Auditing and Assurance in Australia: ASA 315 and ASA 520 Analysis

VerifiedAdded on 2022/11/17

|5

|1647

|356

Report

AI Summary

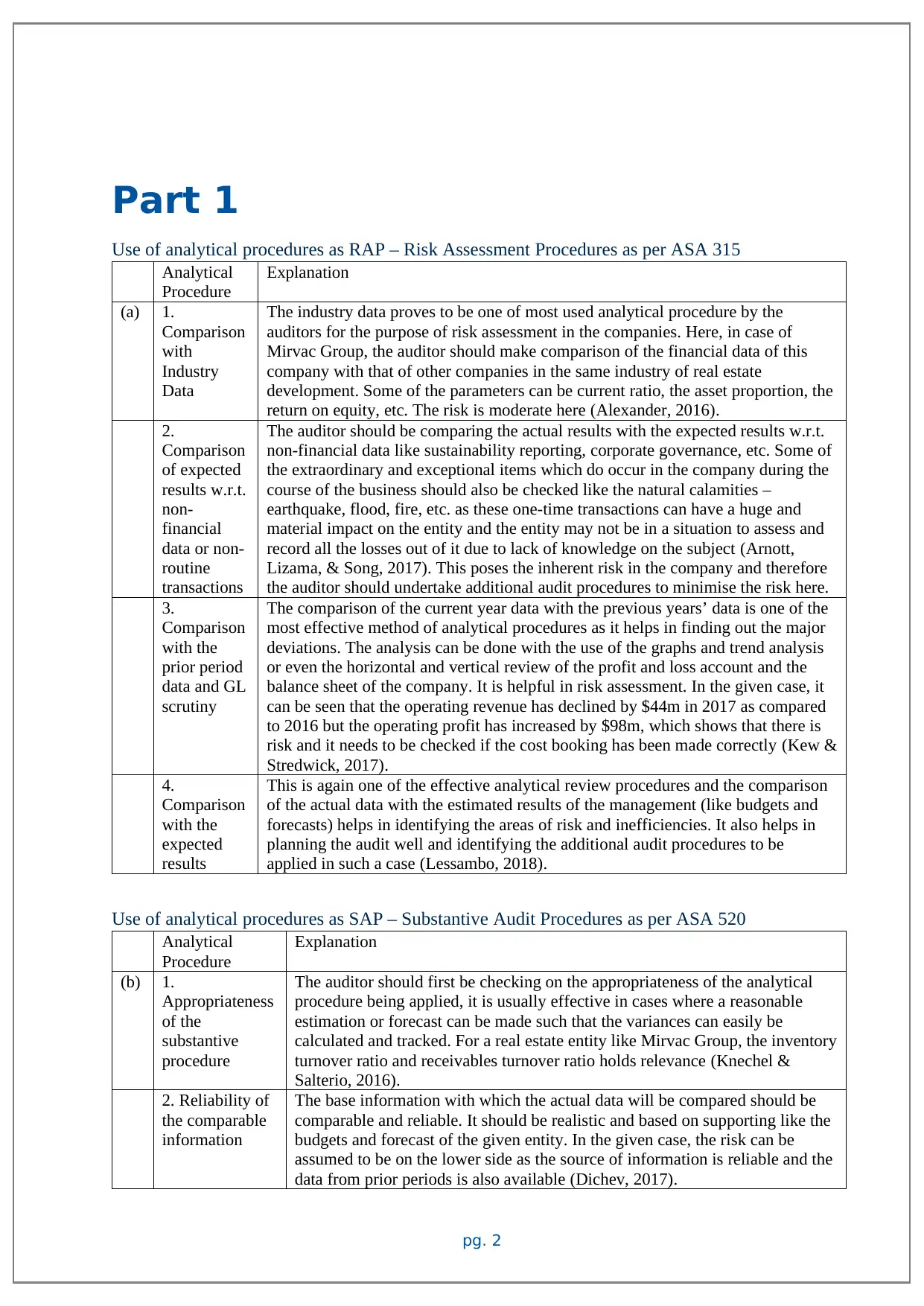

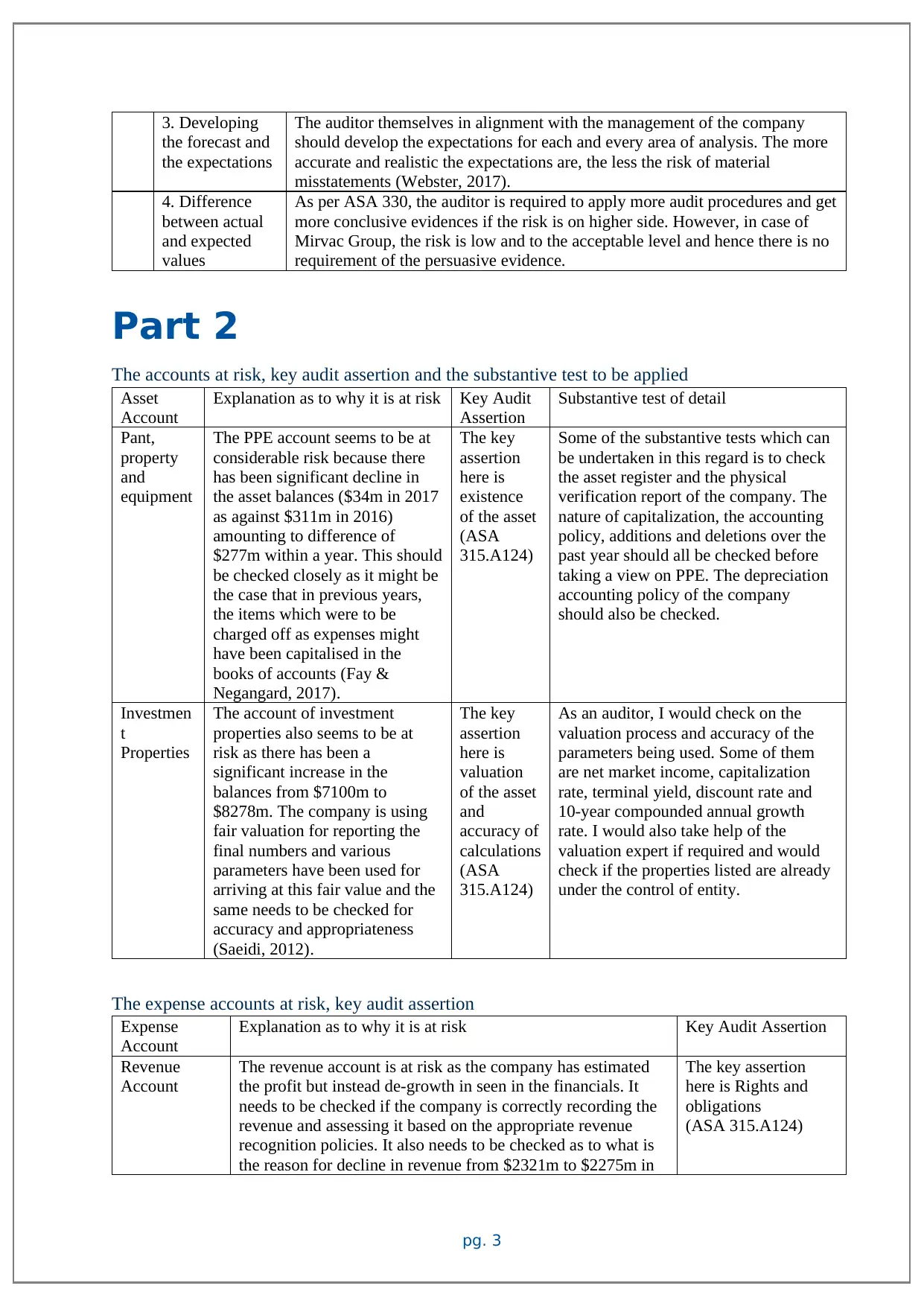

This report analyzes auditing and assurance practices in Australia, focusing on the application of ASA 315 (Risk Assessment Procedures) and ASA 520 (Substantive Audit Procedures). Part 1 distinguishes between analytical procedures used for risk assessment and those used as substantive audit procedures, providing explanations and examples from a case study of Mirvac Group. Part 2 assesses audit risk, identifies key audit assertions, and outlines substantive tests for specific accounts, including Plant, Property, and Equipment (PPE), Investment Properties, and Revenue. The report highlights potential risks associated with each account, such as valuation and accuracy, and recommends specific audit procedures to mitigate these risks, referencing relevant auditing standards and literature.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.