017). DETERMINANTS OF PROFITABILITY IN INDIAN

TELECOM INDUSTRY USING FINANCIAL RATIO ANALYSIS. International Journal

of Research in Management & Social Science, 25.

Eilifsen, A., Hamilton, E. L., & Messier Jr, W. F. (2017). The Importance of Quantifying

Uncertainty: Examining the Effect of Audit Materiality and Sensitivity Analysis Disclosures

on Investors’ Judgments and Decisions. 4(12), 101.

Heikal, M., Khaddafi, M., & Ummah, A. (2014). Influence analysis of return on assets (ROA), return

on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and current ratio

(CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12), 101.

Lakis, V., & Masiulevičius, A. (2017). ACCEPTABLE AUDIT MATERIALITY FOR USERS OF

FINANCIAL STATEMENTS. Journal of Management, 2(31).

Noreen, E. W., Brewer, P. C., & Garrison, R. H. (2014). Managerial accounting for managers. New

York: McGraw-Hill/Irwin.

Ruhnke, K., Pronobis, P., & Michel, M. (2018). Effects of Audit Materiality Disclosures: Evidence

from Credit Lending Decision Adjustments. Betriebswirtschaftliche Forschung und Praxis

(BFuP), 70(4), 440-471.

Ussery, E. N., Omura, J. D., Paul, P., Orr, J., Spoon, C., Geremia, C., & Carlson, S. A. (2019).

Sampling methodology and reliability of a representative walkability audit. Journal of

Transport & Health, 12, 75-85.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.