Auditing and Assurance Service: KPMG Audit of Rolls-Royce Group Report

VerifiedAdded on 2020/05/28

|12

|3619

|80

Report

AI Summary

This report examines the financial scandal involving Rolls-Royce and the auditing firm KPMG. It delves into the corruption charges, including bribery and falsification of accounts, that led to the investigation by the Financial Reporting Council (FRC). The report analyzes the issues that potentially led to the scandal, such as the unethical use of third-party intermediaries and the lack of transparency in financial transactions, highlighting the audit capability failures. The report also discusses the initiatives taken by regulating bodies like ICAEW and ACCA to mitigate accounting scandals, including new reporting models and enhanced corporate reporting. The analysis concludes that the scandal was a result of lack of audit capability, and provides recommendations for improving the reputation of audit and mitigating future financial frauds.

Running head: AUDITING AND ASSURANCE SERVICE

Auditing and Assurance Service

Name of the Student:

Name of the University:

Author Note

Auditing and Assurance Service

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE SERVICE

Table of Contents

Introduction....................................................................................................................................3

KPMG Audit Plc’s audit of Rolls-Royce Group..............................................................................3

Issues that potentially led to the scandal.......................................................................................5

Initiatives taken by the regulating bodies.......................................................................................6

The particular solution in case of the Rolls-Royce accounting scandal.........................................7

Conclusion.....................................................................................................................................8

Appendix 1.....................................................................................................................................9

References and Bibliography.....................................................................................................9

Appendix 2...................................................................................................................................10

Table of Contents

Introduction....................................................................................................................................3

KPMG Audit Plc’s audit of Rolls-Royce Group..............................................................................3

Issues that potentially led to the scandal.......................................................................................5

Initiatives taken by the regulating bodies.......................................................................................6

The particular solution in case of the Rolls-Royce accounting scandal.........................................7

Conclusion.....................................................................................................................................8

Appendix 1.....................................................................................................................................9

References and Bibliography.....................................................................................................9

Appendix 2...................................................................................................................................10

2AUDITING AND ASSURANCE SERVICE

Executive Summary

The frequency of accounting scandals has increased over the years. In spite of the

several initiatives taken by the accounting bodies the instances of the financial frauds have

been overwhelming.

This particular study aims to focus on a particular example of the financial scandal

executed by the British giant automaker company, Rolls-Royce and the auditing firm that has

been evaluating the organizational financial and non-financial auctions. KPMG has been

responsible for the evaluation of the financial statements of the company for the past twenty

years. However, looking at the fraudulent operations carried out by the company, FRC has

launched an investigation in the audit work of the company.

This study aims at providing an overview into the relevant causes of major financial

scandals and the initiatives or the solutions that have been developed by the regulating bodies

for mitigating such fraudulent occurrences.

Executive Summary

The frequency of accounting scandals has increased over the years. In spite of the

several initiatives taken by the accounting bodies the instances of the financial frauds have

been overwhelming.

This particular study aims to focus on a particular example of the financial scandal

executed by the British giant automaker company, Rolls-Royce and the auditing firm that has

been evaluating the organizational financial and non-financial auctions. KPMG has been

responsible for the evaluation of the financial statements of the company for the past twenty

years. However, looking at the fraudulent operations carried out by the company, FRC has

launched an investigation in the audit work of the company.

This study aims at providing an overview into the relevant causes of major financial

scandals and the initiatives or the solutions that have been developed by the regulating bodies

for mitigating such fraudulent occurrences.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE SERVICE

Introduction

The globally known and publicized series of the financial scandals that had occurred in

the last few years have effectively eroded the public trust in regards to the audit process of the

corporate bodies. The gradually increasing mistrust has led to the public, doubting the role of

the auditors carrying out such evaluating procedures. This is because the primary duty of a

public auditor lies in acting, in the interest of the public, thus safeguarding the public welfare.

The series of auditing scandals that have taken place has led to the public, question the ethics

of the auditor. In fact the trust placed in the accuracy of services provided by the auditors has

also been hampered. The importance of the ethical considerations in the profession of auditing

has increased over the years mainly due to these frequent financial scandals. The International

Federation of Accountants (IFAC) has also developed a professional code of ethics for the

auditors. This has been done in order to regulate the ethical considerations involved in the

profession of auditing. In spite of such initiatives taken, the occurrence of the auditing scandals

has not decreased in number (Pearce 2016).

This study particularly aims to focus on this particular topic of accounting scandals and

the initiatives taken by the accounting professional bodies like ICAEW, ACCA, ICAS and CIMA

and the big four auditing firms like PWC, KPMG, Deloitte and EY for improving the reputation of

the audit. In order to achieve such an outcome the particular investigation by the Financial

Reporting Council (FRC) of the audit proceedings by KPMG of British giant, Rolls Royce has

been analyzed. The issues that led to the occurrence of such a particular auditing scandal and

the recommendations for mitigating such financial scandals have also been discussed in this

study.

KPMG Audit Plc’s audit of Rolls-Royce Group

The conglomerate Rolls-Royce had already been alleged in the year of 2010, for paying

a huge amount of fine (£671 million) to the Serious Fraud Office. The luxury car company did

admit to a number of corruption charges that involved falsifying accounts, interference with the

ongoing investigations and payments in tens of millions of pounds to win the ownership of the

contracts in Indonesia, Thailand, Russia and China (Arruda de Almeida and Zagaris 2015).

KPMG has been the sole firm responsible for carrying out the audits of Rolls-Royce. The

investigation by the Financial Reporting Council has been executed in relation to the financial

Introduction

The globally known and publicized series of the financial scandals that had occurred in

the last few years have effectively eroded the public trust in regards to the audit process of the

corporate bodies. The gradually increasing mistrust has led to the public, doubting the role of

the auditors carrying out such evaluating procedures. This is because the primary duty of a

public auditor lies in acting, in the interest of the public, thus safeguarding the public welfare.

The series of auditing scandals that have taken place has led to the public, question the ethics

of the auditor. In fact the trust placed in the accuracy of services provided by the auditors has

also been hampered. The importance of the ethical considerations in the profession of auditing

has increased over the years mainly due to these frequent financial scandals. The International

Federation of Accountants (IFAC) has also developed a professional code of ethics for the

auditors. This has been done in order to regulate the ethical considerations involved in the

profession of auditing. In spite of such initiatives taken, the occurrence of the auditing scandals

has not decreased in number (Pearce 2016).

This study particularly aims to focus on this particular topic of accounting scandals and

the initiatives taken by the accounting professional bodies like ICAEW, ACCA, ICAS and CIMA

and the big four auditing firms like PWC, KPMG, Deloitte and EY for improving the reputation of

the audit. In order to achieve such an outcome the particular investigation by the Financial

Reporting Council (FRC) of the audit proceedings by KPMG of British giant, Rolls Royce has

been analyzed. The issues that led to the occurrence of such a particular auditing scandal and

the recommendations for mitigating such financial scandals have also been discussed in this

study.

KPMG Audit Plc’s audit of Rolls-Royce Group

The conglomerate Rolls-Royce had already been alleged in the year of 2010, for paying

a huge amount of fine (£671 million) to the Serious Fraud Office. The luxury car company did

admit to a number of corruption charges that involved falsifying accounts, interference with the

ongoing investigations and payments in tens of millions of pounds to win the ownership of the

contracts in Indonesia, Thailand, Russia and China (Arruda de Almeida and Zagaris 2015).

KPMG has been the sole firm responsible for carrying out the audits of Rolls-Royce. The

investigation by the Financial Reporting Council has been executed in relation to the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE SERVICE

statements of the Rolls-Royce Group plc for the year ended 31 December 2010 and the Rolls-

Royce holdings plc for the financial years of 2011, 2012 and 2013. This investigation had been

carried out as a result of the Senior Fraud Office announcement on 17th January, 2017 that a

Deferred Prosecution Agreement between the Serious Fraud Office (SFO) and the Rolls-Royce

plc has been agreed (Mayer 2017).

A DPA is a statutory means with the help of which a corporate entity will have gained the

authority to appear to a court for conduct without suffering the complete consequences of a

criminal conviction that might result in restriction of the firm for competing for public contracts.

The particular event that led to the requirement of a DPA was the scandal that had taken place

in the year of 2010. The corruption charges that the leading automaker company was accused

of ranged back for more than over twenty years. Rolls-Royce has been bribing hugely for

gaining the ownerships illegally. The British giant has been adopting such unethical and illegal

practices since 1989 till 2013 (Tombs and Whyte 2015). An instance of the cases against which

the investigations are carried out is that the $100 million order for the supply of Trent 700 jet

engines to Indonesia’s Garuda airline in the year of 1991. The Indonesian deal had been a well

known deal for Rolls-Royce. The general estimation that the engines that were to be selected

belonged to the US rival Pratt & Whitney. However, the deal was overruled in favor of the Rolls-

Royce Group. Even proper evidence had been recorded in support of the unethical action

committed by the company. Senior officials at the Rolls Royce did agree to the payment of

$2.25 million along with a Rolls-Royce Silver Spirit car that was rewarded to an agent for the

sale of Trent 700 engines to Garuda (KISS, FÜLÖP and CORDOŞ 2015).

It had been further recorded that the employees of the Rolls-Royce were charged with

the payment of $2.2 million to the executives of Air Asia for winning the ownership of sales

orders. The company had admitted to a total of seven counts of conspiracy in terms of

corruption and five cases in regards to failure to prevent bribery. Furthermore, the company had

also engaged itself in the payment of bribes of a total amount of $36.3 million to the agents of

Thai Airways for securing orders (Nomoto 2016).

There have been similar instances of such illegal operations in Germany, India and

China. As a consequence, the company had received two profit warnings and had applied for a

DPA so that the company would not be criminally convicted.

statements of the Rolls-Royce Group plc for the year ended 31 December 2010 and the Rolls-

Royce holdings plc for the financial years of 2011, 2012 and 2013. This investigation had been

carried out as a result of the Senior Fraud Office announcement on 17th January, 2017 that a

Deferred Prosecution Agreement between the Serious Fraud Office (SFO) and the Rolls-Royce

plc has been agreed (Mayer 2017).

A DPA is a statutory means with the help of which a corporate entity will have gained the

authority to appear to a court for conduct without suffering the complete consequences of a

criminal conviction that might result in restriction of the firm for competing for public contracts.

The particular event that led to the requirement of a DPA was the scandal that had taken place

in the year of 2010. The corruption charges that the leading automaker company was accused

of ranged back for more than over twenty years. Rolls-Royce has been bribing hugely for

gaining the ownerships illegally. The British giant has been adopting such unethical and illegal

practices since 1989 till 2013 (Tombs and Whyte 2015). An instance of the cases against which

the investigations are carried out is that the $100 million order for the supply of Trent 700 jet

engines to Indonesia’s Garuda airline in the year of 1991. The Indonesian deal had been a well

known deal for Rolls-Royce. The general estimation that the engines that were to be selected

belonged to the US rival Pratt & Whitney. However, the deal was overruled in favor of the Rolls-

Royce Group. Even proper evidence had been recorded in support of the unethical action

committed by the company. Senior officials at the Rolls Royce did agree to the payment of

$2.25 million along with a Rolls-Royce Silver Spirit car that was rewarded to an agent for the

sale of Trent 700 engines to Garuda (KISS, FÜLÖP and CORDOŞ 2015).

It had been further recorded that the employees of the Rolls-Royce were charged with

the payment of $2.2 million to the executives of Air Asia for winning the ownership of sales

orders. The company had admitted to a total of seven counts of conspiracy in terms of

corruption and five cases in regards to failure to prevent bribery. Furthermore, the company had

also engaged itself in the payment of bribes of a total amount of $36.3 million to the agents of

Thai Airways for securing orders (Nomoto 2016).

There have been similar instances of such illegal operations in Germany, India and

China. As a consequence, the company had received two profit warnings and had applied for a

DPA so that the company would not be criminally convicted.

5AUDITING AND ASSURANCE SERVICE

As it can be concluded from the above instances the major offences, against which the

company had been charged guilty, are payment of bribes, receiving bribes, the bribery of foreign

public officials and the failure of a commercial organization to prevent bribery.

Issues that potentially led to the scandal

The issues that led to the unlawful conduct of the leading automaker company involved

the inappropriate or unethical use of the third-party intermediaries (TPIs). TPIs include people

from the category of agents like distributors, brokers, government intermediaries and resellers.

Therefore, the unethical proceedings by Roll-Royce had occurred due to the close associations

with the suppliers, customers or the public officials and making improper offers to them for

securing orders or obtaining favoritism (Bingham and Druker 2017).

Now, the particular causes for the occurrence of a financial scandal may be numerous.

For instance, the lack of transparency in the financial transactions or the existence of a poor

structure of internal control within the organization may be the potential reasons for the

occurrence of a financial fraud. Moreover, the lack of independent audit department in the

organization might also lead to fraudulent occurring. In case of Rolls-Royce the company had

also revealed that its civil aerospace unit would have made an operating loss instead of an 800

million pound profit, if the company had used a different accounting method. The operating profit

of the group would be two-fifth of what had already been reported in the annual report. This

clearly indicates that the accounting practices followed by the automaker are complicated and

difficult to comprehend which has effectively helped in the process of executing the fraudulent

activities (Bowman 2014).

Furthermore, the issue that is coming up from the above discussions is that the auditing

evaluations of the accounting as well as the internal operating procedures of the organization

have not been conducted properly. The primary duty of an auditor lies in making sure that the

business operations that are carried out by a particular firm are genuine and reflects a true and

fair view of the financial condition of the company. However, in case of the British giant, Rolls-

Royce that primary perspective of audit has been effectively hampered. Thus, to be very

particular the issue that led to the financial scandal in Rolls-Royce was an instance of audit

capability. This means that the audit carried out by the particular auditing firm is not appropriate

as it is not looking into the proper areas or is not conducting the auditing evaluations in

accordance to the analysis framework established by the regulating bodies (Carr and Jago

2014).

As it can be concluded from the above instances the major offences, against which the

company had been charged guilty, are payment of bribes, receiving bribes, the bribery of foreign

public officials and the failure of a commercial organization to prevent bribery.

Issues that potentially led to the scandal

The issues that led to the unlawful conduct of the leading automaker company involved

the inappropriate or unethical use of the third-party intermediaries (TPIs). TPIs include people

from the category of agents like distributors, brokers, government intermediaries and resellers.

Therefore, the unethical proceedings by Roll-Royce had occurred due to the close associations

with the suppliers, customers or the public officials and making improper offers to them for

securing orders or obtaining favoritism (Bingham and Druker 2017).

Now, the particular causes for the occurrence of a financial scandal may be numerous.

For instance, the lack of transparency in the financial transactions or the existence of a poor

structure of internal control within the organization may be the potential reasons for the

occurrence of a financial fraud. Moreover, the lack of independent audit department in the

organization might also lead to fraudulent occurring. In case of Rolls-Royce the company had

also revealed that its civil aerospace unit would have made an operating loss instead of an 800

million pound profit, if the company had used a different accounting method. The operating profit

of the group would be two-fifth of what had already been reported in the annual report. This

clearly indicates that the accounting practices followed by the automaker are complicated and

difficult to comprehend which has effectively helped in the process of executing the fraudulent

activities (Bowman 2014).

Furthermore, the issue that is coming up from the above discussions is that the auditing

evaluations of the accounting as well as the internal operating procedures of the organization

have not been conducted properly. The primary duty of an auditor lies in making sure that the

business operations that are carried out by a particular firm are genuine and reflects a true and

fair view of the financial condition of the company. However, in case of the British giant, Rolls-

Royce that primary perspective of audit has been effectively hampered. Thus, to be very

particular the issue that led to the financial scandal in Rolls-Royce was an instance of audit

capability. This means that the audit carried out by the particular auditing firm is not appropriate

as it is not looking into the proper areas or is not conducting the auditing evaluations in

accordance to the analysis framework established by the regulating bodies (Carr and Jago

2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE SERVICE

In case of Rolls-Royce the audit had been conducted by one of the big four firms that is

KPMG. However, the exposure of the financial scandal carried out by the company has

questioned the audit carried out by KPMG over the years. The Financial Reporting Council has

thus launched an investigation into the audit of Rolls-Royce by KPMG. Though KPMG had

taken enough initiative and it would be unfair to blame an audit firm for the misconduct of their

client, KPMG has failed to ensure its primary duty that is to ensure the welfare of the public who

are in this case the employees of the organization, the stakeholders and the luxury car makers

whose reputation had been at stake due to the unethical deeds carried out by Rolls-Royce. In

the annual report of Rolls-Royce for the financial year of 2014, KPMG had indicated that the

company had made use of estimations and assumptions that resulted in mildly cautious profit

recognition (Soh, Leung and Leong 2015). However, the audit firm should have been much

stricter and should have delved into the issue further, highlighting the fraudulent operations

carried out by the corporate body. The audit firm in a 2013 report had also mentioned that the

company was at risk of bribery, but again did not delve further into the issue. In support of the

perspective that the accounting scandal was a result of lack of audit capability, the FRC while

conducting the investigation had reported that the audit proceedings were deficient in nature

(William, Glover and Prawitt 2016).

Therefore, the fact that can be summarized from the above discussion is that accounting

scandal that had been carried out by the leading automaker company was a result of lack of

audit capability.

Initiatives taken by the regulating bodies

One of the international regulating bodies like the ICAEW has established an entire new

reporting model for the purpose of mitigating the occurrence of accounting scandals. The new

reporting model effectively promotes the communication of the business proceedings to the

investors and other stakeholders of business at regular intervals. The new reporting model also

establishes a transparency in reporting the business proceedings. ICAEW believes in the fact

that the ongoing financial scandals have led to a huge gap between what is being audited and

what the public believe should be audited (Cannon and Bedard 2016). The regulating body

acknowledges the requirement of an enhanced corporate reporting and a greater degree of

assurance. Thus, the potential solution lies in the fact that the corporate reporting has to

improve qualitatively. The new reporting model not only promotes transparency but also

mandates the preparation of a sustainability report that effectively should disclose all the

In case of Rolls-Royce the audit had been conducted by one of the big four firms that is

KPMG. However, the exposure of the financial scandal carried out by the company has

questioned the audit carried out by KPMG over the years. The Financial Reporting Council has

thus launched an investigation into the audit of Rolls-Royce by KPMG. Though KPMG had

taken enough initiative and it would be unfair to blame an audit firm for the misconduct of their

client, KPMG has failed to ensure its primary duty that is to ensure the welfare of the public who

are in this case the employees of the organization, the stakeholders and the luxury car makers

whose reputation had been at stake due to the unethical deeds carried out by Rolls-Royce. In

the annual report of Rolls-Royce for the financial year of 2014, KPMG had indicated that the

company had made use of estimations and assumptions that resulted in mildly cautious profit

recognition (Soh, Leung and Leong 2015). However, the audit firm should have been much

stricter and should have delved into the issue further, highlighting the fraudulent operations

carried out by the corporate body. The audit firm in a 2013 report had also mentioned that the

company was at risk of bribery, but again did not delve further into the issue. In support of the

perspective that the accounting scandal was a result of lack of audit capability, the FRC while

conducting the investigation had reported that the audit proceedings were deficient in nature

(William, Glover and Prawitt 2016).

Therefore, the fact that can be summarized from the above discussion is that accounting

scandal that had been carried out by the leading automaker company was a result of lack of

audit capability.

Initiatives taken by the regulating bodies

One of the international regulating bodies like the ICAEW has established an entire new

reporting model for the purpose of mitigating the occurrence of accounting scandals. The new

reporting model effectively promotes the communication of the business proceedings to the

investors and other stakeholders of business at regular intervals. The new reporting model also

establishes a transparency in reporting the business proceedings. ICAEW believes in the fact

that the ongoing financial scandals have led to a huge gap between what is being audited and

what the public believe should be audited (Cannon and Bedard 2016). The regulating body

acknowledges the requirement of an enhanced corporate reporting and a greater degree of

assurance. Thus, the potential solution lies in the fact that the corporate reporting has to

improve qualitatively. The new reporting model not only promotes transparency but also

mandates the preparation of a sustainability report that effectively should disclose all the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE SERVICE

information that concerns the stakeholders. Even the materiality issues should also be disclosed

in order to ensure the report reflects the true and fair view of the company (Soh, Leung and

Leong 2015).

ACCA on the other hand, has identified the reasons of lack of audit capability like the

lack of human resources as a result of high talent attrition rate, lack of focus on the audit quality

and inability to understand the business carried out by the client. ACCA recommends the

development of solutions by the proper collection of audit evidence and adopting an honest

approach while preparing the audit report for the client (Masztalerz 2014).

The ICAS or FRC that had played the major role in launching an investigation behind the

auditing proceedings carried out by KPMG in case of Rolls-Royce has developed strict

guidelines in achieving the objective of less frequent accounting scandals. After the occurrence

of the Rolls-Royce accounting scandal, the FRC did make a mandatory rule that an organization

is required to change the auditing firm carrying out its annual audit in every ten years. This is

another potential solution that may be applicable in the case of Rolls-Royce. The auditing firm,

KPMG had been associated with Rolls-Royce for a period of 25 years. This might have led to

the development of personal relationship between the firm and the company, on account of

which they adopted a lenient approach towards auditing the British giant (Dewing and Russell

2015).

The global body CIMA aims to develop a risk prevention framework that consists of four

major components prevention, detection, deterrence and response. The regulating body also

states that maintenance of high ethical standards in regards to business operations also reap

long term benefits not only to the stakeholders but also to the company as well (Knechel and

Salterio 2016).

The particular solution in case of the Rolls-Royce accounting scandal

The particular solution in regards to the Rolls-Royce financial scandal is that the auditing

process should be conducted following a particular framework. It is the primary duty of the

organization to maintain the highest standards of integrity while dealing in business operations.

However, when the case is not such, the auditor must step in and point out the particular areas

of doubt. In case of Rolls-Royce, the fraud was not just limited to a handful of rogue employees

but the senior management was also involved in paying and receiving bribes. This should have

been noted by KPMG and allegedly reported. The reasons KPMG failed to do so was lack of

information that concerns the stakeholders. Even the materiality issues should also be disclosed

in order to ensure the report reflects the true and fair view of the company (Soh, Leung and

Leong 2015).

ACCA on the other hand, has identified the reasons of lack of audit capability like the

lack of human resources as a result of high talent attrition rate, lack of focus on the audit quality

and inability to understand the business carried out by the client. ACCA recommends the

development of solutions by the proper collection of audit evidence and adopting an honest

approach while preparing the audit report for the client (Masztalerz 2014).

The ICAS or FRC that had played the major role in launching an investigation behind the

auditing proceedings carried out by KPMG in case of Rolls-Royce has developed strict

guidelines in achieving the objective of less frequent accounting scandals. After the occurrence

of the Rolls-Royce accounting scandal, the FRC did make a mandatory rule that an organization

is required to change the auditing firm carrying out its annual audit in every ten years. This is

another potential solution that may be applicable in the case of Rolls-Royce. The auditing firm,

KPMG had been associated with Rolls-Royce for a period of 25 years. This might have led to

the development of personal relationship between the firm and the company, on account of

which they adopted a lenient approach towards auditing the British giant (Dewing and Russell

2015).

The global body CIMA aims to develop a risk prevention framework that consists of four

major components prevention, detection, deterrence and response. The regulating body also

states that maintenance of high ethical standards in regards to business operations also reap

long term benefits not only to the stakeholders but also to the company as well (Knechel and

Salterio 2016).

The particular solution in case of the Rolls-Royce accounting scandal

The particular solution in regards to the Rolls-Royce financial scandal is that the auditing

process should be conducted following a particular framework. It is the primary duty of the

organization to maintain the highest standards of integrity while dealing in business operations.

However, when the case is not such, the auditor must step in and point out the particular areas

of doubt. In case of Rolls-Royce, the fraud was not just limited to a handful of rogue employees

but the senior management was also involved in paying and receiving bribes. This should have

been noted by KPMG and allegedly reported. The reasons KPMG failed to do so was lack of

8AUDITING AND ASSURANCE SERVICE

auditing capabilities. The firm being attached to its client for more than 20 years made the audit

team to blindly believe in the integrity standards of the conglomerate. Thus, this evidently

indicates that audit rotation in regards to the firm is also necessary. However, the fact that the

foremost should be adhered to is the strict following of the audit principles as laid down by the

regulating bodies. The corporate bodies should also adhere to the corporate reporting standards

established by the regulatory boards.

Conclusion

Thus, as can be concluded from the above discussions, in spite of the trust issues

between the public and the audit firms, the compliance to the solutions or amendments

established by the regulating bodies will certainly improve the future of the profession. The

corporate bodies have to understand that adopting fraudulent techniques will definitely harm the

business in the long run. Therefore, the maintenance of ethical standards will make the work of

the auditors easy and in turn ascertain and promote transparent business operations.

auditing capabilities. The firm being attached to its client for more than 20 years made the audit

team to blindly believe in the integrity standards of the conglomerate. Thus, this evidently

indicates that audit rotation in regards to the firm is also necessary. However, the fact that the

foremost should be adhered to is the strict following of the audit principles as laid down by the

regulating bodies. The corporate bodies should also adhere to the corporate reporting standards

established by the regulatory boards.

Conclusion

Thus, as can be concluded from the above discussions, in spite of the trust issues

between the public and the audit firms, the compliance to the solutions or amendments

established by the regulating bodies will certainly improve the future of the profession. The

corporate bodies have to understand that adopting fraudulent techniques will definitely harm the

business in the long run. Therefore, the maintenance of ethical standards will make the work of

the auditors easy and in turn ascertain and promote transparent business operations.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE SERVICE

Appendix 1

References and Bibliography

Alles, M.G., 2015. Drivers of the Use and Facilitators and Obstacles of the Evolution of Big Data

by the Audit Profession. Accounting Horizons, 29(2), pp.439-449.

Arruda de Almeida, M. and Zagaris, B., 2015. Political Capture in the Petrobus Corruption

Scandal: The Sad Tale of an Oil Giant. Fletcher F. World Aff., 39, p.87.

Backof, A., Bowlin, K. and Goodson, B., 2017. The impact of proposed changes to the content

of the audit report on jurors’ assessments of auditor negligence.

Bingham, C. and Druker, J., 2017. Acting With Integrity Across The World’? What Do

Multinationals Say About Labour Standards?.

Bowman, C., 2014. When are Executives Paid Too Much?.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. and

Vasarhelyi, M., 2015. Evolution of auditing: from the traditional approach to the future audit.

Audit Analytics, 71.

Cannon, N.H. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review, 92(4), pp.81-114.

Carr, I.M. and Jago, R., 2014. Corruption, Money Laundering, Secrecy and Societal

Responsibility of Banks.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Dewing, I.P. and Russell, P.O., 2015. Audit, Supervision and Risk in Financial Services. ICAS.

KISS, C., FÜLÖP, M.T. and CORDOŞ, G.S., 2015. Relevant Aspects Regarding the Changes of

the Statutory Audit Report in the Light of International Regulations. Audit Financiar, 13(126).

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Appendix 1

References and Bibliography

Alles, M.G., 2015. Drivers of the Use and Facilitators and Obstacles of the Evolution of Big Data

by the Audit Profession. Accounting Horizons, 29(2), pp.439-449.

Arruda de Almeida, M. and Zagaris, B., 2015. Political Capture in the Petrobus Corruption

Scandal: The Sad Tale of an Oil Giant. Fletcher F. World Aff., 39, p.87.

Backof, A., Bowlin, K. and Goodson, B., 2017. The impact of proposed changes to the content

of the audit report on jurors’ assessments of auditor negligence.

Bingham, C. and Druker, J., 2017. Acting With Integrity Across The World’? What Do

Multinationals Say About Labour Standards?.

Bowman, C., 2014. When are Executives Paid Too Much?.

Byrnes, P.E., Al-Awadhi, C.A., Gullvist, B., Brown-Liburd, H., Teeter, C.R., Warren Jr, J.D. and

Vasarhelyi, M., 2015. Evolution of auditing: from the traditional approach to the future audit.

Audit Analytics, 71.

Cannon, N.H. and Bedard, J.C., 2016. Auditing challenging fair value measurements: Evidence

from the field. The Accounting Review, 92(4), pp.81-114.

Carr, I.M. and Jago, R., 2014. Corruption, Money Laundering, Secrecy and Societal

Responsibility of Banks.

Christensen, B.E., Glover, S.M., Omer, T.C. and Shelley, M.K., 2016. Understanding audit

quality: Insights from audit professionals and investors. Contemporary Accounting Research,

33(4), pp.1648-1684.

Dewing, I.P. and Russell, P.O., 2015. Audit, Supervision and Risk in Financial Services. ICAS.

KISS, C., FÜLÖP, M.T. and CORDOŞ, G.S., 2015. Relevant Aspects Regarding the Changes of

the Statutory Audit Report in the Light of International Regulations. Audit Financiar, 13(126).

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Taylor & Francis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ASSURANCE SERVICE

Kogan, A., Alles, M.G., Vasarhelyi, M.A. and Wu, J., 2014. Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice & Theory, 33(4), pp.221-

245.

Masztalerz, M., 2014. Global Management Accounting Principles-Emperor's New Clothes.

Research Papers of Wrocław University of Economics, (345).

Mayer, C., 2017. Whose Responsible for Irresponsible Business? An Assessment.

Nomoto, S., 2016, September. Product planning and innovative developments from the

perspective of anticipated market trends in the coming years: An analytical approach based on

machine tools developed for auto manufacturers. In Management of Engineering and

Technology (PICMET), 2016 Portland International Conference on (pp. 2549-2562). IEEE.

Pearce, B., 2016. Gatsby’s Rolls-Royce: reflections on the automobile and literature. English

Academy Review, 33(2), pp.52-67.

Soh, D.S., Leung, P. and Leong, S., 2015. The development of integrated reporting and the role

of the accounting and auditing profession. In Social Audit Regulation (pp. 33-57). Springer

International Publishing.

Tombs, S. and Whyte, D., 2015. Introduction to the Special Issue on ‘Crimes of the Powerful’.

The Howard Journal of Crime and Justice, 54(1), pp.1-7.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Appendix 2

ISSUES

AUDIT

FACTORS

POTENTIAL

SOLUTION

Deloitte LLP - Mitie Group plc audit Discrepancy in

the books of

accounts by

the amout of

$40 to $50

million had

been found

Lack of Audit

capability

Improvement

s in regards to

risk

management

and internal

audiit

required

BT Group plc and the audit by

PricewaterhouseCoopers LLP Financial

irregularities

in the Italian

Lack of Audit

capability

FRC had

mandated the

period of

Kogan, A., Alles, M.G., Vasarhelyi, M.A. and Wu, J., 2014. Design and evaluation of a

continuous data level auditing system. Auditing: A Journal of Practice & Theory, 33(4), pp.221-

245.

Masztalerz, M., 2014. Global Management Accounting Principles-Emperor's New Clothes.

Research Papers of Wrocław University of Economics, (345).

Mayer, C., 2017. Whose Responsible for Irresponsible Business? An Assessment.

Nomoto, S., 2016, September. Product planning and innovative developments from the

perspective of anticipated market trends in the coming years: An analytical approach based on

machine tools developed for auto manufacturers. In Management of Engineering and

Technology (PICMET), 2016 Portland International Conference on (pp. 2549-2562). IEEE.

Pearce, B., 2016. Gatsby’s Rolls-Royce: reflections on the automobile and literature. English

Academy Review, 33(2), pp.52-67.

Soh, D.S., Leung, P. and Leong, S., 2015. The development of integrated reporting and the role

of the accounting and auditing profession. In Social Audit Regulation (pp. 33-57). Springer

International Publishing.

Tombs, S. and Whyte, D., 2015. Introduction to the Special Issue on ‘Crimes of the Powerful’.

The Howard Journal of Crime and Justice, 54(1), pp.1-7.

William Jr, M., Glover, S. and Prawitt, D., 2016. Auditing and assurance services: A systematic

approach. McGraw-Hill Education.

Appendix 2

ISSUES

AUDIT

FACTORS

POTENTIAL

SOLUTION

Deloitte LLP - Mitie Group plc audit Discrepancy in

the books of

accounts by

the amout of

$40 to $50

million had

been found

Lack of Audit

capability

Improvement

s in regards to

risk

management

and internal

audiit

required

BT Group plc and the audit by

PricewaterhouseCoopers LLP Financial

irregularities

in the Italian

Lack of Audit

capability

FRC had

mandated the

period of

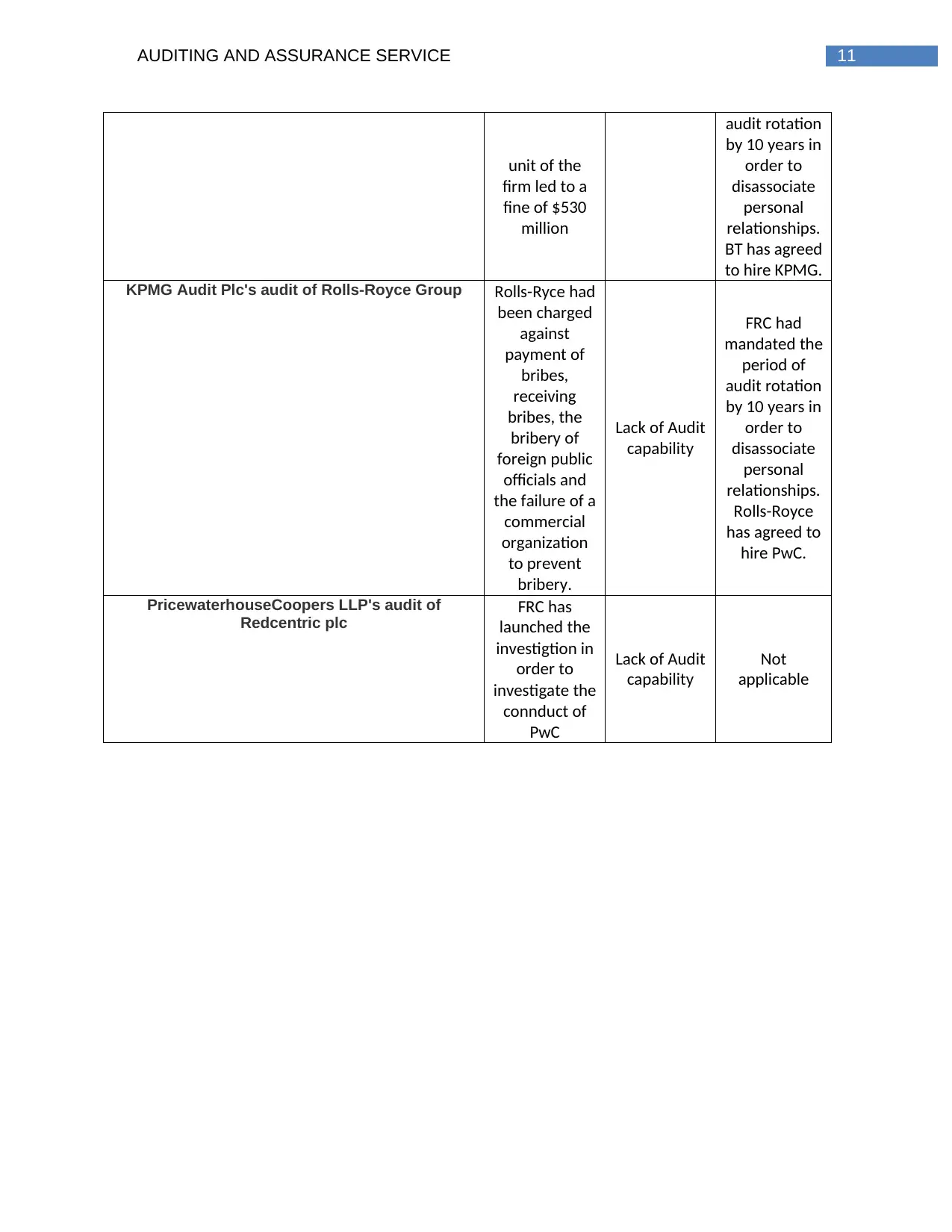

11AUDITING AND ASSURANCE SERVICE

unit of the

firm led to a

fine of $530

million

audit rotation

by 10 years in

order to

disassociate

personal

relationships.

BT has agreed

to hire KPMG.

KPMG Audit Plc's audit of Rolls-Royce Group Rolls-Ryce had

been charged

against

payment of

bribes,

receiving

bribes, the

bribery of

foreign public

officials and

the failure of a

commercial

organization

to prevent

bribery.

Lack of Audit

capability

FRC had

mandated the

period of

audit rotation

by 10 years in

order to

disassociate

personal

relationships.

Rolls-Royce

has agreed to

hire PwC.

PricewaterhouseCoopers LLP's audit of

Redcentric plc

FRC has

launched the

investigtion in

order to

investigate the

connduct of

PwC

Lack of Audit

capability

Not

applicable

unit of the

firm led to a

fine of $530

million

audit rotation

by 10 years in

order to

disassociate

personal

relationships.

BT has agreed

to hire KPMG.

KPMG Audit Plc's audit of Rolls-Royce Group Rolls-Ryce had

been charged

against

payment of

bribes,

receiving

bribes, the

bribery of

foreign public

officials and

the failure of a

commercial

organization

to prevent

bribery.

Lack of Audit

capability

FRC had

mandated the

period of

audit rotation

by 10 years in

order to

disassociate

personal

relationships.

Rolls-Royce

has agreed to

hire PwC.

PricewaterhouseCoopers LLP's audit of

Redcentric plc

FRC has

launched the

investigtion in

order to

investigate the

connduct of

PwC

Lack of Audit

capability

Not

applicable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.