Auditing and Assurance in Australia: Inventory and Intangible Assets

VerifiedAdded on 2022/11/11

|10

|3505

|63

Report

AI Summary

This report presents a comprehensive analysis of two case studies, Computing Solutions and Beautiful Hair, within the context of auditing and assurance in Australia. The primary objective is to identify and assess audit assertions at risk, specifically focusing on valuation and allocation, and existence related to inventory and intangible assets. The report delves into the development of appropriate substantive audit procedures to mitigate these risks, considering the specific circumstances of each case. Furthermore, the report discusses the application of ASA 701, Communicating Key Audit Matters, to determine and disclose significant issues that could impact the financial statements. The findings highlight the importance of tailored audit procedures for inventory and intangible assets, reflecting the unique characteristics of each company. The report also emphasizes the auditor's responsibility in communicating key audit matters effectively, ensuring transparency and providing valuable information to stakeholders.

Running head: AUDITING AND ASSURANCE IN AUSTRALIA

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author Note

Auditing and Assurance in Australia

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE IN AUSTRALIA

Executive Summary

The main purpose of this report is the analysis of the cases of Computing Solutions and

Beautiful Hair with the aim to identify the assertions at risk so that appropriate substantive

audit procedures can be developed for them. This report also focuses on the discussion of

ASA 701 Communicating Key Audit Matters for the determination of the key audit matters.

Findings of the report show that both inventory and intangible assets have different assertions

that lead to the development of different substbtive audit procedures.

Executive Summary

The main purpose of this report is the analysis of the cases of Computing Solutions and

Beautiful Hair with the aim to identify the assertions at risk so that appropriate substantive

audit procedures can be developed for them. This report also focuses on the discussion of

ASA 701 Communicating Key Audit Matters for the determination of the key audit matters.

Findings of the report show that both inventory and intangible assets have different assertions

that lead to the development of different substbtive audit procedures.

2AUDITING AND ASSURANCE IN AUSTRALIA

Table of Contents

Introduction................................................................................................................................3

Computing Solutions..................................................................................................................3

Requirement a: Audit Assertions...........................................................................................3

Requirement b: Substantive Audit Procedures......................................................................3

Requirement c: ASA 701.......................................................................................................4

Beautiful Hair.............................................................................................................................5

Requirement a: Audit Assertions...........................................................................................5

Requirement b: Substantive Audit Procedures......................................................................5

Requirement c: ASA 701.......................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Table of Contents

Introduction................................................................................................................................3

Computing Solutions..................................................................................................................3

Requirement a: Audit Assertions...........................................................................................3

Requirement b: Substantive Audit Procedures......................................................................3

Requirement c: ASA 701.......................................................................................................4

Beautiful Hair.............................................................................................................................5

Requirement a: Audit Assertions...........................................................................................5

Requirement b: Substantive Audit Procedures......................................................................5

Requirement c: ASA 701.......................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE IN AUSTRALIA

Introduction

Auditing is the process to examine a company’s financial statements and records in

order to determine that whether they are accurate and as per the applicable accounting rules

and regulations. External auditors come from outside organizations for examining accounting

as well as financial records with the aim to provide independent opinion on these financial

statements. In this whole process, the auditors have to fulfill certain responsibilities to

consider all the necessary aspects in the whole auditing process (Johnstone, Gramling and

Rittenberg, 2013). Inspection and examination of the audit assertions is one of those

responsibilities of the auditors. Audit assertions are the explicit or implicit claims as well as

representations that the managements of the audit clients make related to the correctness of

different elements in order to prepare the financial statements. The auditors are required to

assess whether any of the audit assertions are at risk. In case the auditors conclude the one or

more than one audit assertions are at risk, they must undertake the required substantive audit

procedures to handle the audit assertions. Substantive audit procedures are the processes,

steps, or tests that create conclusive evidence regarding the presence of audit assertions in the

financial statements of the audit clients (Houqe, Ahmed and van Zijl, 2017). There are three

parts of the report. First part examines which audit assertions are at risk in the provided

companies; second part suggests the appropriate substantive audit procedures to minimize

those risks; and the last part sheds light on the responsibilities of the auditors regarding the

key audit matters.

Computing Solutions

Requirement a: Audit Assertions

Valuation and Allocation – This is a crucial assertion associated with inventory which helps

in confirming the value is appropriate in which the company has valued, recorded and

disclosed. It is visible in Computing Solutions that there is 26% of sales in 2019 and 19% of

sales in 2018 included in the inventory in hand. Moreover, inventory turnover ratio has

decreased to 3.8 from 5.2. All these aspects are the indicators of potential slow moving of

inventory or inventories are outdated. It is also observable that the commencement date of the

government contract is middle of July 2019. For this reason, it will be required to write down

any stock in hand in hand at the end of the year to net realizable value due to the requirement

of the contract (Hazlett and Honig, 2016).

Existence – This particular assertion is used to analyze the aspect that there is existence of

inventory at the end of the financial year that are recorded in different financial reports.

According to the provided case, Computing Solutions has recently moved all of their

inventories from the central warehouse to six regional warehouses. This incident indicates

towards the major potential that there has been lost of certain portion of the inventories in the

lost in transit while transferring to the new regional warehouses. In addition, it is also

possible that there have been certain errors in the physical inventory counting process in the

new warehouses. All these aspects put this assertion at risk (Tung and Deng, 2013).

Requirement b: Substantive Audit Procedures

Valuation and Allocation – For this risk, the first substantive audit procedure for the auditor

is to test the releasable value and lower of cost of the main inventory by comparing the cost

of the inventory with the latest price. After that, it is needed for the auditor checking the

inventories kept for selling to the government after the balance date whether their valuation

has been done in net realizable value or lower of cost. Moreover, it is also required for the

auditor to review the major product line of Computing Solution so that they can determine

whether the inventories have been moving slowly or they have become obsolete. In addition,

Introduction

Auditing is the process to examine a company’s financial statements and records in

order to determine that whether they are accurate and as per the applicable accounting rules

and regulations. External auditors come from outside organizations for examining accounting

as well as financial records with the aim to provide independent opinion on these financial

statements. In this whole process, the auditors have to fulfill certain responsibilities to

consider all the necessary aspects in the whole auditing process (Johnstone, Gramling and

Rittenberg, 2013). Inspection and examination of the audit assertions is one of those

responsibilities of the auditors. Audit assertions are the explicit or implicit claims as well as

representations that the managements of the audit clients make related to the correctness of

different elements in order to prepare the financial statements. The auditors are required to

assess whether any of the audit assertions are at risk. In case the auditors conclude the one or

more than one audit assertions are at risk, they must undertake the required substantive audit

procedures to handle the audit assertions. Substantive audit procedures are the processes,

steps, or tests that create conclusive evidence regarding the presence of audit assertions in the

financial statements of the audit clients (Houqe, Ahmed and van Zijl, 2017). There are three

parts of the report. First part examines which audit assertions are at risk in the provided

companies; second part suggests the appropriate substantive audit procedures to minimize

those risks; and the last part sheds light on the responsibilities of the auditors regarding the

key audit matters.

Computing Solutions

Requirement a: Audit Assertions

Valuation and Allocation – This is a crucial assertion associated with inventory which helps

in confirming the value is appropriate in which the company has valued, recorded and

disclosed. It is visible in Computing Solutions that there is 26% of sales in 2019 and 19% of

sales in 2018 included in the inventory in hand. Moreover, inventory turnover ratio has

decreased to 3.8 from 5.2. All these aspects are the indicators of potential slow moving of

inventory or inventories are outdated. It is also observable that the commencement date of the

government contract is middle of July 2019. For this reason, it will be required to write down

any stock in hand in hand at the end of the year to net realizable value due to the requirement

of the contract (Hazlett and Honig, 2016).

Existence – This particular assertion is used to analyze the aspect that there is existence of

inventory at the end of the financial year that are recorded in different financial reports.

According to the provided case, Computing Solutions has recently moved all of their

inventories from the central warehouse to six regional warehouses. This incident indicates

towards the major potential that there has been lost of certain portion of the inventories in the

lost in transit while transferring to the new regional warehouses. In addition, it is also

possible that there have been certain errors in the physical inventory counting process in the

new warehouses. All these aspects put this assertion at risk (Tung and Deng, 2013).

Requirement b: Substantive Audit Procedures

Valuation and Allocation – For this risk, the first substantive audit procedure for the auditor

is to test the releasable value and lower of cost of the main inventory by comparing the cost

of the inventory with the latest price. After that, it is needed for the auditor checking the

inventories kept for selling to the government after the balance date whether their valuation

has been done in net realizable value or lower of cost. Moreover, it is also required for the

auditor to review the major product line of Computing Solution so that they can determine

whether the inventories have been moving slowly or they have become obsolete. In addition,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE IN AUSTRALIA

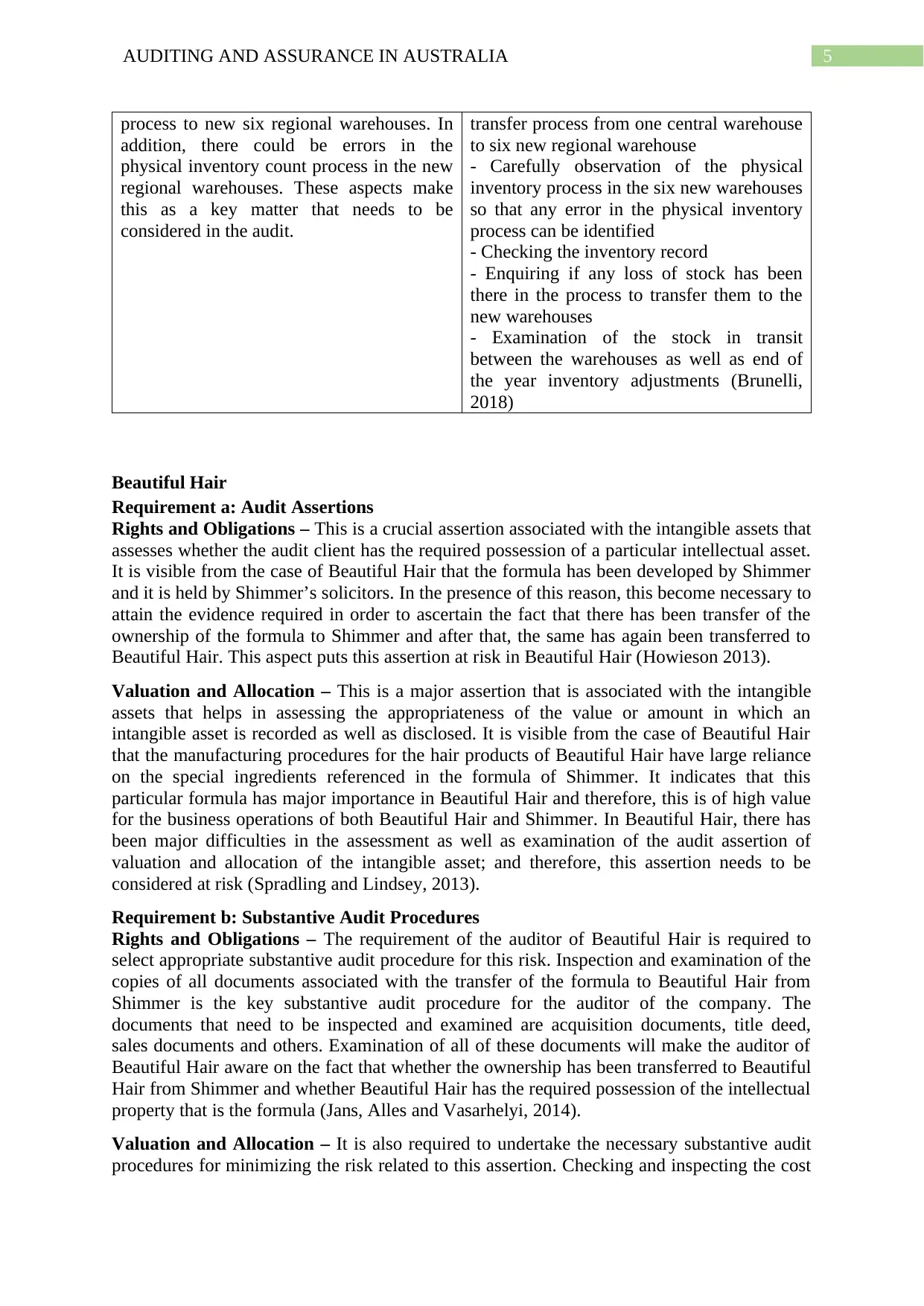

the level of sales for the main products of the company needs to be checked (Knechel and

Salterio, 2016).

Existence – For this risk, attending as well as observing the inventory transfer process from

one central warehouse to six new regional warehouse is one major substantive audit

procedure. In addition, the auditor of Computing Solution is required to carefully observe the

physical inventory process in the six new warehouses so that any error in the physical

inventory process can be identified. Moreover, checking the inventory record is another

major substantive audit procedure that the auditor needs to undertake for checking the

inventory in floor. After that, the auditor must enquire with the management that if any loss

of stock has been there in the process to transfer them to the new warehouses. The last audit

step is to accurately examine the stock in transit between the warehouses as well as end of the

year inventory adjustments with the aim to validate the transactions related to the inventories

(Groomer and Murthy, 2018).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters puts the obligation on the auditor to

comply with certain requirement regarding the key audit matters. The auditors are required to

put specific attention to the areas of the financial statements that are sensitive to the risk of

material misstatement (auasb.gov.au, 2019). At the same time, the auditors are needed to

appropriately assess and examine the used accounting estimates and assumptions in the

financial statements with high level of uncertainty. Apart from this, it is needed for the

auditors to put special consideration to any kind of accounting events that are significant to

the audit of that year. In addition, the auditors are needed to undertake proper communication

of the identified key audit matters with the related parties. These factors are required to be

considered by the auditors of Computing Solutions for the determination of the key audit

matters (Carson, Fargher and Zhang, 2016).

It can be said on the basis of the above requirements that the presence of the risks in

assertions in Computing Solutions can crate material misstatement in the financial statements

of the company. The used assumptions and accounting judgments that the management of the

firm has used for inventory have the potential to be uncertain. At the same time, transferring

the inventories to six new regional warehouses from the central warehouse is the significant

event in the company that can affect the audit (Vik and Walter, 2017). All these aspects make

the assertion risks as the key audit matters of Computing Solutions. These key audit matters

need to be disclosed in the following manner.

Why Significant Substantive Audit Procedures

Valuation and Allocation

There can be slow moving of inventory in

2019 due to the inclusion of previous year’s

sales as well as reduction in the inventory

turnover ratio. For this reason, this is a

major event that needs to be considered in

the audit of the company.

The substantive audit procedures are as

follows:

- Testing the releasable value and lower of

cost of the main inventory by comparing the

cost of the inventory with the latest price

- Checking the inventories kept for selling

to the government to assess whether their

valuation has been done in net realizable

value or lower of cost

- Review the major product line

- Checking the level of sales (Cordoş 2015)

Existence

There can the possibility of theft of

inventory in the inventory transferring

The substantive audit procedures are as

follows:

- Attending and observing the inventory

the level of sales for the main products of the company needs to be checked (Knechel and

Salterio, 2016).

Existence – For this risk, attending as well as observing the inventory transfer process from

one central warehouse to six new regional warehouse is one major substantive audit

procedure. In addition, the auditor of Computing Solution is required to carefully observe the

physical inventory process in the six new warehouses so that any error in the physical

inventory process can be identified. Moreover, checking the inventory record is another

major substantive audit procedure that the auditor needs to undertake for checking the

inventory in floor. After that, the auditor must enquire with the management that if any loss

of stock has been there in the process to transfer them to the new warehouses. The last audit

step is to accurately examine the stock in transit between the warehouses as well as end of the

year inventory adjustments with the aim to validate the transactions related to the inventories

(Groomer and Murthy, 2018).

Requirement c: ASA 701

ASA 701 Communicating Key Audit Matters puts the obligation on the auditor to

comply with certain requirement regarding the key audit matters. The auditors are required to

put specific attention to the areas of the financial statements that are sensitive to the risk of

material misstatement (auasb.gov.au, 2019). At the same time, the auditors are needed to

appropriately assess and examine the used accounting estimates and assumptions in the

financial statements with high level of uncertainty. Apart from this, it is needed for the

auditors to put special consideration to any kind of accounting events that are significant to

the audit of that year. In addition, the auditors are needed to undertake proper communication

of the identified key audit matters with the related parties. These factors are required to be

considered by the auditors of Computing Solutions for the determination of the key audit

matters (Carson, Fargher and Zhang, 2016).

It can be said on the basis of the above requirements that the presence of the risks in

assertions in Computing Solutions can crate material misstatement in the financial statements

of the company. The used assumptions and accounting judgments that the management of the

firm has used for inventory have the potential to be uncertain. At the same time, transferring

the inventories to six new regional warehouses from the central warehouse is the significant

event in the company that can affect the audit (Vik and Walter, 2017). All these aspects make

the assertion risks as the key audit matters of Computing Solutions. These key audit matters

need to be disclosed in the following manner.

Why Significant Substantive Audit Procedures

Valuation and Allocation

There can be slow moving of inventory in

2019 due to the inclusion of previous year’s

sales as well as reduction in the inventory

turnover ratio. For this reason, this is a

major event that needs to be considered in

the audit of the company.

The substantive audit procedures are as

follows:

- Testing the releasable value and lower of

cost of the main inventory by comparing the

cost of the inventory with the latest price

- Checking the inventories kept for selling

to the government to assess whether their

valuation has been done in net realizable

value or lower of cost

- Review the major product line

- Checking the level of sales (Cordoş 2015)

Existence

There can the possibility of theft of

inventory in the inventory transferring

The substantive audit procedures are as

follows:

- Attending and observing the inventory

5AUDITING AND ASSURANCE IN AUSTRALIA

process to new six regional warehouses. In

addition, there could be errors in the

physical inventory count process in the new

regional warehouses. These aspects make

this as a key matter that needs to be

considered in the audit.

transfer process from one central warehouse

to six new regional warehouse

- Carefully observation of the physical

inventory process in the six new warehouses

so that any error in the physical inventory

process can be identified

- Checking the inventory record

- Enquiring if any loss of stock has been

there in the process to transfer them to the

new warehouses

- Examination of the stock in transit

between the warehouses as well as end of

the year inventory adjustments (Brunelli,

2018)

Beautiful Hair

Requirement a: Audit Assertions

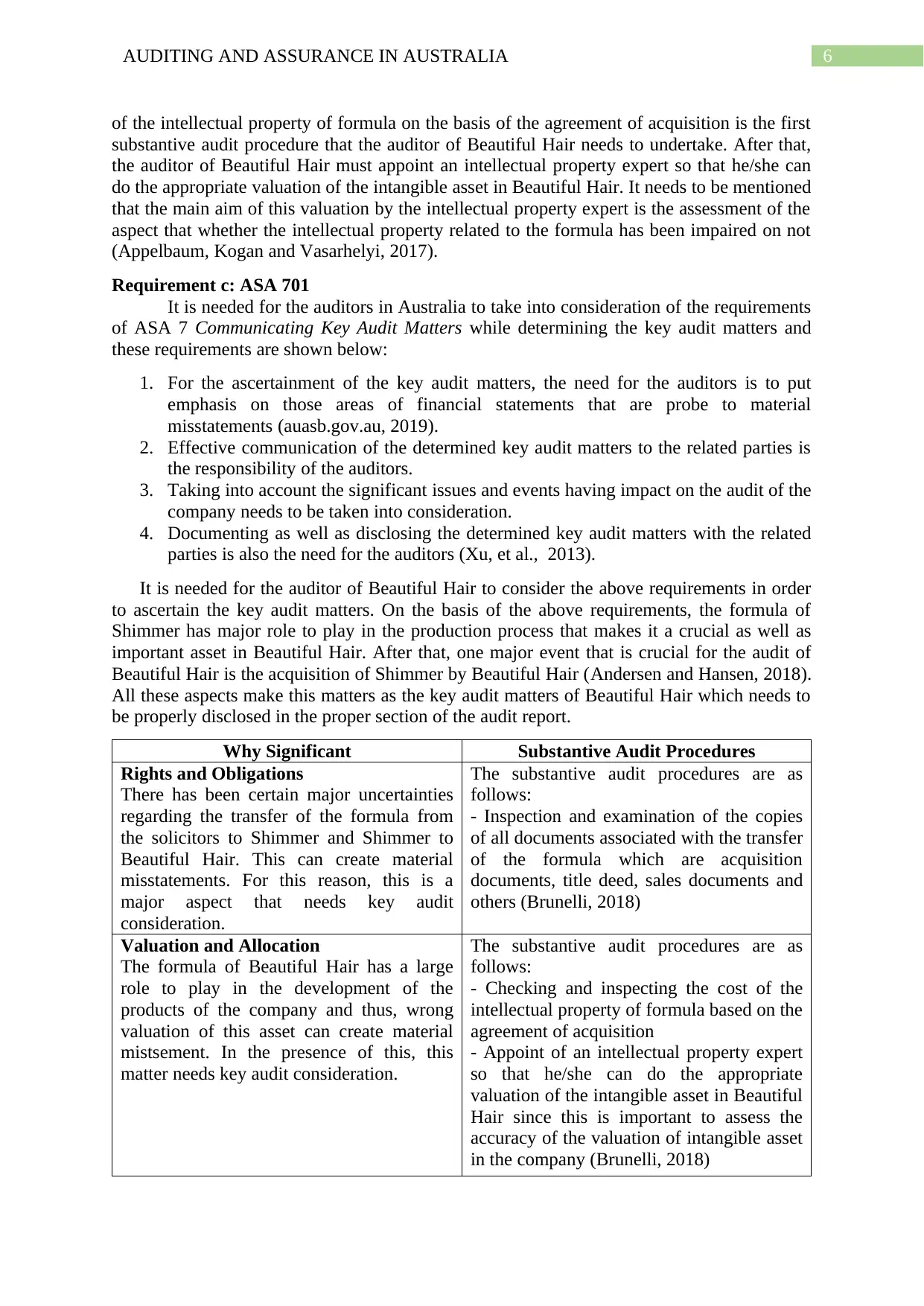

Rights and Obligations – This is a crucial assertion associated with the intangible assets that

assesses whether the audit client has the required possession of a particular intellectual asset.

It is visible from the case of Beautiful Hair that the formula has been developed by Shimmer

and it is held by Shimmer’s solicitors. In the presence of this reason, this become necessary to

attain the evidence required in order to ascertain the fact that there has been transfer of the

ownership of the formula to Shimmer and after that, the same has again been transferred to

Beautiful Hair. This aspect puts this assertion at risk in Beautiful Hair (Howieson 2013).

Valuation and Allocation – This is a major assertion that is associated with the intangible

assets that helps in assessing the appropriateness of the value or amount in which an

intangible asset is recorded as well as disclosed. It is visible from the case of Beautiful Hair

that the manufacturing procedures for the hair products of Beautiful Hair have large reliance

on the special ingredients referenced in the formula of Shimmer. It indicates that this

particular formula has major importance in Beautiful Hair and therefore, this is of high value

for the business operations of both Beautiful Hair and Shimmer. In Beautiful Hair, there has

been major difficulties in the assessment as well as examination of the audit assertion of

valuation and allocation of the intangible asset; and therefore, this assertion needs to be

considered at risk (Spradling and Lindsey, 2013).

Requirement b: Substantive Audit Procedures

Rights and Obligations – The requirement of the auditor of Beautiful Hair is required to

select appropriate substantive audit procedure for this risk. Inspection and examination of the

copies of all documents associated with the transfer of the formula to Beautiful Hair from

Shimmer is the key substantive audit procedure for the auditor of the company. The

documents that need to be inspected and examined are acquisition documents, title deed,

sales documents and others. Examination of all of these documents will make the auditor of

Beautiful Hair aware on the fact that whether the ownership has been transferred to Beautiful

Hair from Shimmer and whether Beautiful Hair has the required possession of the intellectual

property that is the formula (Jans, Alles and Vasarhelyi, 2014).

Valuation and Allocation – It is also required to undertake the necessary substantive audit

procedures for minimizing the risk related to this assertion. Checking and inspecting the cost

process to new six regional warehouses. In

addition, there could be errors in the

physical inventory count process in the new

regional warehouses. These aspects make

this as a key matter that needs to be

considered in the audit.

transfer process from one central warehouse

to six new regional warehouse

- Carefully observation of the physical

inventory process in the six new warehouses

so that any error in the physical inventory

process can be identified

- Checking the inventory record

- Enquiring if any loss of stock has been

there in the process to transfer them to the

new warehouses

- Examination of the stock in transit

between the warehouses as well as end of

the year inventory adjustments (Brunelli,

2018)

Beautiful Hair

Requirement a: Audit Assertions

Rights and Obligations – This is a crucial assertion associated with the intangible assets that

assesses whether the audit client has the required possession of a particular intellectual asset.

It is visible from the case of Beautiful Hair that the formula has been developed by Shimmer

and it is held by Shimmer’s solicitors. In the presence of this reason, this become necessary to

attain the evidence required in order to ascertain the fact that there has been transfer of the

ownership of the formula to Shimmer and after that, the same has again been transferred to

Beautiful Hair. This aspect puts this assertion at risk in Beautiful Hair (Howieson 2013).

Valuation and Allocation – This is a major assertion that is associated with the intangible

assets that helps in assessing the appropriateness of the value or amount in which an

intangible asset is recorded as well as disclosed. It is visible from the case of Beautiful Hair

that the manufacturing procedures for the hair products of Beautiful Hair have large reliance

on the special ingredients referenced in the formula of Shimmer. It indicates that this

particular formula has major importance in Beautiful Hair and therefore, this is of high value

for the business operations of both Beautiful Hair and Shimmer. In Beautiful Hair, there has

been major difficulties in the assessment as well as examination of the audit assertion of

valuation and allocation of the intangible asset; and therefore, this assertion needs to be

considered at risk (Spradling and Lindsey, 2013).

Requirement b: Substantive Audit Procedures

Rights and Obligations – The requirement of the auditor of Beautiful Hair is required to

select appropriate substantive audit procedure for this risk. Inspection and examination of the

copies of all documents associated with the transfer of the formula to Beautiful Hair from

Shimmer is the key substantive audit procedure for the auditor of the company. The

documents that need to be inspected and examined are acquisition documents, title deed,

sales documents and others. Examination of all of these documents will make the auditor of

Beautiful Hair aware on the fact that whether the ownership has been transferred to Beautiful

Hair from Shimmer and whether Beautiful Hair has the required possession of the intellectual

property that is the formula (Jans, Alles and Vasarhelyi, 2014).

Valuation and Allocation – It is also required to undertake the necessary substantive audit

procedures for minimizing the risk related to this assertion. Checking and inspecting the cost

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE IN AUSTRALIA

of the intellectual property of formula on the basis of the agreement of acquisition is the first

substantive audit procedure that the auditor of Beautiful Hair needs to undertake. After that,

the auditor of Beautiful Hair must appoint an intellectual property expert so that he/she can

do the appropriate valuation of the intangible asset in Beautiful Hair. It needs to be mentioned

that the main aim of this valuation by the intellectual property expert is the assessment of the

aspect that whether the intellectual property related to the formula has been impaired on not

(Appelbaum, Kogan and Vasarhelyi, 2017).

Requirement c: ASA 701

It is needed for the auditors in Australia to take into consideration of the requirements

of ASA 7 Communicating Key Audit Matters while determining the key audit matters and

these requirements are shown below:

1. For the ascertainment of the key audit matters, the need for the auditors is to put

emphasis on those areas of financial statements that are probe to material

misstatements (auasb.gov.au, 2019).

2. Effective communication of the determined key audit matters to the related parties is

the responsibility of the auditors.

3. Taking into account the significant issues and events having impact on the audit of the

company needs to be taken into consideration.

4. Documenting as well as disclosing the determined key audit matters with the related

parties is also the need for the auditors (Xu, et al., 2013).

It is needed for the auditor of Beautiful Hair to consider the above requirements in order

to ascertain the key audit matters. On the basis of the above requirements, the formula of

Shimmer has major role to play in the production process that makes it a crucial as well as

important asset in Beautiful Hair. After that, one major event that is crucial for the audit of

Beautiful Hair is the acquisition of Shimmer by Beautiful Hair (Andersen and Hansen, 2018).

All these aspects make this matters as the key audit matters of Beautiful Hair which needs to

be properly disclosed in the proper section of the audit report.

Why Significant Substantive Audit Procedures

Rights and Obligations

There has been certain major uncertainties

regarding the transfer of the formula from

the solicitors to Shimmer and Shimmer to

Beautiful Hair. This can create material

misstatements. For this reason, this is a

major aspect that needs key audit

consideration.

The substantive audit procedures are as

follows:

- Inspection and examination of the copies

of all documents associated with the transfer

of the formula which are acquisition

documents, title deed, sales documents and

others (Brunelli, 2018)

Valuation and Allocation

The formula of Beautiful Hair has a large

role to play in the development of the

products of the company and thus, wrong

valuation of this asset can create material

mistsement. In the presence of this, this

matter needs key audit consideration.

The substantive audit procedures are as

follows:

- Checking and inspecting the cost of the

intellectual property of formula based on the

agreement of acquisition

- Appoint of an intellectual property expert

so that he/she can do the appropriate

valuation of the intangible asset in Beautiful

Hair since this is important to assess the

accuracy of the valuation of intangible asset

in the company (Brunelli, 2018)

of the intellectual property of formula on the basis of the agreement of acquisition is the first

substantive audit procedure that the auditor of Beautiful Hair needs to undertake. After that,

the auditor of Beautiful Hair must appoint an intellectual property expert so that he/she can

do the appropriate valuation of the intangible asset in Beautiful Hair. It needs to be mentioned

that the main aim of this valuation by the intellectual property expert is the assessment of the

aspect that whether the intellectual property related to the formula has been impaired on not

(Appelbaum, Kogan and Vasarhelyi, 2017).

Requirement c: ASA 701

It is needed for the auditors in Australia to take into consideration of the requirements

of ASA 7 Communicating Key Audit Matters while determining the key audit matters and

these requirements are shown below:

1. For the ascertainment of the key audit matters, the need for the auditors is to put

emphasis on those areas of financial statements that are probe to material

misstatements (auasb.gov.au, 2019).

2. Effective communication of the determined key audit matters to the related parties is

the responsibility of the auditors.

3. Taking into account the significant issues and events having impact on the audit of the

company needs to be taken into consideration.

4. Documenting as well as disclosing the determined key audit matters with the related

parties is also the need for the auditors (Xu, et al., 2013).

It is needed for the auditor of Beautiful Hair to consider the above requirements in order

to ascertain the key audit matters. On the basis of the above requirements, the formula of

Shimmer has major role to play in the production process that makes it a crucial as well as

important asset in Beautiful Hair. After that, one major event that is crucial for the audit of

Beautiful Hair is the acquisition of Shimmer by Beautiful Hair (Andersen and Hansen, 2018).

All these aspects make this matters as the key audit matters of Beautiful Hair which needs to

be properly disclosed in the proper section of the audit report.

Why Significant Substantive Audit Procedures

Rights and Obligations

There has been certain major uncertainties

regarding the transfer of the formula from

the solicitors to Shimmer and Shimmer to

Beautiful Hair. This can create material

misstatements. For this reason, this is a

major aspect that needs key audit

consideration.

The substantive audit procedures are as

follows:

- Inspection and examination of the copies

of all documents associated with the transfer

of the formula which are acquisition

documents, title deed, sales documents and

others (Brunelli, 2018)

Valuation and Allocation

The formula of Beautiful Hair has a large

role to play in the development of the

products of the company and thus, wrong

valuation of this asset can create material

mistsement. In the presence of this, this

matter needs key audit consideration.

The substantive audit procedures are as

follows:

- Checking and inspecting the cost of the

intellectual property of formula based on the

agreement of acquisition

- Appoint of an intellectual property expert

so that he/she can do the appropriate

valuation of the intangible asset in Beautiful

Hair since this is important to assess the

accuracy of the valuation of intangible asset

in the company (Brunelli, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE IN AUSTRALIA

Conclusion

It can be seen from the above discussion that determination of the key assertions at

risk is considered as one of the major responsibilities of the auditors since it puts the

obligation on them to design the appropriate substantive audit procedures to minimize those

risks. The above discussion indicates that the assertions at risks are largely dependent on the

nature of the assets, liabilities and transactions. For example, the related assertions at risk in

case of inventories are valuation and allocation and existence; but the relevant assertions at

risk in case of intellectual assets are right and obligation and valuation and allocation. At the

same time, the above discussion also shows that the selection of the substbtive audit

procedures is dependent on the nature of the assertions at risk. For example, it is required to

test the valuation mechanism in case of inventories when the requirement is to test the selling

or transfer related documents in case of the intellectual assets. Another crucial aspect is that

the auditors are needed to comply with the principles and requirements of ASA 701

Communicating Key Audit Matters in order to ascertain the fact that whether the assertions at

risk are the key audit matters or not. Lastly, they are also needed to disclose these key audit

matters in the proper manner in the appropriate section of the audit report.

Conclusion

It can be seen from the above discussion that determination of the key assertions at

risk is considered as one of the major responsibilities of the auditors since it puts the

obligation on them to design the appropriate substantive audit procedures to minimize those

risks. The above discussion indicates that the assertions at risks are largely dependent on the

nature of the assets, liabilities and transactions. For example, the related assertions at risk in

case of inventories are valuation and allocation and existence; but the relevant assertions at

risk in case of intellectual assets are right and obligation and valuation and allocation. At the

same time, the above discussion also shows that the selection of the substbtive audit

procedures is dependent on the nature of the assertions at risk. For example, it is required to

test the valuation mechanism in case of inventories when the requirement is to test the selling

or transfer related documents in case of the intellectual assets. Another crucial aspect is that

the auditors are needed to comply with the principles and requirements of ASA 701

Communicating Key Audit Matters in order to ascertain the fact that whether the assertions at

risk are the key audit matters or not. Lastly, they are also needed to disclose these key audit

matters in the proper manner in the appropriate section of the audit report.

8AUDITING AND ASSURANCE IN AUSTRALIA

References

Andersen, J. and Hansen, N.B., 2018. Key Audit Matters: En undersøkelse av norske

foretak (Master's thesis, Handelshøyskolen BI).

Appelbaum, D., Kogan, A. and Vasarhelyi, M.A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), pp.1-27.

Auasb.gov.au. 2019. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed 15 Sep. 2019].

Brunelli, S., 2018. The Firm’Going Concern in the Contemporary Era. In Audit Reporting for

Going Concern Uncertainty (pp. 1-25). Springer, Cham.

Brunelli, S., 2018. Audit Reporting for Going Concern Uncertainty: Global Trends and the

Case Study of Italy. Springer.

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Cordoş, G.S., 2015. Implications of the current exposure draft on audit

reporting. Management Intercultural, (33), pp.61-70.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hazlett, T.W. and Honig, M., 2016. Valuing spectrum allocations. Mich. Telecomm. & Tech.

L. Rev., 23, p.45.

Houqe, M.N., Ahmed, K. and van Zijl, T., 2017. Audit quality, earnings management, and

cost of equity capital: evidence from India. International Journal of Auditing, 21(2), pp.177-

189.

Howieson, B., 2013. Quis auditoret ipsos auditores? Can auditors be trusted?. Australian

Accounting Review, 23(4), pp.295-306.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Johnstone, K., Gramling, A. and Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Spradling, L.S. and Lindsey, S.W., Thomson Reuters Global Resources ULC, 2013. Method

and system for auditing internal controls. U.S. Patent 8,504,452.

Tung, C.T. and Deng, P.S., 2013. Improved solution for inventory model with defective

goods. Applied Mathematical Modelling, 37(7), pp.5574-5579.

Vik, C. and Walter, M.C., 2017. The reporting practices of key audit matters in the big five

audit firms in Norway (Master's thesis, BI Norwegian Business School).

References

Andersen, J. and Hansen, N.B., 2018. Key Audit Matters: En undersøkelse av norske

foretak (Master's thesis, Handelshøyskolen BI).

Appelbaum, D., Kogan, A. and Vasarhelyi, M.A., 2017. Big Data and analytics in the modern

audit engagement: Research needs. Auditing: A Journal of Practice & Theory, 36(4), pp.1-27.

Auasb.gov.au. 2019. Auditing Standard ASA 701 Communicating Key Audit Matters in the

Independent Auditor’s Report. [online] Available at:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_Compiled_2019-FRL.pdf

[Accessed 15 Sep. 2019].

Brunelli, S., 2018. The Firm’Going Concern in the Contemporary Era. In Audit Reporting for

Going Concern Uncertainty (pp. 1-25). Springer, Cham.

Brunelli, S., 2018. Audit Reporting for Going Concern Uncertainty: Global Trends and the

Case Study of Italy. Springer.

Carson, E., Fargher, N. and Zhang, Y., 2016. Trends in auditor reporting in Australia: a

synthesis and opportunities for research. Australian Accounting Review, 26(3), pp.226-242.

Cordoş, G.S., 2015. Implications of the current exposure draft on audit

reporting. Management Intercultural, (33), pp.61-70.

Groomer, S.M. and Murthy, U.S., 2018. Continuous auditing of database applications: An

embedded audit module approach. In Continuous Auditing: Theory and Application (pp. 105-

124). Emerald Publishing Limited.

Hazlett, T.W. and Honig, M., 2016. Valuing spectrum allocations. Mich. Telecomm. & Tech.

L. Rev., 23, p.45.

Houqe, M.N., Ahmed, K. and van Zijl, T., 2017. Audit quality, earnings management, and

cost of equity capital: evidence from India. International Journal of Auditing, 21(2), pp.177-

189.

Howieson, B., 2013. Quis auditoret ipsos auditores? Can auditors be trusted?. Australian

Accounting Review, 23(4), pp.295-306.

Jans, M., Alles, M.G. and Vasarhelyi, M.A., 2014. A field study on the use of process mining

of event logs as an analytical procedure in auditing. The Accounting Review, 89(5), pp.1751-

1773.

Johnstone, K., Gramling, A. and Rittenberg, L.E., 2013. Auditing: a risk-based approach to

conducting a quality audit. Cengage learning.

Knechel, W.R. and Salterio, S.E., 2016. Auditing: Assurance and risk. Routledge.

Spradling, L.S. and Lindsey, S.W., Thomson Reuters Global Resources ULC, 2013. Method

and system for auditing internal controls. U.S. Patent 8,504,452.

Tung, C.T. and Deng, P.S., 2013. Improved solution for inventory model with defective

goods. Applied Mathematical Modelling, 37(7), pp.5574-5579.

Vik, C. and Walter, M.C., 2017. The reporting practices of key audit matters in the big five

audit firms in Norway (Master's thesis, BI Norwegian Business School).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE IN AUSTRALIA

Xu, Y., Carson, E., Fargher, N. and Jiang, L., 2013. Responses by Australian auditors to the

global financial crisis. Accounting & Finance, 53(1), pp.301-338.

Xu, Y., Carson, E., Fargher, N. and Jiang, L., 2013. Responses by Australian auditors to the

global financial crisis. Accounting & Finance, 53(1), pp.301-338.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.