Auditing and Assurance: Reviewing Financial Statement Integrity

VerifiedAdded on 2023/04/24

|18

|2795

|186

Homework Assignment

AI Summary

This assignment solution covers various aspects of auditing and assurance, including ethical considerations, financial statement analysis, and fraud detection. It addresses specific questions related to auditor responsibilities, transaction-related audit objectives, and the reliability of different types of audit evidence. The solution also explores analytical procedures for enhancing audit quality and provides insights into potential misstatements and fraud risks within financial reports. Key areas covered include the assessment of internal controls, the confirmation of account balances, and the importance of independent evidence in forming audit opinions. The document provides detailed explanations and examples, offering a comprehensive understanding of auditing principles and practices. Desklib offers a platform for students to access similar solved assignments and past papers.

Running head: AUDITING AND ASSURANCE

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Auditing and Assurance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

Table of Contents

Question 5-23:.................................................................................................................................3

Requirement a:.............................................................................................................................3

Requirement b:.............................................................................................................................3

Requirement c:.............................................................................................................................3

Question 5-24:.................................................................................................................................3

Requirement 1:.............................................................................................................................3

Requirement 2:.............................................................................................................................4

Requirement 3:.............................................................................................................................4

Requirement 4:.............................................................................................................................4

Requirement 5:.............................................................................................................................4

Requirement 6:.............................................................................................................................4

Question 6-23:.................................................................................................................................4

Requirement a:.............................................................................................................................4

Requirement b:.............................................................................................................................4

Requirement c:.............................................................................................................................5

Question 6-27:.................................................................................................................................5

Requirement a:.............................................................................................................................5

Requirements b and c:.................................................................................................................6

Table of Contents

Question 5-23:.................................................................................................................................3

Requirement a:.............................................................................................................................3

Requirement b:.............................................................................................................................3

Requirement c:.............................................................................................................................3

Question 5-24:.................................................................................................................................3

Requirement 1:.............................................................................................................................3

Requirement 2:.............................................................................................................................4

Requirement 3:.............................................................................................................................4

Requirement 4:.............................................................................................................................4

Requirement 5:.............................................................................................................................4

Requirement 6:.............................................................................................................................4

Question 6-23:.................................................................................................................................4

Requirement a:.............................................................................................................................4

Requirement b:.............................................................................................................................4

Requirement c:.............................................................................................................................5

Question 6-27:.................................................................................................................................5

Requirement a:.............................................................................................................................5

Requirements b and c:.................................................................................................................6

2AUDITING AND ASSURANCE

Question 11-30:...............................................................................................................................6

Question 7-27:.................................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................8

Question 7-30:.................................................................................................................................9

Requirement a:.............................................................................................................................9

Requirement b:.............................................................................................................................9

Requirement c:.............................................................................................................................9

Requirement d:.............................................................................................................................9

Requirement e:.............................................................................................................................9

Requirement f:...........................................................................................................................10

Requirement g:...........................................................................................................................10

Question 7-31:...............................................................................................................................11

Question 8-22:...............................................................................................................................13

Question 8-33:...............................................................................................................................13

Requirement a:...........................................................................................................................13

Requirement b:...........................................................................................................................14

Question 9-33:...............................................................................................................................14

References:....................................................................................................................................16

Question 11-30:...............................................................................................................................6

Question 7-27:.................................................................................................................................7

Requirement a:.............................................................................................................................7

Requirement b:.............................................................................................................................8

Question 7-30:.................................................................................................................................9

Requirement a:.............................................................................................................................9

Requirement b:.............................................................................................................................9

Requirement c:.............................................................................................................................9

Requirement d:.............................................................................................................................9

Requirement e:.............................................................................................................................9

Requirement f:...........................................................................................................................10

Requirement g:...........................................................................................................................10

Question 7-31:...............................................................................................................................11

Question 8-22:...............................................................................................................................13

Question 8-33:...............................................................................................................................13

Requirement a:...........................................................................................................................13

Requirement b:...........................................................................................................................14

Question 9-33:...............................................................................................................................14

References:....................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

Question 5-23:

Requirement a:

Chen has the liability towards the bank, since it is evident that the bank would be

utilizing the financial statements for undertaking decision on issuing the loan. Chen has the full

knowledge that the bank has been taking decision depending on the audited financial statements

and the report has been issued by using wrong information. Even though there is presence of

documents for backing up this report, this situation is unethical, as Chen has complete

knowledge of all wrongdoings.

Requirement b:

Chen has the obligation towards the lessor, as the latter is an estimated user of the audited

financial statements (Ahmed Haji & Anifowose, 2016). Despite the fact that Chen has been

unaware of the lessor, the latter falls under the category of reasonably limited and identifiable

user groups relying on the work of the auditor.

Requirement c:

Chen knew that the financial statements are not prepared in accordance with GAAP and

despite such problem; an unqualified audit opinion has been issued. Thus, criminal allegations

could be brought against Chen, since he has submitted wrong financial documents deliberately.

The act could be categorized as criminal act, as there has been the motive to deceive.

Question 5-24:

Requirement 1:

Option c

Question 5-23:

Requirement a:

Chen has the liability towards the bank, since it is evident that the bank would be

utilizing the financial statements for undertaking decision on issuing the loan. Chen has the full

knowledge that the bank has been taking decision depending on the audited financial statements

and the report has been issued by using wrong information. Even though there is presence of

documents for backing up this report, this situation is unethical, as Chen has complete

knowledge of all wrongdoings.

Requirement b:

Chen has the obligation towards the lessor, as the latter is an estimated user of the audited

financial statements (Ahmed Haji & Anifowose, 2016). Despite the fact that Chen has been

unaware of the lessor, the latter falls under the category of reasonably limited and identifiable

user groups relying on the work of the auditor.

Requirement c:

Chen knew that the financial statements are not prepared in accordance with GAAP and

despite such problem; an unqualified audit opinion has been issued. Thus, criminal allegations

could be brought against Chen, since he has submitted wrong financial documents deliberately.

The act could be categorized as criminal act, as there has been the motive to deceive.

Question 5-24:

Requirement 1:

Option c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

Requirement 2:

Option c

Requirement 3:

Option d

Requirement 4:

Option d

Requirement 5:

Option b

Requirement 6:

Option b

Question 6-23:

Requirement a:

Reasonable assurance could be identified as greater assurance level, which is denoted by

the auditing standards. The users need to contain increased degree of confidence in the financial

reports. Reasonable assurance is an absolute assurance level, since there are some minimum risks

that there might be material misstatements in the audited financial reports (Chambers & Odar,

2015).

Requirement b:

The independent auditors have the responsibility to provide an opinion on the audited

financial reports. Thus, they are needed to check the adequacy and accuracy of the financial

statements by adhering to the necessary auditing standards based on which they should provide

Requirement 2:

Option c

Requirement 3:

Option d

Requirement 4:

Option d

Requirement 5:

Option b

Requirement 6:

Option b

Question 6-23:

Requirement a:

Reasonable assurance could be identified as greater assurance level, which is denoted by

the auditing standards. The users need to contain increased degree of confidence in the financial

reports. Reasonable assurance is an absolute assurance level, since there are some minimum risks

that there might be material misstatements in the audited financial reports (Chambers & Odar,

2015).

Requirement b:

The independent auditors have the responsibility to provide an opinion on the audited

financial reports. Thus, they are needed to check the adequacy and accuracy of the financial

statements by adhering to the necessary auditing standards based on which they should provide

5AUDITING AND ASSURANCE

their opinion. At the time of representing in the form of independent auditors, they need to

possess the capabilities of being qualified individuals in the profession. Such qualities do not

include appraiser, insurer, lawyer or expert in materials.

Requirement c:

An auditor is liable to gain reasonable assurance that significant misstatements engaged

in the statement are identified to find out whether they are due to errors or frauds. More

precisely, frauds are difficult to be detected than errors, since the management or staffs

conducting fraud would try to conceal the same; however, the auditor has to overcome this

difficulty at the time of planning the audit process.

The auditor needs to uncover situations when audits are performed leading to doubts or

fraudulent financial reporting. The auditor generally analyses the chance of considerable

misappropriation of assets as a part of insight of internal control along with analyzing control

risk. The evidences need to be described at the time the auditor fails to comply with the

necessary guidelines or to consider substantial fraud (Christensen, Glover & Wolfe, 2014).

Question 6-27:

Requirement a:

General transaction-related audit objectives:

These objectives assist in providing a detailed structure through which the auditors could

gather competent evidence. The auditors formulate audit objectives after the management

assertions are identified appropriately. These objectives have close relationships with

management assertions.

Management assertions about classes of transactions and events:

their opinion. At the time of representing in the form of independent auditors, they need to

possess the capabilities of being qualified individuals in the profession. Such qualities do not

include appraiser, insurer, lawyer or expert in materials.

Requirement c:

An auditor is liable to gain reasonable assurance that significant misstatements engaged

in the statement are identified to find out whether they are due to errors or frauds. More

precisely, frauds are difficult to be detected than errors, since the management or staffs

conducting fraud would try to conceal the same; however, the auditor has to overcome this

difficulty at the time of planning the audit process.

The auditor needs to uncover situations when audits are performed leading to doubts or

fraudulent financial reporting. The auditor generally analyses the chance of considerable

misappropriation of assets as a part of insight of internal control along with analyzing control

risk. The evidences need to be described at the time the auditor fails to comply with the

necessary guidelines or to consider substantial fraud (Christensen, Glover & Wolfe, 2014).

Question 6-27:

Requirement a:

General transaction-related audit objectives:

These objectives assist in providing a detailed structure through which the auditors could

gather competent evidence. The auditors formulate audit objectives after the management

assertions are identified appropriately. These objectives have close relationships with

management assertions.

Management assertions about classes of transactions and events:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

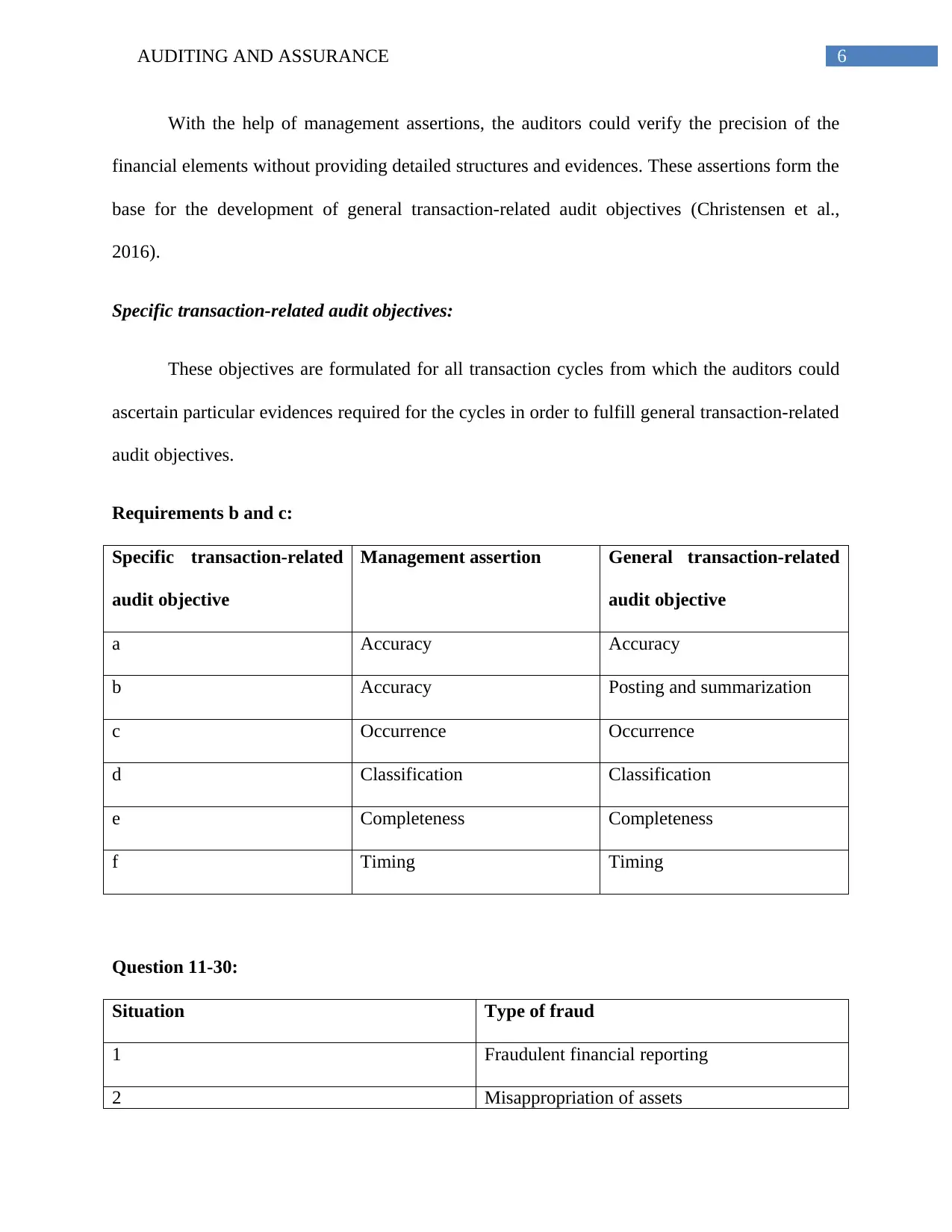

With the help of management assertions, the auditors could verify the precision of the

financial elements without providing detailed structures and evidences. These assertions form the

base for the development of general transaction-related audit objectives (Christensen et al.,

2016).

Specific transaction-related audit objectives:

These objectives are formulated for all transaction cycles from which the auditors could

ascertain particular evidences required for the cycles in order to fulfill general transaction-related

audit objectives.

Requirements b and c:

Specific transaction-related

audit objective

Management assertion General transaction-related

audit objective

a Accuracy Accuracy

b Accuracy Posting and summarization

c Occurrence Occurrence

d Classification Classification

e Completeness Completeness

f Timing Timing

Question 11-30:

Situation Type of fraud

1 Fraudulent financial reporting

2 Misappropriation of assets

With the help of management assertions, the auditors could verify the precision of the

financial elements without providing detailed structures and evidences. These assertions form the

base for the development of general transaction-related audit objectives (Christensen et al.,

2016).

Specific transaction-related audit objectives:

These objectives are formulated for all transaction cycles from which the auditors could

ascertain particular evidences required for the cycles in order to fulfill general transaction-related

audit objectives.

Requirements b and c:

Specific transaction-related

audit objective

Management assertion General transaction-related

audit objective

a Accuracy Accuracy

b Accuracy Posting and summarization

c Occurrence Occurrence

d Classification Classification

e Completeness Completeness

f Timing Timing

Question 11-30:

Situation Type of fraud

1 Fraudulent financial reporting

2 Misappropriation of assets

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

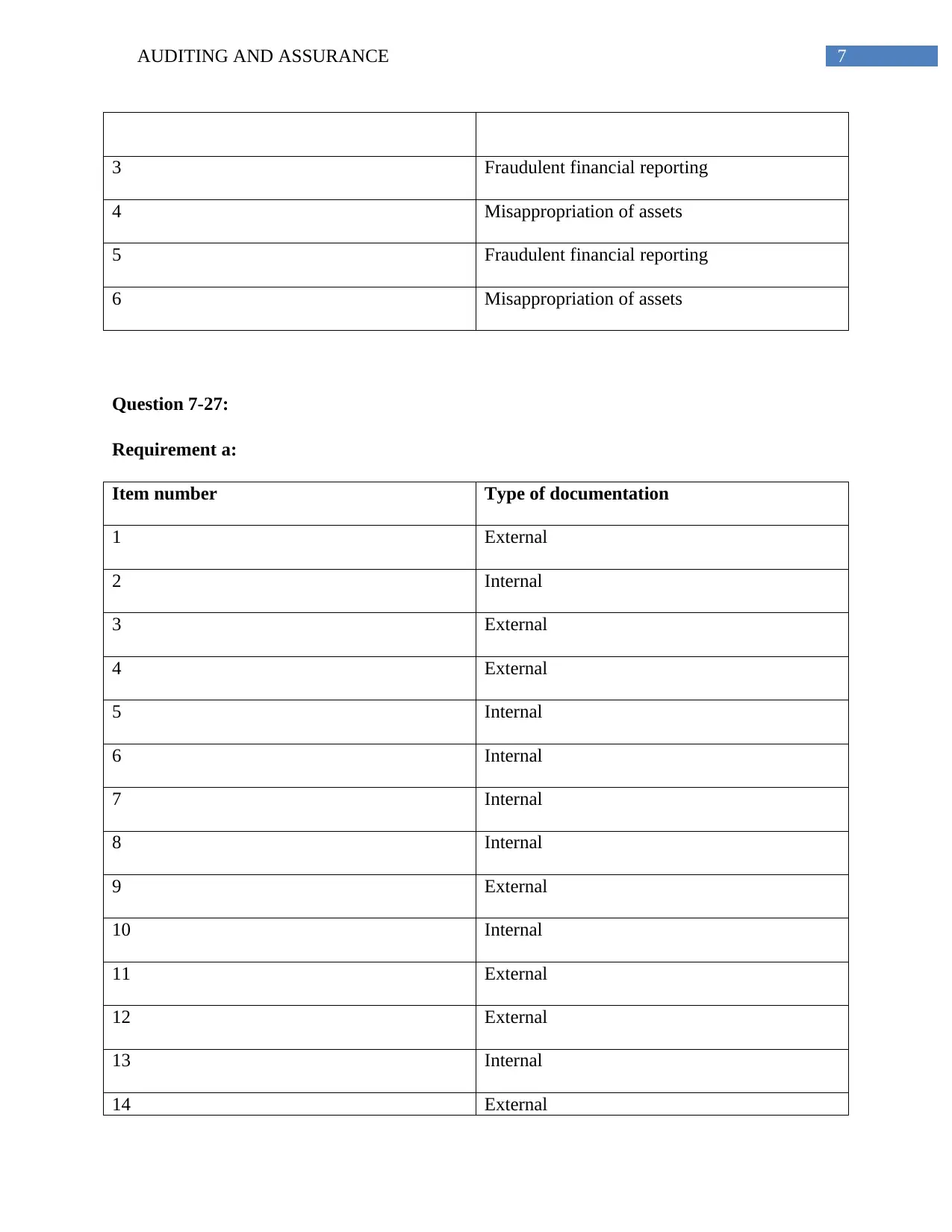

3 Fraudulent financial reporting

4 Misappropriation of assets

5 Fraudulent financial reporting

6 Misappropriation of assets

Question 7-27:

Requirement a:

Item number Type of documentation

1 External

2 Internal

3 External

4 External

5 Internal

6 Internal

7 Internal

8 Internal

9 External

10 Internal

11 External

12 External

13 Internal

14 External

3 Fraudulent financial reporting

4 Misappropriation of assets

5 Fraudulent financial reporting

6 Misappropriation of assets

Question 7-27:

Requirement a:

Item number Type of documentation

1 External

2 Internal

3 External

4 External

5 Internal

6 Internal

7 Internal

8 Internal

9 External

10 Internal

11 External

12 External

13 Internal

14 External

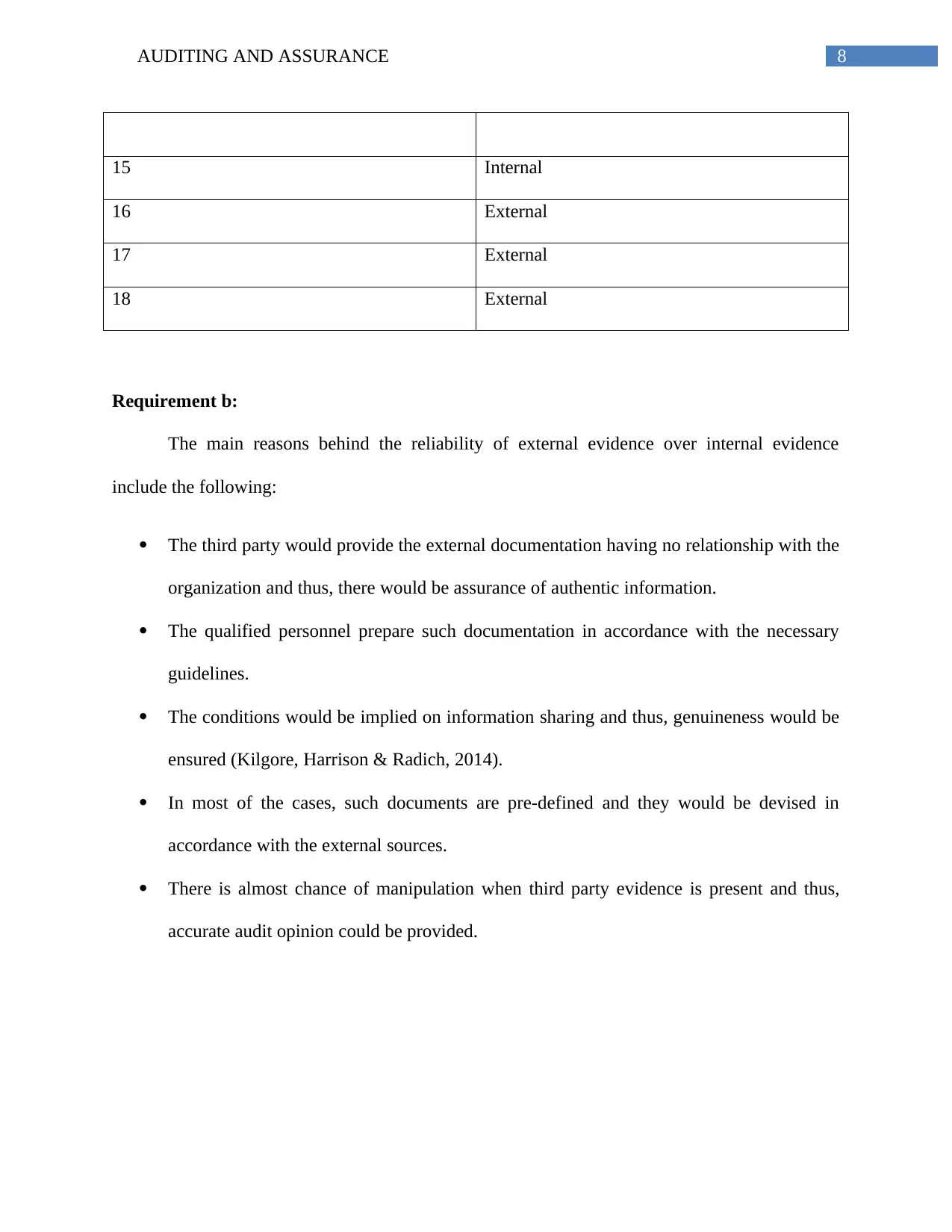

8AUDITING AND ASSURANCE

15 Internal

16 External

17 External

18 External

Requirement b:

The main reasons behind the reliability of external evidence over internal evidence

include the following:

The third party would provide the external documentation having no relationship with the

organization and thus, there would be assurance of authentic information.

The qualified personnel prepare such documentation in accordance with the necessary

guidelines.

The conditions would be implied on information sharing and thus, genuineness would be

ensured (Kilgore, Harrison & Radich, 2014).

In most of the cases, such documents are pre-defined and they would be devised in

accordance with the external sources.

There is almost chance of manipulation when third party evidence is present and thus,

accurate audit opinion could be provided.

15 Internal

16 External

17 External

18 External

Requirement b:

The main reasons behind the reliability of external evidence over internal evidence

include the following:

The third party would provide the external documentation having no relationship with the

organization and thus, there would be assurance of authentic information.

The qualified personnel prepare such documentation in accordance with the necessary

guidelines.

The conditions would be implied on information sharing and thus, genuineness would be

ensured (Kilgore, Harrison & Radich, 2014).

In most of the cases, such documents are pre-defined and they would be devised in

accordance with the external sources.

There is almost chance of manipulation when third party evidence is present and thus,

accurate audit opinion could be provided.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

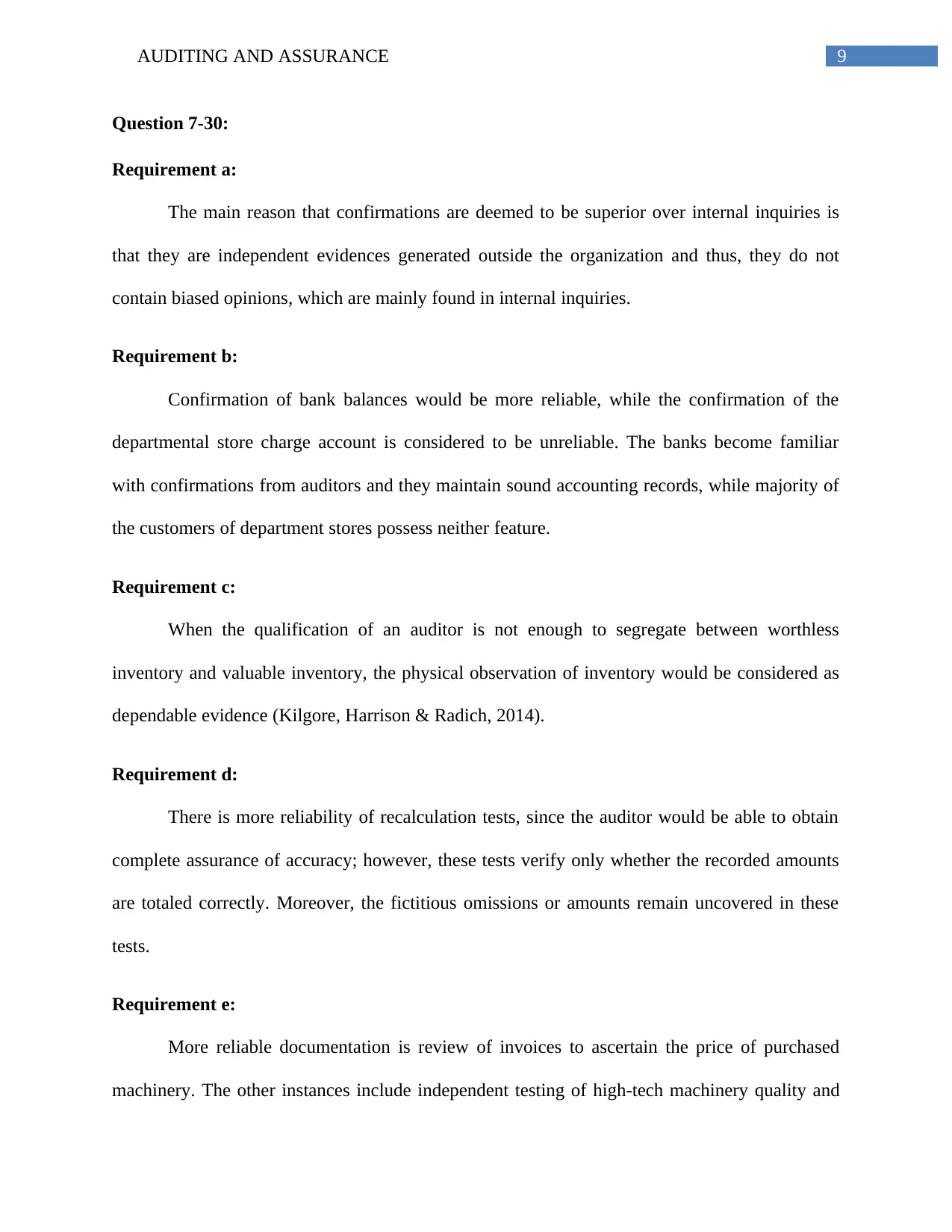

Question 7-30:

Requirement a:

The main reason that confirmations are deemed to be superior over internal inquiries is

that they are independent evidences generated outside the organization and thus, they do not

contain biased opinions, which are mainly found in internal inquiries.

Requirement b:

Confirmation of bank balances would be more reliable, while the confirmation of the

departmental store charge account is considered to be unreliable. The banks become familiar

with confirmations from auditors and they maintain sound accounting records, while majority of

the customers of department stores possess neither feature.

Requirement c:

When the qualification of an auditor is not enough to segregate between worthless

inventory and valuable inventory, the physical observation of inventory would be considered as

dependable evidence (Kilgore, Harrison & Radich, 2014).

Requirement d:

There is more reliability of recalculation tests, since the auditor would be able to obtain

complete assurance of accuracy; however, these tests verify only whether the recorded amounts

are totaled correctly. Moreover, the fictitious omissions or amounts remain uncovered in these

tests.

Requirement e:

More reliable documentation is review of invoices to ascertain the price of purchased

machinery. The other instances include independent testing of high-tech machinery quality and

Question 7-30:

Requirement a:

The main reason that confirmations are deemed to be superior over internal inquiries is

that they are independent evidences generated outside the organization and thus, they do not

contain biased opinions, which are mainly found in internal inquiries.

Requirement b:

Confirmation of bank balances would be more reliable, while the confirmation of the

departmental store charge account is considered to be unreliable. The banks become familiar

with confirmations from auditors and they maintain sound accounting records, while majority of

the customers of department stores possess neither feature.

Requirement c:

When the qualification of an auditor is not enough to segregate between worthless

inventory and valuable inventory, the physical observation of inventory would be considered as

dependable evidence (Kilgore, Harrison & Radich, 2014).

Requirement d:

There is more reliability of recalculation tests, since the auditor would be able to obtain

complete assurance of accuracy; however, these tests verify only whether the recorded amounts

are totaled correctly. Moreover, the fictitious omissions or amounts remain uncovered in these

tests.

Requirement e:

More reliable documentation is review of invoices to ascertain the price of purchased

machinery. The other instances include independent testing of high-tech machinery quality and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE

confirming accounts receivable from a significant customer having long standing business

relationship with the client. On the other hand, less reliable evidence could be the visual

inspection of high-tech machinery. The other evidences include confirming accounts receivable

from a local customer of electric utility and schedule of construction cost of management to

make an addition to existing inventory.

The below-stated characteristics differentiate the two aspects:

Objective, independent and outside documentation such as invoices of the vendor

compared to the scheduled cost of construction of the management

Data audited in the past in opposition to similar data, which have not been audited

previously

Independent information of appraisal given by appropriate appraisers compared to

internally generated management assumptions (Knechel, 2016).

Requirement f:

The examples include investigation of corporate minutes, in which experienced partner

would be required compared to a new assistant. Some other instances include attorney’s letter

where the use of general counsel would be made in contrast to the attorney engaged only with

the patents and confirming trade receivables where organizations become familiar to

confirmations compared to the general public members.

Requirement g:

Analytical procedures are described as evidences of the occurrence of misstatements in

the financial reports; however, they are not adequate to infer the misstatements of reports. Thus,

confirming accounts receivable from a significant customer having long standing business

relationship with the client. On the other hand, less reliable evidence could be the visual

inspection of high-tech machinery. The other evidences include confirming accounts receivable

from a local customer of electric utility and schedule of construction cost of management to

make an addition to existing inventory.

The below-stated characteristics differentiate the two aspects:

Objective, independent and outside documentation such as invoices of the vendor

compared to the scheduled cost of construction of the management

Data audited in the past in opposition to similar data, which have not been audited

previously

Independent information of appraisal given by appropriate appraisers compared to

internally generated management assumptions (Knechel, 2016).

Requirement f:

The examples include investigation of corporate minutes, in which experienced partner

would be required compared to a new assistant. Some other instances include attorney’s letter

where the use of general counsel would be made in contrast to the attorney engaged only with

the patents and confirming trade receivables where organizations become familiar to

confirmations compared to the general public members.

Requirement g:

Analytical procedures are described as evidences of the occurrence of misstatements in

the financial reports; however, they are not adequate to infer the misstatements of reports. Thus,

11AUDITING AND ASSURANCE

other supporting evidences are required for ascertaining whether the misstatements are material

(Knechel & Salterio, 2016).

Question 7-31:

Account Name From Whom Confirmed Information to Be Confirmed

Cash at bank Cash transactions occurred in the

year to be confirmed by the

individual responsible for

entering all transactions

1. Bank information such as type and

nature of the bank

2. The amounts deposited in all

accounts

3. Account balance at the end of the

year

4. Names of account

5. Information related to cash

drawings and rates of interest

Trade accounts receivable Confirmation of trade

receivables to be made through

verification of a sample account

1. Debtors’ personal information

2. Account numbers

3. Particular date confirmation

4. Balance of invoices with dates

Inventories Confirmation of inventory

account to be made by the

warehouse custodian

1. Warehouse-related transaction

information

2. Detailed inventory list

3. Balance of inventory at specific

date

Trade accounts payable Verification of payable 1. Supplier information

other supporting evidences are required for ascertaining whether the misstatements are material

(Knechel & Salterio, 2016).

Question 7-31:

Account Name From Whom Confirmed Information to Be Confirmed

Cash at bank Cash transactions occurred in the

year to be confirmed by the

individual responsible for

entering all transactions

1. Bank information such as type and

nature of the bank

2. The amounts deposited in all

accounts

3. Account balance at the end of the

year

4. Names of account

5. Information related to cash

drawings and rates of interest

Trade accounts receivable Confirmation of trade

receivables to be made through

verification of a sample account

1. Debtors’ personal information

2. Account numbers

3. Particular date confirmation

4. Balance of invoices with dates

Inventories Confirmation of inventory

account to be made by the

warehouse custodian

1. Warehouse-related transaction

information

2. Detailed inventory list

3. Balance of inventory at specific

date

Trade accounts payable Verification of payable 1. Supplier information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.